Download presentation

Presentation is loading. Please wait.

1

Needles Powers Crosson Principles of Accounting 12e Standard Costing and Variance Analysis 24 C H A P T E R © human/iStockphoto

2

LEARNING OBJECTIVES ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. LO1: Define standard costs, and explain why standard costing is useful. LO2: Compute standard unit costs, and describe the role of flexible budgets in variance analysis to control costs. LO3: Compute and analyze direct materials variances. LO4: Compute and analyze direct labor variances. LO5: Compute and analyze overhead variances. LO6: Explain how variances are used to evaluate a business’s performance.

3

SECTION 1: CONCEPTS ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. Comparability: the convention of presenting information in a way that enables decision makers to recognize similarities, differences, and trends over different periods in the same company and among different companies Understandability: the qualitative characteristic of information that enables users to comprehend the meaning of the information they receive

4

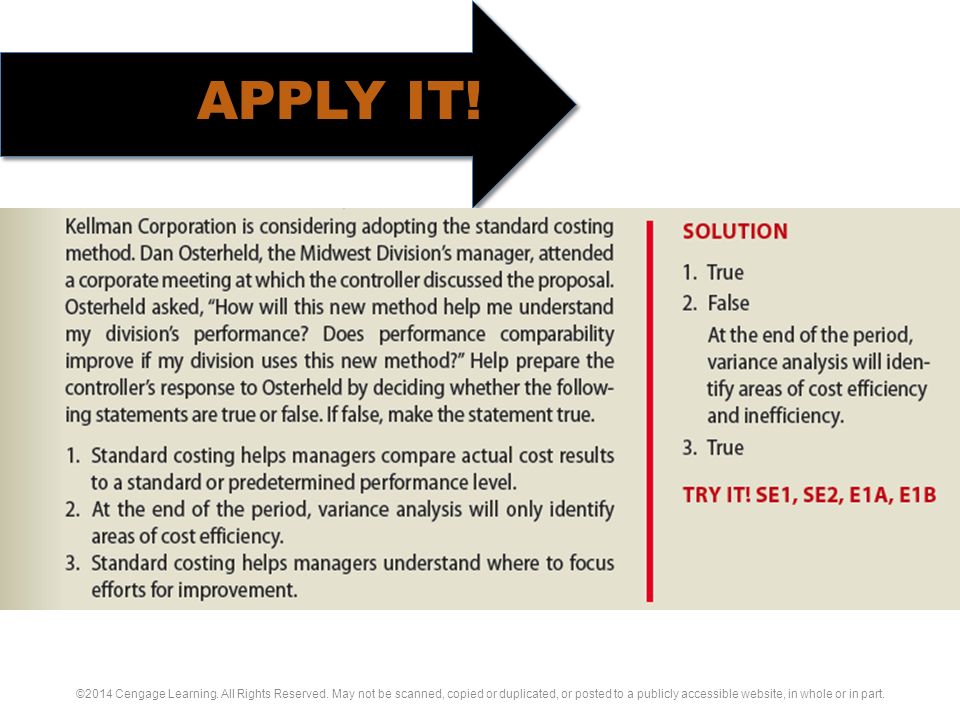

Concepts Underlying Standard Costing (slide 1 of 2) Standard costs are realistic estimates of costs based on analyses of both past and projected operating costs and conditions. –They provide a standard, or predetermined, performance level for use in standard costing. Standard costing is a method of cost control that is used to compare the difference, or variance, between standard and actual performance. –This method differs from actual and normal costing methods in that it uses estimated costs exclusively to compute all three elements of product cost. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

5

Concepts Underlying Standard Costing (slide 2 of 2) –Standard costing is especially effective for understanding and managing cost centers. –Managers find standard costing and variance analysis useful to develop budgets, to control costs, and to prepare reports. By analyzing variances between standard and actual costs, managers gain insight into the causes of those differences. –Standard costing can be used in any type of business and in conjunction with a job order costing, process costing, or activity- based costing system. –A disadvantage to using standard costing is that it can be expensive and time-consuming to gather all the needed information. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

