Download presentation

Presentation is loading. Please wait.

1

Department Administrator Session #8 – June 25th 2013

2

Agenda Introductions/Update of RFS Update on commitment questions Understanding FRS Header Information Steps taken by RFS to prepare a financial report –FRS vs. Financial Statement –Tri-Council Form 300 Tri-Council – what to do when end date approaching Set up of accounts with Internal Transfer – In-direct costs Next session

3

6/4/2016 Research Financial Services Director Research Financial Services (Dave Reinhart) – 0595-001 Manager, Infrastructure Programs (Lee Bennard) – 0595-002 Financial Officer, Infrastructure Programs (Linda Hoffman) – 0595-003 Administrative Support, Infrastructure Programs – 24 hours per week – (Christa Aljoe) Manager, Tri Council (Asif Momin) – 0595-009 Tri-Council Awards Accountant (Karen Lee) – 0595-010 Manager, Research Grants and Contracts (Other Government and Industry) (Eric Hinse) – 0595-011 Financial Officer, Research Trust Accounts (Susan Ferguson) – 0595-007 Financial Officer, Research Trust Accounts (Vacant) – 0595-005 Manager, Major Research Contracts (Shaun Wilson) – 0595-004 INFRASTRUCTURE PROGRAMS Application budget Award Finalization Account set up Budget input to FRS Compliance review In-kind review Financial Reports Supporting documentation Disbursement of funds Faculty and Dept Administrator training TRI-COUNCIL Budget assistance Budget input to FRS Account set up Compliance review Financial reports Disbursement of funds Transfer letters Faculty and Dept Administrator training OTHER GOV’T AND INDUSTRY Budget assistance Budget input to FRS Account set up Compliance review Invoicing Deposit of cheques Collection of aged receivables Financial reports Supporting documentation Faculty and Dept Administrator training MAJOR RESEARCH CONTRACTS Application budget Award Finalization Account set up Budget input to FRS Compliance review In-kind review Financial Reports Supporting documentation Disbursement of funds Audits Faculty and Dept Administrator training

– Manager, Infrastructure Programs (Lee Bennard) – Financial Officer, Infrastructure Programs (Linda Hoffman) – Administrative Support, Infrastructure Programs – 24 hours per week – (Christa Aljoe) Manager, Tri Council (Asif Momin) – Tri-Council Awards Accountant (Karen Lee) – Manager, Research Grants and Contracts (Other Government and Industry) (Eric Hinse) – Financial Officer, Research Trust Accounts (Susan Ferguson) – Financial Officer, Research Trust Accounts (Vacant) – Manager, Major Research Contracts (Shaun Wilson) – INFRASTRUCTURE PROGRAMS Application budget Award Finalization Account set up Budget input to FRS Compliance review In-kind review Financial Reports Supporting documentation Disbursement of funds Faculty and Dept Administrator training TRI-COUNCIL Budget assistance Budget input to FRS Account set up Compliance review Financial reports Disbursement of funds Transfer letters Faculty and Dept Administrator training OTHER GOV’T AND INDUSTRY Budget assistance Budget input to FRS Account set up Compliance review Invoicing Deposit of cheques Collection of aged receivables Financial reports Supporting documentation Faculty and Dept Administrator training MAJOR RESEARCH CONTRACTS Application budget Award Finalization Account set up Budget input to FRS Compliance review In-kind review Financial Reports Supporting documentation Disbursement of funds Audits Faculty and Dept Administrator training")

4

Understanding Commitments Questions about commitments? Commitments entered as credits Process for clearing commitments when amount paid is less than PO Commitment for support staff (less than full time) Object 61417 – no longer show commitment for salaried student labour

Object – no longer show commitment for salaried student labour.")

