Download presentation

Presentation is loading. Please wait.

1

Liquidity and Market Efficiency Tarun Chordia (Emory) Richard Roll (UCLA) A. Subrahmanyam (UCLA)

Richard Roll (UCLA) A. Subrahmanyam (UCLA)")

2

Market Efficiency Cannot be instantaneous Cannot be instantaneous CRS (2005) shows that order flows do predict very short-term returns CRS (2005) shows that order flows do predict very short-term returns Efficiency is created in part by arbitrageurs, who are subject to transaction costs Efficiency is created in part by arbitrageurs, who are subject to transaction costs What is the empirical relation between liquidity and market efficiency? What is the empirical relation between liquidity and market efficiency?

3

Liquidity Has generally been related to broader finance by way of a premium in asset returns (Amihud and Mendelson, 1986) Has generally been related to broader finance by way of a premium in asset returns (Amihud and Mendelson, 1986) Also may play a role in moving prices to efficient outcomes—this is what we investigate Also may play a role in moving prices to efficient outcomes—this is what we investigate

Has generally been related to broader finance by way of a premium in asset returns (Amihud and Mendelson, 1986) Also may play a role in moving prices to efficient outcomes—this is what we investigate Also may play a role in moving prices to efficient outcomes—this is what we investigate")

4

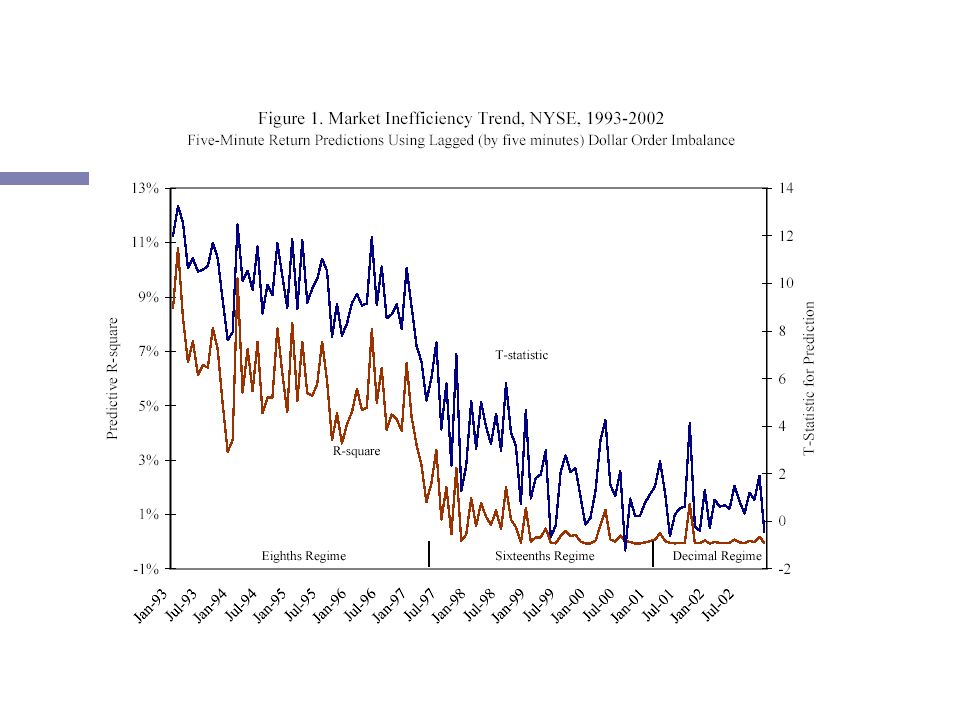

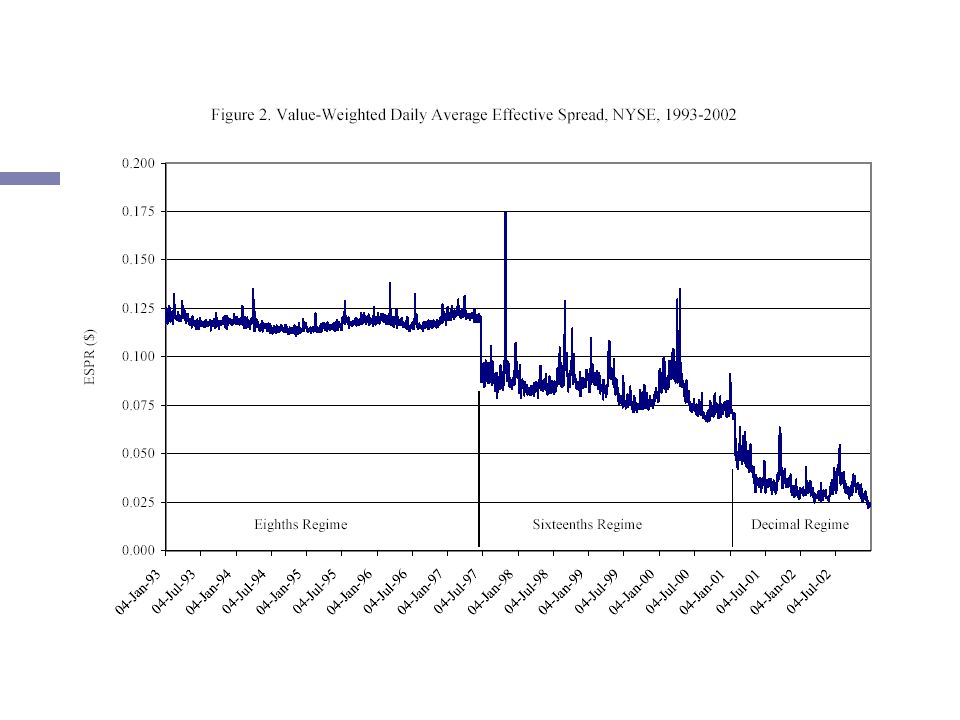

Efficiency over time Secular decrease in bid-ask spreads across the three tick regimes Secular decrease in bid-ask spreads across the three tick regimes How did this affect efficiency? How did this affect efficiency? How does efficiency vary within the day? How does efficiency vary within the day?

5

Interday efficiency measures Open-close and close-open variance ratios (viz. French and Roll, 1984) Open-close and close-open variance ratios (viz. French and Roll, 1984) Daily return autocorrelations Daily return autocorrelations How have these varied across the three tick size regimes corresponding to increased liquidity? How have these varied across the three tick size regimes corresponding to increased liquidity?

Open-close and close-open variance ratios (viz. French and Roll, 1984) Daily return autocorrelations Daily return autocorrelations How have these varied across the three tick size regimes corresponding to increased liquidity. How have these varied across the three tick size regimes corresponding to increased liquidity .")

6

Theoretical setting A security is traded at dates 1 and 2 and pays off + at date 3 (variances v and v ). A security is traded at dates 1 and 2 and pays off + at date 3 (variances v and v ). A demand of z 2 arrives at period 2. A demand of z 2 arrives at period 2. In addition, a fraction kz 1 arrives at period 1 and (1-k)z 1 at period 2 where 0<k<1. In addition, a fraction kz 1 arrives at period 1 and (1-k)z 1 at period 2 where 0<k<1. Variances of z 1 and z 2 both equal v z. Variances of z 1 and z 2 both equal v z.

