Download presentation

Presentation is loading. Please wait.

1

The 3 rd Younger Members Convention 29-30 November 2004, The Chesford Grange Hotel, Kenilworth

2

The World Of Health Protection Peter Banthorpe Business Development Actuary, Munich Re UKLB Institute of Actuaries Healthcare Conference Organising Committee

3

The Bluffer’s Guide to Protection Peter Banthorpe Business Development Actuary, Munich Re UKLB Institute of Actuaries Healthcare Conference Organising Committee

4

What is Health Protection Insurance? Five Main Building Blocks: Customers Distribution Insurers Reinsurers Products

5

Critical Illness Insurance

6

CI Cancer Definition All tumours which are histologically described as pre-malignant, as non-invasive or as cancer in situ. All tumours of the prostate unless histologically classified as having a Gleason score greater than 6 or having progressed to at least TNM classification T2N0M0. All forms of lymphoma in the presence of any Human Immunodeficiency Virus. Kaposi's sarcoma in the presence of any Human Immunodeficiency Virus. Any skin cancer other than invasive malignant melanoma. Any malignant tumour characterised by the uncontrolled growth and spread of malignant cells and invasion of tissue. The term cancer includes leukaemia and hodgkin’s disease but the following are excluded:

7

Products Income Protection (PHI) Private Medical Insurance Long-term Care Insurance Life Assurance Packaged Products Group and Individual SA1 / ST1 Exam Critical Illness Insurance

Private Medical Insurance Long-term Care Insurance Life Assurance Packaged Products Group and Individual SA1 / ST1 Exam Critical Illness Insurance")

8

Distribution Brokers Banks Tied Agents Direct Sales Forces Direct Marketing

9

Mix of Sales By Channel Source: ABI. Products considered: Life, CI and IP. Mix by Total New Premiums in 2003

10

Insurance Companies Household names Niche players Sales and Marketing Administration Underwriting capacity Claims Processing Legal construction Labour Intensive

11

Relative Size of Insurers Source: Munich Re analysis of FSA returns. Based on new protection business in 2003.

12

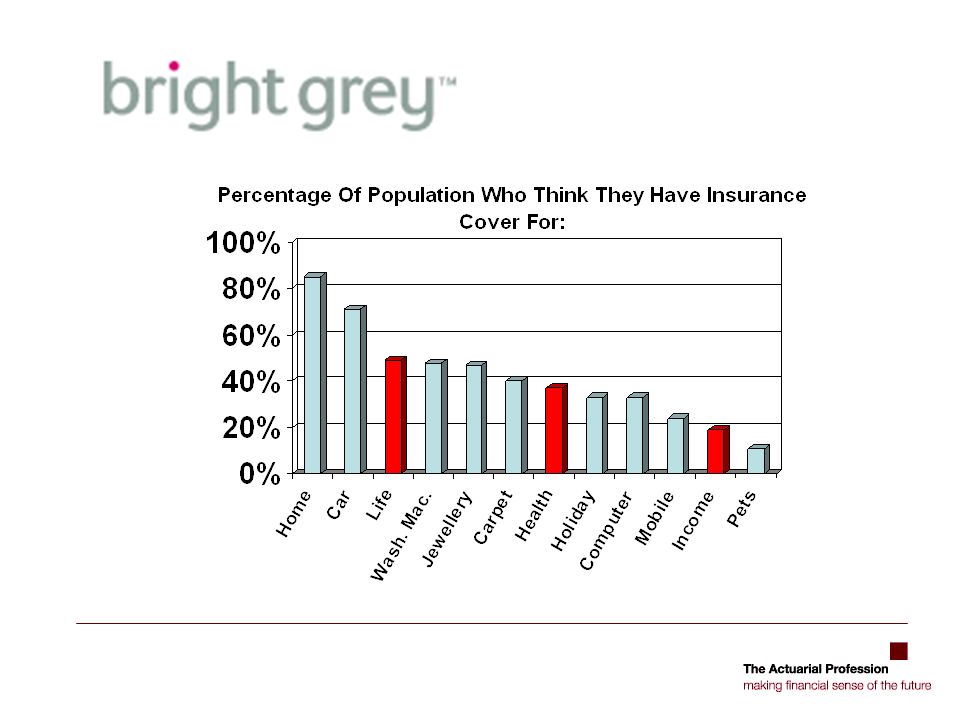

Why Protection is Important Source: ABI.

