Download presentation

Presentation is loading. Please wait.

1

Impact of Food Retail Investments Evidence from Czech Republic, Slovakia, Poland and Russia Liesbeth Dries – K.U.Leuven EastAgri 2005 Annual Meeting, Rome, 28 February 2005

2

Goal & methodology Goal: tot analyse the impact of food retail investments on food systems in CEE countries Goal: tot analyse the impact of food retail investments on food systems in CEE countries Methodology: Methodology: Countries: Czech Republic, Slovakia, Poland and Russian FederationCountries: Czech Republic, Slovakia, Poland and Russian Federation Food chains: FFV & DairyFood chains: FFV & Dairy Interviews with retail chains; wholesalers; processors & farm survey (Czech Republic)Interviews with retail chains; wholesalers; processors & farm survey (Czech Republic)

Interviews with retail chains; wholesalers; processors & farm survey (Czech Republic)")

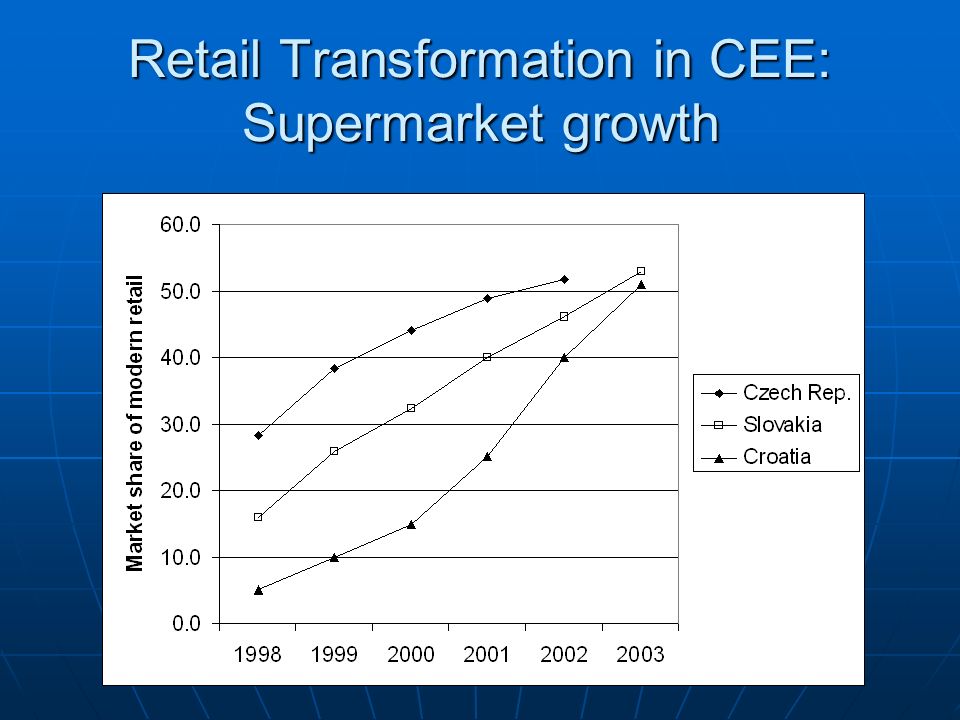

3

Retail Transformation in CEE: Supermarket growth

8

Retail Transformation in CEE Dramatic rise in market share of supermarkets and modern retail sector Dramatic rise in market share of supermarkets and modern retail sector Multinationalization Multinationalization Concentration Concentration Inter-country as well as intra-country supermarket diffusion Inter-country as well as intra-country supermarket diffusion Important changes in procurement systems Important changes in procurement systems

9

Implications for supply chain: procurement system changes Initially: retailers buy from local wholesalers and importers Initially: retailers buy from local wholesalers and importers Shift to centralised procurement systems: Build distribution centres Shift to centralised procurement systems: Build distribution centres

10

Change of procurement system Shift toward cross-border systems: Shift toward cross-border systems: Coordinate procurement over Distribution Centres in different countries of operation:Coordinate procurement over Distribution Centres in different countries of operation: Ahold Central Europe Ahold Central Europe Tesco ‘International Purchasing Dept.’ Tesco ‘International Purchasing Dept.’ To what extent? E.g. Tesco/Metro – CEE products for UK/German supermarketsTo what extent? E.g. Tesco/Metro – CEE products for UK/German supermarkets

11

Change of procurement system Shift toward specialized/dedicated wholesalers (specialized in product category, dedicated to supermarkets) Shift toward specialized/dedicated wholesalers (specialized in product category, dedicated to supermarkets) Shift toward preferred supplier systems to select producers meeting quality and safety standards and lower transaction costs Shift toward preferred supplier systems to select producers meeting quality and safety standards and lower transaction costs Evidence survey Czech Republic: 30% suppliers WS & 60% suppliers SM have contracts (preferred suppliers)Evidence survey Czech Republic: 30% suppliers WS & 60% suppliers SM have contracts (preferred suppliers)

