Download presentation

Presentation is loading. Please wait.

1

Economic Systems CHAPTER TWO

2

3 Basic Questions What goods and services should be produced?

How should these goods and services be produced? Who consumes these goods and services?

3

What to Value? Economic System – method used by a society to produce and distribute goods and services Easiest way to distinguish an economy is by who answers the basic questions OR owns and controls the factors of production Dependent upon that society’s goals and values. What should a society value? What do you value? Do different societies have different values?

4

Goals & Values Economic Efficiency – maximize what you can get with what you have to work with. Economic Freedom – be able to make your own decision from a variety of choices. Economic Security – knowing you can find the goods/services that you need. safety net – set of government programs that protect people experiencing unfavorable economic conditions Economic Equity – does everyone get the same? Economic Stability Economic Growth – the economy must grow for a nation to improve. standard of living – level of economic prosperity

5

Traditional Economies

Relies on habit, custom, or tradition to answer the 3 basic questions. OR the village controls the factors of production--resources are shared Everything revolves around family Your occupation would be what your ancestors have always done Small and close communities that engage in subsistence agriculture

6

Traditional Society ADVANTAGES Simple, natural, caring DISADVANTAGES

Struggle to cope with large disasters Slow to adapt to change Lack modern conveniences No social mobility

7

Market Economies Individuals answer the basic questions based on exchange or trade. Factors of production are privately owned Choices determine what is produced and who gets it. Also referred to as the Free Market or Capitalism.

8

Why Engage in Exchange? Self-interest motivates people to exchange and trade By looking out for their own utility (getting what they want) society becomes better off Producers seek greater profit, workers higher wages, consumers the best deal Competition regulates the market and keeps it reasonably fair Producers seek profit and low costs Consumers seek the best deals to satisfy their wants and needs

society becomes better off. Producers seek greater profit, workers higher wages, consumers the best deal. Competition regulates the market and keeps it reasonably fair. Producers seek profit and low costs. Consumers seek the best deals to satisfy their wants and needs.")

9

Incentive – ways of altering behavior (taxes, punishment, candy)

Economists believe few problems cannot be solved by the right incentives Invisible Hand – phenomenon by which a market operates fairly without planning Consumers get what they want, as do producers

10

Free Market Market – arrangement of buyers and sellers to exchange things. Flea market, ebay Specialization – makes businesses and the economy more productive and efficient Households / individuals own the factors of production Markets organize trade and exchange in a non-fraudulent way Allows all parties to benefit “The meaning of economic freedom is this: that the individual is in a position to choose the way in which he wants to integrate himself into the totality of society.” ~Ludwig von Mises

