Download presentation

Presentation is loading. Please wait.

1

1 2 Analyzing Transactions

2

2 1. Describe the characteristics of an account and record transactions using a chart of accounts and journal. 2. Describe and illustrate the posting of journal entries to accounts. 3. Prepare an unadjusted trial balance and explain how it can be used to discover errors. 4. Discover and correct errors in recording transactions. After studying this chapter, you should be able to:

3

3 2-1 Describe the characteristics of an account and record transactions using a chart of accounts and journal. Objective 1

4

4 Accounting systems are designed to show the increases and decreases in each financial statement item as a separate record. This record is called an account. 2-1

5

5 5 The T account has a title. Title 2-1 The T Account

6

6 6 The left side of the account is called the debit side. Title Debit 2-1

7

7 The right side of the account is called the credit side. Title DebitCredit 2-1 7

8

8 Title DebitCredit Amounts entered on the left side are debits. 2-1 8

9

9 Title DebitCredit Amounts entered on the right side are credits. 2-1 9

10

10 Cash (a)25,000(b)20,000 (d)7,500(e)3,650 (f)950 (h)2,000 Balance5,900 Balance of the account 2-1 10 (In Rp 000)

25,000(b)20,000 (d)7,500(e)3,650 (f)950 (h)2,000 Balance5,900 Balance of the account (In Rp 000)")

11

11 A group of accounts for a business entity is called a ledger. 2-1

12

12 A list of the accounts in a ledger is called a chart of accounts. 2-1

13

13 Assets are resources owned by the business entity. Cash Supplies Prepaid expenses Buildings 2-1

14

14 Liabilities are debts owed to outsiders (creditors). Accounts payable Notes payable Wages payable 2-1

15

15 Owner’s equity is the owner’s right to the assets of the business. A drawing account represents the amount of withdrawals by the owner. 2-1

16

16 Revenues are increases in owner’s equity as a result of selling services or products to customers. Fees earned Commission revenue Rent revenue 2-1

17

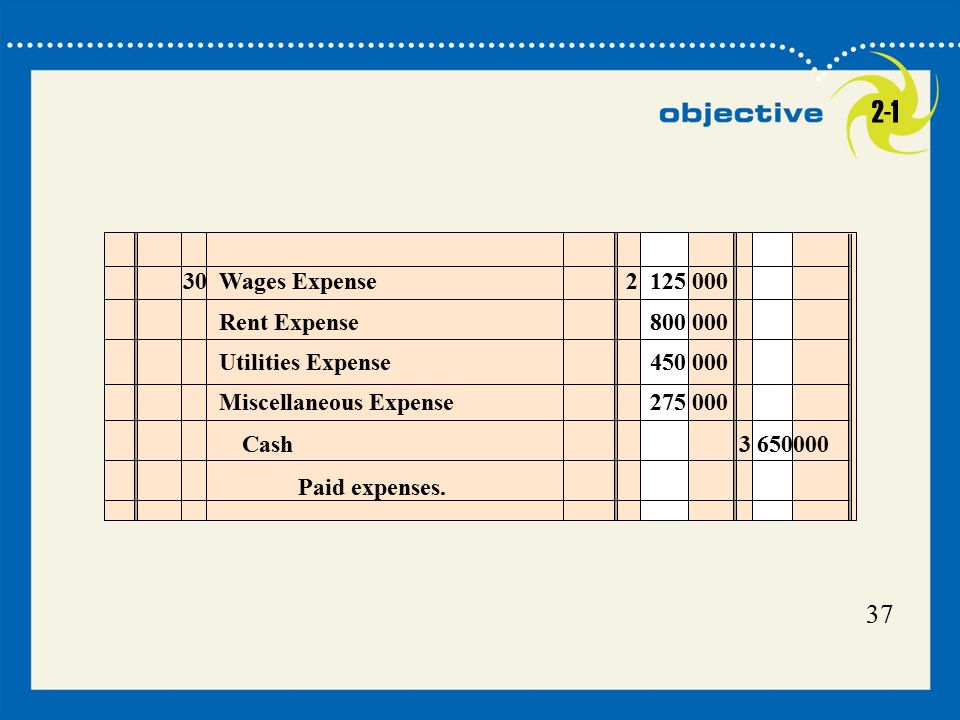

17 The using up of assets or consuming services in the process of generating revenues results in expenses. Wages expense Rent expense Miscellaneous expense 2-1

