Download presentation

Presentation is loading. Please wait.

1

Does Financial Liberalization Spur Growth?

Emerging Markets Corporate Finance February 2003 Does Financial Liberalization Spur Growth? Geert Bekaert Columbia University and NBER Campbell R. Harvey Duke University and NBER Christian T. Lundblad Indiana University

2

Real GDP Growth Five Years Before and After Financial Liberalizations

3

Financial Liberalization Financial Development Growth Cost of Capital

Opportunities Relaxing Fin Constraints Financial Development Investment Efficiency of Investment Growth

4

Financial Liberalization and Growth

Controversial exercise Liberalization implies consumption booms and inefficient investment (crisis literature) Liberalization may lead to reduced savings (endogenous growth literature) Liberalization may lead to “hot speculative capital” and induce capital flight (Stiglitz & others)

Liberalization may lead to reduced savings (endogenous growth literature) Liberalization may lead to hot speculative capital and induce capital flight (Stiglitz & others)")

5

Financial Liberalization and Growth

What we already know (too many references to list!): Financial/banking development associated with higher growth Cost of capital decreases Investment increases

: Financial/banking development associated with higher growth. Cost of capital decreases. Investment increases.")

6

Financial Liberalization and Growth

Outline: 1. Did liberalization spur growth? Large panel of data Cross-sectional growth regression with temporal dimension 2. How did liberalization spur growth? 3. Accounting for the liberalization effect Is is macro-economic reforms? Is it financial development? Other simultaneity biases? 4. Conclusions

7

Financial Liberalization and Growth

Caveats: Not much guidance from theory. As a result, it is important to conduct extensive robustness experiments

8

Financial Liberalization and Growth

Econometric Framework: where yi,t+k,k is real per capita GDP growth between t and t+k Qi,1980 is initial GDP, Xi,t represents control variables Libi,t is a Liberalization indicator variable

9

Financial Liberalization and Growth

Econometric Framework:

10

Financial Liberalization and Growth

Econometric Framework: ST is the variance covariance matrix of the sample orthogonality conditions

11

Financial Liberalization and Growth

Key issues: Temporal dimension Different weighting matrices Liberalization variable Choice of “k” Endogeneity of the liberalization decision

12

Financial Liberalization and Growth

Liberalization dates: Use Bekaert and Harvey (JF 2000) “official liberalization” dates These dates are based on a detailed chronology of important regulatory events Augmented with IFC frontier markets and three developed markets, Spain, New Zealand and Japan

official liberalization dates. These dates are based on a detailed chronology of important regulatory events. Augmented with IFC frontier markets and three developed markets, Spain, New Zealand and Japan.")

13

Financial Liberalization and Growth

Data: Four samples determined by availability of data Sample I: 95 countries Sample II: 75 countries [macroeconomic and demographic data]

14

Financial Liberalization and Growth

Data: Four samples determined by availability of data Sample III: 50 countries Sample IV: 28 countries [add financial development indicators] As data requirements become more stringent, the variance of GDP levels across countries in the sample decreases.

15

Financial Liberalization and Growth

Liberalization dates: Use Bekaert and Harvey (JF 2000) “official liberalization” dates These dates are based on a detailed chronology of important regulatory events Augmented with IFC frontier markets and three developed markets, Spain, New Zealand and Japan

official liberalization dates. These dates are based on a detailed chronology of important regulatory events. Augmented with IFC frontier markets and three developed markets, Spain, New Zealand and Japan.")

16

Financial Liberalization and Growth

Liberalization dates: Robustness of our results checked by examining Bekaert and Harvey (2000)’s “First Sign” dates These dates based on the earliest date of {official liberalization, first ADR and first closed-end fund} Example: Thailand “Official” 1987:09 “First Sign” 1985:07

’s First Sign dates. These dates based on the earliest date of {official liberalization, first ADR and first closed-end fund} Example: Thailand. Official 1987:09. First Sign 1985:07.")

18

Financial Liberalization and Growth

Liberalization dates: Capturing “intensity” or “comprehensiveness” of the liberalization Ratio of IFC investable market cap to global stocks (Bekaert (1995) and Edison and Warnock (2002)) U.S. holdings of domestic market capitalization Is it just a proxy for capital account openness? [See Rodrik-Edwards debate]

and Edison and Warnock (2002)) U.S. holdings of domestic market capitalization. Is it just a proxy for capital account openness [See Rodrik-Edwards debate]")

19

Financial Liberalization and Growth

Are the dates exogenous? Counter examples Spain in the EU Some countries cannot liberalize their financial markets

20

Financial Liberalization and Growth

Findings so far: We document a liberalization effect on growth with certain "standard control variables"

