Download presentation

Presentation is loading. Please wait.

1

Trade Policy Responses to the Crisis: Implications for the WTO and the Doha Round Bernard Hoekman International Trade Department World Bank Beirut, November 12, 2009

2

The context Economic situation under stress – Global GDP to decline by -2.9% in 2009 – Net private capital flows to developing countries down US$800 billion 2007 peak – Global trade volumes to fall by some 10% in 2009 – Global unemployment up by some 60 million To date, limited recourse to protectionism Many voices arguing that Doha will generate trivial market access gains at best

3

Doha: a quixotic quest? To the contrary

4

Doha matters more now Protectionist pressures should not be ignored or system taken for granted – Unemployment continues to rise, while exports recovering – recipe for more, not less pressure – Substantial scope to raise tariffs/support industries Developing countries hit hard – Doha is an opportunity to help them exit crisis faster – In part by pursuit of trade facilitation and greater South-South trade Can help reduce OECD fiscal outlays (agriculture) Signaling effect: multilateral cooperation at work

Signaling effect: multilateral cooperation at work")

5

WTO is mostly about policy bindings Negotiating coin = policy commitments: – Tariff bindings; specific commitments in services – Policy disciplines (rules of the game) Both reduce the size of potential negative spillover effects of national policies – During crisis responses and after – when fiscal stimulus needs to be reduced Reducing applied trade policies (liberalization) is just one element of WTO negotiations – As it was under the GATT: lock-in and MFN extension of unilateral reforms, in part driven by steady EC expansion

Both reduce the size of potential negative spillover effects of national policies – During crisis responses and after – when fiscal stimulus needs to be reduced Reducing applied trade policies (liberalization) is just one element of WTO negotiations – As it was under the GATT: lock-in and MFN extension of unilateral reforms, in part driven by steady EC expansion")

6

What’s on the table? 1.More secure market access in goods 2.New or stronger disciplines on policies that create negative spillovers 3.Some new market opening in agriculture and manufacturing 4.Somewhat greater security of access in services 5.Initiatives to expand export opportunities of LDCs and low-income countries NB: many other issues

7

1. More secure market access in goods Modalities will substantially lower average bound tariffs and to a lesser extent, applied rates – Bound average in ag. down to 30%; NAMA: 5% – But what matters is that tariff peaks come down most—and these are the most costly/constraining Ban on agricultural export subsidies Large cuts in maximum permitted ag. subsidies— by 70% in US; 60% in EU—bringing them close to/below applied levels

8

2. Disciplines on policies that create negative spillovers Food policies – Subsidy disciplines not just a market access story – Less insulation of national markets will reduce volatility of world prices; create thicker markets Cotton. Global support up more than twofold from $2.7 billion in 2007/08 to an estimated $5.9 billion in 2008/09 Sustainable development – Fishery policies cost the world economy $50 billion (60% of the landed value of the global catch); EU and US production support > $1bn per year Important for food security & livelihoods of many small developing countries/coastal regions – Tariff reductions on environmental goods – averaging some 10% in low-income countries

; EU and US production support > $1bn per year Important for food security & livelihoods of many small developing countries/coastal regions – Tariff reductions on environmental goods – averaging some 10% in low-income countries.")

9

3. Some new market opening for goods Average farm tariffs confronting developing (OECD) country exporters will drop to 11.5% (12.1%) Tariffs on their exports of manufactures to fall to 2.1% (2.4%) This is significant: focus on the levels not the change at the margin

country exporters will drop to 11.5% (12.1%) Tariffs on their exports of manufactures to fall to 2.1% (2.4%) This is significant: focus on the levels not the change at the margin.")

10

4. Services: somewhat greater security Note: A large ‘offer gap’ remains (factor of 2 on average)

")

11

5. Initiatives to expand exports of low- income countries 97% duty-free, quota free for LDCs – Not as good as 100%, but still worth $1 billion in the US market Trade facilitation – Improving the logistics performance of low income countries to that of middle income countries would increase their trade by more than 50% Aid for trade – Not linked to DDA but closure would strengthen prospects of delivery on Hong Kong commitments, especially given fiscal pressures in OECD

12

The value of the WTO is revealed/rises in bad times Up to mid 2008: “not enough on the table” – Trade was booming; little prospect of backsliding That was then…. – So far so good on protectionist responses – a low level fever But there are policy areas that are not subject to disciplines – and concluding the DDA is a precondition for starting to do so

