Download presentation

Presentation is loading. Please wait.

1

Erkan Kara, Ph.D. Candidate Department of School of Applied Sciences Konya Necmettin Erbakan University, Turkey Corporate Governance and Share Prices: Firm Level Review in Turkey

2

OBJECTIVE: The main objective of this research is to investigate the relationship between corporate governance rating and stock prices of 26 Turkish firms listed in Turkish Stock Exchange (Borsa Istanbul) and comparing these firms’ stock performance (return) with the main market both prior and after corporate scoring began. Method used: Panel data analysis by using Eviews.

3

SUMMARY OF LITERATURE: Over the couple of decade many studies have focused on determining the relation between corporate governance and share prices. Many of them found positive relation (Gompers, Ishii and Metrick (2003); Kowalewski (2012); Balasubramanian et al. (2011); Rahman (2010); and Karamustafa et al. (2009)). Others found negative relation (Aman and Nguyen (2008); Kilic (2011) and Dincer and Dincer (2013).

; Kowalewski (2012); Balasubramanian et al. (2011); Rahman (2010); and Karamustafa et al. (2009)). Others found negative relation (Aman and Nguyen (2008); Kilic (2011) and Dincer and Dincer (2013)..")

4

DATA AND METHODOLOGY: Data of 26 firms are collected from a security trading firm and Borsa Istanbul. First, each firm’s stock prices were adjusted for stock splits and dividend paid. Later, corporate governance rating of firms taken and used for panel data analysis. Panel data help us to collect data over time and over the same individuals and then regress these two dimensions.

5

DATA AND METHODOLOGY: As stated in the objective section, we, firstly, found relation between corporate governance rating and share prices. To do that panel data analysis was used. Secondly, we found the performance of the firms with governance rating with comparison to main market return in two periods. For panel data analysis, we constructed the following model:

6

Where, SP is dependent variable and CG is independent variable, consisting 26 firms (cross sectional element) and with time horizon between 2009 and 2013 (time- series element).

and with time horizon between 2009 and 2013 (time- series element).")

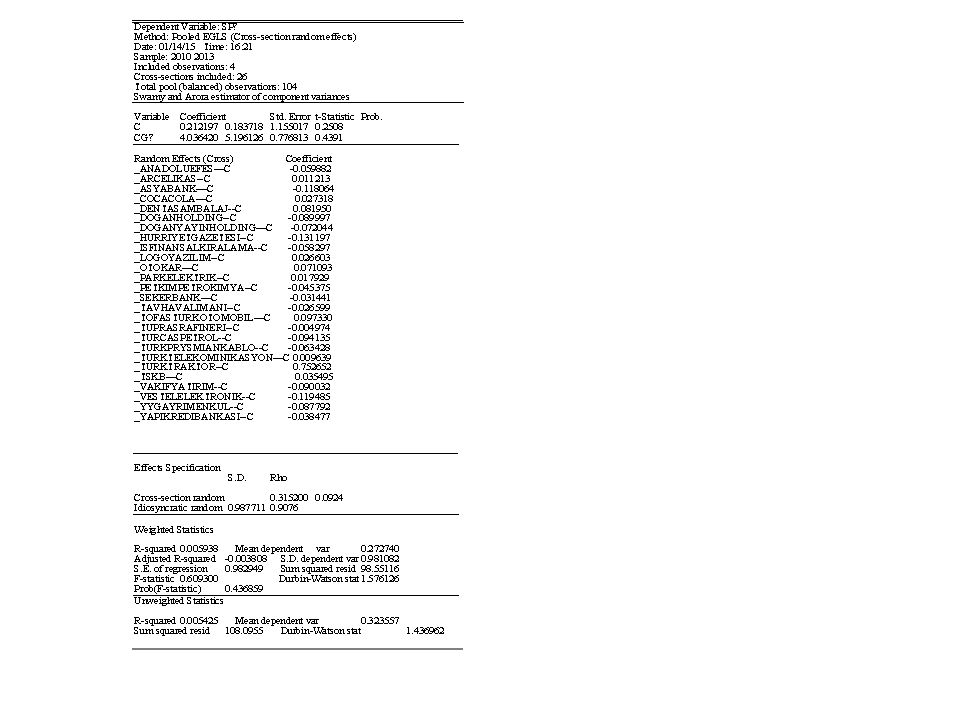

7

REGRESSION RESULTS: After running regression, we had the following estimated coefficient for the model: The numbers in the parenthesis indicate the probability value of coefficents. The regression results suggest that the parameters value are not significant. And when looking at R 2 value, independent variable, i.e corporate governance, explain only 0,6% stock price changes.

9

FIRMS PERFORMANCE COMPARISON: Performance of the firms prior to being rated (2004- 2008):

:")

10

FIRMS PERFORMANCE COMPARISON: Performance of the firms after being rated (2000-2013):

:")

11

CONCLUSION: Having done the above estimation of panel data and finding the stock price performance of the rated firms, the result of this study is not in line with the works of (Gompers, Ishii and Metrick (2003); Kowalewski (2012); Balasubramanian et al. (2011); Rahman (2010); and Karamustafa et al. (2009) which found that good corporate governance lead higher performance for the firms. And, finally, our results support the findings of (Aman and Nguyen (2008); Kilic (2011) and Dincer and Dincer (2013).

; Rahman (2010); and Karamustafa et al. (2009) which found that good corporate governance lead higher performance for the firms. And, finally, our results support the findings of (Aman and Nguyen (2008); Kilic (2011) and Dincer and Dincer (2013)..")

12

CONCLUSION: Though, as statistically found that there is no linkage between change in corporate governance rating and change in stock prices, the return performance of share prices over the return of main market portfolio indicate that firms’ annual share returns are higher than Turkey’s stock exchange return both on prior and after the firms being scored. However, the degree of stock outperformance declines over the years and become less influential at the second period when the firms have begun to be rated.

13

Hence, we conclude that corporate governance rating is not an important variable to determine stock prices on its own. Other than corporate governance rating, some other influential dynamics are behind the stock price movement such as stock exchanges direction, general economic outlook, firm specific characteristics and sectorial progresses. We should also note that this result does not mean that corporate governance rules are not important for the firms. Otherwise, they would not be listed in stock exchanges as this issue is crucial in terms of shareholders rights.

14

THANK YOU...

Similar presentations

Chung Yuan Christian University.>")

, Shaun Bond (University of Cincinnati), & Joseph Ooi (National University of Singapore)>")

>")