Download presentation

Presentation is loading. Please wait.

1

Understanding H.S.A. Plans A short explanation of Health Savings Accounts and Qualified High Deductible Health Plans

2

H.S.A.s can only be added to a Qualified High Deductible Health Plan or HDHP HDHP Rules, 2015: Generally One deductible per policy, not per person. Minimum deductible for a single person is $1250. Minimum deductible for a family is $2500 Maximum out of pocket in network is $6350/single Maximum out of pocket in network is $12,700/family No first dollar benefits allowed except for wellness. 1.NO Dr. Office visit co-pays. 2.NO RX co-pays Must be filed as a qualified plan

3

All H.S.A. Qualified plans are Not Created Equal The rules are clear as to what can not be in a HDHP. There are very few rules dealing with what Must be included. All H.S.A. plans are not the same.

4

H.S.A.s = Medical I.R.A.s Once the Qualified HDHP is in place, a health savings account may be set up to work in conjunction with that health plan. Contributions to an H.S.A. are made using pre-tax dollars. Funds in the H.S.A. account are not taxed when used to pay for qualified medical expenses.

5

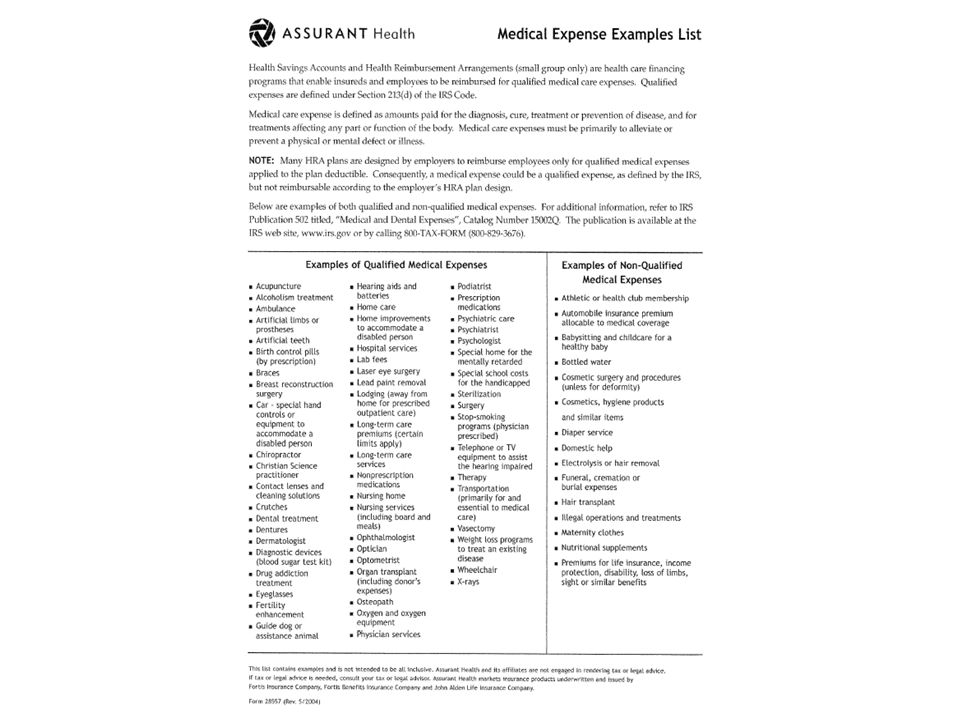

Funds in the H.S.A. Are not taxed when used for medical expenses!!!! Tax free $$$ can be used to pay for: 1.Expenses that qualify toward the deductible on the health plan 2.Expenses for non-normal medical products and services that are not covered by the health plan

7

Consumer A’s Health-care Expense dollars Health insurance premiums HSA At year’s end, unused Money stays in the Account for the following Year’s medical expenses Unused $ $ $ = Your savings Health Insurance Premiums & out-of- Pocket expenses Consumer B’s Healthcare Expense dollars

8

*H.S.A. Rules* 2015 Annual Contributions for a single person are limited to$3350. 2015 Annual contributions for a family are limited to $6650. H.S.A.s have a catch-up provision that allows account holders over age 55 to contribute additional money to their savings accounts each year.(This year $1000) There is no minimum funding requirement for H.S.A.s

There is no minimum funding requirement for H.S.A.s.")

9

Future Savings If the money put into the Health Savings Account is not used, it stays in the account accruing interest, or appreciation. Each year the account holder is allowed to contribute additional funds into their Health Savings Account, building their Medical I.R.A.

10

At age 65: Account funds can be used to pay Medicare Part B premiums as well as Health needs unmet by Medicare. Funds can be accessed for non-medical reasons without penalty. (normal taxes apply.)

.")

Similar presentations

Everything You Need to Know.>")

This presentation will probably involve audience discussion, which will create action items. Use PowerPoint to keep track.>")

with HSA Effective July 1, 2009.>")

HSA Accounts were signed into Law on Dec. 8 th, 2004 as part of the Medicare Rx-Bill.>")