Download presentation

Presentation is loading. Please wait.

2

Presented by:

3

THEBASICS

4

WHAT IS THE DIFFERENCE? CASH? CASH? A DEBIT CARD? A DEBIT CARD? A CREDIT CARD? A CREDIT CARD? A GIFT CARD? A GIFT CARD?

5

What is DEBT? A. You are in a deep hole. B.You have to pay money to someone. C.You owe someone a favor. D. You are entitled to free stuff.

6

Answer: B When you are in debt, you have to pay money to someone.

7

What does CREDIT mean? A. You have a good reputation. B. You might graduate. C. You can borrow to buy things. D. You can get things at the store for free.

8

Answer: C Credit is the ability to borrow money. Credit is the ability to borrow money. Borrowing is the creation of debt. Borrowing is the creation of debt. Debt is what you owe Debt is what you owe There is no such thing as a free lunch.

9

What is INTEREST? A.Money you pay to rent money. B.Someone else likes you. C. You like someone else. D. You qualify for a scholarship.

10

Answer: A Interest is the amount a lender charges you to borrow money from them.

11

The Trick about Interest The higher the interest rate, the more you will pay. The higher the interest rate, the more you will pay.

12

What is compound interest? A.Liking more than 1 girlfriend or boyfriend. B.Interest charged on interest that is added on to the credit card bill. C.Something you learn in chemistry class. D. A grinding power.

13

Answer: B A debt that goes unpaid and is subject to compound interest grows into a much larger number very quickly.

14

The True Cost of Credit

15

A $7,000 Balance (at 20% interest) = $1, 400/year = $116/month (…and you haven’t paid any of the $7,000 back yet)

= $1, 400/year = $116/month (…and you haven’t paid any of the $7,000 back yet)")

16

MAKING MINIMUM PAYMENTS If you make the minimum payment of 2%: Your interest charges will total: $30,294.80 Number of payments you make: 601 Total number of years to payment: 50.08

17

In 50.08 years you will paying your final payment on that $7,000 balance with your social security check!

18

If You SAVE That Money… If you save or invest $20 per month for 50.08 years you will have: 5% = $54, 082.00 6% = $76,923.97 8% =$161,861.61 This is compound interest working for YOU!

19

Thank goodness for Make-overs The Credit CARD Act of 2010 requires that account statements disclose additional information such as your payment due date and consequences of only making the minimum payments. The Credit CARD Act of 2010 requires that account statements disclose additional information such as your payment due date and consequences of only making the minimum payments. Source: Creditcards.com

20

No More Tricks! 45 days advance notice to increase interest rate 45 days advance notice to increase interest rate Cancellation of card is not a default Cancellation of card is not a default Interest rate cannot be increased for past charges or because you default on another card Interest rate cannot be increased for past charges or because you default on another card Fees and interest rates cannot increase for 1 year except when there was a promotional rate for 6 months Fees and interest rates cannot increase for 1 year except when there was a promotional rate for 6 months

21

No more fooling you! No more fooling you! No over limit charges unless you agree No over limit charges unless you agree Card agreements (the fine print) must be available on the internet Card agreements (the fine print) must be available on the internet No credit cards if you are under 21 unless you have an over 21 co-signer or you can show you can pay the card No credit cards if you are under 21 unless you have an over 21 co-signer or you can show you can pay the card No more freebies to open up cards on college campuses No more freebies to open up cards on college campuses WATCH OUT! This does not apply to sporting events or other venues.

must be available on the internet Card agreements (the fine print) must be available on the internet No credit cards if you are under 21 unless you have an over 21 co-signer or you can show you can pay the card No credit cards if you are under 21 unless you have an over 21 co-signer or you can show you can pay the card No more freebies to open up cards on college campuses No more freebies to open up cards on college campuses WATCH OUT. This does not apply to sporting events or other venues..")

22

New & Improved Statement will show: Payment information New balance $1,734.53 Minimum payment due $53.00 Payment due date 4/20/12 Payment information New balance $1,734.53 Minimum payment due $53.00 Payment due date 4/20/12 –Late payment warning: If we do not receive your minimum payment by the date listed above, you may have to pay a late fee of up to XX and your APRs may be increased up to the Penalty APR of 28.99% Source: Creditcards.com

