Download presentation

Presentation is loading. Please wait.

1

Unemployment, Inflation and Growth

2

Money and Prices The quantity theory of money The equation of exchange: MV = PY –M money supply –V velocity of circulation –P price level (number of times greater than in base year) –Y real value of output at base-year prices –MV = PQ The link between money and prices –quantity theory holds if V and Y are determined independently of M The quantity theory of money The equation of exchange: MV = PY –M money supply –V velocity of circulation –P price level (number of times greater than in base year) –Y real value of output at base-year prices –MV = PQ The link between money and prices –quantity theory holds if V and Y are determined independently of M

–Y real value of output at base-year prices –MV = PQ The link between money and prices –quantity theory holds if V and Y are determined independently of M The quantity theory of money The equation of exchange: MV = PY –M money supply –V velocity of circulation –P price level (number of times greater than in base year) –Y real value of output at base-year prices –MV = PQ The link between money and prices –quantity theory holds if V and Y are determined independently of M")

3

Money and Prices Assumptions about the velocity of circulation –the short run uncertain relationship between money and prices the monetary transmission mechanism –the money–interest rate link –the interest rate–spending link –the long run the theory of portfolio balance Assumptions about the velocity of circulation –the short run uncertain relationship between money and prices the monetary transmission mechanism –the money–interest rate link –the interest rate–spending link –the long run the theory of portfolio balance

4

Money and Prices Assumptions about output and prices –the short-run aggregate supply curve relatively elastic in short run –stickiness of wages and prices –confidence Assumptions about output and prices –the short-run aggregate supply curve relatively elastic in short run –stickiness of wages and prices –confidence

5

O Price level National output AS Different aggregate supply curves

6

O AS Price level National output Y1Y1 P1P1 AD 1 Different aggregate supply curves

7

P2P2 O AS Y1Y1 Price level National output Y2Y2 P1P1 AD 2 AD 1 Different aggregate supply curves

8

Q1Q1 Short-run response of a profit-maximising firm to a rise in demand MC AR 1 MR 1 £ Q P1P1

9

AR 1 MR 1 P1P1 Q1Q1 AR 2 MR 2 £ Q MC Short-run response of a profit-maximising firm to a rise in demand

10

AR 1 MR 1 P1P1 Q1Q1 AR 2 MR 2 Q2Q2 P2P2 £ Q MC Short-run response of a profit-maximising firm to a rise in demand

11

Money and Prices Assumptions about output and prices –the short-run aggregate supply curve relatively elastic in short run –stickiness of wages and prices –confidence –the long run aggregate supply curve Assumptions about output and prices –the short-run aggregate supply curve relatively elastic in short run –stickiness of wages and prices –confidence –the long run aggregate supply curve

12

Money and Prices Assumptions about output and prices –the short-run aggregate supply curve relatively elastic in short run –stickiness of wages and prices –confidence –the long run aggregate supply curve relatively inelastic Assumptions about output and prices –the short-run aggregate supply curve relatively elastic in short run –stickiness of wages and prices –confidence –the long run aggregate supply curve relatively inelastic

13

O AS Price level National output Y Different aggregate supply curves

14

P1P1 O Price level National output AD 1 Y AS Different aggregate supply curves

15

O P1P1 Price level National output AD 2 P2P2 Y AS AD 1 Different aggregate supply curves

16

Money and Prices Assumptions about output and prices –the short-run aggregate supply curve relatively elastic in short run –stickiness of wages and prices –confidence –the long run aggregate supply curve relatively inelastic –the interdependence of markets Assumptions about output and prices –the short-run aggregate supply curve relatively elastic in short run –stickiness of wages and prices –confidence –the long run aggregate supply curve relatively inelastic –the interdependence of markets

17

Money and Prices Assumptions about output and prices –the short-run aggregate supply curve relatively elastic in short run –stickiness of wages and prices –confidence –the long run aggregate supply curve relatively inelastic –the interdependence of markets –the flexibility of prices Assumptions about output and prices –the short-run aggregate supply curve relatively elastic in short run –stickiness of wages and prices –confidence –the long run aggregate supply curve relatively inelastic –the interdependence of markets –the flexibility of prices

18

O Price level National output AD 1 SRAS 1 (expected price level = P 1 ) P1P1 Q1Q1 a The long-run aggregate supply curve when firms are interdependent

