Download presentation

Presentation is loading. Please wait.

1

ACCG 11900 Introduction to Accounting A

Lecturer - Ian Crawford Clinics - Fridays, , 0C2 Notices - See Economics Dept.

4

Financial Accounting External reporting/users Legal requirements

Financial information Annual Past events

6

Fundamental Accounting Concepts

Accruals (matching) Consistency Prudence Going concern Substance over Form

Consistency. Prudence. Going concern. Substance over Form.")

7

Rules Which Affect Accounts

Accounting Standards / Accountancy bodies Companies Acts / Company Law Stock Exchange Requirements Audit Reports / Auditing legislation Taxation Requirements

8

Forms of Businesses Business is always accounted for separately

Sole Traders (single owner) Partnerships (multiple owners) Companies (single or multiple owners) LLPs (multiple owners)

Partnerships (multiple owners) Companies (single or multiple owners) LLPs (multiple owners)")

9

Incorporation as a Company

Limited liability of owners Taxation differences (corporation tax not personal income tax) Succession and control (company is independent of its owners) Greater financing opportunities (e.g. listed companies sell shares to the public) Costs of compliance and administration

Succession and control (company is independent of its owners) Greater financing opportunities (e.g. listed companies sell shares to the public) Costs of compliance and administration.")

10

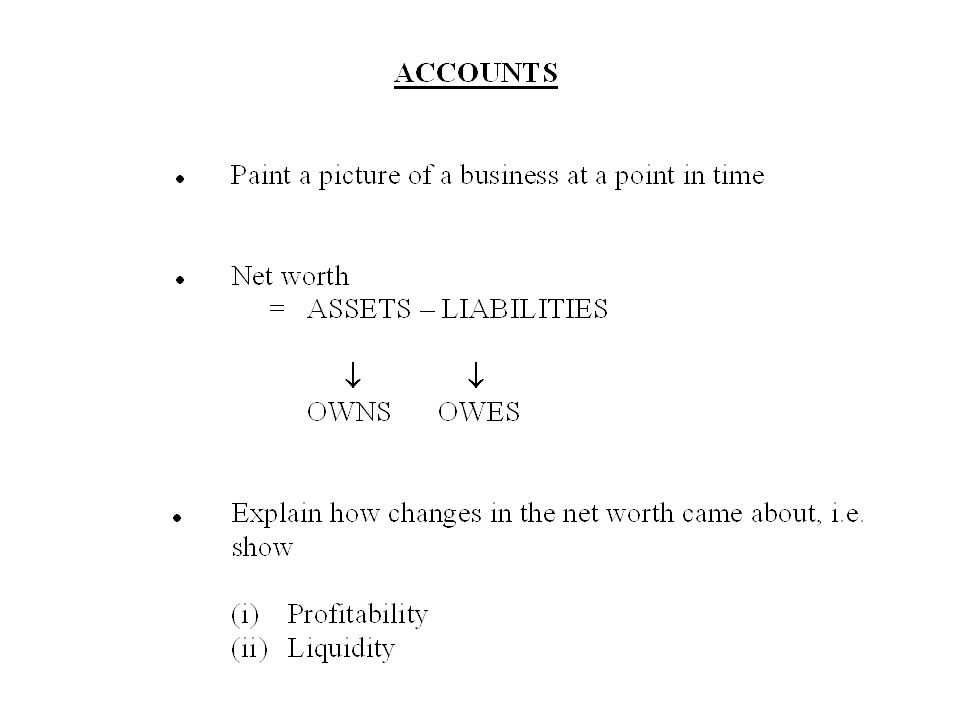

3 Main Financial Statements

Balance Sheets: Show: ‘A snapshot of a business at a point in time.’ Show: The net worth of a business. Net Worth = Owners’ equity. Profit and Loss Accounts: Show: The profitability of the business. Explain changes in Net Worth. Cash Flow Statements: Show: The liquidity of the business. Show: Sources and applications of funds. Explain changes in cash

11

show them Somerfield accounts explain assets, liabilities point out layout of items

12

Balance Sheets Show: snapshot of business at point in time (the balance sheet date) net worth = net assets = total assets - total liabilities working capital (= net current assets) owners’ equity (= capital + reserves) sources of finance (= owners’ equity + long-term liabilities)

owners’ equity (= capital + reserves) sources of finance (= owners’ equity + long-term liabilities)")

13

The Balance Sheet Equation

Net Worth = Owners’ Equity Horizontal Format: Total Assets = Total Liabilities + Owners’ Equity Vertical Formats: 1 Fixed Assets + Working Capital - Long-Term Liabilities = Owners’ Equity 2 Fixed Assets + Working Capital = Long-Term Liabilities + Owners’ Equity

14

Discuss pictorial representation, Bristol Industries and Invented Ltd

Point out differences in vertical formats note horizontal format as example 2.2 in textbook Explain briefly what each item is Start talking about differences between company accounts and other business accounts (e.g. proprietor’s capital) Capital and reserves: If you don’t know how much was invested or brought forward from last year, and how much is this year’s profit, just use the total figure.

