Download presentation

Presentation is loading. Please wait.

1

HOUSTON COUNTY BUDGET PREPARATION PROCESS Presented by: Bill Dempsey, CAO

2

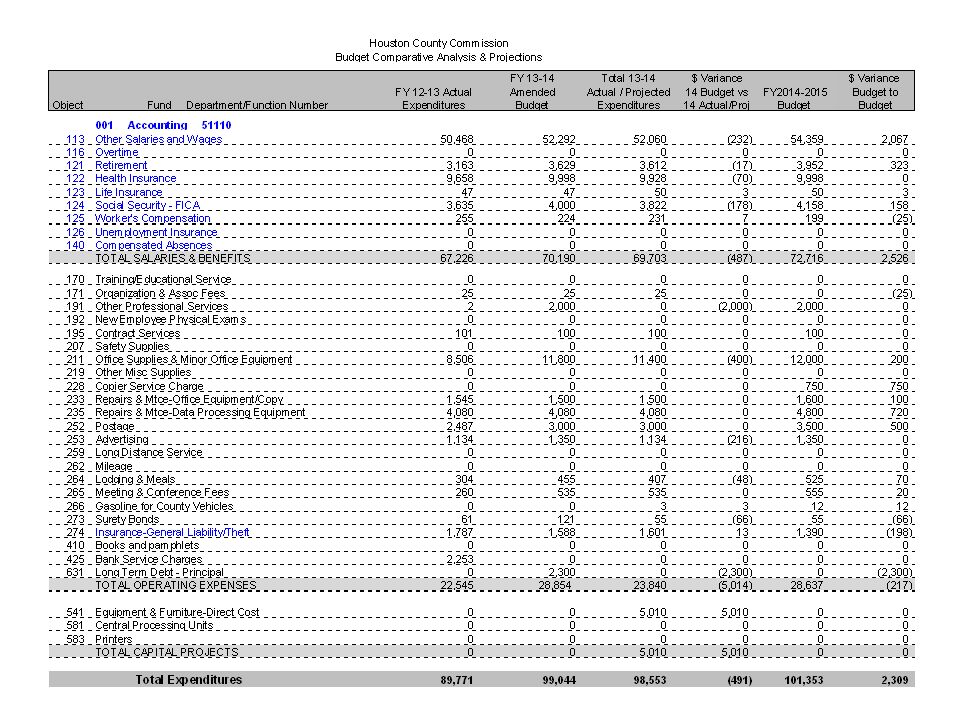

CALCULATING DEPARTMENTAL EXPENSES We divide our departmental expenditures into three different categories: 1)Salaries and Benefits 2)Operations 3)Capital Expenditures

Salaries and Benefits 2)Operations 3)Capital Expenditures")

4

JUNESEPTEMBER Mid-June we hold our departmental manpower, capital and major expense meeting for the coming year. Around July 10 th we hold our departmental operations meeting in which department heads are given their operations budget expenditure target for the coming year. E/July department heads submit their operations budget estimated expenditures for July ~ September and their coming years operation budget object detail based on their operations budget target. During July, using our revenue data base, departmental input and/or abstract calculations, the CAO determines projected yearly revenues for the current and new year. This step is repeated in late August. By early August, prepare first-pass budget. Throughout August we tweak the budget with Commissioners and Department Heads. Target final budget approval the first Commission meeting in September. THE BUDGET PROCESS INCLUDES FORECASTING REVENUE & EXPENDITURES FOR JULY – SEPTEMBER IN THE CURRENT YEAR AND REVENUES/EXPENDITURES FOR THE NEW YEAR.

5

EXPENSE CALCULATIONS: Labor & Benefits, Capital and Other Major Expenditures During this mid-June meeting, any department head that seeks to add people, add capital equipment or requests funding for a major spending project (other than normal Road and Bridge projects) presents their detailed justification to the Commission. This is typically the only detailed meeting that the Commission will have with department heads. Due to the nature of the meeting, only a few department heads will meet with the Commission. The final filtered outcome from this meeting will provide the basis for our coming year’s labor/benefits and capital expenditure budgets.

