Download presentation

Presentation is loading. Please wait.

2

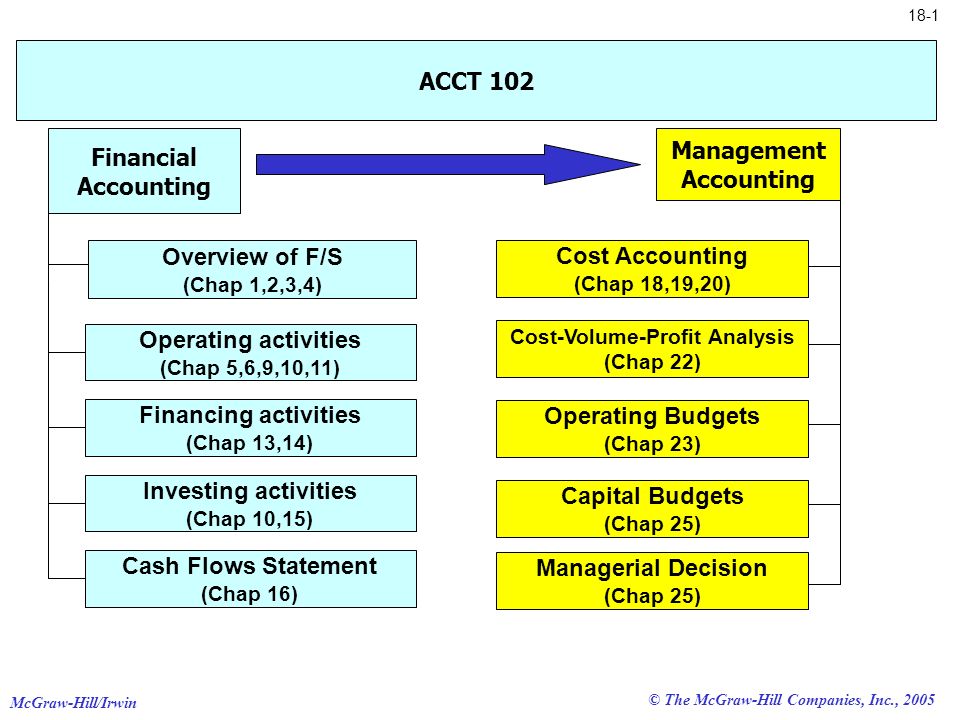

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-1 ACCT 102 Financial Accounting Overview of F/S (Chap 1,2,3,4) Cash Flows Statement (Chap 16) Investing activities (Chap 10,15) Operating activities (Chap 5,6,9,10,11) Financing activities (Chap 13,14) Management Accounting Cost Accounting (Chap 18,19,20) Cost-Volume-Profit Analysis (Chap 22) Operating Budgets (Chap 23) Capital Budgets (Chap 25) Managerial Decision (Chap 25)

Cash Flows Statement (Chap 16) Investing activities (Chap 10,15) Operating activities (Chap 5,6,9,10,11) Financing activities (Chap 13,14) Management Accounting Cost Accounting (Chap 18,19,20) Cost-Volume-Profit Analysis (Chap 22) Operating Budgets (Chap 23) Capital Budgets (Chap 25) Managerial Decision (Chap 25)")

3

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-2 Managerial Accounting Concepts and Principles Chapter 18

4

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-3 Learning objectives 1. Managerial Accounting Basics 2. Managerial Cost Concepts 3. Reporting Manufacturing Activities Balance Sheet Income Statement Flow of Manufacturing Activities Manufacturing Statement 4. Decision analysis: Unit Contribution Margin Contribution Margin Ratio

5

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-4 Managerial accounting provides information for managers of an organization who plan and control its operations. Financial accounting provides information to stockholders, creditors and others who are outside the organization. 1.Managerial Accounting Basics - Purpose Managerial Accounting

6

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-5 Planning Formulating Long- and Short-Term Plans Controlling 1. Measuring Actual Performance Implementing Plans Directing and Motivating Controlling 2. Evaluating Actual Performance versus Planned Performance Begin FEED BACK MONI TORING Planning and Control

7

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-6 1. Managerial Accounting Basics - Nature of Managerial Accounting

8

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-7 1. Managerial Accounting Basics - Increased Relevance of Managerial Accounting Customer Orientation Global Economy Lean Business Model Elimination of Waste Satisfy the Customer Positive Return

9

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-8 Lean Practices Customer Orientation in a Global Economy

10

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-9 on Quality throughout the production process. Rewards for employees who find defects. Employees encouraged to try new methods to improve quality. Company emphasizes value of quality through quality awards. Total Quality Management

11

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-10 Complete products just in time to ship to customers. Complete parts just in time for assembly into products. Receive materials just in time for production. Schedule production. Receive customer orders. Just-In-Time (JIT) Manufacturing

Manufacturing.")

