Download presentation

Presentation is loading. Please wait.

1

Consolidated Accounts

2

How can a company be a holding one? Controls the composition of the board of director Controls more than half of the voting power holds more than half of the issued share capital (ordinary shares)

.")

3

Why do companies want to be a holding one? Any benefits? Increase in revenue (improvement in marketing, reduction of competition, gain in monopoly power, etc) Cost reduction (purchase in bulk and discount obtained)

Cost reduction (purchase in bulk and discount obtained).")

4

Why are consolidated accounts needed? Present group’s financial position and operating results Required by the Companies ordinance eliminate inter-group transactions (over / under estimate net profit) Parent + holding = a group =one single economic entity

Parent + holding = a group =one single economic entity.")

5

Under what occasions, will a subsidiary be excluded from the consolidation? Control of parent over subsidiary is temporary (subsequent disposal in the near future) subsidiary operate under severe long-term restriction (unable to transfer funds to the parent)

subsidiary operate under severe long-term restriction (unable to transfer funds to the parent).")

6

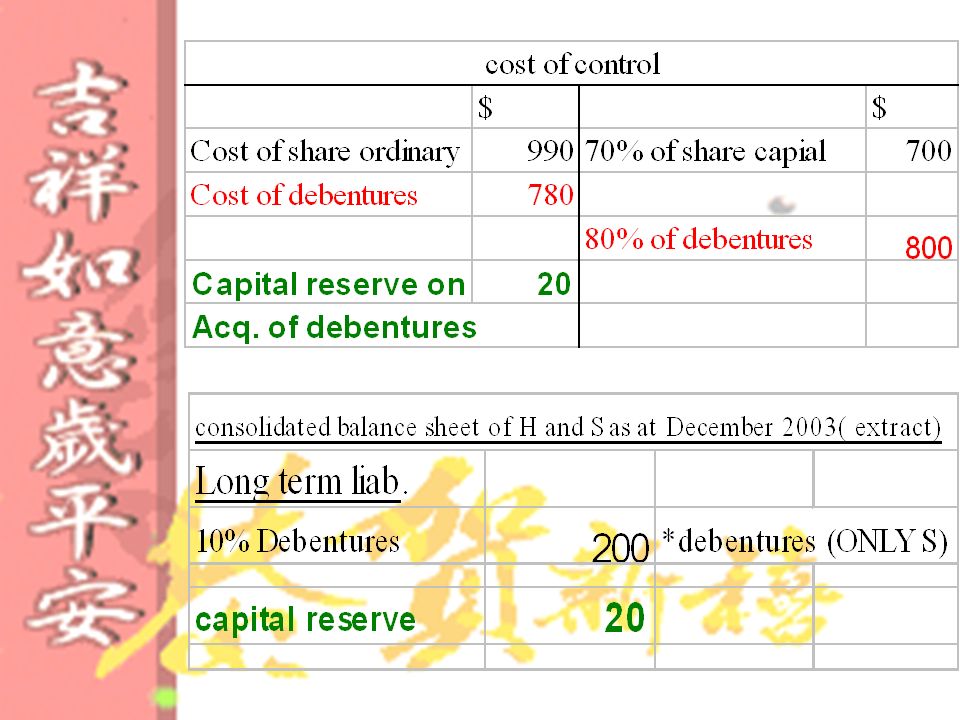

Cost of control Account %=% of Ordinary shares held by parent S=Subsidiary

7

Consolidated Profit or Loss

8

Minority Interest %=% of ordinary shares held by MI

9

Negative Goodwill Dr. Negative Goodwill Cr.P&L Show in brackets in B/S

10

Revaluation RRGWMIPFD

11

Past paper 2004-I-1b In January 2003, Lemon Ltd loaned $10000000 for ten months to John, a shareholder of Tea Ltd. John pledged his investment, which represents 60% of the ordinary capital of Tea Ltd, as security for the loan. When the loan is matured, he was unable to repay the debt and transferred the title of the shares to Lemon Ltd. Lemon Ltd tried to find a buyer for these shares but failed. At its year end on 31 Dec 2003, Lemon Ltd was still holding the shares. The shares were ultimately sold in Feb 2004. With respect to Lemon Ltd’s shareholding in Tea Ltd, explain whether Lemon Ltd is required to prepare consolidated financial statement as at 31 Dec 2003.

12

Answer Lemon Ltd does not acquire the investment for long term purpose. Control in intended to be temporary because the 60% of ordinary share capital is acquired and held with a view to its subsequent disposal in the near future. Despite its majority shareholding in Tea Ltd, Lemon Ltd is not required to prepare the consolidated financial statement.

