Download presentation

Presentation is loading. Please wait.

1

2014

2

* Payroll * The process used by an organization to pay its employees accurately and on time

4

* Complexity * Monitor and implement federal, state, and local tax laws * FPC Testing is based on Federal Law * Communication * Paychecks, paycards, vouchers – must be timely, accurate, and easily understood – must be clear and concise * Technology * Software, equipment, and web-based applications can automate and enhance payroll processing, timekeeping, and record storage * Accuracy * Required for tax filing, management reports, and paychecks

8

Worker Status Employees Need to provide SSN and W-4 Nonexempt ees subject to FLSA standards Taxes withheld and paid by the employer Receive a W-2 Independent Contractors Need to provide an TIN and W-9 Taxes withholding not required Receive a 1099-MISC

9

Temporary/Leased Employees Agency and company have a contractual agreement Workers are employees of the agency but subject to company policy Agency bears the burden of paying, withholding taxes, reporting, and administering benefits for these workers Worker Status (continued)

")

12

* The IRS imposes fines and penalties when employees are mistakenly classified as independent contractors. Treat the worker as an employee to avoid non- compliance and penalties and: * Seek public ruling information * Request private ruling from the IRS

13

* My new hire is an employee. * What’s the next step?

14

* Immigration Reform and Control Act of 1986 * I-9 Employment Eligibility Verification * Required to prove identity and right to work * Employers can face stiff penalties for knowingly hiring workers not eligible for employment: from $375 for first offense to $16,000 for third offense, or if a pattern of violations exists, criminal charges

15

* Form W-4 * Federal Employee Withholding Allowance Certificate * Employee completes W-4 during hire process * Employer can request SS card to verify SSN * SSNVS Social Security Number Verification System & E-Verify

16

* Hire Date * Employee completes Section 1 * Within first 3 days at work * Employer reviews and completes Section 2 * Retention * 3 years OR 1 year after termination

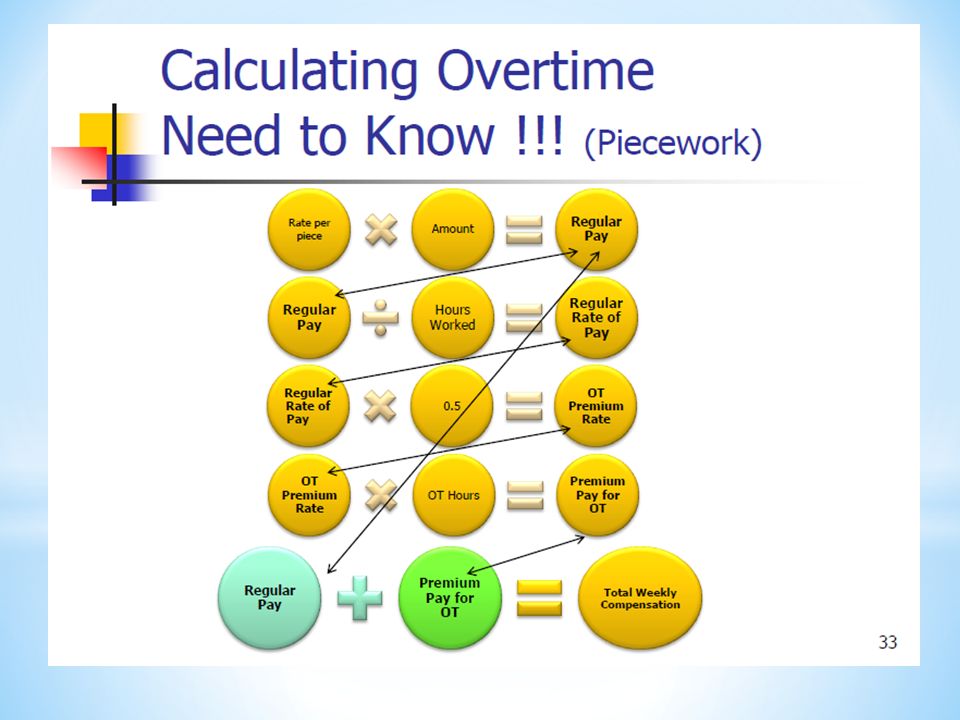

36

W4 – Federal Employee Withholding Allowance Certificate Requested when hired and for life changes Default is Single with 0 exemptions Alterations, flat dollar amounts, and percentages are invalid Exempt status – filed annually, earns less than tax exemption No IRS notification unless requested Retain for 4 years from last 1040 filing or 1 year from termination The “W” Forms

37

W4P - Withholding Certificate for Pension or Annuity Payments Default is Married with 3 exemptions Additional amount is allowed

38

W4S - Request for Federal Income Tax Withholding from Sick Pay 3 rd Party wage payment for illness or injury that is non- job related Minimum withholding is $20/week Minimum net pay of $10 Many states require tax withholding

Similar presentations