18

18 Every transaction affects at least two accounts. 2-1

19

19 This transaction is initially entered in a record called a journal. The process of recording a transaction in the journal is called journalizing. Journalizing 2-1

20

20 Journalizing requires the following steps: 1.Record the date. If this is the first entry on the page, the year is inserted above the month. As long as the month does not change, the rest of the journal entries on the require on the day be recorded. 2.The title of the account debited is listed in the Description column. (Continued) 2-1

2-1.")

21

21 3.Enter the amount in the Debit column. 4.Record the credit account in the Description column. 5.Enter the amount in the Credit column. Watch these steps take place as the entry to record Chris Clark’s deposit is presented in the next slide. 2-1

22

22 (a)On November 1, Cita Cinta opens a new business and deposits Rp. 25,000,000 in a bank account in the name of SolusiNet. Balance Sheet Accounts 2-1 @solusinet

23

23 JOURNAL DateDescription Debit Credit Page 1 12341234 Nov.1 2007 Cash25 000 000 Cita Cinta, Capital25 000 000 Invested cash in SolusiNet. 2-1 P.R.

24

24 The effect of this entry is shown in the accounts of SolusiNet as follows: Cash Nov. 125,000 Cita Cinta, Capital 2-1 (In Rp 000)

.")

25

25 (b)On November 5, SolusiNet bought land for Rp 20,000,000 paying cash. 2-1 @solusinet

On November 5, SolusiNet bought land for Rp 20,000,000 paying cash.")

26

26 5Land20 000 000 Cash20 000 000 Purchased land for building site. 2-1

27

27 ( c)On November 10, SolusiNet purchased supplies on account for Rp1,350,000 2-1 @solusinet

On November 10, SolusiNet purchased supplies on account for Rp1,350,000")

28

28 10Supplies1 350 000 Accounts Payable1 350 000 Purchased supplies on account. 2-1

29

29 (f)On November 30, SolusiNet paid creditors on account, Rp. 950,000 2-1 @solusinet

On November 30, SolusiNet paid creditors on account, Rp. 950,000")

30

30 30Accounts Payable950 000 Cash950 000 Paid creditors on account. 2-1 30

31

31 Debits Credits Asset accounts…….Increase (+)Decrease (-) Liability accounts.…Decrease (-)Increase (+) Owner’s equity (capital) accounts…Decrease (-)Increase (+) Balance Sheet Accounts 2-1 31

Decrease (-) Liability accounts.…Decrease (-)Increase (+) Owner’s equity (capital) accounts…Decrease (-)Increase (+) Balance Sheet Accounts")

32

32 Credit for increases (+) Debit for decreases (–) Owner’s Equity Accounts Credit for decreases (–) Debit for increases (+) Asset Accounts Credit for increases (+) Debit for decreases (–) Liability Accounts Balance Sheet Accounts 2-1 32

Debit for decreases (–) Owner’s Equity Accounts Credit for decreases (–) Debit for increases (+) Asset Accounts Credit for increases (+) Debit for decreases (–) Liability Accounts Balance Sheet Accounts")

33

33 Example Exercise 2-1 Prepare a journal entry for the purchase of a truck on June 3 for Rp.42,500, 000 paying Rp.8,500,000 cash and the remainder on account. Follow My Example 2-1 June 3 TruckRp. 42,500,000 Cash 8,500,000 Accounts Payable34,000,000 For Practice: PE 2-1A, PE 2-1B 2-1 33

34

34 (d)On November 18, SolusiNet received fees of Rp7,500,000 from customers for services provided. Income Statement Accounts 2-1 @solusinet

35

35 30Cash7 500 000 Fees Earned7 500 000 Received fees from customers. 2-1 35

36

36 (e)Throughout the month, SolusiNet incurred the following expenses: wages, Rp. 2,125,000; rent Rp. 800,000; utilities, Rp. 450,000; and miscellaneous, Rp.275,000. 2-1 @solusinet

