Download presentation

Presentation is loading. Please wait.

1

Valuing Business Methods of valuation DCF valuation (e.g. using WACC) DCF valuation (e.g. using WACC) Relative valuation (comparables) Relative valuation (comparables) Cost-based valuation Cost-based valuation

DCF valuation (e.g. using WACC) Relative valuation (comparables) Relative valuation (comparables) Cost-based valuation Cost-based valuation.")

2

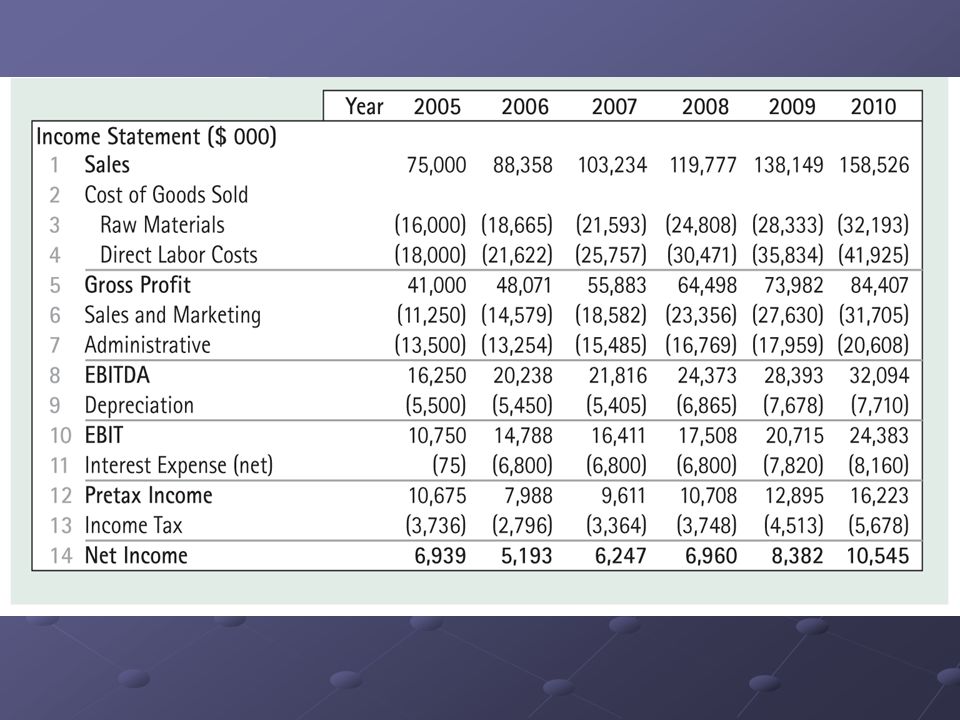

Ideko Corporation Line of business: designing and manufacturing sports eyewear Estimated 2006 Income Statement and Balance Sheet:

3

Sales = 75,000 EBITDA = 16,250 Net Income = 6,939 Debt = 4,500 You want to acquire this company at a price of $150 mln. Is it a fair price? At this price: P/E = 21.6 P/E = 21.6 EV = E + D – cash. Assume you estimate that Ideko holds $6.5 mln in cash in excess of its working capital needs (i.e. invested at a market rate of return) EV = 150 + 4.5 – 6.5 = $148 mln EV = E + D – cash. Assume you estimate that Ideko holds $6.5 mln in cash in excess of its working capital needs (i.e. invested at a market rate of return) EV = 150 + 4.5 – 6.5 = $148 mln EV/Sales = 2 EV/Sales = 2 EV/EBITDA = 9.1 EV/EBITDA = 9.1

EV = – 6.5 = $148 mln EV = E + D – cash. Assume you estimate that Ideko holds $6.5 mln in cash in excess of its working capital needs (i.e. invested at a market rate of return) EV = – 6.5 = $148 mln EV/Sales = 2 EV/Sales = 2 EV/EBITDA = 9.1 EV/EBITDA = 9.1.")