P1P1 Q1Q1 a The long-run aggregate supply curve when firms are interdependent")

19

O Price level National output AD 1 SRAS 1 (expected price level = P 1 ) P1P1 AD 2 a b P2P2 Q2Q2 SRAS 2 (expected price level = P 3 ) P3P3 c Q1Q1 The long-run aggregate supply curve when firms are interdependent

P1P1 AD 2 a b P2P2 Q2Q2 SRAS 2 (expected price level = P 3 ) P3P3 c Q1Q1 The long-run aggregate supply curve when firms are interdependent")

20

O Price level National output AD 1 SRAS 1 (expected price level = P 1 ) P1P1 QnQn AD 2 a b P2P2 Q2Q2 SRAS 2 (expected price level = P 3 ) c P3P3 LRAS The long-run aggregate supply curve when firms are interdependent

P1P1 QnQn AD 2 a b P2P2 Q2Q2 SRAS 2 (expected price level = P 3 ) c P3P3 LRAS The long-run aggregate supply curve when firms are interdependent")

21

Money and Prices Assumptions about output and prices –the short-run aggregate supply curve relatively elastic in short run –stickiness of wages and prices –confidence –the long run aggregate supply curve relatively inelastic –the interdependence of markets –the flexibility of prices the effects of investment on aggregate supply Assumptions about output and prices –the short-run aggregate supply curve relatively elastic in short run –stickiness of wages and prices –confidence –the long run aggregate supply curve relatively inelastic –the interdependence of markets –the flexibility of prices the effects of investment on aggregate supply

22

Effect of investment on the long-run AS curve AD 1 Price level National output a AS 1 (short run)

")

23

AS (long run) AS 2 (short run) AD 1 Price level National output a AD 2 b d AS 1 (short run) Effect of investment on the long-run AS curve

AS 2 (short run) AD 1 Price level National output a AD 2 b d AS 1 (short run) Effect of investment on the long-run AS curve")

24

Inflation and Unemployment: Introducing Expectations Expectations augmented Phillips curve –adaptive expectations Expectations augmented Phillips curve –adaptive expectations

25

O P (%). U (%) a P1P1. U1U1 P2P2. U2U2 A Phillips curve b

. U (%) a P1P1. U1U1 P2P2. U2U2 A Phillips curve b")

26

Expectations augmented Phillips curve –adaptive expectations The accelerationist theory Expectations augmented Phillips curve –adaptive expectations The accelerationist theory Inflation and Unemployment: Introducing Expectations

27

Expectations augmented Phillips curve –adaptive expectations The accelerationist theory –accelerating inflation Expectations augmented Phillips curve –adaptive expectations The accelerationist theory –accelerating inflation Inflation and Unemployment: Introducing Expectations

28

Expectations augmented Phillips curve –adaptive expectations The accelerationist theory –accelerating inflation when unemployment is kept below the ‘natural’ level Expectations augmented Phillips curve –adaptive expectations The accelerationist theory –accelerating inflation when unemployment is kept below the ‘natural’ level Inflation and Unemployment: Introducing Expectations

29

P (%). U (%) 6 8 I (P e = 0). b The accelerationist theory of inflation a

. U (%) 6 8 I (P e = 0). b The accelerationist theory of inflation a")

30

IV (P e = 12%). III (P e = 8%). II (P e = 4%) P (%). U (%) 6 a b c d 8 I (P e = 0).. e The accelerationist theory of inflation f

6 a b c d 8 I (P e = 0).. e The accelerationist theory of inflation f.")

31

Expectations augmented Phillips curve –adaptive expectations The accelerationist theory –accelerating inflation when unemployment is kept below the ‘natural’ level –the long-run Phillips curve Expectations augmented Phillips curve –adaptive expectations The accelerationist theory –accelerating inflation when unemployment is kept below the ‘natural’ level –the long-run Phillips curve Inflation and Unemployment: Introducing Expectations

32

UnUn P (%). U (%) 6 8 The long-run Phillips curve

. U (%) 6 8 The long-run Phillips curve")