37

37 30Wages Expense2 125 000 Rent Expense800 000 Utilities Expense450 000 Miscellaneous Expense275 000 Cash 3 650000 Paid expenses. 2-1 37

38

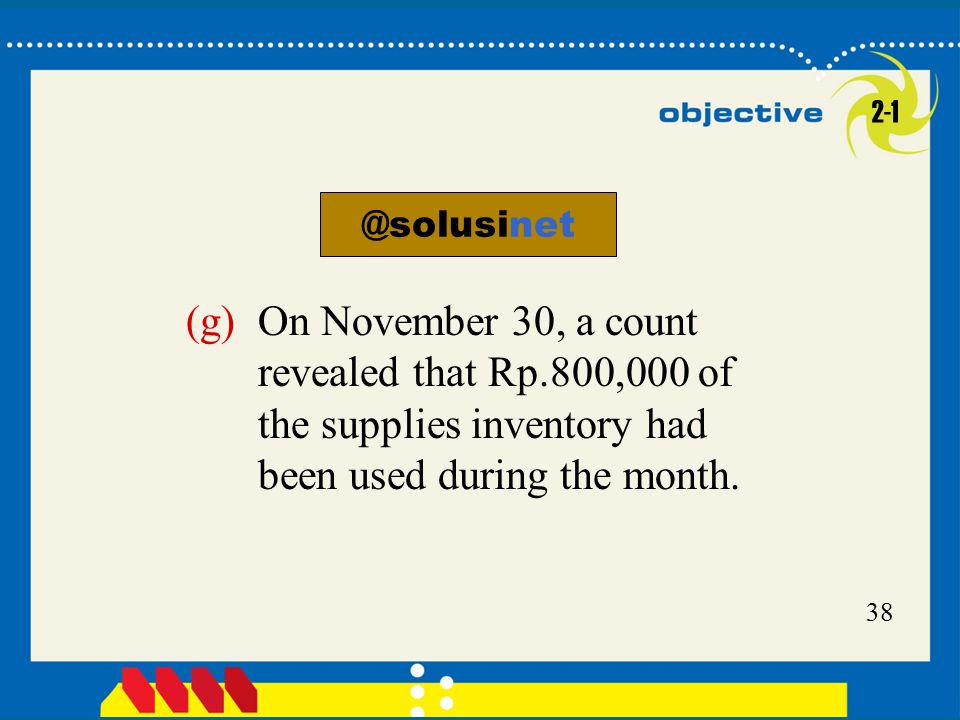

38 (g)On November 30, a count revealed that Rp.800,000 of the supplies inventory had been used during the month. 2-1 @solusinet

39

39 30Supplies Expense 800 000 Supplies 800 000 Supplies used during November. 2-1 39

40

40 Debits Credits Revenue accounts…Decrease (-)Increase (+) Expense accounts…Increase (+)Decrease (-) 2-1 Income Statement Accounts 40

Increase (+) Expense accounts…Increase (+)Decrease (-) 2-1 Income Statement Accounts 40")

41

41 Credit for increases (+) Debit for decreases (–) Revenue Accounts Income Statement Accounts Credit for decreases (–) Debit for increases (+) Expense Accounts Less 2-1 41 Continued

Debit for decreases (–) Revenue Accounts Income Statement Accounts Credit for decreases (–) Debit for increases (+) Expense Accounts Less Continued")

42

42 Equals Net Income (credit > debits) increases owners’ equity (capital) Net Loss (debits > credits) decreases owners’ equity (capital) 2-1 42

increases owners’ equity (capital) Net Loss (debits > credits) decreases owners’ equity (capital)")

43

43 Example Exercise 2-2 Prepare a journal entry on August 7 for the fees earned on account, Rp.115,000,000. Follow My Example 2-2 Aug. 7Accounts Receivable115,000,000 Fees Earned115,000,000 For Practice: PE 2-2A, PE 2-2B 2-1 43

44

44 The owner of a proprietorship may withdraw cash from the business for personal use. Such withdrawals have the effect of decreasing owner’s equity. Drawing Account 2-1