13

2005Past Paper-I-1 (iii) For the purpose of acquisition, a fixed asset of Leaf Ltd (subsidiary) was revalued from $2000000 to $2500000. The revaluation was not recorded in the books of Leaf Ltd. Leaf Ltd had been providing depreciation at a rate of 10% per annum on the net book value of fixed assets.

14

Adjustment Dep over provided:(2500000-2000000)*10%=50000 Dr.Provision of Depreciation Cr.P&L

*10%=50000 Dr.Provision of Depreciation Cr.P&L")

15

Debentures and Preference Shares of Subsidiaries A company will be deemed to be a subsidiary of another company if latter holds more than half of the issued ordinary share capital of the subsidiary. The % of controlling interest is determined by the amount of ordinary shares held instead of preference shares. MI only consists of reserves, ordinary shares and preference shares held by the outside shareholders.In determining whether acompany is a subsidiary, the holding of its debentures is irrelevant.

16

Points to be noted: *debentures should be disclosed as liabilities in the consolidated balance sheet. If the purchase price of debentures > the nominal value, the premium should : Dr consolidated reserves Cr cost of control If the purchase price of debentures < the nominal value, the discount should : Dr cost of control Cr consolidated reserves

17

Example H Ltd. had acquired 70% ordinary shares and debentures of S Ltd on 31/12/2003. H S Investment is S Ltd 700 ordinary shares 990 800 debentures 780 Share capital Ordinary shares of $1 each 1000 10% debentures 1000

19

Proposed dividend If the dividend is paid by the subsidiary : The dividend must be accounted for as payables in the subsidiary’s accounts The dividend must be accounted for as receivables in the parent’s accounts The intra – group dividend will be set off in the consolidated account so that only the dividend payable to outsiders will remain

20

Unrealised Profit(URP) In the preparation of consolidated balance sheet, we should eliminate the intra-group unrealized profit at the end of the financial year.

In the preparation of consolidated balance sheet, we should eliminate the intra-group unrealized profit at the end of the financial year.")

21

Consolidated Balance Sheet as at 31 December 2003 Fixed assets [H + S(**the change of depreciation, unrealised profit ]S(**the change of depreciation, unrealised profit goodwill ( cost - accumulated amortization) / negative goodwill current assets inventories (H + S - goods in transit - unrealized profit)unrealized profit trade receivables ( H + S - intra-group balances)intra-group balances Bank ( H + S + cash in transit) less : Current Liab. trade payables ( H + S - intra-group balances) less : long-term Liab. Debentures (H + 30% S) (assume the holding company holds 70% of the debentures of the subsidiary )

![Consolidated Balance Sheet as at 31 December 2003 Fixed assets [H + S(**the change of depreciation, unrealised profit ]S(**the change of depreciation, unrealised profit goodwill ( cost - accumulated amortization) / negative goodwill current assets inventories (H + S - goods in transit - unrealized profit)unrealized profit trade receivables ( H + S - intra-group balances)intra-group balances Bank ( H + S + cash in transit) less : Current Liab.](http://images.slideplayer.com/25/7595655/slides/slide_21.jpg "trade payables ( H + S - intra-group balances) less : long-term Liab. Debentures (H + 30% S) (assume the holding company holds 70% of the debentures of the subsidiary ).")

22

Financed by: Share Capital ordinary ( H ONLY ) preference (H ONLY ) Reserves P & L { H + (post acquisition reserve of S - inderprovision of depreciation on revalued assets) X 80% - any change in income ) other reserves ( H + prost acquisition reserve of S - inderprovision of depreciation on revalued assets) X 80% ***assume the holding company holds only 80% of the ordinary share capital Minority Interest (20 % of ord. Share, 20 % reserves, 40 % of the preference shares) ***assume the holding company holds 60% of the preference share capital

***assume the holding company holds 60% of the preference share capital.")

23

How to share the URP? There are 2 methods to share the URP The first method: Minority interests are to share any unrealised profit or losses (together with any related depreciation adjustment) arising from sales of assets by the subsidiary to the parent according to their proportion of shareholding Parent shares 80% of the URP MI share 20% of the URP

arising from sales of assets by the subsidiary to the parent according to their proportion of shareholding Parent shares 80% of the URP MI share 20% of the URP.")