13

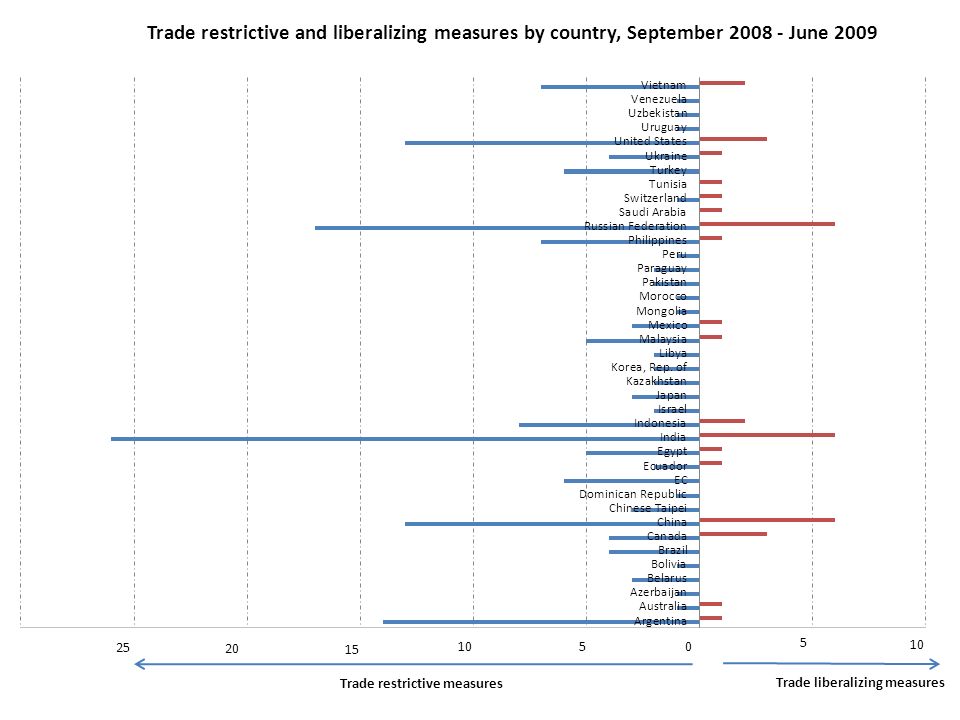

Assessing policy responses to date Lot of action, but no major rise in protection – Focus of many measures – in North and South – is on China A number of countries have also liberalized trade or taken trade facilitation measures Much of the rise in antidumping and safeguards is in “traditional” products – Must wait and see if “new” products come to fore – There are lags – e.g., takes time for drop in prices and unemployment to feed into dumping/injury Extensive fiscal/financial support to key sectors – finance, autos – mostly by OECD Scope for discrimination and political pressure to keep resources at home—including through procurement

15

Developing countries have initiated most new “trade remedy” investigations Source: Chad Bown Global Antidumping Database (World Bank PREM Note 144, October 2009)Global Antidumping Database

Global Antidumping Database")

16

Rules seem to be working: (i) imposed measures flat: (ii) share of investigations leading to higher barriers down:

imposed measures flat: (ii) share of investigations leading to higher barriers down:")

17

Getting to yes WTO Members confront two broad judgments 1.How best to strike a balance between more liberalization of applied policies and more security of access (more bindings) 2.How far and under what conditions to allow for safeguard type actions and trade remedies in return for tighter and more comprehensive tariff and other policy bindings

2.How far and under what conditions to allow for safeguard type actions and trade remedies in return for tighter and more comprehensive tariff and other policy bindings")

18

Market access—“sectorals” NAMA – Modalities generate exceptions for sensitive products – Sectoral deals will mostly involve a (small) subset of WTO members – GATT/WTO rule of thumb has been +/- 90% of world trade – Could be pursued along lines of ITA and financial-telecom- maritime services talks after Uruguay Round – as part of a Doha agreement – Progress also possible through (bilateral) scheduling negotiations Services – Strong push by industry in EU/US for liberalization – Focus instead on significant additional binding of policies – arguably could do much to attract more support for a deal

subset of WTO members – GATT/WTO rule of thumb has been +/- 90% of world trade – Could be pursued along lines of ITA and financial-telecom- maritime services talks after Uruguay Round – as part of a Doha agreement – Progress also possible through (bilateral) scheduling negotiations Services – Strong push by industry in EU/US for liberalization – Focus instead on significant additional binding of policies – arguably could do much to attract more support for a deal")

19

“Safeguards” Special safeguard mechanism for agriculture – Often trade protection will not help when there are shocks (raise prices for the poor) – Analysis suggests a quantity based SSM can increase world price volatility – Price-based SSM has less negative consequences for world price volatility Experience suggests international rules matter but domestic political economy is as important – Focus on monitoring/review; processes that allow domestic stakeholders to defend their interests

– Analysis suggests a quantity based SSM can increase world price volatility – Price-based SSM has less negative consequences for world price volatility Experience suggests international rules matter but domestic political economy is as important – Focus on monitoring/review; processes that allow domestic stakeholders to defend their interests")

20

Conclusion: the bird in hand Major benefits of Doha lie in greater policy disciplines—improved security of access And strengthening of global rules that reduce prospect/size of (future) negative spillovers – Agricultural support policies; environmental goods But there will also be liberalization in areas that matter to many developing countries – For market access: tariff peaks – And market entry: trade facilitation, aid for trade

negative spillovers – Agricultural support policies; environmental goods But there will also be liberalization in areas that matter to many developing countries – For market access: tariff peaks – And market entry: trade facilitation, aid for trade")

