Download presentation

Presentation is loading. Please wait.

1

Some New Perspectives on India’s Approach to Capital Account Liberalization Eswar Prasad Cornell University

2

Benefits of Financial Integration: Theory Efficient international allocation of capital Consumption smoothing via international risk sharing Large welfare effects for developing economies

3

Growth Benefits of Financial Integration: Evidence About 25 studies of growth effects No effect 4 Mixed:18 Positive: 3 No robust macroeconomic evidence of growth benefits

4

Correlation between Growth and Current A/c Balance Non-industrial Countries, 1970-2004

6

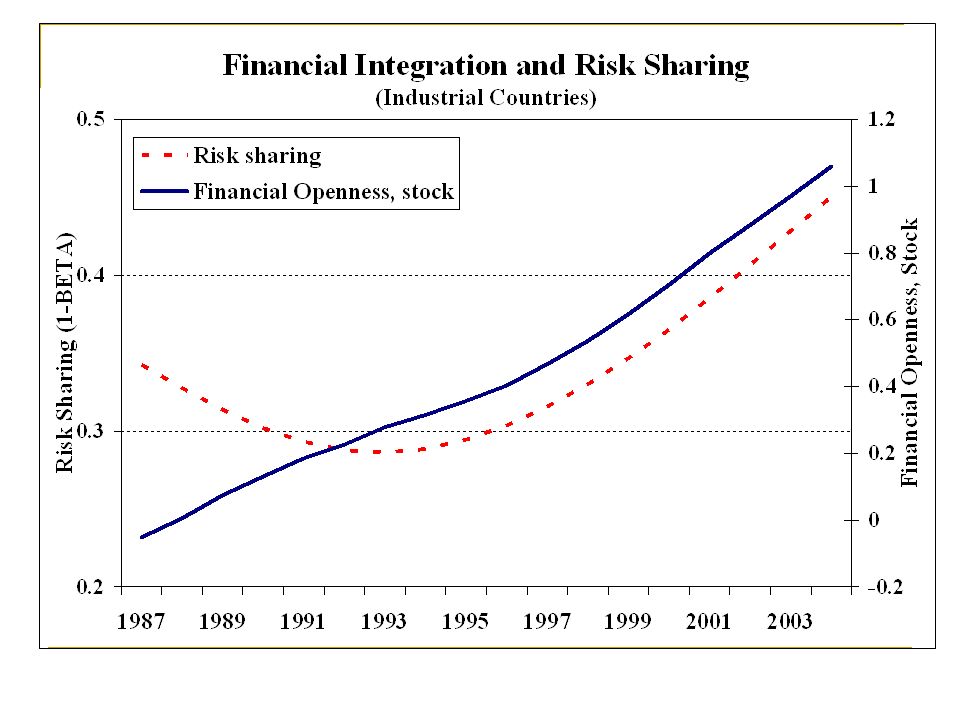

Volatility and Risk Sharing No evidence that financial integration by itself is proximate determinant of financial crises Developing economies, including emerging markets, have not attained better risk sharing

9

New Evidence: A Summary Equity market liberalization seems to work FDI benefits becoming more apparent Benefits more evident in micro data

10

The Traditional View Financial Globalization More efficient international allocation of capital Capital deepening International risk-sharing GDP growth Consumption volatility

11

A Different Perspective Traditional Channels Potential Collateral Benefits Financial market development Institutional development Better governance Macroeconomic discipline Financial Globalization GDP / TFP Growth Consumption volatility

12

Complication: Threshold Effects Threshold Conditions Financial market development Institutional Quality, Governance Macroeconomic policies Trade integration Financial Globalization GDP / TFP growth Risks of Crises GDP / TFP growth Risks of Crises Above Thresholds Below Thresholds X ?

