Download presentation

Presentation is loading. Please wait.

1

Colombian Firm Energy Market: Discussion and Simulation Peter Cramton (joint with Steven Stoft and Jeffrey West) 9 August 2006

9 August 2006")

2

Outline Discussion of issues Simulation of market –Purpose –Model 1 Historical prices Simulated units –Outline of Model 2 Historical prices and output Actual units –Outline of Model 3 Full simulation of auction and investment decision Conclusion

3

Issues

4

Reducing risk in early auction years Further protection from insufficient competition Long lead-time projects Why not have a higher strike price? Repowering bids

5

Reducing risk in early years Early years of auction –Ceiling and floor on firm energy payment to existing suppliers –Spread between ceiling and floor expand each year –Spread starts at 0 (transition years) –Increases to Ceiling = 2 CONE Floor =.5 CONE

–Increases to Ceiling = 2 CONE Floor =.5 CONE")

6

Insufficient competition rule Add additional requirement to assure competition from non-dominant players At qualification, quantity of new projects from small players (less than 15% firm-energy market share) > 50% of required new firm energy Otherwise insufficient competition: –Auction held –New entry paid clearing price –Existing capacity paid 1.1 CONE

> 50% of required new firm energy Otherwise insufficient competition: –Auction held –New entry paid clearing price –Existing capacity paid 1.1 CONE")

7

Long lead-time projects 4-year planning period may be too short for large hydro projects (6-8 years to build) Allow large hydro projects to lock in auction price from 4- year ahead auction seven years (or less) ahead Large hydro project is price taker Decides after auction a fraction of its firm energy to lock in at 4-year ahead auction price Total quantity of firm energy in years > 4 that load purchases is limited by a percent of new firm energy required in that year based on planning projections: Years ahead: 765 Percent limit:405060

Allow large hydro projects to lock in auction price from 4- year ahead auction seven years (or less) ahead Large hydro project is price taker Decides after auction a fraction of its firm energy to lock in at 4-year ahead auction price Total quantity of firm energy in years > 4 that load purchases is limited by a percent of new firm energy required in that year based on planning projections: Years ahead: 765 Percent limit:405060")

8

Strike price Why not have a very high strike price? (US$250 or more) –Benefits of call option are largely lost Load hedge Mitigation of market power in spot energy market –No reason to set strike price higher than marginal cost of an expensive thermal unit

–Benefits of call option are largely lost Load hedge Mitigation of market power in spot energy market –No reason to set strike price higher than marginal cost of an expensive thermal unit.")

9

Repowering bids Easily accommodated in auction Two types: –Quick switchovers (down time less than 1 year) Repower bid is a new entry bid and a conditional retirement –Extended down time (more than 1 year) Retirement followed by new entry bid 1 or more years later

Repower bid is a new entry bid and a conditional retirement –Extended down time (more than 1 year) Retirement followed by new entry bid 1 or more years later")

10

Simulation

11

Purpose

12

Assess supplier risk Consider variations of market design Evaluate alternative auction parameters

