Download presentation

Presentation is loading. Please wait.

1

Economic Forces in American History Banks and Bank Regulation

2

Economic Forces in American History Two Options Tomorrow morning I am scheduled to give a session on “Money and Monetary Policy.” I’ll talk about late 19 th century questions and the establishment of the Federal Reserve. I can also spend a session focusing on the economic crises in the 1830s and 1840s. The Bank War, specie circular, the state default crisis and constitutional changes in the 1840s.

3

Economic Forces in American History Legal Tender During the revolution the federal government (through the Congress) and the state governments were issuing money. These notes circulated as money because they were “legal tender.” That is, they were good for the settlement of “all debts, public and private.” At root, this meant you could pay your taxes with them.

4

Economic Forces in American History The Constitution prohibited states from “emitting bills of credit.” This clause was intended to give the national government control over the money supply. Federal government finances during the Revolution were a mess, and the national debt was somewhere in the neighborhood of $54 million at the end of the war. The Constitution gave the national government the power to raise taxes. Under Hamilton’s financing plan, the federal government replaced all existing federal and state debt with new federal bonds.

5

Economic Forces in American History Hamilton’s policies also created a national bank, chartered by the national government: The First Bank of the United States The BUS had branches throughout the country and acted as the federal government’s bank. The federal government also issued gold and silver coins. These were legal tender as well, and circulated throughout the country, although usually either gold or silver circulated but not both. This mean the United States was on a physical ‘gold standard’

6

Economic Forces in American History Money Banks borrow resources by issuing bonds that pay no interest and are payable to the bearer. These promises to pay are what we call ‘money.’ In the early 19 th century, paper money was redeemable in demand in gold or silver, specifically in gold coins. Today, most of the liabilities of the banks are in the form of deposits, and most of the money in the United States is in the form of checking account balances.

7

Economic Forces in American History Bank Notes Bank notes are the liabilities of the Bank that issued them They were typically payable on demand in specie (gold coins). In most states the privilege of issuing notes requires a corporate charter, and the charter is revocable if the Bank does not redeem notes on demand.

8

Economic Forces in American History

9

Commercial banks make money on the loans they make, and the primary form of loan is commercial paper/bills of exchange. Typically, investors bought stock in the bank and paid with gold and silver coins, what is also known as “specie”

10

Economic Forces in American History Suppose the bank could make loans at 10% interest. CapitalAssetsLiabilities $100 BuyIssue Profit LoansNotes $80$80$8 $160$160$16 $320$320$32

11

Economic Forces in American History The problem for the bank had two sides that had to be balanced. On one side, the more loans it made the more profits it made. On the other side, the more notes it issued the greater the likelihood that note holders (who are the creditors of the bank) would come in and demand that their notes be converted into specie (gold coins). If the bank’s specie reserves were less than their notes outstanding, this could be a real problem.

would come in and demand that their notes be converted into specie (gold coins). If the bank’s specie reserves were less than their notes outstanding, this could be a real problem..")

12

Economic Forces in American History Most banks also took deposits. That makes the situation more complicated, but the same logic applies. Deposits are liabilities of the bank, for which it receives a corresponding asset, in this case gold coins. (We’ll forget about bank capital for a moment). Reserves Gold CoinsDepositsLoansNotes (Assets)(Liabilities)(Assets) (Liabilities) $100 $100 $80$80 $100$100 $80$80 (in red because this is the same as above)

. Reserves Gold CoinsDepositsLoansNotes (Assets)(Liabilities)(Assets) (Liabilities) $100 $100 $80$80 $100$100 $80$80 (in red because this is the same as above).")

13

Economic Forces in American History Reserves DepositsLoansNotes (Assets)(Liabilities)(Assets) (Liabilities) $100$100$80$80 Suppose the notes get deposited $80$64$64 And again $64$51$51

(Liabilities)(Assets) (Liabilities) $100$100$80$80 Suppose the notes get deposited $80$64$64 And again $64$51$51")

14

Economic Forces in American History Since everyone who makes a deposit (of gold coins or bank notes) thinks they have money equal to the amount of their deposit, the money supply goes up every time a deposit is made. Reserves DepositsLoansNotes (Assets)(Liabilities)(Assets) (Liabilities) $100$100$80$80 $80$64$64 $64$51$51 ….….…. Totals $100 $500$400

(Liabilities)(Assets) (Liabilities) $100$100$80$80 $80$64$64 $64$51$51 ….….…. Totals $100 $500$400.")

15

Economic Forces in American History Fractional Reserve The bank has created $500 in money (bank liabilities) in the form of deposits and notes, but the bank only holds $100 in the form of reserves that the bank has on hand to convert the deposits and notes into gold coins. This is why this is called a fractional reserve system. The bank is solvent, its assets are worth more than its liabilities, but it is also ‘illiquid’. It holds assets that are less liquid than its liabilities.

16

Economic Forces in American History Money Multiplier The extent to which the banking system can take and initial infusion of resources (a deposit of gold coins for example) and convert it into money is called the ‘money multiplier.’ In the simplest terms, the ‘reserve ratio’ is the ratio of reserves available to meet depositor or note holders demands, relative the size of bank liabilities: RR = reserves/liabilities The money multiplier is the inverse of the RR MM = 1/RR = liabilties/reserves

and convert it into money is called the ‘money multiplier.’ In the simplest terms, the ‘reserve ratio’ is the ratio of reserves available to meet depositor or note holders demands, relative the size of bank liabilities: RR = reserves/liabilities The money multiplier is the inverse of the RR MM = 1/RR = liabilties/reserves")

17

Economic Forces in American History During the Civil War, the National Banking System made it prohibitively expensive for state chartered banks to issue bank notes, so the state banks began creating checking account balances. Checking Reserves DepositsLoans (Assets)(Liabilities)(Assets) $100$100$80 $80$64 $64$51 ….….…. Totals $100 $500$400

(Liabilities)(Assets) $100$100$80 $80$64 $64$51 ….….…. Totals $100 $500$400.")