. A demand of z 2 arrives at period 2. A demand of z 2 arrives at period 2. In addition, a fraction kz 1 arrives at period 1 and (1-k)z 1 at period 2 where 0<k<1. In addition, a fraction kz 1 arrives at period 1 and (1-k)z 1 at period 2 where 0<k<1. Variances of z 1 and z 2 both equal v z. Variances of z 1 and z 2 both equal v z..")

7

Equilibrium Market makers with CARA utility and risk aversion absorb order flows Market makers with CARA utility and risk aversion absorb order flows The mass of market makers at dates 1 and 2 is M and N, with N>M The mass of market makers at dates 1 and 2 is M and N, with N>M Equilibrium is of the Walrasian type Equilibrium is of the Walrasian type Let P i and Q i be the price and order imbalance at date i, respectively Let P i and Q i be the price and order imbalance at date i, respectively

8

Return Predictability

9

Central results If the mass of market makers at date 2 is sufficiently large, lagged imbalances positively predict future returns If the mass of market makers at date 2 is sufficiently large, lagged imbalances positively predict future returns If markets are very liquid (market makers’ risk bearing capacity is very high), such predictability disappears. If markets are very liquid (market makers’ risk bearing capacity is very high), such predictability disappears.

, such predictability disappears..")

10

Data Comprehensive sample of NYSE stocks that traded every day Comprehensive sample of NYSE stocks that traded every day We construct five minute returns for portfolio based on mid-quote returns We construct five minute returns for portfolio based on mid-quote returns If a stock did not trade in period t, it is excluded from the t-1 portfolio If a stock did not trade in period t, it is excluded from the t-1 portfolio Liquidity proxy is the effective spread, averaged across the trading day Liquidity proxy is the effective spread, averaged across the trading day

12

Decline in return predictability R 2 goes to more than 10% to virtually zero R 2 goes to more than 10% to virtually zero T-statistic also drops from around 12 to about 1-2 T-statistic also drops from around 12 to about 1-2 The pattern in imbalance autocorrelations (which are 0.28, 0.21, 0.21, respectively, across the eighth, sixteenth, and decimal regimes) is not sufficient to directly cause this decrease. The pattern in imbalance autocorrelations (which are 0.28, 0.21, 0.21, respectively, across the eighth, sixteenth, and decimal regimes) is not sufficient to directly cause this decrease.

is not sufficient to directly cause this decrease..")