6

EXPENSE CALCULATIONS: Departmental Operations Budget Key departments are given a bottom-line operations budget expense target. Within this target each department is expected to allocate their expenses to include departmental spending, property insurance allocation, liability insurance calculations and lease costs. CALCULATING DEPARTMENTAL OPERATIONS BUDGET TARGETS CURRENT YEAR’S OPERATIONS TARGET -CURRENT YEAR’S EXTRAORDINARY EXPENSES + NEW YEAR’S EXTRAORDINARY EXPENSES +/- ADJUSTMENTS FOR INSURANCE, LEASE COST, ELECTRICAL AND OTHER ALLOCATIONS COMING YEAR’S OPERATIONS BUDGET TARGET Upon receipt of their operations budget target, department heads allocate their departmental expenditures object-by-object so that their bottom line operations budget does not exceed their allowed expenditure.

7

REVENUE CALCULATIONS We use three sources of information for calculating revenues: 1)Revenue Tracking Data Base 2)Abstract Calculations (from the Revenue Department) 3)Department Head Recommendations Most of our revenue forecasts are done through the use of a Revenue Tracking Data Base.

Revenue Tracking Data Base 2)Abstract Calculations (from the Revenue Department) 3)Department Head Recommendations Most of our revenue forecasts are done through the use of a Revenue Tracking Data Base.")

8

REVENUE TRACKING LOG

9

IN EARLY AUGUST WE COMPILE ALL EXPENSES AND REVENUES TOGETHER FOR OUR FIRST-PASS BUDGET ESTIMATE Revenues – Includes grants, normal revenues and projected unusual or one- time revenues. Expenses – Departmental Expenses (Labor/Benefits, Operations/Capital) Agency Donations Long Term Debt Grant Spending (EXAMPLE) Current year beg. FB: $5,000,000New Year est.FB: $3,800,000 Current years est. rev.: $4,700,000New Year est. rev: $4,850,000 Current years est. exp.: $5,900,000New year est.Exp: $5,300,000 Ending FB current year: $3,800,000New Year est. end FB: $3,350,000 After arriving at a first-pass estimate ending fund balance for the new year we begin tweaking expenses and revenues to arrive at our final targeted ending total FB.

Agency Donations Long Term Debt Grant Spending (EXAMPLE) Current year beg. FB: $5,000,000New Year est.FB: $3,800,000 Current years est. rev.: $4,700,000New Year est. rev: $4,850,000 Current years est. exp.: $5,900,000New year est.Exp: $5,300,000 Ending FB current year: $3,800,000New Year est. end FB: $3,350,000 After arriving at a first-pass estimate ending fund balance for the new year we begin tweaking expenses and revenues to arrive at our final targeted ending total FB..")

10

FINAL BUDGET BY FUND BALANCE After arriving at the Commission-authorized bottom-line fund balance, we prepare a fund allocation summary sheet. NOTE: All money from all funds are included in one normal checking account (Exception: We have created special flow-through checking accounts for payroll and flex payments). We create the Funds Summary through detailed planned transfer of money between projected ending fund balances.

. We create the Funds Summary through detailed planned transfer of money between projected ending fund balances..")

12

The final budget is normally presented for approval during the first scheduled Commission meeting in September. In November we present to the Commission a departmental over/under report indicating any overspending by a department for the prior year and the reason why. Commission authorization is requested to accept the overspending. In November we reconcile the prior year’s actual ending fund balance with the projected ending fund balance. If our projected ending fund balance is less than we estimated, we must adjust spending accordingly throughout the expenditure budget. Throughout the year the CAO is authorized to approve budget adjustments between objects within a department so long as the total adjustments do not increase that departments annual approved spending budget.

Similar presentations

Financial Management.>")

>")