Download presentation

Presentation is loading. Please wait.

1

Initial Public Offerings papers by: Loughran and Ritter FM (2004) Brau and Fawcett JF (2006)

Brau and Fawcett JF (2006)")

2

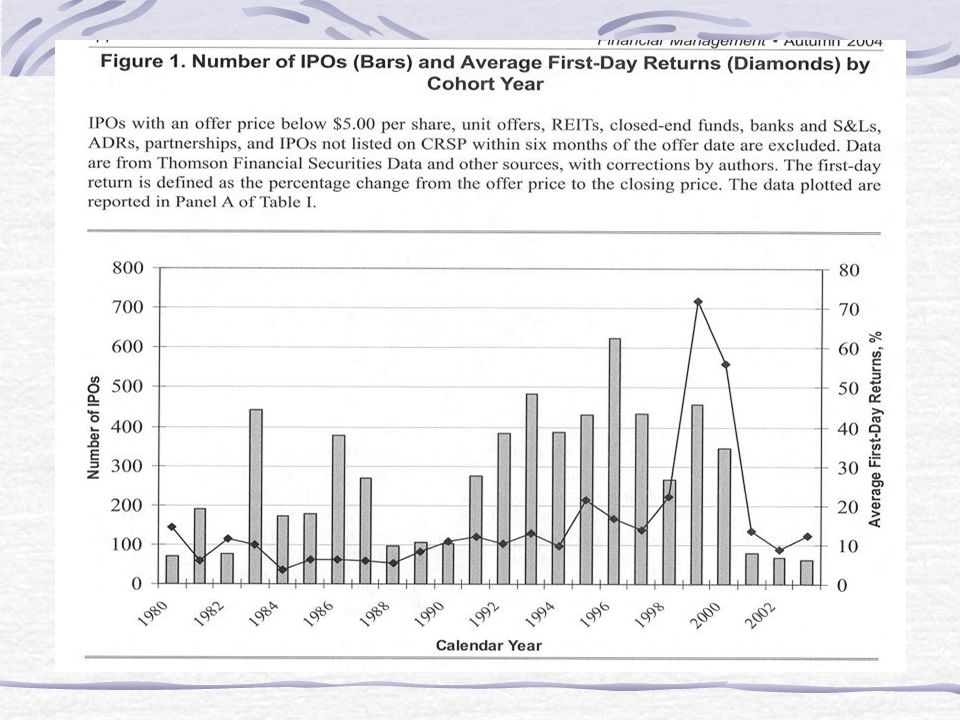

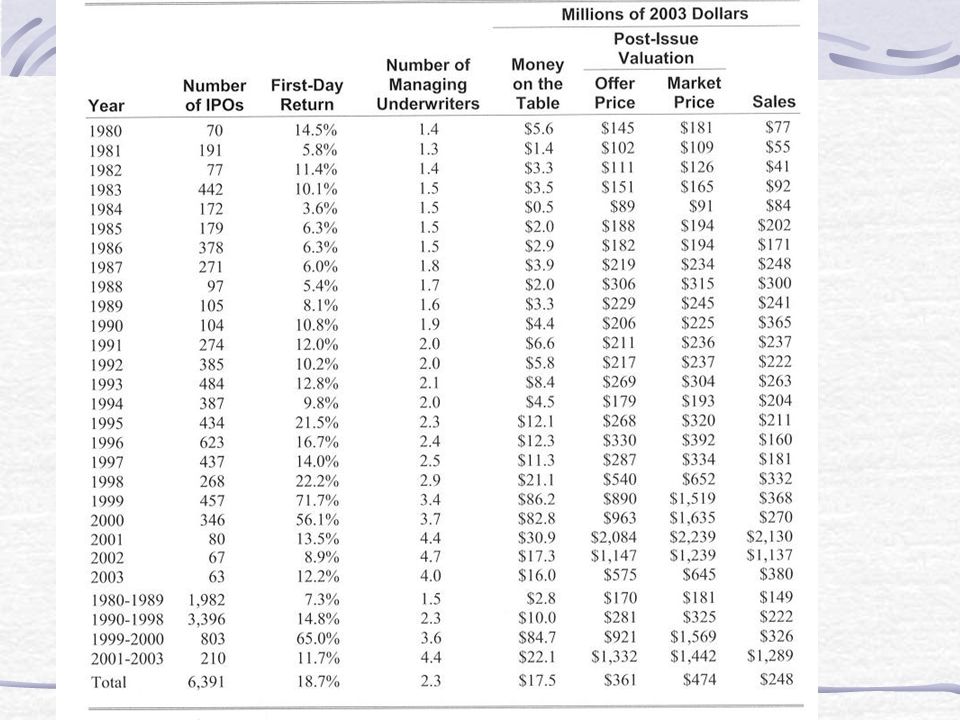

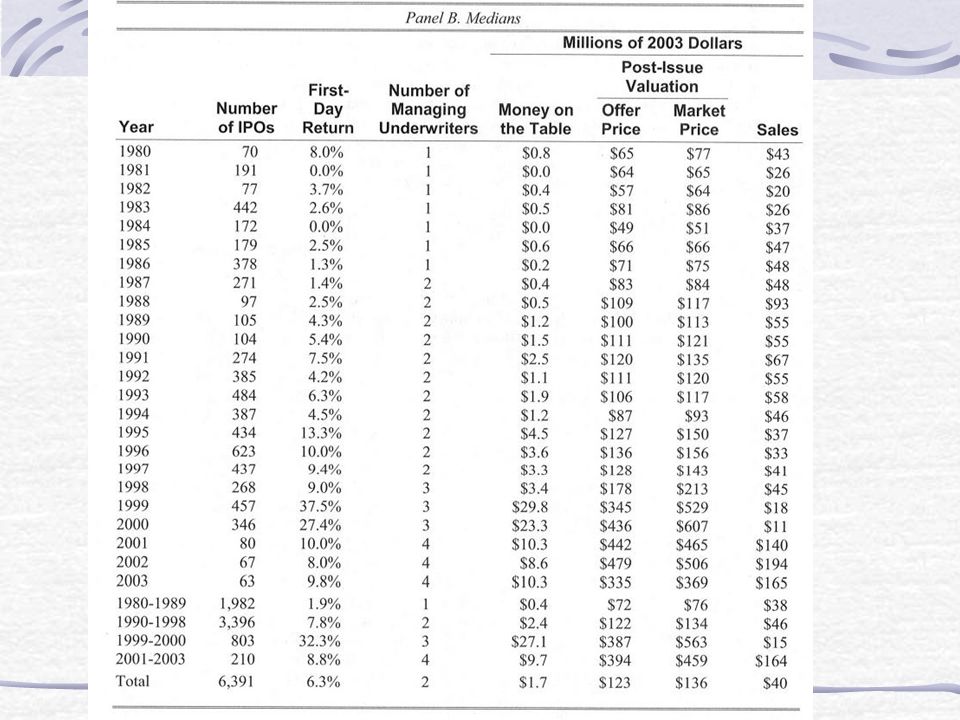

Initial Underpricing average underpricing of 18% varies over time in late 70s and early 80s in early to mid 90s huge in late 90s and 2000 relative to all other times

4

Reasons for Underpricing asymmetric information between underwriter and issuer between issuers and potential buyers between informed and uninformed investors protection against future litigation marketing function increase ownership base facilitate questionable practices prospect theory Brau and Fawcett (JF 2006)

")

5

Expectations and Explanations of Underpricing Brau and Fawcett (2006) CFOs asked to indicate on 5-pt scale “To what extent did the following lead to the level of underpricing expected?” (expected an average of 10%) “to compensate investors for taking risk of IPO” – 3.47 “underwriters underprice to incur favor of institutional investors” – 3.20 “to ensure a wide base of owners” – 3.17 “to increase the post-issue trading volume of the stock” – 3.14

CFOs asked to indicate on 5-pt scale To what extent did the following lead to the level of underpricing expected (expected an average of 10%) to compensate investors for taking risk of IPO – 3.47 underwriters underprice to incur favor of institutional investors – 3.20 to ensure a wide base of owners – 3.17 to increase the post-issue trading volume of the stock – 3.14")

6

Signaling number of papers that suggest certain actions send good/bad signals relative to the quality of the firm/offer selling insider shares selling large portion of firm using prestigious underwriters using reputable accounting firm having backing of VC firm signal firm quality using underpricing insiders committing to long lockup period signal firm quality history of strong earnings signals future strong performance

7