45

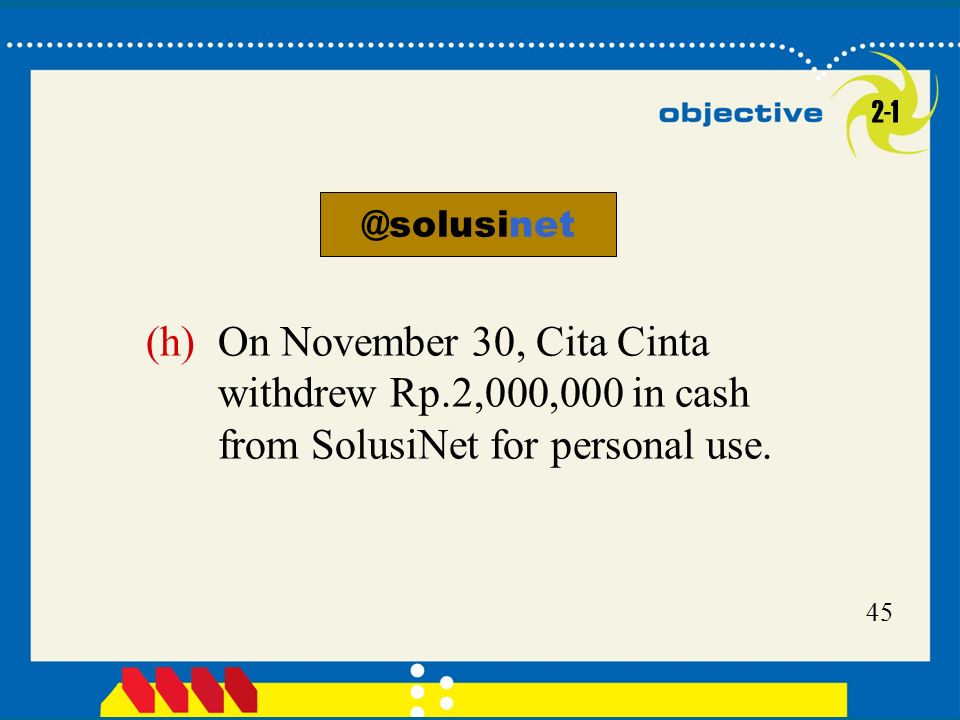

45 (h)On November 30, Cita Cinta withdrew Rp.2,000,000 in cash from SolusiNet for personal use. 2-1 @solusinet

46

46 Cash2 000 000 Cita Cinta withdrew cash for personal use. Nov 30Cita Cinta, Drawing2 000 000 2007 2-1 46

47

47 Example Exercise 2-3 Prepare a journal entry on December 29 for the payment of Rp.12,000,000 to the owner of Smartstaff Consulting Services, Dominique Walsh, for personal use. Follow My Example 2-3 Dec. 29Dominique Walsh, Drawing 12,000,000 Cash12,000,000 For Practice: PE 2-3A, PE 2-3B 2-1 47

48

48 Increase (Normal Bal.) Decreases Balance sheet accounts: AssetDebitCredit LiabilityCreditDebit Owner’s Equity: Capital CreditDebit DrawingDebitCredit Income statement accounts: RevenueCreditDebit ExpenseDebitCredit 2-1 48

Decreases Balance sheet accounts: AssetDebitCredit LiabilityCreditDebit Owner’s Equity: Capital CreditDebit DrawingDebitCredit Income statement accounts: RevenueCreditDebit ExpenseDebitCredit")

49

49 Example Exercise 2-4 State for each account whether it is likely to have (a) debit entries only, (b) credit entries only, or (c) both debit and credit entries. Also, indicate its normal balance. 1.Ambarwati, Drawing 2.Accounts Payable 3.Cash 4.Fees Earned 5.Supplies 6.Utilities Expense 2-1 49

50

50 For Practice: PE 2-4A, PE 2-4B Follow My Example 2-4 1.Debit entries only; normal debit balance 2.Debit and credit entries; normal credit balance 3.Debit and credit entries; normal debit balance 4.Credit entries only; normal credit balance 5.Debit and credit entries; normal debit balance 6.Debit entries only; normal debit balance 2-1 50