7

SECTION 2: ACCOUNTING APPLICATIONS Compute standard unit costs Compute total flexible budget costs Compute and analyze direct materials variances –Direct materials price variance –Direct materials quantity variance Compute and analyze direct labor variances –Direct labor rate variance –Direct labor efficiency variance Compute and analyze overhead variances –Variable overhead spending variance –Variable overhead efficiency variance –Fixed overhead budget variance –Fixed overhead volume variance ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

8

Variance Analysis Variance analysis is the process of computing the differences between standard costs and actual costs and identifying the causes of those differences. –By examining the differences, or variances, between standard and actual costs, managers can gather valuable information about improving the accuracy of variance analysis and controlling costs. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

9

Computing Standard Costs (slide 1 of 2) A fully integrated standard costing system uses standard costs for all the elements of product cost: direct materials, direct labor, and overhead. –Standard costs are recorded in inventory accounts for materials, work in process, and finished goods, as well as the Cost of Goods Sold account. –Actual costs are recorded separately so that managers can compare what should have been spent (the standard costs) with the actual costs incurred in the cost center. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

with the actual costs incurred in the cost center. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part..")

10

Computing Standard Costs (slide 2 of 2) –A standard unit cost for a manufactured product has the following six elements: Direct materials price standard Direct labor rate standard Variable overhead rate standard Direct materials quantity standard Direct labor time standard Fixed overhead rate standard –Note that a standard unit cost for a service includes only the elements that relate to direct labor and overhead. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

11

Standard Direct Materials Cost The standard direct materials cost is the price that should be paid for the materials and is computed as follows. –In this equation, the direct materials price standard is a careful estimate of the cost of a specific direct material in the next period. –The direct materials quantity standard is an estimate of the amount of direct materials, including scrap and waste, that will be used in a period. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

12

Standard Direct Materials Cost: Example ICU, which makes surveillance robots, has recently updated the standards for its Watch Dog product. –Direct materials price standards are now $9.20 per square foot for casing materials and $20.17 for each mechanism. –Direct materials quantity standards are 0.025 square foot of casing materials per robot and one mechanism per robot. –Thus, the direct materials costs of making one robot are: ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

13

Standard Direct Labor Cost The standard direct labor cost is the cost necessary to produce a product, task, or job order and is computed as follows. –The direct labor rate standard is the hourly direct labor rate that is expected to prevail during the next period for each function or job classification. –The direct labor time standard is the expected labor time required for each department, machine, or process to complete the production of one unit or one batch. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

14

Standard Direct Labor Cost: Example –For ICU, direct labor time standards are 0.01 hour per robot for the Case Stamping Department and 0.05 hour per robot for the Assembly Department. –Direct labor rate standards are $8.00 per hour for the Case Stamping Department and $10.20 per hour for the Assembly Department. –Thus, the direct labor costs of making one robot in each department are: ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

15

Standard Overhead Cost (slide 1 of 2) The standard overhead cost is the sum of the estimates of variable and fixed overhead costs in the next period. It has two parts: variable costs and fixed costs. –The standard variable overhead rate is computed by dividing the total budgeted variable overhead costs by an expression of capacity, such as the budgeted number of standard machine hours or standard direct labor hours, as shown in the formula below: ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

16

Standard Overhead Cost (slide 2 of 2) -The standard fixed overhead rate is computed by dividing the total budgeted fixed overhead costs by an expression of capacity, usually normal capacity in terms of standard hours or units. The denominator is expressed in the same terms as the variable overhead rate. Using normal capacity in terms of standard direct labor hours as the denominator, the formula follows: ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

17

Standard Overhead Cost: Example For ICU, the standard variable overhead rate is $12.00 per direct labor hour. Thus, the variable overhead cost of making one robot is: The standard fixed overhead rate is $9.00 per direct labor hour. Thus, the fixed overhead cost of making one robot is: ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

18

Total Standard Unit Cost Once standard costs for direct materials, direct labor, and variable and fixed overhead have been developed, a total standard unit cost can be computed at any time. –For ICU, the standard cost of making one robot would be computed as follows: ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