Capital and reserves: If you don’t know how much was invested or brought forward from last year, and how much is this year’s profit, just use the total figure.")

15

Impact of Different Business Forms

The owners’ equity bit at the bottom of the balance sheet changes depending on the business form Sole trader no share capital, just capital. No dividends - drawings may be either in P&L or B/S Partnership like sole trader, but show each partner’s share separately Company share capital and reserves, dividends in P&L

16

Profit and Loss Accounts

Show: history book of transactions over past period prepared on accruals basis (matching) explains changes in net worth from one balance sheet to the next profit = income - expenditure income = sales revenue (turnover) + other expenditure = cost of sales + expenses (+ divs) COS = op. Stock + purchases - cl. stock

explains changes in net worth from one balance sheet to the next. profit = income - expenditure. income = sales revenue (turnover) + other. expenditure = cost of sales + expenses (+ divs) COS = op. Stock + purchases - cl. stock.")

17

Discuss Invented Ltd, esp

Discuss Invented Ltd, esp. with reference to dividends, and net profit/operating profit/PBIT. Note bank interest (on overdraft) is part of operating profit Explain idea of depreciation - non cash item

is part of operating profit. Explain idea of depreciation - non cash item.")

18

Cash Flow Statements Show: Remember:

history book of cash flows over past period liquidity (without cash, businesses fail) sources and applications of funds explan changes in cash from one balance sheet to the next Remember: profit is not the same as cash, and cash is not the same as profit

sources and applications of funds. explan changes in cash from one balance sheet to the next. Remember: profit is not the same as cash, and cash is not the same as profit.")

19

Discuss Invented Ltd note depreciation is added back as it is a non cash item - explain (briefly) what it is (again!)

what it is (again!)")

20

Balance Sheet Examples (remember the impact of different business forms)

A. Dr Seatham Rythe

21

B. Fast and Furious

22

C. Cosmetics Ltd

23

The Ashton Company This is still a simple example, but notice that there are ‘incomplete records’ This is very common - get used to it now! Here the only missing information is the retained profit reserve for the balance sheet - we can work it out because we know that the balance sheet should balance In future questions could be missing figures for sales, debtors, purchases, creditors, etc. Pay careful attention to the layout

24

How Transactions Affect the Balance Sheet

1. Joe Smith invests £1,000 cash in his new business.

25

How Transactions Affect the Balance Sheet

2. The business spends £100 cash on stock.

26

How Transactions Affect the Balance Sheet

3. The stock is sold for £150 cash. What would have happened if the stock was sold on credit?

27

How Transactions Affect the Balance Sheet

4. More stock costing £50 is bought on credit.

28

Profit and Loss Account for this Example

29

The Ashton Company Again

We have the opening balance sheet (p.19) We are told what transactions have occurred over the past period (September) We have to piece together the new (closing) balance sheet, and the profit and loss account Remember to distinguish cash and profit

We are told what transactions have occurred over the past period (September) We have to piece together the new (closing) balance sheet, and the profit and loss account. Remember to distinguish cash and profit.")

32

Cash Flow Statements Remember, these explain changes in cash

First, calculate the net cash flow from operating activities, adding back non-cash items to operating profit (=net profit=PBIT) Depreciation is a non-cash item depreciation is way of spreading the cost of a fixed asset over its useful economic life (application of the accruals concept) it is deducted from fixed assets in the balance sheet (accumulated amount), and from the P&L account (charge for period only)

Depreciation is a non-cash item. depreciation is way of spreading the cost of a fixed asset over its useful economic life (application of the accruals concept) it is deducted from fixed assets in the balance sheet (accumulated amount), and from the P&L account (charge for period only)")

33

Go through first example NOTE ERROR RE OPERATING PROFIT!

see corrected version on additional handout NOTE ERROR RE INTEREST PAID! Nick’s Newsmart example

Similar presentations

Then use the navigation.>")