5

Understanding Commitments - Discussion I have compiled a list of questions regarding commitments and will bring these forward to the managers of Financial Services. These questions will then be answered and communicated to the group at our next session. Please follow up with me if you have additional questions

6

Understanding Commitments Questions raised How do you end up with a credit (negative) commitment (PO and payroll)? What is the process for clearing commitments when amount paid is less than PO? Can this be done more frequently than annually? Why do commitments for 35 hours appear when people who work less than a full week?

7

Understanding Commitments Questions raised Student labour (Object 61417, 61445, 61433) no longer shows a commitment for salaried student labour. Why can we not show the commitment? If we can not show an accurate commitment value for hourly commitments, is it possible to show the names of the individuals that are being paid from the account?

8

Understanding Commitments Questions raised Who should be contacted when a commitment is incorrect (PO)? How do we convince researchers to use FRS when the commitments are not accurate? Why do we have to keep a separate file to determine the true account balance and remaining funds?

9

Oracle Legend The following two slides show the different attributes included on the setup of an account and the different options for each attribute. Please refer to legend as necessary

10

Oracle Attribute Legend

11

11 MandatoryUnit Number6 Digits Department Number – last 2 digits must be 00 (i.e. 023000) 12OptionalAmount Awarded10 CharactersMaximum 10 digit number 13MandatoryStart Datedd-mm-yyStart of Grant/Contract Term 14OptionalEnd Datedd-mm-yyEnd of Grant/Contact Term 15MandatoryAnniversary DateDrop Down ListLast month reporting period 01 - 12January - December 16MandatoryStatusDrop Down ListOpen (use only) 17MandatoryRestrictionDrop Down ListExternal Restriction Board Restriction (GPA) 18MandatoryInterestDrop Down ListNo for Grants/Contracts (use only) 19MandatoryCategoryDrop Down ListN/A 20OptionalReference Numbers20 Characters Sponsor Reference Number or Sponsor Contract Number 21OptionalProgram Code20 CharactersTri Council – Code from Award Notice 22OptionalGrant ID20 CharactersTri Council – ID from Award Notice 23OptionalCompetition Year20 CharactersTri Council – Year of Competition from Award Notice 24OptionalPIN Number20 Characters Tri Council – Personal Identification Number for each researcher 25OptionalSupporting DocumentationDrop Down List 00None 01All Expenses 02Travel 03Travel & Equipment 04Equipment 26OptionalLast Submitted Report Datedd-mon(th)-year Last Reporting Period Next Report Due Date Next Reporting Period 27OptionalCommentsText 28OptionalE-Mail AddressTextWill be needed for automated grant end reporting 29OptionalEndowment ReportingDrop Down ListUse “No”

12OptionalAmount Awarded10 CharactersMaximum 10 digit number 13MandatoryStart Datedd-mm-yyStart of Grant/Contract Term 14OptionalEnd Datedd-mm-yyEnd of Grant/Contact Term 15MandatoryAnniversary DateDrop Down ListLast month reporting period January - December 16MandatoryStatusDrop Down ListOpen (use only) 17MandatoryRestrictionDrop Down ListExternal Restriction Board Restriction (GPA) 18MandatoryInterestDrop Down ListNo for Grants/Contracts (use only) 19MandatoryCategoryDrop Down ListN/A 20OptionalReference Numbers20 Characters Sponsor Reference Number or Sponsor Contract Number 21OptionalProgram Code20 CharactersTri Council – Code from Award Notice 22OptionalGrant ID20 CharactersTri Council – ID from Award Notice 23OptionalCompetition Year20 CharactersTri Council – Year of Competition from Award Notice 24OptionalPIN Number20 Characters Tri Council – Personal Identification Number for each researcher 25OptionalSupporting DocumentationDrop Down List 00None 01All Expenses 02Travel 03Travel & Equipment 04Equipment 26OptionalLast Submitted Report Datedd-mon(th)-year Last Reporting Period Next Report Due Date Next Reporting Period 27OptionalCommentsText 28Optional AddressTextWill be needed for automated grant end reporting 29OptionalEndowment ReportingDrop Down ListUse No .")