19

The Role of Flexible Budgets in Variance Analysis The accuracy of variance analysis depends to a large extent on the type of budget that managers use when comparing variances. –Static, or fixed, budgets forecast revenues and expenses for just one level of output. –If a company produces more products than predicted, total production costs will almost always be greater than predicted. The performance report on the next slide shows that actual costs exceeded budgeted costs, but notice that the budgeted amounts are based on an output of 17,500 units when the actual output was 19,100 units. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

20

Performance Report Using Data from a Static Budget ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

21

Performance Report Using Data from a Flexible Budget To judge the division’s performance accurately, ICU’s managers can use a flexible budget, adjusted for an actual output of 19,100 units, which shows that actual costs are $29,197 less than the amount budgeted. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

22

Using Variance Analysis to Control Costs As shown on the next slide, using variance analysis to control costs is a four-step process: 1.Managers compute the amount of the variance. If the amount is insignificant—actual operating results are close to those anticipated—no corrective action is needed. 2.If the variance is significant, managers analyze the variance to identify its cause. 3.In identifying the cause, they then select performance measures that will enable them to track the activities that need to be monitored, analyze the results, and determine the action needed to correct the problem. 4.The final step is to take the appropriate corrective action. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

23

Variance Analysis: A Four-Step Approach to Controlling Costs ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

25

Computing and Analyzing Direct Materials Variances To control cost center operations, managers compute and analyze variances for whole cost categories, such as total direct materials costs, as well as variances for elements of those categories, such as the price and quantity of each direct material. –The more detailed their analysis of direct materials variances, the more effective they will be in controlling costs. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

26

Computing Total Direct Materials Cost Variance ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

27

Computing Total Direct Materials Price Variance To find the area responsible for the variance, the total direct materials cost variance must be broken down into the direct materials price variance and the direct materials quantity variance. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

28

Computing Total Direct Materials Quantity Variance ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

29

Summary of Direct Materials Variances The net of the direct materials price variance and the direct materials quantity variance should equal the total direct materials cost variance. –The following check shows that the variances for Cambria were computed correctly. –Variance analyses are sometimes easier to interpret in diagram form, as shown on the next slide. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

30

Diagram of Direct Materials Variance Analysis ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

31

Business Application Cambria’s managers were concerned because the company had been experiencing direct materials price and quantity variances for some time. –The price variances were always favorable and the quantity variances were always unfavorable. –The managers discovered that the company’s purchasing agent had been purchasing a lower grade of leather at a reduced price. –An analysis of scrap and rework revealed that the inferior quality of the substitute leather was causing the unfavorable quantity variance. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

32

(slide 1 of 2)

")

33

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. (slide 2 of 2)

.")

34

Computing Total Direct Labor Cost Variance ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

35

Computing Direct Labor Rate Variance For effective performance evaluation, management must know how much of the total cost arose from different direct labor rates and how much from different numbers of direct labor hours, which is found by computing the direct labor rate variance and the direct labor efficiency variance. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

36

Computing Direct Labor Efficiency Variance ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

37

Summary of Direct Labor Variances The net of the direct labor rate variance and the direct labor efficiency variance should equal the total direct labor cost variance. –The following check shows that the variances were computed correctly: –The next slide summarizes Cambria’s direct labor variances. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

38

Diagram of Direct Labor Variance Analysis ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

39

Business Application Because Cambria’s direct labor rate variance and direct labor efficiency variance were unfavorable, its managers investigated the causes of the variances. –Their analysis revealed that the Bag Assembly Department had replaced an assembly worker who was ill with a machine operator from another department who earned $0.70 more per hour. –The unfavorable efficiency variance was the result of the machine operator needing to learn assembly skills, as well as the late delivery of parts on five occasions. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

40

(slide 1 of 2)

")

41

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. (slide 2 of 2)

.")