51

51 The equality of debits and credits for each transaction is built into the accounting equation: Assets = Liabilities + Owner’s Equity. Because of this double equality, this system is called the double- entry accounting system. 2-1

52

52 2.For each account affected by the transaction, determine whether the account increases or decreases. 3.Determine whether each increase or decrease should be recorded as a debit or a credit. 1.Determine whether an asset, liability, owner’s equity, revenue, expense, or drawing account is affected by the transaction. 2-1 Transaction Analysis Continued

53

53 4.Record the transaction using a journal entry. 5.Periodically post journal entries to the accounts in the ledger. 6.Prepare an unadjusted trial balance at the end of the period. 2-1

54

54 Describe and illustrate the posting of journal entries to the accounts. Objective 2 2-2

55

55 The process of transferring the debits and credits from the journal entries to the accounts is called posting. 2-2

56

56 Dec. 1SolusiNet paid a premium of Rp.2,400,000 for a comprehensive insurance policy covering liability, theft and fire. The policy covers a one-year period. 2-2 @solusinet

57

57 2-2 57 (In Rp. 000)

")

58

58 Dec. 1SolusiNet paid rent for December, Rp.800,000. The company from which SolusiNet is renting its store space requires the payment of rent on the first of each month, rather than at the end of the month. 2-2 @solusinet

59

59 1 Rent Expense52800 000 Cash11800 000 Paid rent for December. 2-2 59

60

60 An alternative approach is to debit Rent Expense for Rp.800,000 on December 1. This avoids having to transfer the balance to an expense account at the end of the month. 2-2

61

61 SolusiNet received an offer from a local retailer to rent the land purchased on November 5. The retailer plans to use the land as a parking lot for its employees and customers. SolusiNet agreed to rent the land to the retailer for three months, with the rent payable in advance. 2-2

62

62 Dec. 1SolusiNet receives Rp. 360,000 for three month’s rent for use of its land beginning December 1. 1 Cash11360 000 Unearned Rent23360 000 Received advance payment for three months’ rent on land. 2-2 62 @solusinet

63

63 Dec. 4SolusiNet purchased office equipment on account from PD.Tunas Jaya. for Rp.1,800,000 4 Office Equipment181 800 000 Accounts Payable211 800 000 Purchased office equipment on account. 2-2 63 @solusinet

64

64 Dec. 6SolusiNet paid Rp.180,000 for a newspaper advertisement. 6 Miscellaneous Expense59180 000 Cash11180 000 Paid for newspaper ad. 2-2 64 @solusinet

65

65 Dec. 11SolusiNet paid creditors Rp.400,000 11 Accounts Payable21400 000 Cash11400 000 Paid creditors on account. 2-2 65 @solusinet

66

66 Dec. 13SolusiNet paid a receptionist and part-time assistant Rp.950,000 for two weeks’ wages. 13 Wages Expense51950 000 Cash11950 000 Paid two weeks’ wages. 2-2 66 @solusinet

67

67 Dec. 16SolusiNet received Rp.3,100,000 from fees earned for the first half of December. 16 Cash113 100 00 Fees Earned413 100 00 Received fees from customers. 2-2 67 @solusinet

68

68 Dec. 16Fees earned on account totaled Rp.1,750,000 for the first half of December. 16 Accounts Receivable121 750 000 Fees Earned411 750 000 Recorded fees earned on account. 2-2 68 @solusinet

69

69 Dec. 20SolusiNet paid Rp.900,000 to Executive Supply Co. on the Rp.1,800,000 debt owed from the December 4 transaction. 20 Accounts Payable21900 000 Cash11900 000 Paid part of amount owed to Executive Supply Co. 2-2 69 @solusinet

70

70 Dec. 21SolusiNet received Rp.650,000 from customers in payment of their accounts. 21 Cash11650 000 Accounts Receivable12650 000 Received fees from customers on account. 2-2 70 @solusinet

71

71 Dec. 23SolusiNet paid Rp 1,450,000 for supplies. 23 Supplies141 450 000 Cash111 450 000 Purchased supplies. 2-2 71 @solusinet