12

Preparing a financial report We prepare our financial reports in a similar fashion: Review FRS, Check File, Contact PI/ADM. Additional Sponsor Requirements: –Transaction listing for the period; –Backup documentation (invoices); and –Tax rebate reports

; and –Tax rebate reports.")

13

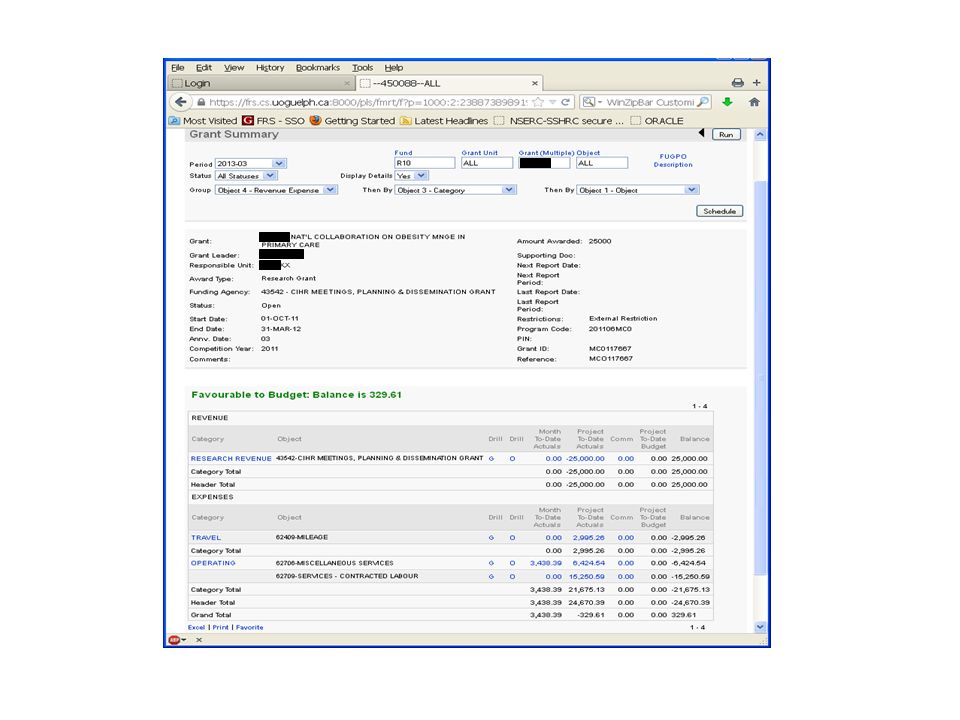

FRS vs. Financial Report Why doesn’t FRS match to the financial statement? Adjusting journal entries: Timing differences; Ineligible expenses; or Overhead;

14

FRS vs. Financial Statement Example: The $5K will have to be adjusted on the next statement! Total Financial Report (March 31/13)$120,000 FRS (March 31/13)$100,000 Difference(20,000) Overhead – 15% eligible expenses15,000 Disallowed expense prior period - $5K 5,000 Reconciliation$0

$120,000 FRS (March 31/13)$100,000 Difference(20,000) Overhead – 15% eligible expenses15,000 Disallowed expense prior period - $5K 5,000 Reconciliation$0.")

15

Thanks! We appreciate your help – you are paramount! Questions?