Signaling Brau and Fawcett (2006) – What type of signal do the following actions convey to investors regarding the value of a firm going public? strong historical earnings – 4.51 using top IB – 4.21 insiders commit to long lockup – 3.99 using a big 4 acctg firm – 3.91 large first day price jump – 3.77

8

Advantages of Underpricing to Underwriter compensation underwriter discretion the good & the bad

12

Timing of IPOs / Underwriter Selection theories on timing take advantage of attractive stock prices / bull markets attractiveness of IPO market firms at a certain point in there growth cycle and need external equity to grow CFOs – take into account market and industry stock returns (Brau and Fawcett) CFOs – select underwriters based on overall reputation, quality of research department, and industry expertise also some on institutional investor base

CFOs – select underwriters based on overall reputation, quality of research department, and industry expertise also some on institutional investor base")

13

Reasons for Going Public motivations suggested by theory cost of capital (M&M) allow insiders to cash out of firm facilitate takeover activity serve as strategic moves broaden ownership base of firm capture first-mover advantage increase publicity or reputation of firm analyst coverage

allow insiders to cash out of firm facilitate takeover activity serve as strategic moves broaden ownership base of firm capture first-mover advantage increase publicity or reputation of firm analyst coverage")

14

CFO survey on Motivation for Going Public “How important were/are the following motivations for conducting an IPO?” IPO serves to create public shares for use in future acquisitions – 3.56 (59% agree) establishment of market price or value for the firm (only other to receive support from more than 50% of CFOs) Why do some firms decide not to go public?

establishment of market price or value for the firm (only other to receive support from more than 50% of CFOs) Why do some firms decide not to go public")

Similar presentations

Desire to raise capital for a growing firm. Create liquidity for founders and other.>")