72

72 Dec. 27SolusiNet paid the receptionist and part-time assistant Rp.1,200,000 for two weeks’ wages. 27Wages Expense511 200 000 Cash111 200 000 Paid two weeks’ wages. 2-2 72 @solusinet

73

73 Dec. 31NetSolutions paid Rp.310,000 for telephone charges for the month. 31Utilities Expense54310 000 Cash11310 000 Paid telephone charges. 2-2 73 @solusinet

74

74 Dec. 31SolusiNet paid Rp.225,000 for electric usage for the month. Post. Ref. JOURNAL DateDescriptionDebitCredit Page 1 Dec 31Utilities Expense54225 000 2007 Cash11225 000 Paid for electric usage. 2-2 74 @solusinet

75

75 Dec. 31SolusiNet received Rp.2,870,000 from fees earned for the second half of December. 31Cash112 870 000 Fees Earned412 870 000 Received fees from customers. 2-2 75 @solusinet

76

76 Dec. 31NetSolutions earned Rp.1,120,000 on account for the second half of December. 31Accounts Receivable121 120 000 Fees Earned411 120 000 Recorded fees earned on account. 2-2 76 @solusinet

77

77 Dec. 31Cita Cinta withdrew Rp.2,000,000 for personal use. 31Cita Cinta, Drawing322 000 000 Cash112 000 000 Cita Cinta withdrew cash for personal use. 2-2 77 @solusinet

78

78 Example Exercise 2-5 On March 1, the cash account balance was Rp. 22,350,000. During March, cash receipts totaled Rp.241,880,000 and the March 31 balance was Rp.19,125,000. Determine the cash payments made during March. 2-2 78

79

79 Follow My Example 2-5 Using the following T-account solve for the amount of cash payment (indicated by ? below). Cash Mar. 1 Bal22,350?Cash payments Cash receipts241,880 Mar. 31 Bal.19,125 Rp.19,125 = Rp.22,350 + Rp.241,880 – Cash payments Cash payments = Rp.22,350 + Rp.241,880 –Rp.19,125 = Rp.245,105 For Practice: PE 2-5A, PE 2-5B 2-2 79 In Rp.000

. Cash Mar. 1 Bal22,350 Cash payments Cash receipts241,880 Mar. 31 Bal.19,125 Rp.19,125 = Rp.22,350 + Rp.241,880 – Cash payments Cash payments = Rp.22,350 + Rp.241,880 –Rp.19,125 = Rp.245,105 For Practice: PE 2-5A, PE 2-5B In Rp.000.")