23

Financial Liberalization and Growth

Findings so far: The liberalization effect is robust to different definitions of liberalization dates to business cycle or interest rate controls allowing for intensity of liberalization ...and independent of capital account liberalization

26

Financial Liberalization and Growth

Channels of increased growth: Both: increased investment, partially through a cost of capital effect and increased productivity (which is different from the financial development literature)

")

27

Financial Liberalization and Growth

On the mechanism ... Liberalization does not lead to consumption binge investment increases trade balance decreases

30

Financial Liberalization and Growth

On the mechanism ... Investment increases - but you need a minimum “country quality level” to see effect decreased cost of capital associated with more investment

32

Financial Liberalization and Growth

On the mechanism ... Productivity increases and this is not just a banking development effect

34

Financial Liberalization and Growth

Accounting for the liberalization effect: We investigate whether part of the effect can be ascribed to macroeconomic reforms financial development other regulatory reforms

35

Financial Liberalization and Growth

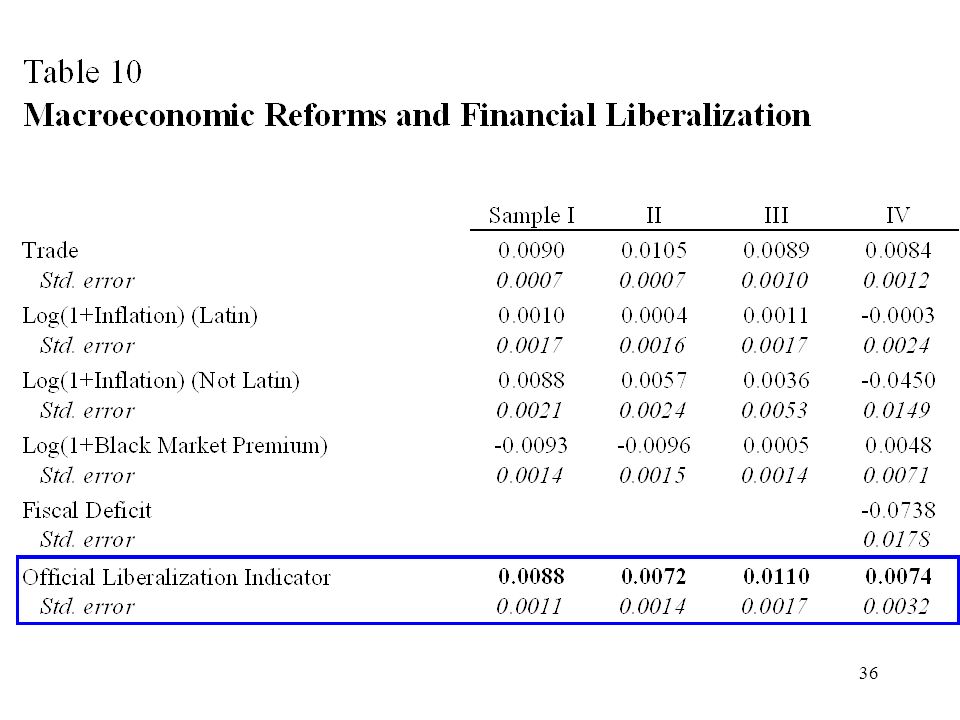

Accounting for the liberalization effect: Macroeconomic reforms ... Liberalization not spuriously reflecting macroeconomic reforms we control for trade openness, inflation, black market premiums, and government deficits

37

Financial Liberalization and Growth

Accounting for the liberalization effect: Financial development ... Degree of banking and equity market development is important but independent boost from liberalization we examine the size of private credit, equity market activity, and equity market size

40

Financial Liberalization and Growth

Accounting for the liberalization effect: Other regulatory reforms ... The financial liberalization/growth effect is not a post-banking crisis effect The enforcement of law and institutions are important

44

Financial Liberalization and Growth

Conclusions Financial liberalization spurs growth by 1% per annum over the five years Survives a battery of robustness experiments We understand better the channels whereby growth impacted by financial liberalization Liberalization effect not spuriously accounted for by a host of other events such as macro-economic reforms

45

Financial Liberalization and Growth

Conclusions Financial liberalization has a very important economic effect

46

Financial Liberalization and Growth

Conclusions Financial liberalization has a very important economic effect Consider economic impact of improvements plus a equity market liberalization Liberalization Total Growth = 3.02%

47

Financial Liberalization and Growth

Future and on-going research Growth volatility Financial development Liquidity and asset pricing The sequencing of liberalizations

Similar presentations

should be more prevalent in poorer countries, with less developed financial markets, with less well->")

; Kaminsky,>")