23

Disclosing the Minimum Payment Pitfall! Disclosing the Minimum Payment Pitfall! Minimum payment warning: If you make only the minimum payment each period, you will pay more in interest and it will take you longer to pay off your balance. Minimum payment warning: If you make only the minimum payment each period, you will pay more in interest and it will take you longer to pay off your balance. For example, if you had a balance of $1,000 at an interest rate of 17% and always paid only the minimum required, it would take over 7 years to repay this balance. For example, if you had a balance of $1,000 at an interest rate of 17% and always paid only the minimum required, it would take over 7 years to repay this balance. If you would like information about credit counseling services, call 1-800-XXX-XXXX If you would like information about credit counseling services, call 1-800-XXX-XXXX

24

What the new statement will show on APR’s These account changes will impact your account as follows: Transactions made on or after 4/9/12: As of 5/10/12, changes to APRs described below will apply to these transactions. Transactions made before 4/9/12: Current APRs will continue to apply to these transactions. Revised terms, as of 5/10/12 These account changes will impact your account as follows: Transactions made on or after 4/9/12: As of 5/10/12, changes to APRs described below will apply to these transactions. Transactions made before 4/9/12: Current APRs will continue to apply to these transactions. Revised terms, as of 5/10/12 APR for purchases16.99% Late payment fee: $32 if your balance is less than or equal to $1,000; $39 if your balance is more than $1,000 Source: Creditcards.com

25

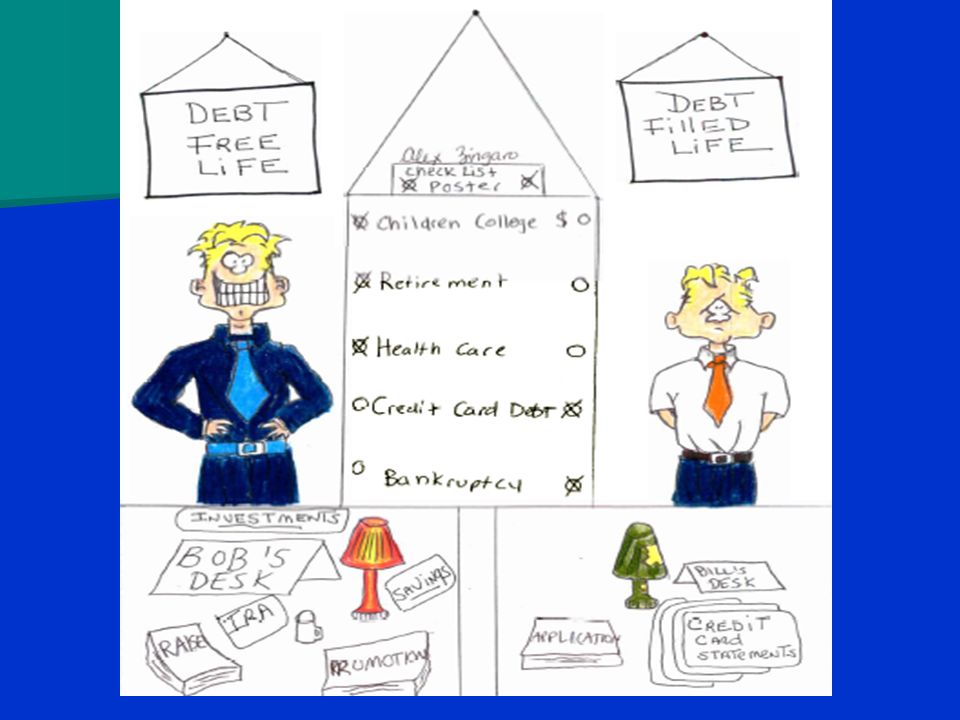

Consequences of Good & Bad Credit

27

WHAT IS CREDIT AND CREDIT SCORE? It’s a matter of life and debt! It’s a matter of life and debt! Just like you are graded in school on how you perform academically…YOU ARE GRADED in LIFE on HOW you perform FINANCIALLY Just like you are graded in school on how you perform academically…YOU ARE GRADED in LIFE on HOW you perform FINANCIALLY A 3-digit number between 300-850. The better your credit, the higher your credit score. A 3-digit number between 300-850. The better your credit, the higher your credit score.

28

Factors used to determine your credit score how you pay back your debts how you pay back your debts –paid on time? –paid at all? –paid debt with credit cards? –paid in part or in full? how you manage your debts how you manage your debts –do you have high balances? –do you have too many open credit cards?