24

The second method: The group also adopts the policy that the unrealised arising from intra-group transaction have to be eliminated in full and shared between the parent and the minority interests according to their respective shareholdings. The parent bear all of the URP

25

Dividend and Bonus issue

26

Dividend From pre-acquistion profits Dr Consolidated P & L Cr Investment in subsidiary From post-acquistion profits No adjustment is needed

27

Bonus issue From pre-acquistion profits There is no change in the consolidated balance sheet From post acquisition profits Dr post-acquisition profits Cr Capital reserve

28

Sample paper On 1/1/2000, Sally Ltd transferred an item of plant to Henry Ltd for $120000.The item was acquired on 1/1/1998 at a cost if $150000. It had an estimated useful life of 5 years with no residual value. After the item was taken over by Henry Ltd, it was estimated that it still had a useful life of 3 years with no residual value.

29

Adjustment We need to prepare the consolidated B/S as at 31 December 2001 So, there have some adjustment in “retained Profit” The value of the plant on 1/1/2000 = $90000 But Sally Ltd transferred the plant to Henry Ltd for $120000 So, the URP is $30000 But this event happened in the previous year, so we need to correct the RETAINED PROFIT.

30

Dr Retained Profit 30000 Cr Plant 30000 The entry should be made

31

Adjustment Also, depreciation is overstated by 10000 (150000/5 – 120000 / 3 = 10000) For 2000 : Dr provision for dep. 10000 Cr retained profit 10000 For 2001 : Dr provision for dep. 10000 Cr profit & loss 10000

32

2004 Examination report Points to be noted : “Minority Interests“ should be separately disclosed after “shareholders fund”, and not together with other liabilities or reserves.

33

2004 Examination report ( contin ) Since the company’s policy was that minority interests would not share any unrealised profits and losses arising from downstream sales of assets, the amounts unrealised profit on fixed asset and the excess depreciation written back were to be adjusted in consolidated P&L account balance. The amount of unrealised profit on inventories arose form sales and hence was to be shared between the group and the MI in the ratio 8:2 ase 2: The subsidiary issues both ordinary and preference share capital (*** In this case, the MI includes the minority preference shareholders’ interest in the preference dividends and the minority ordinary shareholders’ interest in the remaining profits.)

.")

34

2005 past paper The date of acquistion : 1/1/2003 We need to prepare the balance sheet as at 31/12/2004 Goodwill arising on consolidation is to be written off as an administrative expense over 5 years on a straight line basis. **We need to calculate two years’ amortisation on goodwill and write off the current year amortisation as an administrative expense.

35

Consolidated Income Statement

36

(A) (B) (C) (D) (E)

(B) (C) (D) (E)")

37

Inter-company Sales Since inter-company sales do not constitute any sakes nor cost of sales from the viewpoint of the whole group, they should therefore be eliminated as follows: Dr Consolidated Sales ↓ With the selling price of inter- company sales Cr Consolidated Cost of Sales ↓ ***Inter-company sales are eliminated by reducing both the consolidated sales and the consolidated cost of sales. Part (A)

.")

38

When the H Ltd. sells goods costing $100 to S Ltd. for $120, the unsold inventories of subsidiary would be recorded at $120 in S Ltd.’s balance sheet. However, the unsold inventories should be valued at cost of $100 and the unrealized profit should be provided as follows: Dr Consolidated Cost of Sales$20 Cr Consolidated Inventories$20 URP on unsold stock is eliminated by increasing the consolidated Cost of Sales and reducing the consolidated Inventories.

39

Please remember that, if all the goods from inter- company sales have been sold, no adjustment is needed for the unrealized profit.

40

As a result, the Consolidated Income Statement should be shown as follows:

41

Inter-company Dividends Inter-company dividends should be treated as follows: The inter-company dividends should be eliminated in the consolidated accounts. Part (B) However, we should first ensure that the dividends receivable from subsidiaries have been Cr to the P/L account of H Ltd. before we do the elimination.

However, we should first ensure that the dividends receivable from subsidiaries have been Cr to the P/L account of H Ltd. before we do the elimination..")

42

Minority Interest If the holding company does not own 100% of the shares of the subsidiary, some of the subsidiary’s profit after tax belongs to the minority shareholders. Part (C)

.")