80

80 Prepare an unadjusted trial balance and explain how it can be used to discover errors. 2-3 Objective 3

81

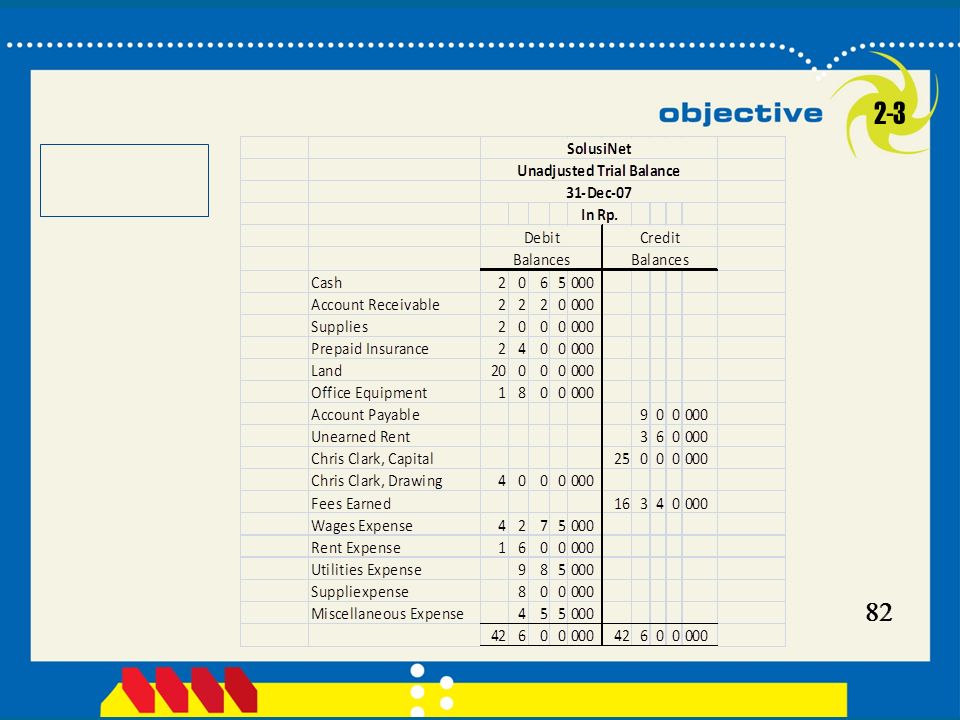

81 The equality of debits and credits in the ledger should be proved at the end of each accounting period by preparing a trial balance. The heading should first list the name of the company, the statement’s title, and the date it is prepared. 2-3

82

82 2-3 82

83

83 Example Exercise 2-6 For each of the following errors, considered individually, indicate whether the error would cause the trial balance totals to be unequal. If the error would cause the trial balance total to be unequal, indicate whether the debit or credit total is higher and by how much. a.Payment of a cash withdrawal of Rp.5,600,000 was journalized and posted as a debit of RP.6,500,000 to Salary Expense and a credit of RP.6,500,000 to Cash. b.A fee of Rp.2,850,000 earned from a client was debited to Accounts Receivable for Rp.2,580,000 and credited to Fees Earned for Rp.2,850,000. c.A payment of Rp.3,500,000 to a creditor was posted as a debit of Rp.3,500,000 to Accounts Payable and a debit of Rp.3,500,000 to Cash. 2-3 83

84

84 Follow My Example 2-6 a.The totals are equal since both the debit and credit entries were journalized and posted for Rp.6,500,000. b.The totals are unequal. The credit total is higher by Rp.270,000 (Rp.2,850,000 – Rp.2,580,000). c.The totals are unequal. The debit total is higher by Rp.7,000,000 (Rp.3,500,000 + Rp.3,500,000). 2-3 For Practice: PE 2-6A, PE 2-6B 84

. c.The totals are unequal. The debit total is higher by Rp.7,000,000 (Rp.3,500,000 + Rp.3,500,000). 2-3 For Practice: PE 2-6A, PE 2-6B 84.")

85

85 Discover and correct errors in recording transactions. 2-4 Objective 4

86

86 A transposition occurs when the order of the digits is changed mistakenly, such as writing Rp.542,000 as Rp.452,000 or Rp.524,000. In a slide, the entire number is mistakenly moved one or more spaces to the right or the left, such as writing RP.542.000 as $54,200. 2-4

87

87 Another type of error is a posting error. Assume that on May 5 a Rp.12,500,000 purchase of office equipment on account was incorrectly journalized and posted as a debit to Supplies and a credit to Accounts Payable for Rp.12,500,000. 2-4

88

88 Entry to Correct Error May 31Office Equipment1812 500 000 Supplies1412 500 000 To correct erroneous debit to Supplies on May 5. See invoice from Bella Office Equipment Company. 2-4 88

89

89 Example Exercise 2-7 a.A withdrawal of Rp.6,000,000 by Roni Ahmad, owner of the business, was recorded as a debit to Office Salaries Expense and a credit to Cash. b.Utilities Expense of Rp.4,500,000 paid for the current month was recorded as a debit to Miscellaneous Expense and a credit to Accounts Payable. The following errors took place in journalizing and posting transactions: Journalize the entries to correct the errors. Omit explanations. 2-4 89

90

90 Follow My Example 2-7 a.Cheri Ramey, Drawing6,000 Office Salaries Expense6,000 b.Accounts Payable4,500 Miscellaneous Expense4,500 Utilities Expense4,500 Cash4,500 Note: The first entry in (b) reverses the incorrect entry, and the second entry records the correct entry. For Practice: PE 2-7A, PE 2-7B 2-4 90 In Rp.000

Similar presentations