Shift toward specialized/dedicated wholesalers (specialized in product category, dedicated to supermarkets) Shift toward preferred supplier systems to select producers meeting quality and safety standards and lower transaction costs Shift toward preferred supplier systems to select producers meeting quality and safety standards and lower transaction costs Evidence survey Czech Republic: 30% suppliers WS & 60% suppliers SM have contracts (preferred suppliers)Evidence survey Czech Republic: 30% suppliers WS & 60% suppliers SM have contracts (preferred suppliers)")

12

Change of procurement system Shift toward private safety and quality standards Shift toward private safety and quality standards E.g SISPO Czech RepblicE.g SISPO Czech Repblic E.g. Eurep-gap (international chains – international standards)E.g. Eurep-gap (international chains – international standards)

E.g. Eurep-gap (international chains – international standards).")

13

Public versus private standards - traceability

14

Private standards - quality

15

Significant higher quality delivered to SM Significant higher quality delivered to SM Growth in high quality production 2000- 2003 for growers supplying SM since 2000 Growth in high quality production 2000- 2003 for growers supplying SM since 2000 Decline in high quality production 2000- 2003 for growers delivering to local market in 2000 Decline in high quality production 2000- 2003 for growers delivering to local market in 2000

16

So: Increased demands on: Increased demands on: QUALITY (and safety)QUALITY (and safety) VOLUMEVOLUME And: COORDINATIONAnd: COORDINATION

QUALITY (and safety) VOLUMEVOLUME And: COORDINATIONAnd: COORDINATION")

17

The development of producer marketing organisations: CZ Developments in Food Retail sector are main driving force behind organisation of farmers: Developments in Food Retail sector are main driving force behind organisation of farmers: 4 out of 5 interviewed Producer Marketing Organisations for FFV indicate as main reason for their establishment: to gather sufficient quantity and product varieties to satisfy the requirements of big supermarket chains4 out of 5 interviewed Producer Marketing Organisations for FFV indicate as main reason for their establishment: to gather sufficient quantity and product varieties to satisfy the requirements of big supermarket chains

18

Potential benefits of PMO to growers Bargaining power Bargaining power Services Services Extension service (55%) Extension service (55%) Storage, sorting, packaging facilities (60%) Storage, sorting, packaging facilities (60%) Access to information (73%) Access to information (73%) Facilitated access to inputs through payment guarantee program with input suppliers Facilitated access to inputs through payment guarantee program with input suppliers Preferred position to apply for bank loans (repayment certainty) Preferred position to apply for bank loans (repayment certainty)......

Extension service (55%) Storage, sorting, packaging facilities (60%) Storage, sorting, packaging facilities (60%) Access to information (73%) Access to information (73%) Facilitated access to inputs through payment guarantee program with input suppliers Facilitated access to inputs through payment guarantee program with input suppliers Preferred position to apply for bank loans (repayment certainty) Preferred position to apply for bank loans (repayment certainty)......")

19

Retailers & vertical coordination may be positive for key weaknesses Key weaknesses of farm sector : Key weaknesses of farm sector : Shortage of finance for investmentsShortage of finance for investments QualityQuality Access to high value marketsAccess to high value markets Retail investments and coordination with supply chains may assist farms in these areas Retail investments and coordination with supply chains may assist farms in these areas

20

Retail assistance to farms ? Direct effect: available evidence indicates that modern retailers introduce assistance packages “if they have to” to secure quality supplies. E.g. Direct effect: available evidence indicates that modern retailers introduce assistance packages “if they have to” to secure quality supplies. E.g. Berdegue et al (Central America)Berdegue et al (Central America) Reardon et al (Croatia)Reardon et al (Croatia) Dries & Reardon (Russia)Dries & Reardon (Russia) Indirect effect: Eg. Poland: Dairy companies focusing on high-quality markets (incl. EU export markets and the modern retail sector) are frontrunners in offering assistance to small farms; market channels targeted to informal markets and low quality sales copy programs later or not at all. Indirect effect: Eg. Poland: Dairy companies focusing on high-quality markets (incl. EU export markets and the modern retail sector) are frontrunners in offering assistance to small farms; market channels targeted to informal markets and low quality sales copy programs later or not at all.

Berdegue et al (Central America) Reardon et al (Croatia)Reardon et al (Croatia) Dries & Reardon (Russia)Dries & Reardon (Russia) Indirect effect: Eg. Poland: Dairy companies focusing on high-quality markets (incl. EU export markets and the modern retail sector) are frontrunners in offering assistance to small farms; market channels targeted to informal markets and low quality sales copy programs later or not at all. Indirect effect: Eg. Poland: Dairy companies focusing on high-quality markets (incl. EU export markets and the modern retail sector) are frontrunners in offering assistance to small farms; market channels targeted to informal markets and low quality sales copy programs later or not at all..")

Similar presentations