13

Model 1

14

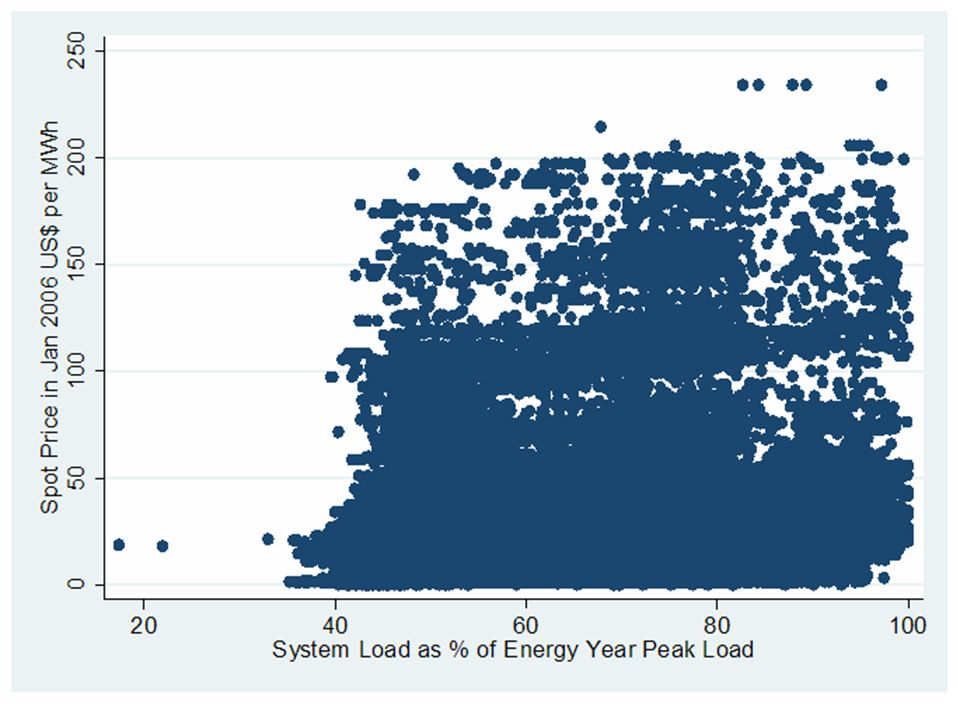

Model 1 Historical prices, simulated units Sample: October 1995 through May 2006 Scarcity hours: spot price > strike price One long dry period: thirteen months –30 Mar 1997 to 21 Apr 1998 One short period of high prices (start of market) –21 Nov 1995 to 24 Dec 1995

–21 Nov 1995 to 24 Dec 1995")

15

Scarcity hours by year

16

Scarcity hours by month and year Almost every hour is a scarcity hour in long dry periods.

17

Thermal percent of load Thermal share of load much higher in dry periods. Hydro share is still large in long dry periods.

18

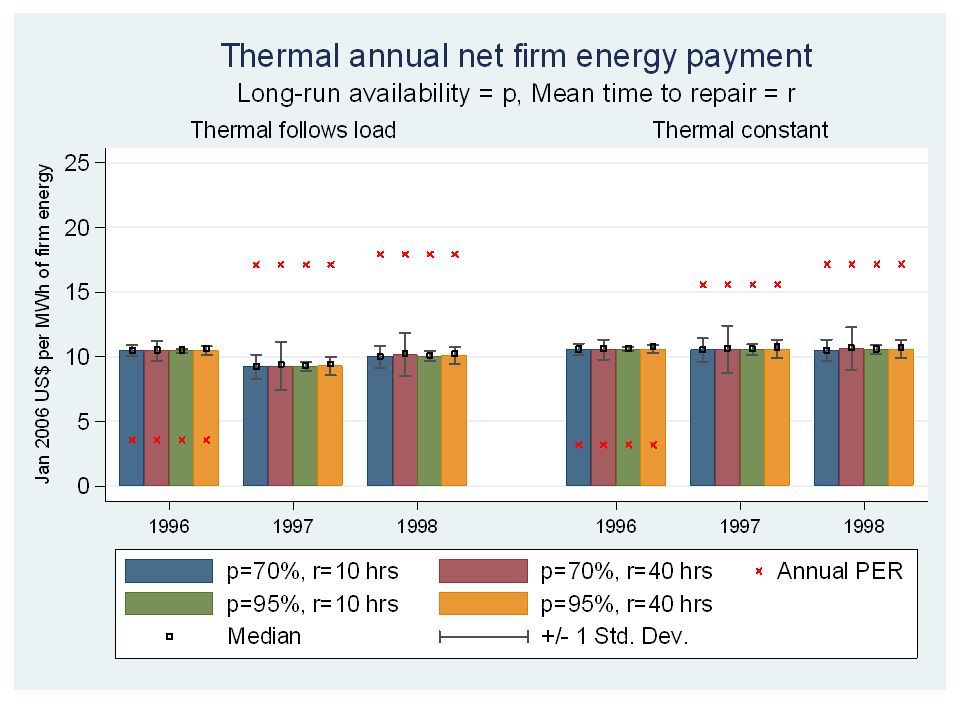

Model 1: Thermal unit Random time until failure Random time to repair Both exponentially distributed –Long-run availability: 70% and 95% –Mean time to repair: 10 hours and 40 hours 1000 simulations over entire time period –Calculate distribution of net firm energy payment

19

Firm energy payment All amounts in January 2006 US dollars Auction not modeled so assume payment Firm energy payment = $10.86/MWh –Should be $13.045 –Exact value not relevant