18

Economic Forces in American History The system of banking where most of the money supply is held in checking account balances (demand deposits), is more or less the system we still have today. Bank note issues gradually declined in importance over the end of the 19 th century. Today currency is issued by the Federal Reserve Banks, though it is printed by the Treasury.

19

Economic Forces in American History Financial Intermediaries One of the primary functions of financial intermediaries is to convert short term liabilities into long term assets. The bank has short term liabilities, the assets of note holders and depositors (what is one person’s liability is another person’s asset!) The bank has enabled people to deposit short term funds and borrow for longer terms. What did they borrow?

The bank has enabled people to deposit short term funds and borrow for longer terms. What did they borrow .")

20

Economic Forces in American History Financial Markets In credit markets, reputation matters. Bills of Exchange were credit instruments, bonds, issued in the course of a commercial exchange. Banks dealt in Bills, exchanging their own liabilities – bank notes – for the bills. Wheat and other goods moved in a national market; bills of exchanged moved in a parallel national market; bank notes or gold did not need to move in a national market (except to balance accounts).

..")

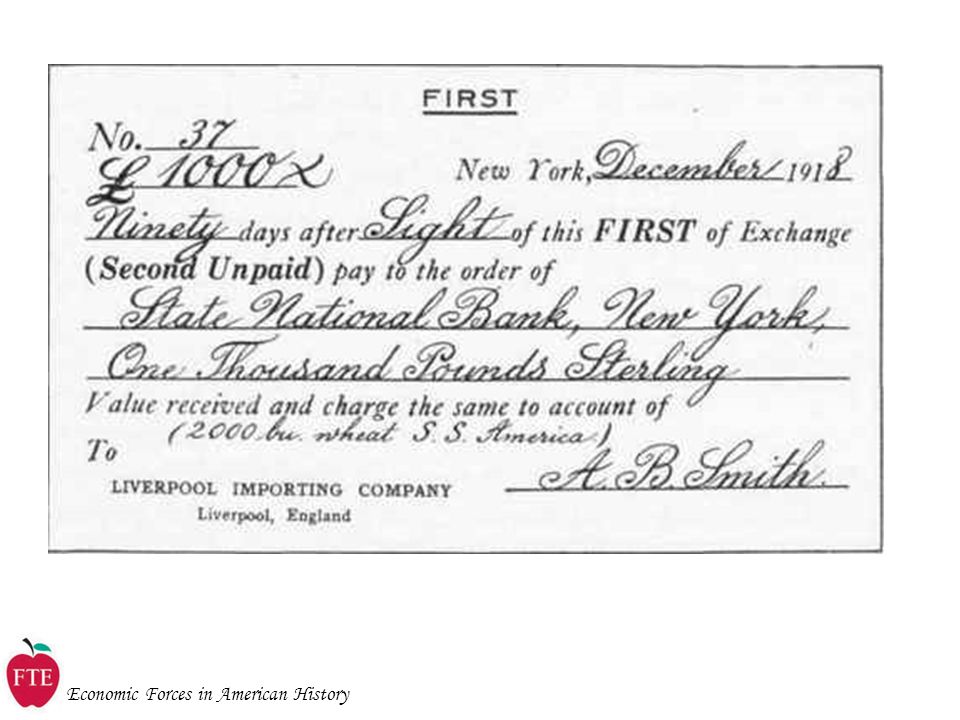

21

Economic Forces in American History Bill of Exchange A Bill looks like this: Pay $100 to Farmer Jones, 60 days from presentation, at the office of Miller Smith in New York. Signed: ________

22

Economic Forces in American History

24

IndianaNew York FarmerMiller Wheat Bill IN Notes Bill NY Notes Bank/Agent INBank/Agent NY Bill Bill payable in Indiana from another transaction

25

Economic Forces in American History Three Transactions IndianaNew York FarmerMiller Wheat Bill IN Notes Bill NY Notes Bank/Agent INBank/Agent NY Bill Bill payable in Indiana from another transaction

26

Economic Forces in American History Three transactions Note that rather than one transaction of wheat for money, a more complicated (but also cheaper) transaction took place in three independent steps using the bill of exchange. In the first step the Indiana farmer sold the bill to a bank in Indiana, for cash in the form of the bank notes of the Indiana bank. The Indiana bank sold the bill to a New York bank, usually by buying an bill payable in Indiana. The New York bank presented the bill for payment at the Miller in New York, the bill was paid with New York bank notes.

27

Economic Forces in American History Bank Regulation Banks could be regulated in several ways: Regulating entry Regulating reserves – What kind of reserves banks had to hold. – How many reserves banks had to hold, often as a percentage of liabilities. Regulating loans – What kinds of loans banks could make, which is also regulating the kind of assets that banks could hold. Regulating Capital

28

Economic Forces in American History Regulating Reserves A state, nation, central bank, or any other kind of bank regulator, exerts direct control over the money multiplier by effecting the amount of reserves a bank is required to hold. Remember, RR = reserve ratio = reserves/laibilities Money multiplier = 1/RR

Similar presentations

Banks 2) How Banks Create Money 3) The Money Multiplier Banks have several important functions 1.Store.>")