Download presentation

Presentation is loading. Please wait.

1

2012 Tennessee Human Rights Commission Commissioners Meeting July 20, 2012 David Berenbaum, Chief Program Officer National Community Reinvestment Coalition

2

To increase fair & equal access to credit, capital, and banking services/products for low- and moderate-income communities, because discrimination is illegal, unjust and detrimental to the economic growth of underserved communities in the United States and around the world. National Community Reinvestment Coalition Mission

3

Presentation Goals This presentation will focus on NCRCs extensive analysis of Home Mortgage Disclosure Act (HMDA) data in four of the largest Metropolitan Statistical Areas (MSAs) in the state of Tennessee, to identify lenders originating high volume loans and pricing disparities in each jurisdiction. These findings will enable the Commission to make general observations about the mortgage lending activities that have taken place over the past eight years throughout the State. The catalog covers the predatory lending crisis at its pinnacle, collapse of the subprime market, and lending activities in the current foreclosure crisis. Further, the presentation will focus on existing and emerging civil rights and consumer protection issues relating to mortgage lending & mortgage backed securities and securitization principles, including structures and prepayment issues, definitions & policy issues.

4

Emerging Fair Lending Issues Declining Markets/REO Valuation & Appraisal Issues – Use of Automated Valuation Models Minimum Loan Amounts Loan Level Price Adjusters – FHFA as GSE Conservator Credit Overlays (NCRCs Challenge of 40+ Lenders) Portfolio /Servicing Risk Management Regulatory Issues – Qualified Residential Mortgages & QM Standards Down Payment Requirements New Forms of Redlining & Reverse Redlining – Pricing Disparate Impact Issues

Portfolio /Servicing Risk Management Regulatory Issues – Qualified Residential Mortgages & QM Standards Down Payment Requirements New Forms of Redlining & Reverse Redlining – Pricing Disparate Impact Issues")

5

Disparate Impact Doctrine Disparate Impact Issues Cordray – The Silent Pickpocket HUD FHEO Rulemaking FHIP/FHAP 2013 Budget – House Rs Disparate Impact Rule Funding Prohibition

6

Source: Andrew Davidson & Co Mortgage Market Components

7

Source: MBA National Delinquency Survey Judicial vs. Non-Judicial Foreclosure Trends

8

Share of Home Purchase Lending, by Loan Type, 2006-09

9

Source: Census, National Association of Realtors Inventory of Homes for Sale + Shadow Inventory

10

Source: Mortgage Bankers Association & Census Bureau Thousands of households Homeownership rate (%) Since the end of 2006, the US has added 4.2 million renter households and lost 1.2 million owner households

Since the end of 2006, the US has added 4.2 million renter households and lost 1.2 million owner households")

11

Source: MBA Weekly Application Survey Purchase Applications

12

Source: MBA Weekly Application Survey Refi Apps

13

DOJ Settlements US v. Wells Fargo $175 Million Settlement ($125M for settlement + $50M in direct down payment assistance) Borrower Assistance Program Wells Fargo steered borrowers into subprime loans from 2004- 2009 Countrywide $335 Million Settlement African-Americans/Hispanics paid more than White borrowers Countrywide steered borrowers into subprime loans from 2004- 2007

Borrower Assistance Program Wells Fargo steered borrowers into subprime loans from Countrywide $335 Million Settlement African-Americans/Hispanics paid more than White borrowers Countrywide steered borrowers into subprime loans from")

14

$25 Billion Joint Federal/State Mortgage Settlement with Five Servers Servicers commit a minimum of $17 billion directly to borrowers through a series of national homeowner relief effort options, including principal reduction. Servicers will likely provide up to an estimated $32 billion in direct homeowner relief. Servicers commit $3 billion to an underwater mortgage refinancing program. Servicers pay $5 billion to the states and federal government ($4.25 billion to the states and $750 million to the federal government). Homeowners receive comprehensive new protections from new mortgage loan servicing and foreclosure standards. An independent monitor will ensure mortgage servicer compliance. Government can pursue civil claims outside of the agreement, any criminal case; borrowers and investors can pursue individual, institutional or class action cases regardless of agreement.

. Homeowners receive comprehensive new protections from new mortgage loan servicing and foreclosure standards. An independent monitor will ensure mortgage servicer compliance. Government can pursue civil claims outside of the agreement, any criminal case; borrowers and investors can pursue individual, institutional or class action cases regardless of agreement..")