20

Net firm energy payment Net firm energy payment = Firm energy payment + reward for over performance − penalty for under performance In hours where spot price > strike price, Reward or penalty = (Q actual – Q obligation )(P spot – P strike ) Q obligation = supplier’s share of load

(P spot – P strike ) Q obligation = supplier’s share of load")

21

Energy rents $0 Unit’s marginal cost Strike price Peak energy rent Energy rent Unit does not operate Forward energy contract Call option (FEM)

")

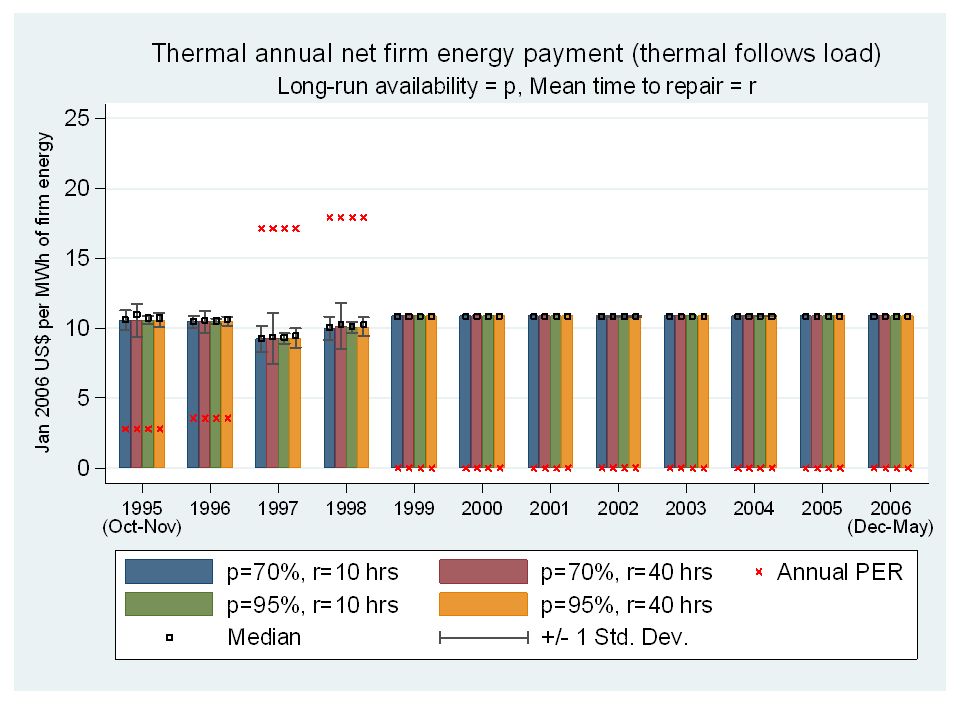

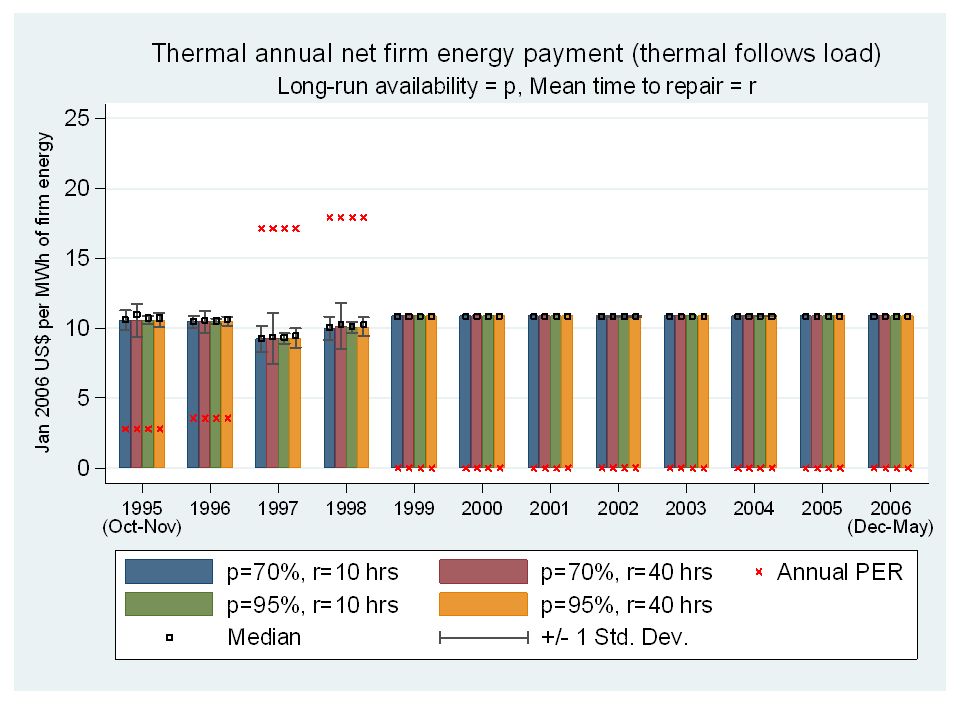

24

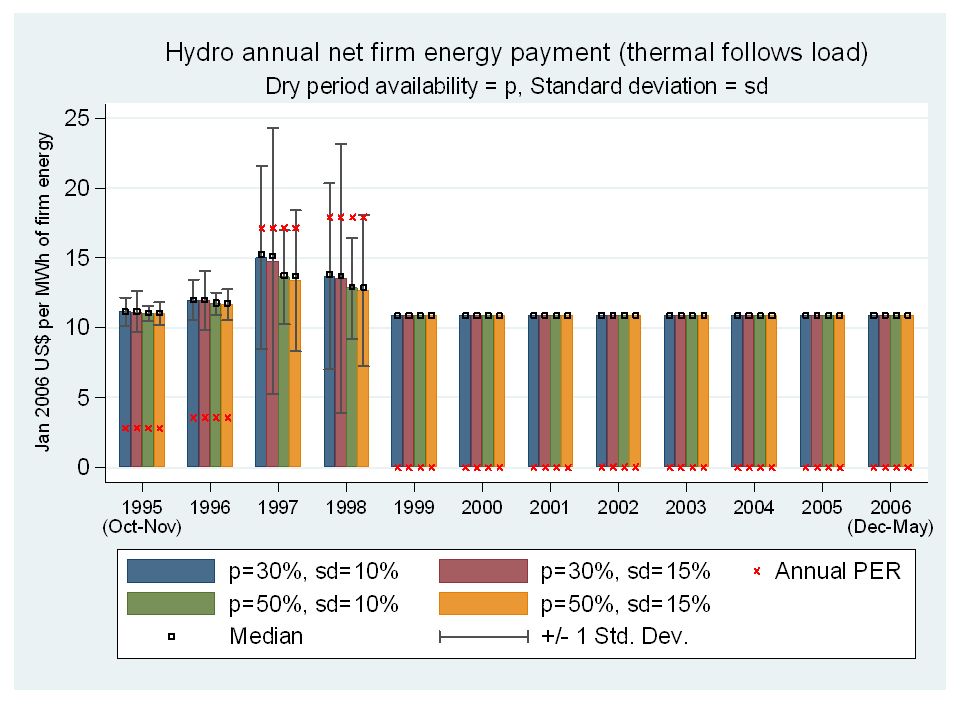

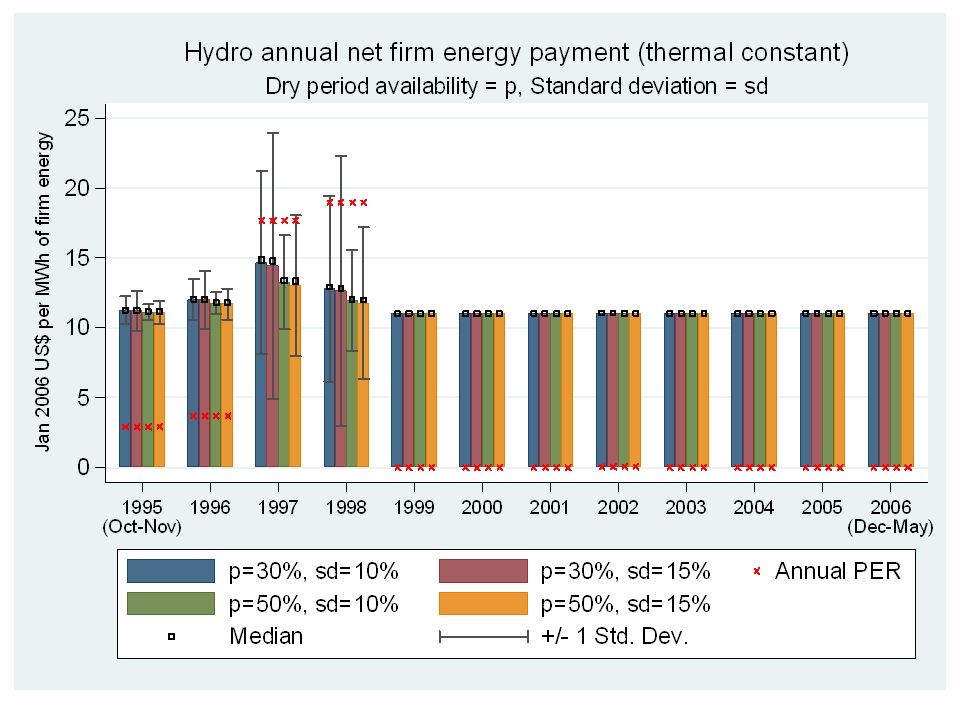

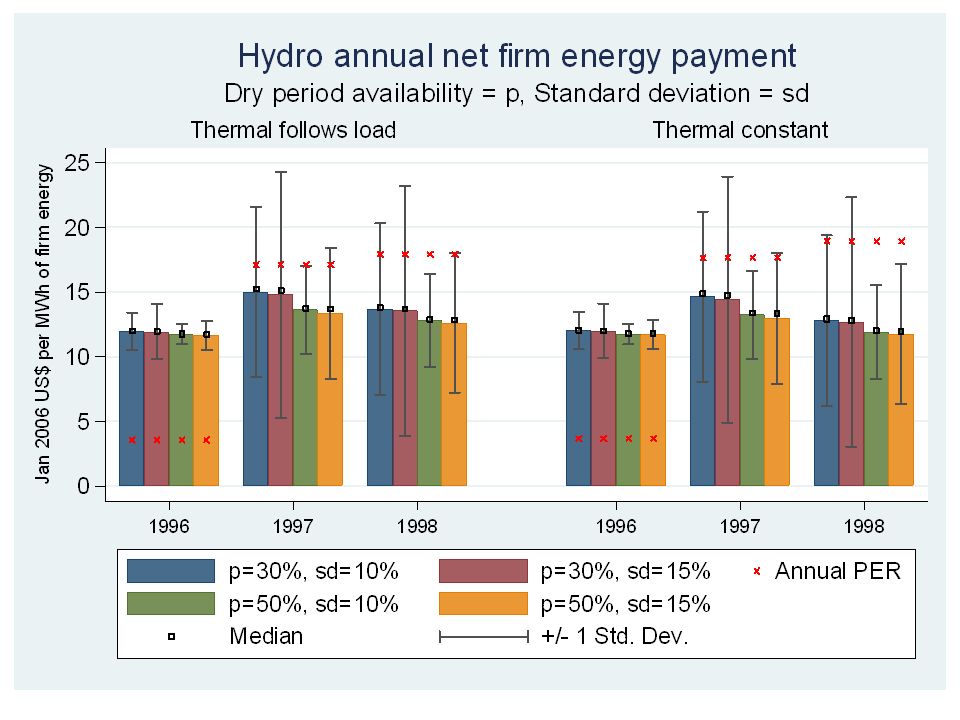

Model 1 results: thermal Net firm energy payment roughly constant Some variation in dry periods –Standard deviation is small compared to mean –Variation greatest for unreliable units with long mean repair times Slight reduction in dry periods (about 10%) –Thermals under perform on average Over perform in low-load conditions Under perform in high-load conditions Small positive correlation between price and load

–Thermals under perform on average Over perform in low-load conditions Under perform in high-load conditions Small positive correlation between price and load")