33

Expectations augmented Phillips curve –adaptive expectations The accelerationist theory –accelerating inflation when unemployment is kept below the ‘natural’ level –the long-run Phillips curve –effects of deflationary policies Expectations augmented Phillips curve –adaptive expectations The accelerationist theory –accelerating inflation when unemployment is kept below the ‘natural’ level –the long-run Phillips curve –effects of deflationary policies Inflation and Unemployment: Introducing Expectations

34

P (%). U (%) 8 13 J X (P e = 20%). k The effects of deflation

. U (%) 8 13 J X (P e = 20%). k The effects of deflation")

35

P (%). U (%) 8 13 k X (P e = 20%). XI (P e = 18%). XII (P e = 16%). l J m The effects of deflation

. U (%) 8 13 k X (P e = 20%). XI (P e = 18%). XII (P e = 16%). l J m The effects of deflation")

36

P (%). U (%) 8 13 k l m a J The effects of deflation

. U (%) 8 13 k l m a J The effects of deflation")

37

Expectations augmented Phillips curve –adaptive expectations The accelerationist theory –accelerating inflation when unemployment is kept below the ‘natural’ level –the long-run Phillips curve –effects of deflationary policies Phillips loops Expectations augmented Phillips curve –adaptive expectations The accelerationist theory –accelerating inflation when unemployment is kept below the ‘natural’ level –the long-run Phillips curve –effects of deflationary policies Phillips loops Inflation and Unemployment: Introducing Expectations

38

Year 2 P (%). U (%) UnUn a b c Year 0, 1 Clockwise Phillips loops

. U (%) UnUn a b c Year 0, 1 Clockwise Phillips loops")

39

Year 5 Year 4 P (%). U (%) UnUn a b c d e f Year 0, 1 Year 2 Year 3 Clockwise Phillips loops

. U (%) UnUn a b c d e f Year 0, 1 Year 2 Year 3 Clockwise Phillips loops")

40

P (%). U (%) UnUn a b c d e f h i J Year 0, 1, 10 Year 2, 9 Year 3, 8 Year 4, 7 Year 5, 8 Clockwise Phillips loops g

UnUn a b c d e f h i J Year 0, 1, 10 Year 2, 9 Year 3, 8 Year 4, 7 Year 5, 8 Clockwise Phillips loops g.")

41

Expectations augmented Phillips curve –adaptive expectations The accelerationist theory –accelerating inflation when unemployment is kept below the ‘natural’ level –the long-run Phillips curve –effects of deflationary policies Phillips loops Policy implications Expectations augmented Phillips curve –adaptive expectations The accelerationist theory –accelerating inflation when unemployment is kept below the ‘natural’ level –the long-run Phillips curve –effects of deflationary policies Phillips loops Policy implications Inflation and Unemployment: Introducing Expectations

42

Inflation and Unemployment: New Classical Views Assumption of flexible wages and prices Rational expectations –meaning of rational expectations –imperfect information –implications for AS and the Phillips curve –policy implications Real business cycles –fluctuations in aggregate supply –causes of changes in aggregate supply –policy implications Assumption of flexible wages and prices Rational expectations –meaning of rational expectations –imperfect information –implications for AS and the Phillips curve –policy implications Real business cycles –fluctuations in aggregate supply –causes of changes in aggregate supply –policy implications

43

Inflation and Unemployment: Keynesian Views Changes in equilibrium unemployment –structural unemployment –hysteresis The persistence of demand-deficient unemployment –payment of efficiency wages –insider power Incorporation of expectations –expansion of aggregate demand –contraction of aggregate demand Keynesian criticism of non-intervention Changes in equilibrium unemployment –structural unemployment –hysteresis The persistence of demand-deficient unemployment –payment of efficiency wages –insider power Incorporation of expectations –expansion of aggregate demand –contraction of aggregate demand Keynesian criticism of non-intervention

44

Common ground between economists? Short-run effect of changes in AD –major effect on output and employment –relatively small effect on prices Long-run effect of changes in AD –relatively small effect on output and jobs –relatively large effect on prices –some Keynesians disagree stress long-run effects of changes in AD on investment Importance of expectations Short-run effect of changes in AD –major effect on output and employment –relatively small effect on prices Long-run effect of changes in AD –relatively small effect on output and jobs –relatively large effect on prices –some Keynesians disagree stress long-run effects of changes in AD on investment Importance of expectations