4

Ideko Financial Ratios Comparison 150 looks like a reasonable price

5

Valuing Ideko using DCF So, assume you are buying it for 150 mln. What’s the NPV of this transaction? (how much will you gain) Multiples give a rough idea. After you acquire the firm you will change it. Hence, you need to forecast future (after acquisition) FCF and use DCF techniques Business plan Business plan Financial model (to forecast FCF and terminal value) Financial model (to forecast FCF and terminal value) Estimating cost of capital Estimating cost of capital Valuation using DCF Valuation using DCF

Multiples give a rough idea. After you acquire the firm you will change it. Hence, you need to forecast future (after acquisition) FCF and use DCF techniques Business plan Business plan Financial model (to forecast FCF and terminal value) Financial model (to forecast FCF and terminal value) Estimating cost of capital Estimating cost of capital Valuation using DCF Valuation using DCF.")

6

Estimated 2005 Income Statement and Balance Sheet Data for Ideko Corporation (Spreadsheet)

")

7

The Business Plan Expected market growth: 5% per year Cut administrative expenses and increase expenditures on product development, sales and marketing expected raise in the firm’s market share from 10% to 15% over 5 years Once cumulative sales growth reaches 50% expansion needed Inflation Selling price will rise at 2% per year Selling price will rise at 2% per year Raw materials price will rise at 1% per year Raw materials price will rise at 1% per year Labor costs will rise at 4% per year (inflation + additional overtime) Labor costs will rise at 4% per year (inflation + additional overtime)

Labor costs will rise at 4% per year (inflation + additional overtime)")

8

Ideko Sales and Operating Cost Assumptions

9

Capital expenditure assumptions

10

Capital structure changes: levering up Planned debt and interest payments (after 2010 all is repaid) Indeko is underleveraged (book value of debt = 4,500 while total assets = 86,822) Indeko is underleveraged (book value of debt = 4,500 while total assets = 86,822) Hence, plan to increase debt: 100 mln now (put in our pocket) and some more in 2008 and 2009, interest rate = 6.8% Hence, plan to increase debt: 100 mln now (put in our pocket) and some more in 2008 and 2009, interest rate = 6.8%

Indeko is underleveraged (book value of debt = 4,500 while total assets = 86,822) Indeko is underleveraged (book value of debt = 4,500 while total assets = 86,822) Hence, plan to increase debt: 100 mln now (put in our pocket) and some more in 2008 and 2009, interest rate = 6.8% Hence, plan to increase debt: 100 mln now (put in our pocket) and some more in 2008 and 2009, interest rate = 6.8%")

11

Sources and uses of funds You buy the company for 150 mln, get an excess cash of 6.5 mln and repay the debt of 4.5 mln. Hence, essentially you spend 148… + 5 mln in fees = 153 mln But you raise 100 mln in debt – this allows you to pay essentially only 53 mln for the company

12

Building the financial model Forecasting earnings

14

Working capital forecast (for details see BD, ch. 19)

")

15

Forecasting free cash flow

16

Estimating the cost of capital Estimating beta We have to unlever betas first:

17

Let our unlevered beta = 1.20 (based on comparables) Let market risk premium = 5% Hence, r U = r f + β U (E[R mkt ] – r f ) = 4% + 1.20*5% = 10%

![Let our unlevered beta = 1.20 (based on comparables) Let market risk premium = 5% Hence, r U = r f + β U (E[R mkt ] – r f ) = 4% *5% = 10%](http://images.slideplayer.com/25/8123360/slides/slide_17.jpg "Let our unlevered beta = 1.20 (based on comparables) Let market risk premium = 5% Hence, r U = r f + β U (E[R mkt ] – r f ) = 4% *5% = 10%")

18

Valuing the investment First, we need to estimate continuation value in year 2010. Multiples approach (but DCF can also be used):

:.")

19

Now we can value Ideko. Let’s use APV V L t = V U t + T t

20

So, we obtain Equity Value = 113 mln We have spent only 53 mln Hence, NPV = 113 mln – 53 mln = $60 mln – good deal! Our estimate of EV based on comparables, $148mln, was an underestimation (now we obtain $213 mln) Why? Because previously we did not take into account the changes that we are going to implement in the firm

Why. Because previously we did not take into account the changes that we are going to implement in the firm.")

Similar presentations

–Residual income Model DCF and risidual income model are.>")