42

Computing and Analyzing Overhead Variances Controlling variable and fixed overhead costs is more difficult than controlling direct materials and direct labor costs because the responsibility for overhead costs is hard to assign. –Fixed overhead costs may be unavoidable past costs, such as depreciation and lease expenses, which are not under the control of any department manager. –If variable overhead costs can be related to departments or activities, however, some control is possible. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

43

Computing Total Overhead Cost Variance (slide 1 of 2) ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

44

Computing Total Overhead Cost Variance (slide 2 of 2) This amount can be divided into a variable overhead variance and a fixed overhead variance. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

45

Total Variable Overhead Cost Variance ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

46

Diagram of Variable Overhead Variance Analysis ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

47

Computing Variable Overhead Spending Variance Managers must know how much of the total cost arose from variable overhead spending deviations and how much from variable overhead application deviations (i.e., applied and actual direct labor hours). ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

48

Computing Variable Overhead Efficiency Variance ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

49

Summary of Variable Overhead Variances The net of the variable overhead spending variance and the variable overhead efficiency variance should equal the total variable overhead variance. –The following check shows that these variances have been computed correctly: ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

50

Total Fixed Overhead Cost Variance ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

51

Diagram of Fixed Overhead Variance Analysis ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

52

Computing Fixed Overhead Budget Variance For effective performance evaluation, managers break down the total fixed overhead cost variance into two additional variances: the fixed overhead budget variance and the fixed overhead volume variance. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

53

Computing Fixed Overhead Volume Variance ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

54

Computing Fixed Overhead Volume Variance –Because the fixed overhead volume variance measures the use of existing facilities and capacity, a volume variance will occur if more or less than normal capacity is used. When capacity exceeds the expected amount, the result is a favorable overhead volume variance because fixed overhead was overapplied. When a company operates at a level below the normal capacity in units, the result is an unfavorable volume variance. –Not all of the fixed overhead costs will be applied to units produced. In other words, fixed overhead is underapplied, and the cost of goods produced does not include the full budgeted cost of fixed overhead. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

55

Summary of Variable and Fixed Overhead Variances The net of the variable and fixed overhead variances should equal the total overhead cost variance. –Checking the computations, we find that the variable and fixed overhead variances do equal the total overhead cost variance: ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

56

Business Application In analyzing the unfavorable total overhead cost variance of $212, the manager of Cambria’s Bag Assembly Department found the following causes: –The inefficiency of the machine operator who substituted for an assembly worker created unfavorable variances for both direct labor efficiency and variable overhead efficiency. –Higher-than-anticipated factory insurance premiums were the reason for the unfavorable fixed overhead budget variance. –Since the 432 standard hours were well above the normal capacity of 400 direct labor hours, fixed overhead was overapplied, and it resulted in a $104 (F) volume variance. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

volume variance. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part..")

57

(slide 1 of 3)

")

58

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. (slide 2 of 3)

.")

59

©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. (slide 3 of 3)

.")

60

SECTION 3: BUSINESS APPLICATIONS Planning Performing Evaluating Communicating ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

61

Using Cost Variances to Evaluate Managers’ Performance To ensure that the evaluation of a business’s performance is effective and fair, a company’s policies should be based on input from managers and employees and should specify the procedures that managers are to use when: –Preparing operational plans –Assigning responsibility for carrying out the operational plans –Communicating the operational plans to key personnel –Evaluating performance in each area of responsibility –Identifying the causes of significant variances from the operational plan –Taking corrective action to eliminate problems ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

62

Variance Analysis and the Management Process ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part. The diagram below frames manager responsibilities for standard costing and variance analysis within the management process of planning, performing, evaluating, and reporting on cost center operations.

63

Using Cost Variances to Evaluate Managers’ Performance Variance analysis is usually more effective at pinpointing efficient and inefficient operating areas than are basic comparisons of budgeted and actual data. –As shown on the next slide, a managerial performance report based on standard costs and related variances should identify the causes of each significant variance, the personnel involved, and the corrective actions taken. –The mere occurrence of a variance does not indicate that a manager has performed poorly, so long as causes are identified and corrective action is taken. ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

64

Managerial Performance Report Using Variance Analysis (slide 1 of 2) ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

65

Managerial Performance Report Using Variance Analysis (slide 2 of 2) ©2014 Cengage Learning. All Rights Reserved. May not be scanned, copied or duplicated, or posted to a publicly accessible website, in whole or in part.

Similar presentations