43

The amount will be calculated as follows: Case 1: The subsidiary issues only ordinary share capital Minority Interest = Profit after tax of subsidiary * (1 – Percentage of ordinary shares held)

")

44

Case 2: The subsidiary issues both ordinary and preference share capital (*** In this case, the MI includes the minority preference shareholders’ interest in the preference dividends and the minority ordinary shareholders’ interest in the remaining profits.) Minority Interest = (1 – Percentage of preference shares held) * Preference dividends + (Profit after tax of subsidiary – Preference dividends) * ( 1 – Percentage of ordinary shares held)

Minority Interest = (1 – Percentage of preference shares held) * Preference dividends + (Profit after tax of subsidiary – Preference dividends) * ( 1 – Percentage of ordinary shares held)")

45

Example for Case 2 H Ltd. owns 70% of the issued ordinary share capital and 80% of the issued preference share capital of its subsidiary. (1-* % of pref. Shares held)* Pref. Divd.+(PAT of S – Pref. Divd)*(1-% of Ord. Shares held)

* Pref. Divd.+(PAT of S – Pref. Divd)*(1-% of Ord. Shares held).")

46

Proposed Dividend Inter-company dividends do not represent investment income of the group from outsiders, therefore they should be eliminated in the consolidated income statement. Since MI has already been excluded in arriving at the profit attributable to the group, there is no need to disclose how many dividends should be distributed from the MI. Part (D) Only the dividends paid and proposed by the holding company should be shown.

Only the dividends paid and proposed by the holding company should be shown..")

47

Transfer of Reserves Only the transfer of reserves of the holding company and the share of post-acquisition transfers of the group should be shown in the consolidated P&L. Part (E) Pre-acquisition transfers are capital in nature, therefore they must be excluded. If the subsidiary is acquired part way through an accounting period, the transfer of reserves should be apportioned on a time basis.

Pre-acquisition transfers are capital in nature, therefore they must be excluded. If the subsidiary is acquired part way through an accounting period, the transfer of reserves should be apportioned on a time basis..")

48

Example of Transfer of Reserves H Ltd. Bought 80% of the issued ordinary shares of S Ltd. On 1 April 2003. On 31 Dec. 2003, the directors of H Ltd. And S Ltd. Resolved to transfer $4000 and $1000 to the general reserve respectively. Transfer to General Reserve ($4000 + $1000 * 80% *9/12) = $ 4,600

= $ 4,600.")

49

Past-paper - 2004-I-1(B) Points to be noted: (B) You are required to prepare for the group of Michael Ltd : (b) a statement showing the calculation of consolidated profit and loss account balance as at 31 Dec 2003.

Points to be noted: (B) You are required to prepare for the group of Michael Ltd : (b) a statement showing the calculation of consolidated profit and loss account balance as at 31 Dec 2003.")

50

Past Paper –2005-I-1(A) As at 31 Dec. 2004, Big Ltd owns 400 000 8% preference shares and 220 000 ordinary shares in Small Ltd as an investment. Small Ltd has an issued share capital of 600 000 8% preference shares of $0.5 each fully paid and 500 000 ordinary shares of $1 each fully paid. Required: With respect to Big Ltd’s shareholding in Small Ltd, explain whether Big Ltd is required to prepare consolidated financial statement as at 31 Dec 2004. Points to be noted: Some candidates did not differentiate the holding of preference shares from that of ordinary shares and wrongly counted the majority holding of preference shares as an indication of control. Others mistakenly calculated the percentage of shareholding by grouping the two types of shares.

51

Past Paper – 2005-I-1(B) Points to be noted: Some candidates were not familiar with the adjustments relating to intra-group transactions. Some of them did not adjust the cost of goods sold with the cost of unsold stock. Performance for the consolidated income statement was proved weak. Intra-group debenture interest was generally not excluded and this resulted in an overstatement of financial expenses. The amount of retained profit brought forward should have been reduced by the amounts of goodwill amortization and depreciation adjustment for 2003.

52

Trend Super Hot Topic in 2006 AL Exam.! Prepare Well!

53

*END*

54

URP : stock During the year 2004, goods at invoiced value of $30000 were sold by H To S. 1/3 of these goods remained unsold at the year end. H sell good at a mark-up of 25% ANSWER: The cost : 30000/1.25 = 24000 The extra amount : 30000 – 24000 = 6000 The URP : 6000 x 1/3 = 2000 URP = 2000

55

URP : Debtor At the balance sheet date S owes H $20000 100 70

56

URP : depreciation On 1/1/2003, S transferred a machine to H for $120000. This item was acquired on 1/1/2002 at a cost of $100000. It had an estimated useful life of 5 years with no residual value. After the item was taken over by H, it still had an estimated useful life of 4 years with no residual value. Original dep: 120k / 5yrs = 24k The dep charged after revaluation : 100k / 4yrs = 25k URP : 100k –(120k – 24k)= 4k Dep : overcharged 25k – 24k=1k

= 4k Dep : overcharged 25k – 24k=1k.")

Similar presentations

purchases the share capital of its subsidiary (or subsidiaries), each company in the group: remains a legal.>")