13

TENSION !! Financial integration can catalyze financial development, improve governance, impose discipline on macro policies... But, in the absence of a basic pre-existing level of these supporting conditions, financial integration can wreak havoc

14

Collateral Benefits Framework Could Help Make Progress Unified conceptual framework Country-specific requirements, initial conditions can be taken into account Selective approach to liberalization based on prioritization of collateral benefits Can manage risks during transition to thresholds, but can not eliminate them

15

Really New Evidence: Composition of External Liabilities Matters FDI and portfolio equity liabilities improve risk sharing outcomes; Debt worsens risk sharing FDI and portfolio equity liabilities boost TFP growth; Debt has negative impact Negative effects of debt attenuated by deeper financial markets, better institutions Level of financial integration itself is a threshold

16

Reality on the Ground De facto financial openness increasing Capital controls becoming less effective > Expansion of trade > Larger international financial flows > Rising sophistication of international investors Trying to maintain rigid capital controls doesn’t solve inflows problem + creates distortionary costs

17

How Open is India’s Capital Account? De jure capital account openness >Capital controls De facto financial integration > Stocks of external assets, liabilities as ratio to GDP

18

De Jure Capital Account Openness

19

De Facto Financial Integration

20

De Facto Financial Integration: Emerging Markets (2006)

")

21

Balance of Payments (in billions of U.S. dollars)

")

22

Foreign Exchange Reserves: Flows and Stocks (in billions of U.S. dollars)

")

23

A Decomposition of the Recent Reserve Buildup (in billions of U.S. dollars)

")

24

Has the Benefit-Cost Tradeoff Improved? Composition of inflows, stocks of external liabilities has become more favorable

25

Share of FDI and Portfolio Liabilities in Gross External Liabilities

26

Ratio of FDI + Portfolio Liabilities to Gross External Liabilities: Emerging Markets (1995)

")

27

Ratio of FDI + Portfolio Liabilities to Gross External Liabilities: Emerging Markets (2006)

")

28

Has the Benefit-Cost Tradeoff Improved? Composition of inflows, stocks of external liabilities has become more favorable High levels of foreign exchange reserves

29

International Investment Position (in billions of U.S. dollars)

")

30

External Debt Stocks

31

Reserve Adequacy (ratio of reserves to relevant variables)

")

32

Has the Benefit-Cost Tradeoff Improved? Composition of inflows, stocks of external liabilities has become more favorable High levels of foreign exchange reserves Rising trade openness

33

Trade Openness Ratio

34

The Savings-Investment Balance (in percent of GDP)

")

35

Has the Benefit-Cost Tradeoff Improved? Composition of inflows, stocks of external liabilities has become more favorable High levels of foreign exchange reserves Rising trade openness Greater exchange rate flexibility

36

Nominal Exchange Rate Relative to U.S. Dollar

37

Real and Nominal Effective Exchange Rates

38

Has the Benefit-Cost Tradeoff Improved? Composition of inflows, stocks of external liabilities has become more favorable High levels of foreign exchange reserves Rising trade openness Greater exchange rate flexibility Financial markets stronger (banking reforms) and broader (equity markets deep and liquid) More international flows of capital, including by institutional investors who have longer-term horizons; new financial instruments

and broader (equity markets deep and liquid) More international flows of capital, including by institutional investors who have longer-term horizons; new financial instruments.")

39

India’s Share of Gross Inflows to Emerging Markets and Other Developing Countries

40

India’s Share of Gross Outflows from Emerging Markets and Other Developing Countries

41

But … May still be below threshold levels of financial, institutional development Managed exchange rate; absence of singular focus of monetary policy on inflation objective Surges in inflows create macro complications Financial markets still have way to go: bond markets not working well, banking sector problems tied in with other aspects of government policy (fiscal) Many imperfections in international financial markets: herding behavior; incomplete markets; risks in system harder to trace

Many imperfections in international financial markets: herding behavior; incomplete markets; risks in system harder to trace")

42

Interest Rate Differentials Relative to U.S.

43

Outstanding Stock of Market Stabilization Bonds (in billions of INR)

")

44

Implications Best to actively manage process of capital account liberalization rather than fight the inevitable Seize windows of opportunity when benefit-risk tradeoff improves; but coast is never completely clear. Capital account liberalization not an end in itself; needs to be put in the context of a more complete policy/reform agenda

45

Extra Slides

46

Chinas Foreign Exchange Reserves: (bi llions of U.S. dollars)

")

47

Growth Accounting for More Financially Open Economies (MFO) (1966-1985 and 1986-2005)

( and )")

48

Growth Accounting for Less Financially Open Economies (LFO) (1966-1985 and 1986-2005)

( and )")

49

Does the Composition of External Liabilities Matter?

Similar presentations

; Kaminsky,>")