29

WHO GRADES YOUR CREDIT REPORT? Credit Bureaus! Visit AnnualCreditReport.com for a free copy of your credit report and myfico.com for your credit score. TransUnion EquifaxExperian Credit- reporting agencies

30

What is so important about Good Credit? Obtain loans for cars, home, education Obtain loans for cars, home, education Better interest rates Better interest rates Lower installment payments Lower installment payments May help you rent and obtain employment May help you rent and obtain employment

31

What are consequences of Bad Credit? Being turned down for a loan Being turned down for a loan Being turned down from a job Being turned down from a job Creditors calling your home or work Creditors calling your home or work Being sued and having judgments against you including wages garnished Being sued and having judgments against you including wages garnished Bankruptcy Bankruptcy Relationship problems, depression, suicide Relationship problems, depression, suicide

32

Did you know? If you apply for an auto loan, the lender will probably review your credit report. If you apply for an auto loan, the lender will probably review your credit report.

33

And did you know? FALSE FALSE

34

And did you also know? - Missing just 1 or 2 credit card payments will hurt your credit rating. - Negative information can legally remain on your credit report for up to 7 years.

35

What is bankruptcy? - What you own may get sold to pay off your debts - Some of your income may be used to pay your old debt - If you’re an honest debtor, the Court may discharge your debt and you will have a fresh start

36

Tips for Good Credit Pay bills in full and on time Pay bills in full and on time Don’t open too many cards but if already opened, do not close these established accounts Don’t open too many cards but if already opened, do not close these established accounts Do not have a balance on your credit card exceeding more than 20-30% of your credit limit (DON’T MAX OUT!) Do not have a balance on your credit card exceeding more than 20-30% of your credit limit (DON’T MAX OUT!)

Do not have a balance on your credit card exceeding more than 20-30% of your credit limit (DON’T MAX OUT!)")

37

TIPS: Get Credit with knowledge Beware of Credit Card Representatives at Games, Concerts, Events. Beware of Credit Card Representatives at Games, Concerts, Events. Resist opening a new credit card account for the enticing “free gifts” Resist opening a new credit card account for the enticing “free gifts”

38

Tips: Obtaining a Card “Shop” for a credit card with the best terms that suit you “Shop” for a credit card with the best terms that suit you ANNUAL MEMBERSHIP FEE: Refer to your statement in the month in which the fee is billed. RENEWING YOUR ACCOUNT: You may have your annual membership fee credited to your account if you close your account within 30 days from the mailing or delivery date of the statement containing the fee, even if you use your card during that period. You may call the Customer Service number or write to the Customer Service address on your statement during this 30 day period and your account will be terminated; we will credit your account for the amount of the annual fee. RENEWING YOUR ACCOUNT: You may have your annual membership fee credited to your account if you close your account within 30 days from the mailing or delivery date of the statement containing the fee, even if you use your card during that period. You may call the Customer Service number or write to the Customer Service address on your statement during this 30 day period and your account will be terminated; we will credit your account for the amount of the annual fee. ANNUAL PERCENTAGE RATE: Refer to the Rate Summary section of this statement. Your periodic rates and APRs may vary. ANNUAL PERCENTAGE RATE: Refer to the Rate Summary section of this statement. Your periodic rates and APRs may vary. RATE AND ACCOUNT SUMMARIES: The purchase and advance features of this account may be listed in the Rate Summary Section of this statement under the following titles: Standard Purch, Purch/Adv, Standard Adv, and various numbered Offers. The Account Summary section of this statement includes on the PURCHASES line subtotals for all purchase features, and on the ADVANCES line subtotals for all advance features, of the Previous Balance, new Purchases & Advances, Payments & Credits, FINANCE CHARGE and New Balance amounts. PERIODIC RATES: (D) and (F) indicate a daily periodic rate. (M) indicates a monthly periodic rate. –Read and understand the terms in the disclosure (review online) –Pay close attention to various late fees and penalties

and (F) indicate a daily periodic rate. (M) indicates a monthly periodic rate. –Read and understand the terms in the disclosure (review online) –Pay close attention to various late fees and penalties.")

39

Tip: Shop for a Credit Card COMPARE CREDIT COMPARE CREDIT CARD OFFERS: BANKRATE.COM BANKRATE.COM –click on the tab “credit cards”

40

TIPS: Make a Budget INCOME Gross wages $1,600 Less payroll deductions $400 Net Monthly Pay $1,200 Expenses & Savings Rent$500 Utilities$30 Food$200 Clothing$100 Laundry$20 Recreation$50 Transportation$100 Savings (LESS)$200 Total Expenses:$1,200

$200 Total Expenses:$1,200")

41

Tip: Use your card wisely! Limit credit card use for essential purchases only. You may want that shirt, but do you really need it? Limit credit card use for essential purchases only. You may want that shirt, but do you really need it?

42

How to write a check: Step 1

43

Step 2

44

Step 3

45

Step 4

46

THE END

Similar presentations

Program U.S. Bankruptcy Court – Southern District of California.>")