13

Reinsurers “9” reinsurers in the Life & Health market Provide capacity – risk wholesalers Mitigate new business strains Allow more competitive premiums Data – information for pricing Product development advice Facilitate underwriting Claims experience Operational Risk

14

Relative Size of Reinsurers Source: Redmayne Report 2004. Relative size judged on Regular Premium Earned

15

Current issues Inappropriate sales Regulation Guaranteed rate critical illness Reviewable premiums Service

16

Sales of Protection Products Source: ABI, this may understate Term Life sales versus CI Sales in the early years No of Policies – 000s

18

‘We think CI is a luxury product and for most people it’s more important that you have adequate life insurance and IP in place before thinking about CI’. ‘Worryingly, sales of CI are much higher than IP. We are concerned that advisers are pushing CI policies when IP would be more suitable and that many people simply don’t have adequate protection in the event of their being unable to work.’ September 2003

19

Regulation: Demands and Needs General Insurance Regulation Impact on protection market Mortgage payment protection insurance Fact-finds at all levels More IP, Less CI? Big issue for FSA

20

Regulation - Depolarisation Insurer 1 Insurer 2 Insurer 3 Insurer 4 Tied Agent Multi-tie Independent Financial Advisor Different regime for different products Different regime for different clients

21

Regulation Individual Capital Assessments Realistic capital => risk based capital How much capital for: 1.100 life assurance policies all of £1 each for identical lives 2.1 life assurance policy for £100 for one identical life European Reinsurance Directive Allowance for reinsurance credit risk

22

Guaranteed Rate Critical Illness Price Increases of 20%-30% over past two years Some reinsurers withdraw capacity…. ….some reinsurers increase capacity

23

Reviewable Premium Contracts If you don’t guarantee premiums then can you review them? Legal interpretation FOS interpretation Client doesn’t understand Client can’t understand Unfair contract term

24

Service How insurance companies compete: Product Product and Price Product, Price and Service

25

Protection into The Future PruHealth “Virtual” Insurance Companies New CI Products Better IP Products New Product Platform

26

PruHealth

27

Virtual Life Insurance Companies Source: progress From Royal Liver Website

28

New CI Products What is the need for a CI product? Huge inertia What next: Tighter definitions Stand the test of time? Impact based definitions Subjectivity Build from Income Protection

29

Better Income Protection Products Clear need Low emotional appeal Uncertainty over state provision But problems with sale: Complicated to explain More detailed underwriting Accurate quotation methods Problems at claims stage

30

Product Platform Age at entry pricing is the norm Annually costed better? Consumer: No prepayment for cover Works out cheaper for most Insurer: More flexibility for product innovations Distributor Less commission?

31

The End Any questions?

Similar presentations

End time: ____ Please set phones to silent ring and answer outside of the room.>")

![ÜNVAN Bakı, AZ1078, C.Məmmədquluzadə küç, 998-ci məhəllə TELEFON/FAKS [994 12] 596 66 69 PERSPECTIVES OF LIFE.](/15/4725389/big_thumb.jpg "ÜNVAN Bakı, AZ1078, C.Məmmədquluzadə küç, 998-ci məhəllə TELEFON/FAKS [994 12] 596 66 69 PERSPECTIVES OF LIFE.>")

Lecture 2 The Economic and Regulatory Environment.>")

Unit 1 Lesson 44: Industry trade and professional bodies Investment distribution.>")