15

Credit Overlays (NCRC Challenge) NCRC Consulted with FHA on Development of new underwriting criteria to ensure access to credit while stabilizing the FHA portfolios. FHA established minimum FICO of 580 with 3.5% down based on portfolio performance to ensure equal access to credit for both purchase and refinance loans to all consumers who use FHA 25% of all Americans have a FICO Below 620, but a disproportionate number qualified African Americans & Latinos fall into this range, increasing the importance of the FHA loan program in communities of color. FHA Intended Underwriting to Help At-Risk Homeowners to Refi.

16

Credit Overlays (NCRC Challenge) cont. NCRC became aware of lenders applying more restrictive underwriting standards despite new FHA rules in Spring 2010. NCRC role as a National HUD Counseling Intermediary exposed: Qualified protected class consumers being denied access to credit; Member groups & HUD Certified Housing Counseling Agencies raising red flags at meetings & trainings; FHA lending being discussed at Industry compliance programs, conferences & meetings; Meetings with FHA & regulators & Media Inquiries NCRC is also examining impact of other restrictive policies, including those introduced by the GSEs and being used in VA & USDA Loan Programs.

17

NCRC Investigation of FHA Residential Loan Program Lender FICO Requirements

18

NCRC sent challenge letters to over 45 FHA participating lenders. Notably, 16 immediately agreed to direct discussions. NCRC also filed 24 HUD FHEO Complaints & requested investigations by prudential regulators. The investigation forced NCRC and our member organizations to divert resources and the lenders and investors discriminatory practices frustrated our mission. NCRC Challenge has resulted in 19 Lenders Abandoning Practice and 23 FHEO Complaints. Over 10,000 Loans Originated. Credit Overlays (NCRC Challenge) cont.

cont..")

19

Overview of Home Mortgage Disclosure Act (HMDA) Home Mortgage Disclosure Act (HMDA) has three purposes: 1.To help determine whether financial institutions are serving the housing needs of their communities 2.To assist public officials in distributing public-sector investment so as to attract private sector investment to areas where it is needed 3.To assist in identifying possible discriminatory lending patterns and enforcing anti- discrimination statutes

Home Mortgage Disclosure Act (HMDA) has three purposes: 1.To help determine whether financial institutions are serving the housing needs of their communities 2.To assist public officials in distributing public-sector investment so as to attract private sector investment to areas where it is needed 3.To assist in identifying possible discriminatory lending patterns and enforcing anti- discrimination statutes")

20

Overview of Home Mortgage Disclosure Act (HMDA)cont. Loan Information: -What action was taken with the loan -Information on pre-approval and denial -Dollar amount of the loan -Loan type -Purpose of the loan -Pricing date for high-cost loans -Lien status indicated -Purchasers of loans -Reporting if loans are covered by HOEPA -Reporting institution

21

Investigative Options: Disparate Impact Lending discrimination cases generally fall into the following three categories: 1.Discrimination based on the race or other protected class status of an applicant or borrower; 2.Discrimination based on the unwillingness to lend to applicants or borrowers in particular neighborhoods or geographic regions, known asredlining; 3.Targeting applicants or residents in certain geographic areas for disadvantageous or abusive loan terms or conditions based on race, age and/or other protected class basis of the residents in such communities, known as reverse redlining.

22

Investigative Options: Disparate Impact cont. To establish a prima facie case for Disparate Impact, the complainant must show: 1.He/she is a member of a protected class entitled to protection, and the respondent was aware of the complainants protected class status; 2.The complainant applied for and was qualified for a loan* 3.The respondent rejected, or otherwise failed to approve the application on favorable terms and conditions, despite the complainants qualifications; and 4.The respondent continued to approve loans, or provided more favorable terms and conditions, with respect to contrasting class applicants with qualifications substantially similar to those of the complainant * #2 may be separate elements. If so, there will be five elements of a prima facie case

23

Investigative Plan Complaint(s) Intake Disparate Impact vs. Treatment Redlining vs. Reverse Redlining File Analysis Eligibility – servicing, refi, origination Valuation Issues Public Data Analysis Comparative File Review Fair Lending Testing Prudential Regulators HUD Counseling Agencies Fair Housing Organizations Affirmatively Furthering Fair Housing

24

Tennessee Metropolitan Statistical Areas (MSAs) 2004 Percentage of Loan Applicants in Chattanooga, Knoxville, Memphis & Nashville