14

Illiquid periods Defined as days where the de-trended effective spread is more than one standard deviation above its mean within each tick size regime Defined as days where the de-trended effective spread is more than one standard deviation above its mean within each tick size regime We use an indicator variable, ILD, which is one on illiquid days We use an indicator variable, ILD, which is one on illiquid days

15

Regressions using illiquidity indicator ILD (dependent variable is mid-quote returns at time t)

")

16

Liquidity and predictability The predictability of returns from lagged order flows is greater on more illiquid days The predictability of returns from lagged order flows is greater on more illiquid days The effect is present in every tick regime The effect is present in every tick regime

17

Market efficiency by time of day Since spreads vary by time of day (McInish and Wood, 1992), there is reason to expect a similar pattern in return predictability Since spreads vary by time of day (McInish and Wood, 1992), there is reason to expect a similar pattern in return predictability We define two dummies, morn (9:30- 12), and eve (14:00-16:00) We define two dummies, morn (9:30- 12), and eve (14:00-16:00)

, there is reason to expect a similar pattern in return predictability Since spreads vary by time of day (McInish and Wood, 1992), there is reason to expect a similar pattern in return predictability We define two dummies, morn (9:30- 12), and eve (14:00-16:00) We define two dummies, morn (9:30- 12), and eve (14:00-16:00)")

18

Time-of-day effects

19

Intraday efficiency results The market’s ability to accommodate order flows was smaller during the morning and, to a lesser extent, the evening period within the eighth regime The market’s ability to accommodate order flows was smaller during the morning and, to a lesser extent, the evening period within the eighth regime This effect has declined considerably during the decimal period This effect has declined considerably during the decimal period

20

Interday measures of efficiency We consider open-close and close-open variance ratios, and return autocorrelations We consider open-close and close-open variance ratios, and return autocorrelations French and Roll (1984) show that these are statistically greater than unity French and Roll (1984) show that these are statistically greater than unity They show that this phenomenon is not due to greater public information flows (by analyzing business day closures) and argue that it may be due to microstructure effects, mispricing, or private information trading They show that this phenomenon is not due to greater public information flows (by analyzing business day closures) and argue that it may be due to microstructure effects, mispricing, or private information trading How do these quantities change across the three tick regimes? How do these quantities change across the three tick regimes?

21

Daily variance ratios and autocorrelations

22

Interpretation The evidence is that variance ratios have increased but autocorrelations appear to have declined The evidence is that variance ratios have increased but autocorrelations appear to have declined We use mid-quote returns, so bid-ask bounce is not an issue We use mid-quote returns, so bid-ask bounce is not an issue If mispricing were driving the increase in variance ratios across time, autocorrelations should have increased as the tick size decreased; but there is no evidence of this. If mispricing were driving the increase in variance ratios across time, autocorrelations should have increased as the tick size decreased; but there is no evidence of this. Consequently, the evidence is consistent with private information being more effectively incorporated into prices in the lower tick regimes, especially for smaller firms. Consequently, the evidence is consistent with private information being more effectively incorporated into prices in the lower tick regimes, especially for smaller firms.

23

Conclusions The extent of return predictability from order flows (an inverse measure of market efficiency) has decreased over time and also is higher on illiquid days. The extent of return predictability from order flows (an inverse measure of market efficiency) has decreased over time and also is higher on illiquid days. Variation in efficiency by time of day has diminished following decimalization Variation in efficiency by time of day has diminished following decimalization Variance ratios have increased whereas autocorrelations have decreased in recent years, suggesting an increase in private information being incorporated into prices following decimalization. Variance ratios have increased whereas autocorrelations have decreased in recent years, suggesting an increase in private information being incorporated into prices following decimalization.

has decreased over time and also is higher on illiquid days. Variation in efficiency by time of day has diminished following decimalization Variation in efficiency by time of day has diminished following decimalization Variance ratios have increased whereas autocorrelations have decreased in recent years, suggesting an increase in private information being incorporated into prices following decimalization. Variance ratios have increased whereas autocorrelations have decreased in recent years, suggesting an increase in private information being incorporated into prices following decimalization..")

Similar presentations

>")

>")