12

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-11 New ways to improve operations Continuous Improvement

13

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-12 Labor Costs Variable Costs Use of Technology AutomationOverhead Fixed Costs Increase Decrease 1.Managerial Accounting Basics - Implications for Manufacturing Accounting

14

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-13 Behavior Traceability Controllability Relevance Function 2. Managerial Cost Concept - Cost Classification

15

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-14 Cost behavior means how a cost will react to changes in the level of business activity. Total fixed costs do not change when activity changes. Total variable costs change in proportion to activity changes. Classification by Behavior

16

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-15 Activity Cost Activity Cost Classification by Behavior Cost behavior means how a cost will react to changes in the level of business activity. Total fixed costs do not change when activity changes. Total variable costs change in proportion to activity changes.

17

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-16 Direct costs Costs incurred for the benefit of one specific cost object. Examples: material and labor cost for a product. Indirect costs Costs incurred for the benefit of more than one cost object. Example: maintenance expenditures benefiting two or more departments. Classification by Traceability

18

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-17 The degree of control depends on the level of management in the organization. More Control Very little control Classification by Controllability

19

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-18 The potential benefit that is given up when one alternative is selected over another. Example: If you were not attending college, you could be earning $20,000 per year. Your opportunity cost of attending college for one year is $20,000. Classification by Relevance: Opportunity Costs

20

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-19 All costs incurred in the past that cannot be changed by any decision made now or in the future. Sunk costs should not be considered in decisions. Example: You bought an automobile that cost $15,000 two years ago. The $15,000 cost is sunk because whether you drive it, park it, trade it, or sell it, you cannot change the $15,000 cost. Classification by Relevance: Sunk Costs

21

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-20 The Product Classification by Function: Product Costs Direct Labor Direct Material Manufacturing Overhead

22

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-21 Period costs are expenses not charged to the product. Classification by Function: Period Costs Administrative Costs Nonmanufacturing costs of staff support and administrative functions – accounting, data processing, personnel, research and development. Selling Costs Costs incurred to obtain customer orders and to deliver finished goods to customers – advertising and shipping.

23

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-22 Period Costs (Expenses) Product Costs (Inventory) Inventory Not Sold in 2005 Operating Expenses Cost of Goods Sold Raw Materials Goods in Process Finished Goods Cost of Goods Sold 2005 Costs Incurred 2005 Income Statement 2006 Income Statement 2005 Balance Sheet Inventory Inventory Sold in 2005 Period and Product Costs in Financial Statements

Product Costs (Inventory) Inventory Not Sold in 2005 Operating Expenses Cost of Goods Sold Raw Materials Goods in Process Finished Goods Cost of Goods Sold 2005 Costs Incurred 2005 Income Statement 2006 Income Statement 2005 Balance Sheet Inventory Inventory Sold in 2005 Period and Product Costs in Financial Statements")

24

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-23 Potential Multiple Cost Classifications

25

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-24 I suppose these same cost concepts apply to service companies. Cost Concepts for Service Companies

26

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-25 Merchandisers... Buy finished goods. Sell finished goods. SaleMart Manufacturers... Buy raw materials. Produce and sell finished goods. 3. Reporting Manufacturing Activities

27

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-26 Manufacturing Inventory Classifications 3. Reporting Manufacturing Activities - Balance Sheet of a Manufacturer Raw Materials Finished Goods Goods in Process

28

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-27 Completed products for sale. Materials waiting to be processed. Partially complete products. Material to which some labor and/or overhead have been added. Balance Sheet of a Manufacturer Raw Materials Finished Goods Goods in Process

29

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-28 MERCHANDISER Current Assets Cash Receivables Merchandise Inventory MANUFACTURER Current Assets Cash Receivables Inventories Raw Materials Goods in Process Finished Goods The only difference is inventory. Balance Sheet of a Manufacturer

30

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-29 Beginning Merchandise Inventory Beginning Finished Goods Inventory Cost of Goods Purchased Cost of Goods Manufactured Ending Merchandise Inventory Ending Finished Goods Inventory Cost of Goods Sold MerchandiserManufacturer + _ + == _ The major difference 3. Reporting Manufacturing Activities - Income Statement of a Manufacturer

31

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-30 Cost of goods sold for manufacturers differs only slightly from cost of goods sold for merchandisers. 3. Reporting Manufacturing Activities - Income Statement of a Manufacturer