2004 Percentage of Loan Applicants in Chattanooga, Knoxville, Memphis & Nashville")

25

Tennessee Metropolitan Statistical Areas (MSAs) 2006 Percentage of Loan Applicants in Chattanooga, Knoxville, Memphis & Nashville

2006 Percentage of Loan Applicants in Chattanooga, Knoxville, Memphis & Nashville")

26

Tennessee Metropolitan Statistical Areas (MSAs) 2008 Percentage of Loan Applicants in Chattanooga, Knoxville, Memphis & Nashville

2008 Percentage of Loan Applicants in Chattanooga, Knoxville, Memphis & Nashville")

27

Tennessee Metropolitan Statistical Areas (MSAs) 2010 Percentage of Loan Applicants in Chattanooga, Knoxville, Memphis & Nashville

2010 Percentage of Loan Applicants in Chattanooga, Knoxville, Memphis & Nashville")

28

Tennessee Metropolitan Statistical Areas (MSAs) Percentage of Purchase Loans

Percentage of Purchase Loans")

29

Tennessee Metropolitan Statistical Areas (MSAs) Percentage of Refinance Loans

Percentage of Refinance Loans")

30

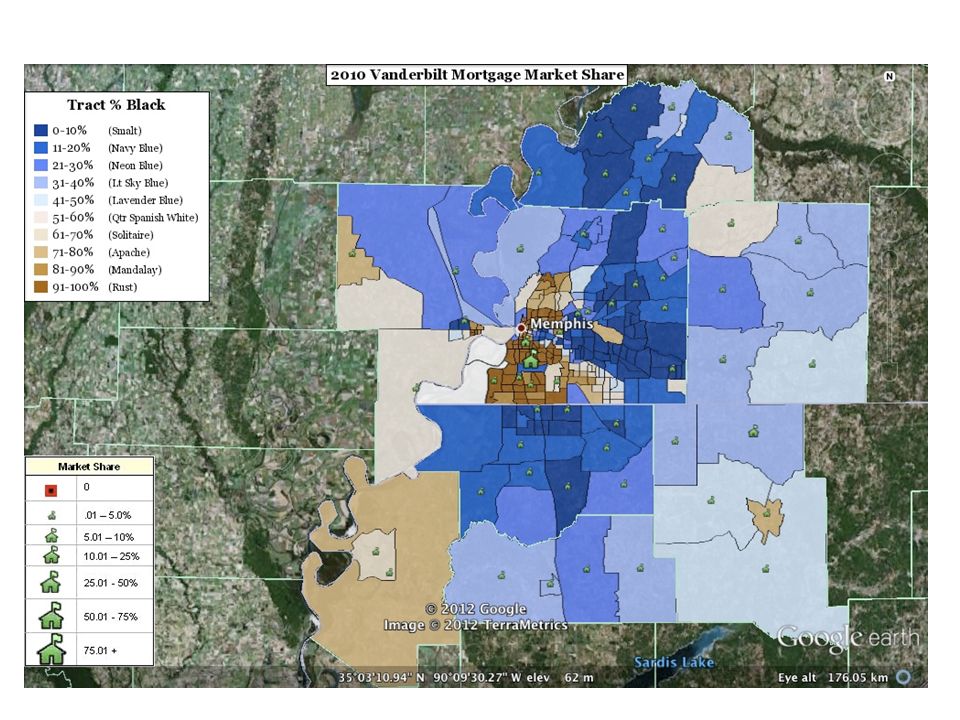

Investigative Options MARKETWHITEOTHER NAMETYPEVOLUMESHARE %AVG SPREAD AHSDI JP Morgan Chase BankPrime12,3733.682.063.011.46 First Tennessee BankPrime6,0331.81.922.111.1 Vanderbilt MortgageManufactured4,0131.194.835.311.1 USAA FSBPrime3,1480.944.275.661.32 Flagstar Bank FSBPrime2,2280.661.631.821.12

39

Conclusion For more information please contact: David Berenbaum, Chief Program Officer; or Cheryl Cassell, Director, NCRC Housing Counseling Network National Community Reinvestment Coalition 727 15th Street, Suite 900 Washington, DC 20005 dberenbaum@ncrc.org P: (202) 628.8866 F: (202) 628.9800 www.ncrc.org

F: (202)")

Similar presentations

City of Missoula.>")

Orange County, Florida.>")

, 15 U.S.C.>")