45

Demand-side Policy Attitudes towards demand management Case against discretion –time lags –problem of over-correction –government may ignore long-term consequences Case for rules –help to reduce inflationary expectations –create a stable environment for investment and growth Attitudes towards demand management Case against discretion –time lags –problem of over-correction –government may ignore long-term consequences Case for rules –help to reduce inflationary expectations –create a stable environment for investment and growth

46

Source: The Use of Explicit Targets for Monetary Policy: Practical Experiences of 91 economies in the 1990s, (Bank of England, August 1999) Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation

Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation")

47

Source: The Use of Explicit Targets for Monetary Policy: Practical Experiences of 91 economies in the 1990s, (Bank of England, August 1999) Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation

Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation")

48

Source: The Use of Explicit Targets for Monetary Policy: Practical Experiences of 91 economies in the 1990s, (Bank of England, August 1999) Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation

Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation")

49

Source: The Use of Explicit Targets for Monetary Policy: Practical Experiences of 91 economies in the 1990s, (Bank of England, August 1999) Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation

Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation Who sets explicit targets and monitoring ranges for the exchange rate, money and inflation")

50

Demand-side Policy Case against rules –can cause severe fluctuations in interest rates and can cause greater instability –which rule to choose? –rules may conflict –rules may become unsuitable Case for discretion –fine tuning can be improved by better forecasting and quick-acting policies –allows governments to respond to changing circumstances Case against rules –can cause severe fluctuations in interest rates and can cause greater instability –which rule to choose? –rules may conflict –rules may become unsuitable Case for discretion –fine tuning can be improved by better forecasting and quick-acting policies –allows governments to respond to changing circumstances

51

Demand-side Policy Demand-side policy in the UK –increasingly rules-based –fiscal policy 'golden rule' but some flexibility –monetary policy target of 2% inflation set by government Monetary Policy Committee adjusts interest rates to meet this 2% target benefits of transparency benefits for expectations Demand-side policy in the UK –increasingly rules-based –fiscal policy 'golden rule' but some flexibility –monetary policy target of 2% inflation set by government Monetary Policy Committee adjusts interest rates to meet this 2% target benefits of transparency benefits for expectations

52

Long-term Economic Growth Growth over the decades

53

UK GDP at market prices (1995=100)

")

55

Long-term Economic Growth The causes of economic growth –increase in quantity of factors –increase in productivity of factors Capital accumulation –a simple model of economic growth effect of an increase in capital diminishing returns steady-state national income The causes of economic growth –increase in quantity of factors –increase in productivity of factors Capital accumulation –a simple model of economic growth effect of an increase in capital diminishing returns steady-state national income

56

K0K0 Depreciation (D) Investment (I) Steady-state output Capital stock (K) Output (Y), Investment (I), Depreciation (D) K1K1 Y1Y1 Output (Y) g Y0Y0 b I0I0 D0D0 O c f a

Investment (I) Steady-state output Capital stock (K) Output (Y), Investment (I), Depreciation (D) K1K1 Y1Y1 Output (Y) g Y0Y0 b I0I0 D0D0 O c f a")

57

Long-term Economic Growth The causes of economic growth –increase in quantity of factors –increase in productivity of factors Capital accumulation –a simple model of economic growth effect of an increase in capital diminishing returns steady-state national income –effect of an increase in the saving rate The causes of economic growth –increase in quantity of factors –increase in productivity of factors Capital accumulation –a simple model of economic growth effect of an increase in capital diminishing returns steady-state national income –effect of an increase in the saving rate

58

Capital stock (K) K1K1 K2K2 Y2Y2 Y1Y1 Y D I2I2 I1I1 g m n h Output (Y), Investment (I), Depreciation (D) f Effect of an increase in the rate of saving and investment

K1K1 K2K2 Y2Y2 Y1Y1 Y D I2I2 I1I1 g m n h Output (Y), Investment (I), Depreciation (D) f Effect of an increase in the rate of saving and investment")

59

Long-term Economic Growth Technological progress –effect on steady-state output Technological progress –effect on steady-state output

60

Capital stock (K) K1K1 K2K2 Y2Y2 Y2Y2 D I2I2 I1I1 g p n h Output (Y), Investment (I), Depreciation (D) Effect of a technological advance Y1Y1 Y1Y1 f