16

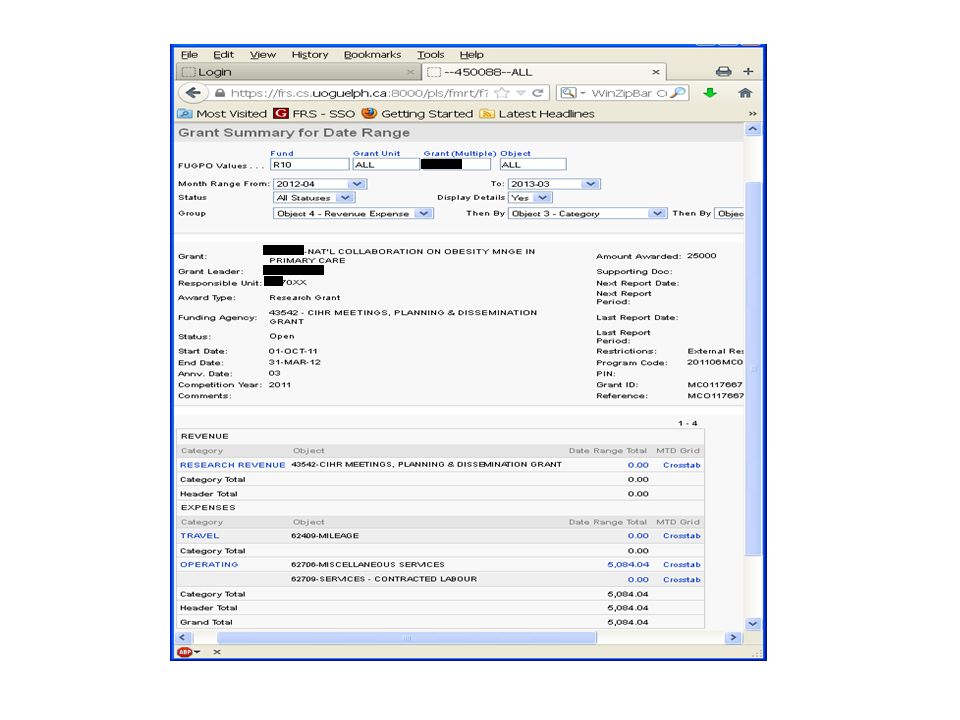

Tri-Council F300 F300 for the previous period FRS – Grant Summary as of the current report end date ( e.g. 31-Mar- 2013 ) FRS – Grant Summary for Data Range ( e.g. 01-Apr-2012 to 31-Mar-2013 ). FRS – Salary Summary Check the eligibility of expenses by looking at the object code level

FRS – Grant Summary for Data Range ( e.g. 01-Apr-2012 to 31-Mar-2013 ). FRS – Salary Summary Check the eligibility of expenses by looking at the object code level.")

17

Tri-Council F300 (conti.) If ineligible expense, we ask researcher and admin to provide more info and/or to move that expense from the grant Ending balance should match with FRS balance – if not – reconcile it with backup Dave sign the F300 followed by the copy sent to researcher for signature F300 is sent to the sponsor

If ineligible expense, we ask researcher and admin to provide more info and/or to move that expense from the grant Ending balance should match with FRS balance – if not – reconcile it with backup Dave sign the F300 followed by the copy sent to researcher for signature F300 is sent to the sponsor")

20

What to do when the grant end date is approaching: Inform the researcher about the end date the grant will not be accessible after the end date If there is any surplus, it will be moved out from the grant All eligible expenses, incurred on or before the end date, should be charged to the grant before end date. If you miss the end date please inform Karen Lee or myself New expenses (i.e. incurred after end date) should not be charged to the grant.

should not be charged to the grant..")