21

Building on recent progress and lessons Aid for trade – EIF: now up and running – Trade Facilitation Facility: Real trade/transactions costs are the major factor reducing competitiveness of firms/farms in developing countries – Recent trade finance initiatives by MDBs – Increased emphasis on regional public goods – Interest by private sector to leverage AFT (e.g., Aid for Trade Facilitation Partnership) Improve transparency: better data on policies and flows – Lesson from the crisis: data is a public good – under-provided – This true even for tariffs – but especially subsidies, other nontariff measures, services policies, and procurement – Build on recommendations of the multi-agency taskforce on NTMs – allocate resources needed to collect/disseminate data

Improve transparency: better data on policies and flows – Lesson from the crisis: data is a public good – under-provided – This true even for tariffs – but especially subsidies, other nontariff measures, services policies, and procurement – Build on recommendations of the multi-agency taskforce on NTMs – allocate resources needed to collect/disseminate data")

22

Possible high return areas for Arab economies

23

Doing Business (World Bank)

")

24

Doing Business ranking N =178

25

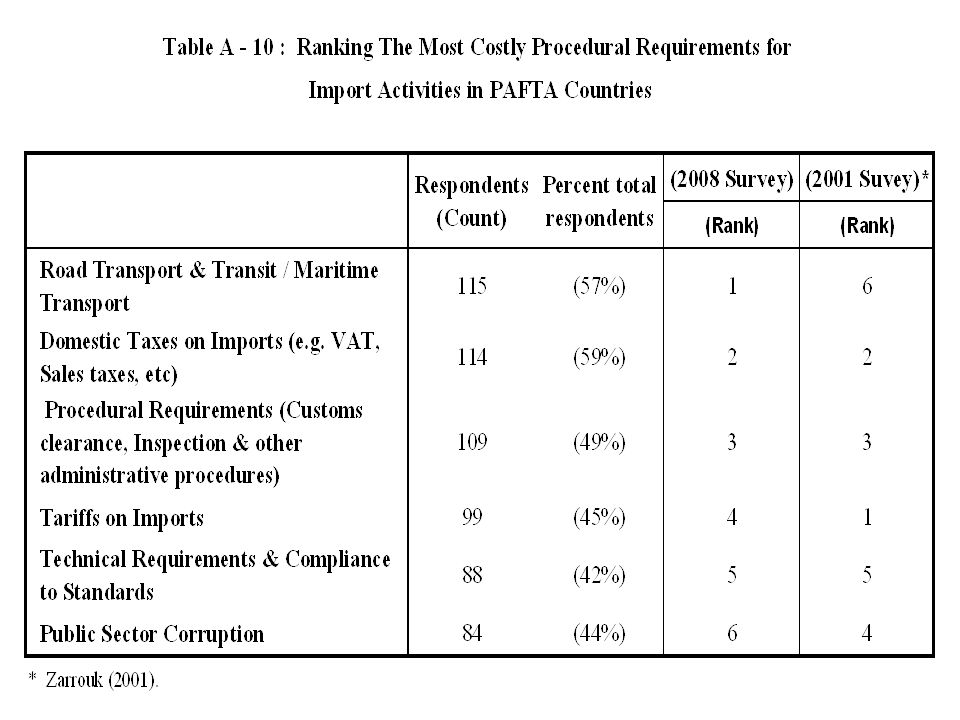

Recent survey of Arab trading firms: Intra- PAFTAD trading costs have declined Source: Hoekman and Zarrouk 2008 (World Bank Policy Research Working Paper)

")

26

Big reductions in time spent on bureaucracy

27

Procedures have been simplified: signatures

28

Variance in clearance times

30

Implications Illustrates importance of: – Trade facilitation broadly defined, including as an instrument to promote integration of regional markets – This linked to services agenda: logistics, transport, insurance, among others are all determinants of trade costs – Greater transparency: mechanisms to collect and monitor data on sources of trade costs for firms – All three areas require action at the national/regional level, but WTO can help

31

What matters more? Focus on real trade costs (including NTMs) and services – What type generates highest potential gains? What are the specific policies/barriers that raise costs/limit flows? – A “mapping” exercise: measure policies to permit analysis and monitoring of change over time – Discriminatory vs. nondiscriminatory measures Compile existing data and benchmark policies/performance – generate indices Identify key gaps – Bilateral FDI by sector; Bilateral services flows – NTMs: subsidies, product standards, origin rules

and services – What type generates highest potential gains. What are the specific policies/barriers that raise costs/limit flows. – A mapping exercise: measure policies to permit analysis and monitoring of change over time – Discriminatory vs. nondiscriminatory measures Compile existing data and benchmark policies/performance – generate indices Identify key gaps – Bilateral FDI by sector; Bilateral services flows – NTMs: subsidies, product standards, origin rules.")

32

Monitor implementation Of existing agreements – not just WTO. Also GAFTA, EU/US, GCC – Focus on administrative requirements and impacts – e.g., effect of rules of origin – Enforcement and transparency mechanisms – including dispute settlement Disputes mean agreements are working/relevant to citizens (enterprises, workers) A report on “The State of Arab Integration”? – With private sector; by private sector/civil society

A report on The State of Arab Integration . – With private sector; by private sector/civil society.")

Similar presentations

www.cuts-international.org.>")

>")

Shumeet K. Grewal.>")