25

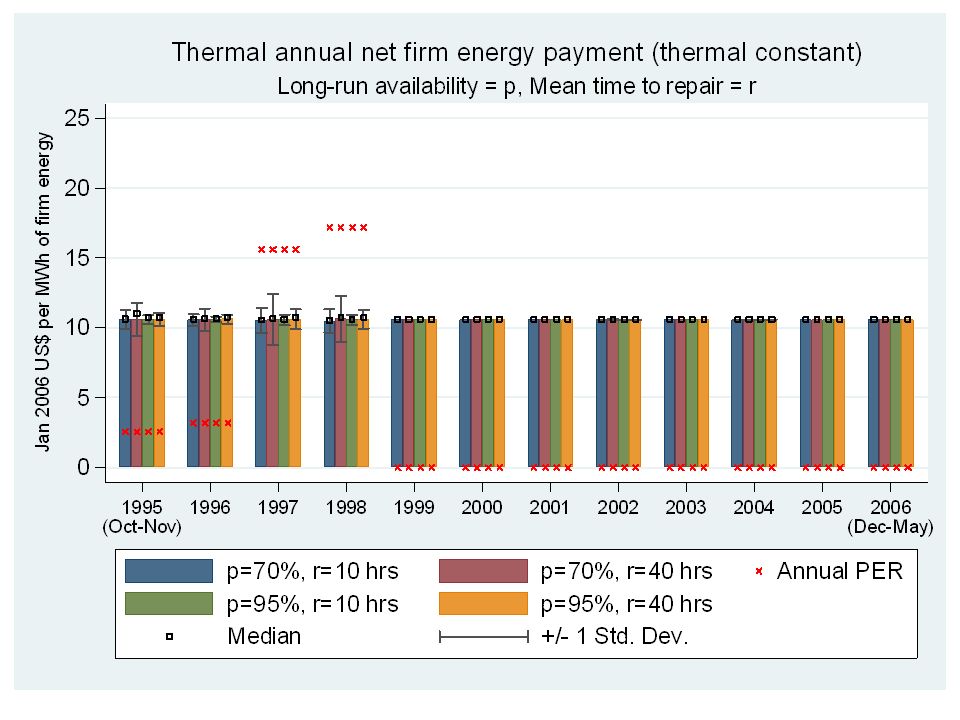

Alternative obligation: Thermal constant Idea: Make obligation more consistent with unit’s actual dispatch Give thermal a constant obligation during scarcity hours (obligation = LR availability) Hydro follows residual demand (load minus thermal obligation) Can still treat as one product –Load following is not scare –Service is priced at zero in competitive market

Hydro follows residual demand (load minus thermal obligation) Can still treat as one product –Load following is not scare –Service is priced at zero in competitive market")

28

Model 1: Hydro unit Actual quantity of firm energy in dry period is a random variable (normal distribution) Unit sells its mean firm energy in dry period (mean availability = 30% or 50%) Actual firm energy has standard deviation (sd = 10% or 15%) –Note: Probably too high. Will rerun with empirically fitted distribution from hydrology data from 1950s.

33

Thermal-constant alternative No impact on risk Thermal: Higher mean in dry period Hydro: Lower mean in dry period Obligation better matches actual dispatch –Units enter spot market with balanced position –No incentive to exercise market power –With load-following approach: Hydro increases slope of supply curve (increasing price in high-load hours) Thermal bids higher (increasing low-load price)

Thermal bids higher (increasing low-load price)")

34

Model 2

35

Model 2 Historical prices, output; Actual units Assume each unit sells its firm energy certification (either reference or maximum for hydro) Calculate net firm energy payment for each unit in each hour –Aggregate over month –Aggregate over year –Aggregate over company’s portfolio Provides some insight on supplier risk

Calculate net firm energy payment for each unit in each hour –Aggregate over month –Aggregate over year –Aggregate over company’s portfolio Provides some insight on supplier risk")

36

Model 3

37

Model 3 Full simulation of auction and investment Can ask new questions –How does acquired firm energy differ from firm energy target? –What is the impact of increasing the slope of the demand curve around the target? Stationary model –Three project types: baseload, peaker, hydro –Baseload and peaker: Capacity, FC, VC –Hydro: Capacity, FC, Firm Energy

38

Conclusion

39

Call option reduces market risk –Load is hedged from high spot prices –Hedge is not too costly for suppliers to offer Physical asset covers obligation Call option reduces supplier risk –Get nearly constant payment, rather than highly variable peak energy rents Call option improves spot market –Mitigates market power problem during scarcity –Better spot market improves forward energy market Spot energy prices are more stable and predictable Thermal-constant obligation is better than load- following obligation

Similar presentations

would prefer to hedge their.>")

18 December 2006.>")