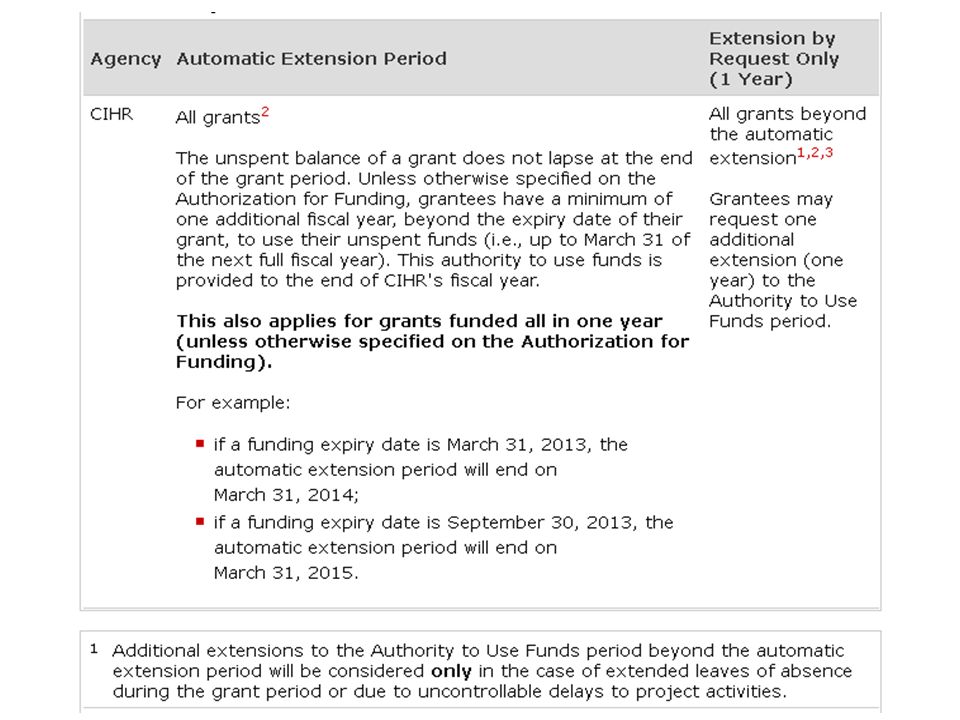

21

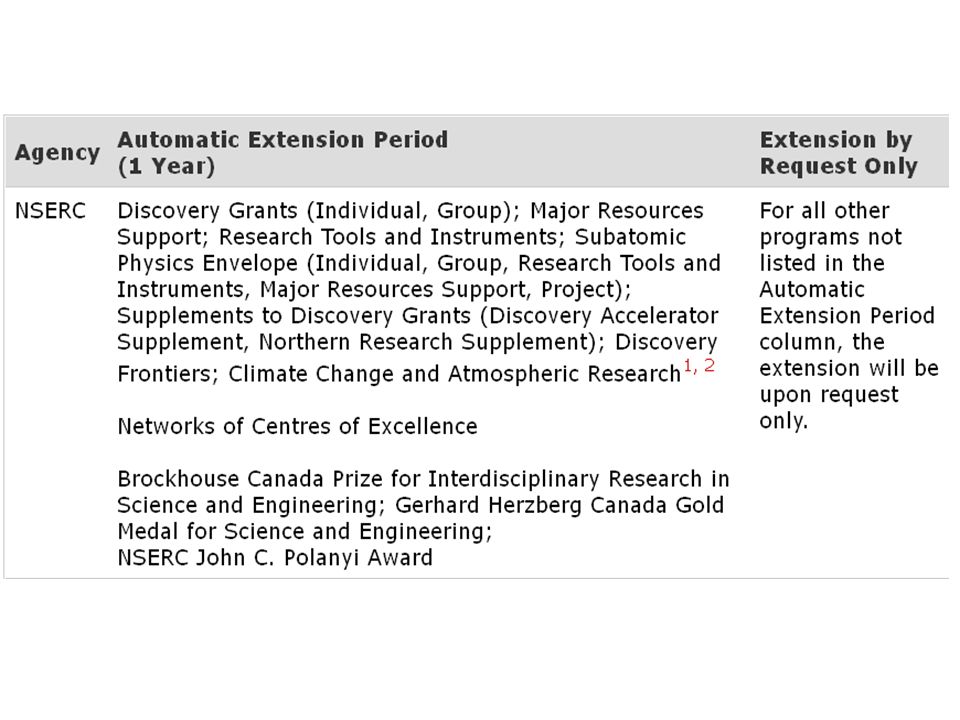

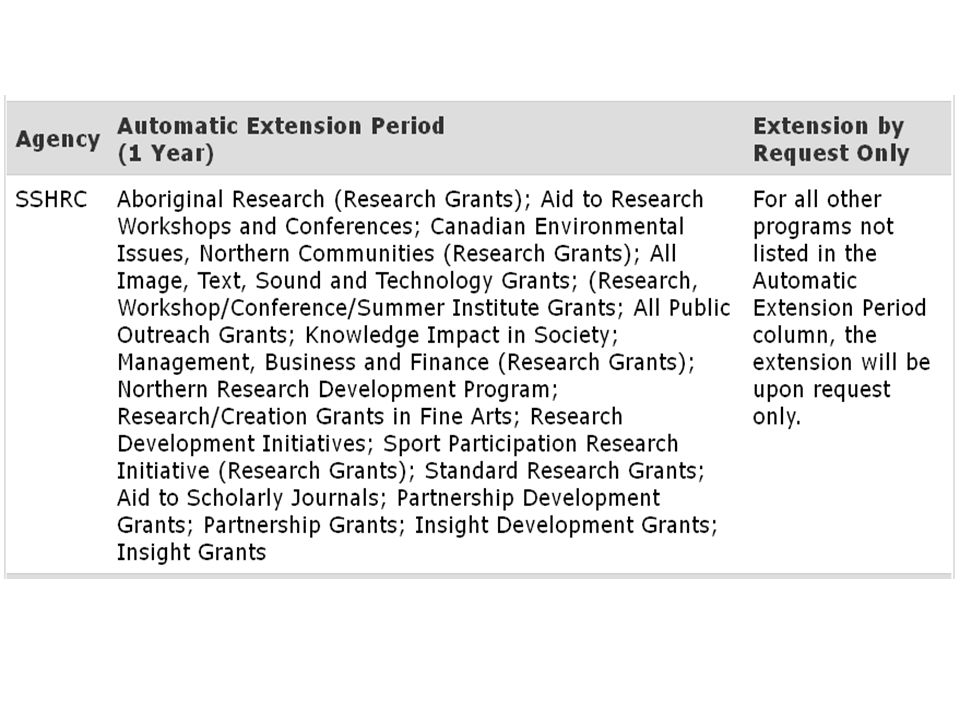

2013 Tri-Agency Financial Administration Guide (TAFAG) http://www.nserc-crsng.gc.ca/Professors- Professeurs/FinancialAdminGuide- GuideAdminFinancier/index_eng.asp Some important information: Roles and Responsibilities of researchers and institution Use of Grant Funds- Eligibility of expenses Extension Period for Use of Funds Beyond a Grant Period

Professeurs/FinancialAdminGuide- GuideAdminFinancier/index_eng.asp Some important information: Roles and Responsibilities of researchers and institution Use of Grant Funds- Eligibility of expenses Extension Period for Use of Funds Beyond a Grant Period")

25

Set up of accounts with Internal Transfers Researcher A from Plant Ag to receive $100K award from AAFC Researcher A wishes to transfer $20K to Researcher B from Biomedical Sciences

26

Set up of accounts with Internal Transfers Account A –Award Amount $100K –Funding Agency - AAFC –Deposit $100K –Comments – Reference Account B and relevant indirect costs per budget from researcher –Revenue Transfer to Account B

27

Set up of accounts with Internal Transfers Account B –Award Amount $20K –Funding Agency - AAFC –Comments – Reference Account A and relevant indirect costs per budget from researcher –Revenue Transfer from Account A

28

Set up of accounts with Internal Transfers RFS, Office of Research will continue to review and look for solution that conveys appropriate information to users regarding award amount and indirect costs RFS will be working with CCS and Budget Office to establish a separate category for Indirect Costs (removing Overhead Charge from Operating category)

")

29

My Grants Tracker RFS will follow up with OAC and CBS to plan additional My Grants Tracker training sessions Please contact Eric Hinse if you would like to arrange training sessions for your department/college

30

Next Session When would you like to meet again? Will plan next meeting for October 2013 –Please forward any agenda items that you may have ENJOY YOUR SUMMER!!!

Similar presentations