Download presentation

Presentation is loading. Please wait.

1

Investing

2

When You’re “Young, Fabulous and Broke” You’re dealing with: College costs, maybe student loans Starting a career and low early wages Needing to start saving EARLY for retirement Needing to buy a house, the sooner the better If you’re female, maybe starting a family and maybe not wanting to work at all!

3

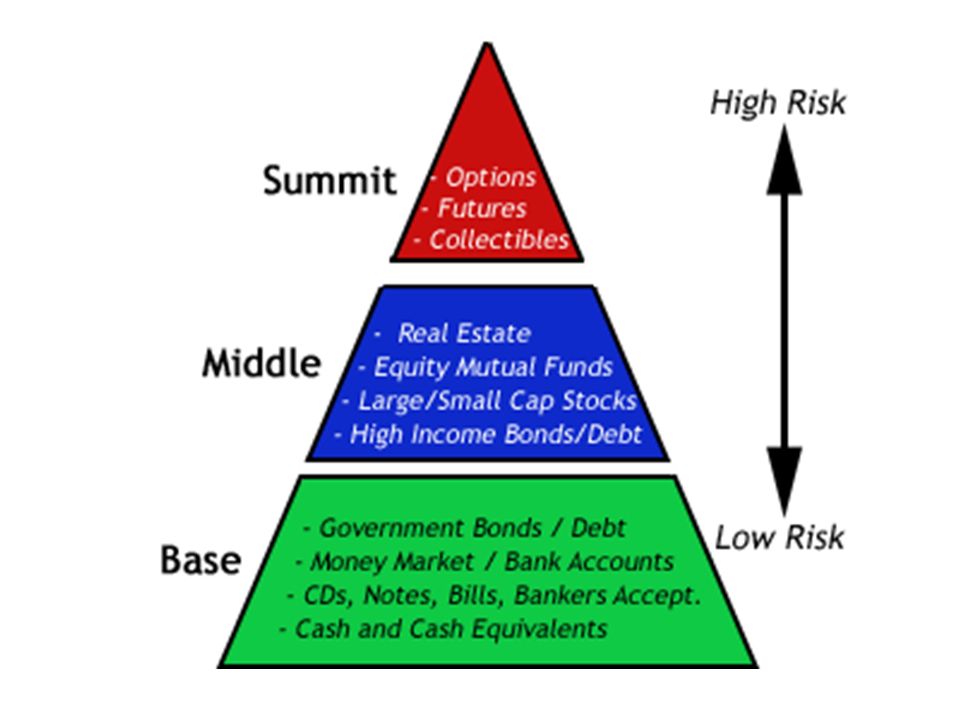

It’s all about … Risk – in your portfolio Debt management – debt will probably be a reality – high FICO score = low interest rate! Timing – take advantage of your youth in investing early!!

4

Retirement Funds IRA’s and 401k’s are not investments – they are containers that you fill with investments You generally can’t access this money until age 59 ½ There is a limit to how much you can put into them, since there are tax benefits

5

Retirement Funds – 401k’s These are offered by many employers The money you put into them is tax deferred, which means it is worth a lot more Some employers will offer to match your contribution – this is “free money” you should not turn down! You have to enroll in the 401k and choose your investments

6

IRA’s – Individual Retirement Accounts Anyone can open an IRA Traditional IRA’s –Contributions are tax deferred –Earnings are taxed when you withdraw them Roth IRA’s –Contributions are not tax-deferred BUT –Earnings are not taxed when you withdraw them –You can borrow money from them with no penalty, so they can serve as an emergency fund

7

Long-Term Options If you won’t need the money invested for over ten years: Stocks Bonds Mutual funds

8

Short-Term Options If you are saving for a car or house down-payment, for example: Savings account Money Market account Certificate of Deposit (CD)

")

9

Stocks Stocks are “equity,” or ownership in a company. You get one vote per share in electing the Board of Directors. You earn money through: –Dividends (rarely these days) –Price going up (you hope)

–Price going up (you hope).")

10

Stocks Advantages: –You may make more money –Stocks have risen about 10-12% per year historically Disadvantages –You could lose all your money

11

Buying Stocks Stock exchanges – real places in New York (NYSE), London, Hong Kong, etc. Over-the-Counter (OTC) – “virtual exchange” You can buy in person at a brokerage, over the phone, or online. You pay a commission for every trade.

– virtual exchange You can buy in person at a brokerage, over the phone, or online. You pay a commission for every trade..")

12

Types of Stocks Size Large cap (market capitalization, or total number of a company’s shares times their price) Medium cap Small cap Type Growth – high potential growth; higher risk Value – large, established companies with good track records Blend

Medium cap Small cap Type Growth – high potential growth; higher risk Value – large, established companies with good track records Blend")

13

Stock Indices Dow Jones Industrial Average – 30 stocks Standard & Poor 500 – 500 large, established stocks NASDAQ – all stocks in this exchange – usually small & tech stocks Wilshire 500 – broad variety of stocks

14

How do you know what to buy? Buy a mutual or index fund and let someone else decide! Research industries, companies, etc. Price/Earnings or other ratio Follow experts’ advice

15

Bonds Bonds are “debt,” and have a fixed rate of return. There is less risk, and less potential to make money.

16

Maturity Times Bills – under one year Notes – 1-10 years Bonds – over 10 years (The longer the maturity time, the more bonds pay)

")

17

Bond Terminology Face or Par Value – the original price of bonds upon issuance Coupon – interest the bonds pays, either quarterly, annually, etc. Price – what they sell for between issuance and maturity Current yield – coupon divided by price When price goes down, yield goes up, and vice versa

18

Types of Bonds Corporate Treasury Bills (T-bills) – safest U.S. Savings Bonds Municipal Bonds – pay no federal tax on earnings

19

Rating of Bonds AAA – safest B & C – “junk” – high-risk, high-yield D – in default

20

Mutual Funds Consist of many stocks and/or bonds A small investor can gain “instant diversification” Reinvesting the dividends is what creates the “miracle of compounding”

21

Types of Mutual Funds Actively Managed - by a fund manager Index –Managed by computer –Stocks matching a particular index are purchased –Very low management fees –As good or better returns than managed funds Exchange-Traded (ET’s) –Traded on stock exchange, usually Amex –Often specialize in a certain type of stocks –Can be traded at any time of the day instead of having to wait until the end of the day

–Traded on stock exchange, usually Amex –Often specialize in a certain type of stocks –Can be traded at any time of the day instead of having to wait until the end of the day")

22

What to look for in Mutual Funds No-Load – you shouldn’t have to pay a commission or “load” when buying or selling –Load funds have “A” or “B” at the end of their names – avoid them Low expense ratio –Average - 1.5% –Vanguard 500 -.18% Good track record Suze Orman says NO variable-rate annuities

23

Short-Term Investments From lowest to highest interest rate: Interest bearing checking account Savings account Money Market Funds –You can withdraw money at any time Certificates of Deposit (CD’s) –30 day to 1 year rates of maturity

–30 day to 1 year rates of maturity")

Similar presentations

at a financial institution. Certificates of.>")