32

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-31 Direct Materials Materials that are clearly and easily identified with a particular product. Direct Materials Materials that are clearly and easily identified with a particular product. Example: Steel used to manufacture the automobile. Example: Steel used to manufacture the automobile. Income Statement of a Manufacturer

33

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-32 Direct Labor Labor costs that are clearly traceable to, or readily identifiable with, the finished product. Direct Labor Labor costs that are clearly traceable to, or readily identifiable with, the finished product. Example: Wages paid to an automobile assembly worker. Example: Wages paid to an automobile assembly worker. Income Statement of a Manufacturer

34

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-33 Factory Overhead All factory costs except direct material and direct labor. Factory costs that cannot be traced directly to specific units produced. Factory Overhead All factory costs except direct material and direct labor. Factory costs that cannot be traced directly to specific units produced. Examples: Indirect labor – maintenance Indirect material – cleaning supplies Factory utility costs Supervisory costs Income Statement of a Manufacturer

35

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-34 Direct Material Direct Labor Manufacturing Overhead Prime Cost Conversion Cost Manufacturing costs are often combined as follows: Income Statement of a Manufacturer

36

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-35 Question What type of account is the manufacturing goods in process account? a.Income statement expense account. b.Balance sheet inventory account. c.Temporary clearing account for direct material and direct labor. d.Holding account for manufacturing overhead and direct labor. What type of account is the manufacturing goods in process account? a.Income statement expense account. b.Balance sheet inventory account. c.Temporary clearing account for direct material and direct labor. d.Holding account for manufacturing overhead and direct labor.

37

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-36 What type of account is the manufacturing goods in process account? a.Income statement expense account. b.Balance sheet inventory account. c.Temporary clearing account for direct material and direct labor. d.Holding account for manufacturing overhead and direct labor. What type of account is the manufacturing goods in process account? a.Income statement expense account. b.Balance sheet inventory account. c.Temporary clearing account for direct material and direct labor. d.Holding account for manufacturing overhead and direct labor. Question

38

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-37 Question The primary distinction between product and period costs is... a.Product costs are expensed in the period incurred. b.Product costs are directly traceable to product units. c.Product costs are inventoriable. d.Period costs are inventoriable. The primary distinction between product and period costs is... a.Product costs are expensed in the period incurred. b.Product costs are directly traceable to product units. c.Product costs are inventoriable. d.Period costs are inventoriable.

39

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-38 The primary distinction between product and period costs is... a.Product costs are expensed in the period incurred. b.Product costs are directly traceable to product units. c.Product costs are inventoriable. d.Period costs are inventoriable. The primary distinction between product and period costs is... a.Product costs are expensed in the period incurred. b.Product costs are directly traceable to product units. c.Product costs are inventoriable. d.Period costs are inventoriable. Question

40

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-39 Finished Goods Beginning Inventory Cost of Goods Manufactured Finished Goods Ending Inventory Raw Materials Beginning Inventory Raw Materials Purchases Raw Materials Ending Inventory Cost of Goods Sold Goods in Process Beginning Inventory Direct Labor Factory Overhead Raw Materials Used Sales activityProduction activity Materials activity 3. Reporting Manufacturing Activities - Flow of Manufacturing Activities Goods in Process Ending Inventory

41

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-40 Cost of all goods completed and transferred from goods in process to finished goods during a reporting period. Direct Materials Used +Direct Labor +Factory Overhead =Total Manufacturing Costs +Beginning Work in Process – Ending Work in Process =Cost of Goods Manufactured 3. Reporting Manufacturing Activities - Manufacturing Statement

42

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-41 Let’s take a look at Rocky Mountain Bikes’ Manufacturing Statement. Manufacturing Statement

43

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-42 Manufacturing Statement

44

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-43 Manufacturing Statement Exh. 18-16

45

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-44 Include all direct labor costs incurred during the current period. Manufacturing Statement

46

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-45 Manufacturing Statement Exh. 18-16

47

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-46 Beginning work in process inventory is carried over from the prior period. Manufacturing Statement Exh. 18-16

48

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-47 Ending work in process inventory contains the cost of unfinished goods, and is reported in the current assets section of the balance sheet. Manufacturing Statement Exh. 18-16

49

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-48 4. Decision Analysis - Unit Contribution Margin Contribution margin contributes to covering fixed costs and generating profits.

50

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-49 Unit Contribution Margin Contribution margin ratio is the portion of each sales dollar remaining after deducting total unit variable cost.

51

McGraw-Hill/Irwin © The McGraw-Hill Companies, Inc., 2005 18-50 End of Chapter 18

Similar presentations