11

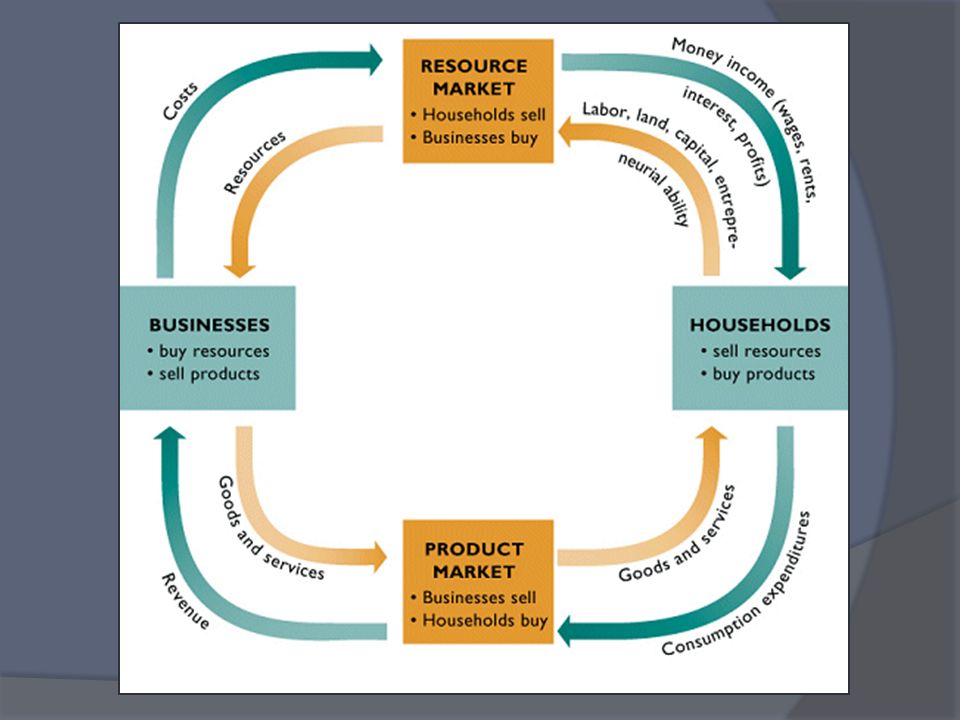

Factor & Product Markets

All economic transactions take place on one of two markets Factor market – resources are bought and sold (raw) Rent, land, labor Product market – where goods/services are purchased by households (cooked)

Rent, land, labor. Product market – where goods/services are purchased by households (cooked)")

13

Raw vs. Cooked Factors of production Resources “Raw materials”

Goods and services Ready to be bought and sold “Finished products”

15

Free Market Advantages

Efficiency – highly productive and responds rapidly to change Freedom – work, produce, consume how/want you want Potential for Growth – creative destruction, innovation Consumer Sovereignty – “customer is king” If anyone rules the free market, it is the consumer If you don’t like it—don’t buy it!

16

Free Market Disadvantages

Vast amounts of inequality and insecurity Greater chance of failure OR wealth is spread unevenly Not only is a large percentage of the population in poverty, but a disproportionate amount of the population holds the majority of the wealth

17

Command Economies Central government answers basic economic questions.

Government controls the resources Distribution based on equity No choices given to people. Elite inner circle of planners decide what & how much gets made along with how much to charge for it Thus the name “Central Planning” Stalin at the Helm

18

Centrally Planned Economies

Government controls factors of production and wages, sets prices and output goals Communism - (authoritarian) complete governmental control Socialism – blend of centrally planned and free market systems includes high degrees of regulation, high taxation, large safety nets and some economic planning

complete governmental control. Socialism – blend of centrally planned and free market systems. includes high degrees of regulation, high taxation, large safety nets and some economic planning.")

19

Disadvantages: Central Planning

No efficiency Poor quality, shortages Performance never meets ideals Lack of incentives No innovation or profit, no private property, price controls Sacrifice of individual freedoms Gov’t decides what industries are essential

20

Advantages: Central Planning

No competition Few business failures and few mega-rich citizens Basic security Essential amounts of most necessities are available Ex: healthcare, cooking oil, bread… General equality Majority of population experiences a similar life No class divisions, jobs for most Wealth theoretically spread more evenly

21

Mixed Economies Market-based economy

with government making some decisions Good deal of control and regulation Most modern economies are mixed. China, India, the US

22

Modern Economies Transition – economies typically moving from centrally planned to free-market are characterized by a few observations: Privitization – businesses are transferred from state (gov’t) control to individuals, allows for competition Less nationalization—fewer state-run firms Respect for rule of law and private property Encourages outside investment

control to individuals, allows for competition. Less nationalization—fewer state-run firms. Respect for rule of law and private property. Encourages outside investment. v=XiXs7oBynYA.")

23

Bovine Economics COMMUNISM: You have two cows. The government takes both and gives you some of the milk. SOCIALISM: You have two cows The government takes one cow and gives it to your less fortunate neighbor. TRADITIONAL: You have two cows; you want chickens; you set out to find another farmer who will trade eggs for milk. CAPITALISM: You have two cows. You sell one and buy a bull.

Similar presentations