K1K1 K2K2 Y2Y2 Y2Y2 D I2I2 I1I1 g p n h Output (Y), Investment (I), Depreciation (D) Effect of a technological advance Y1Y1 Y1Y1 f")

61

Long-term Economic Growth Technological progress –effect on steady-state output –endogenous growth theory Technological progress –effect on steady-state output –endogenous growth theory

62

Long-term Economic Growth Productivity and economic growth –importance of productivity –determinants of productivity private investment public investment in infrastructure and education innovation business environment management and entrepreneurial activity Productivity and economic growth –importance of productivity –determinants of productivity private investment public investment in infrastructure and education innovation business environment management and entrepreneurial activity

63

Supply-side Policy The use of supply-side policies –to reduce unemployment –to reduce inflation –to increase economic growth Market-orientated supply-side policies –reducing government expenditure The use of supply-side policies –to reduce unemployment –to reduce inflation –to increase economic growth Market-orientated supply-side policies –reducing government expenditure

64

Government expenditure (central plus local) as a percentage of GDP

as a percentage of GDP")

71

Supply-side Policy Market-orientated supply-side policies –reducing government expenditure –tax cuts Market-orientated supply-side policies –reducing government expenditure –tax cuts

72

Supply-side Policy Market-orientated supply-side policies –reducing government expenditure –tax cuts effects on labour supply and employment Market-orientated supply-side policies –reducing government expenditure –tax cuts effects on labour supply and employment

73

Supply-side Policy Market-orientated supply-side policies –reducing government expenditure –tax cuts effects on labour supply and employment importance of incentives Market-orientated supply-side policies –reducing government expenditure –tax cuts effects on labour supply and employment importance of incentives

74

Supply-side Policy Market-orientated supply-side policies –reducing government expenditure –tax cuts effects on labour supply and employment importance of incentives effects on imports Market-orientated supply-side policies –reducing government expenditure –tax cuts effects on labour supply and employment importance of incentives effects on imports

75

Supply-side Policy Market-orientated supply-side policies –reducing government expenditure –tax cuts effects on labour supply and employment importance of incentives effects on imports tax cuts for business Market-orientated supply-side policies –reducing government expenditure –tax cuts effects on labour supply and employment importance of incentives effects on imports tax cuts for business

76

Supply-side Policy Market-orientated supply-side policies (cont.) –reducing the power of labour –reducing welfare –policies to encourage competition privatisation deregulation introducing market relationships into the public sector the Private Finance Initiative free trade and capital movements Market-orientated supply-side policies (cont.) –reducing the power of labour –reducing welfare –policies to encourage competition privatisation deregulation introducing market relationships into the public sector the Private Finance Initiative free trade and capital movements

–reducing the power of labour –reducing welfare –policies to encourage competition privatisation deregulation introducing market relationships into the public sector the Private Finance Initiative free trade and capital movements Market-orientated supply-side policies (cont.) –reducing the power of labour –reducing welfare –policies to encourage competition privatisation deregulation introducing market relationships into the public sector the Private Finance Initiative free trade and capital movements")

77

Supply-side Policy Background to interventionist policy –the UK's poor productivity record Background to interventionist policy –the UK's poor productivity record

78

Productivity in selected countries, 2001 (UK = 100) Source: Budget 2003, Economic and Fiscal Strategy Report (HM Treasury, 2003)

Source: Budget 2003, Economic and Fiscal Strategy Report (HM Treasury, 2003)")

79

Productivity in selected countries, 2001 (UK = 100) Source: Budget 2003, Economic and Fiscal Strategy Report (HM Treasury, 2003)

Source: Budget 2003, Economic and Fiscal Strategy Report (HM Treasury, 2003)")

80

Productivity in selected countries, 2001 (UK = 100) Source: Budget 2003, Economic and Fiscal Strategy Report (HM Treasury, 2003)

Source: Budget 2003, Economic and Fiscal Strategy Report (HM Treasury, 2003)")

81

Productivity in selected countries, 2001 (UK = 100) Source: Budget 2003, Economic and Fiscal Strategy Report (HM Treasury, 2003)

Source: Budget 2003, Economic and Fiscal Strategy Report (HM Treasury, 2003)")

82

Supply-side Policy Background to interventionist policy –the UK's poor productivity record –the UK's poor investment record Background to interventionist policy –the UK's poor productivity record –the UK's poor investment record

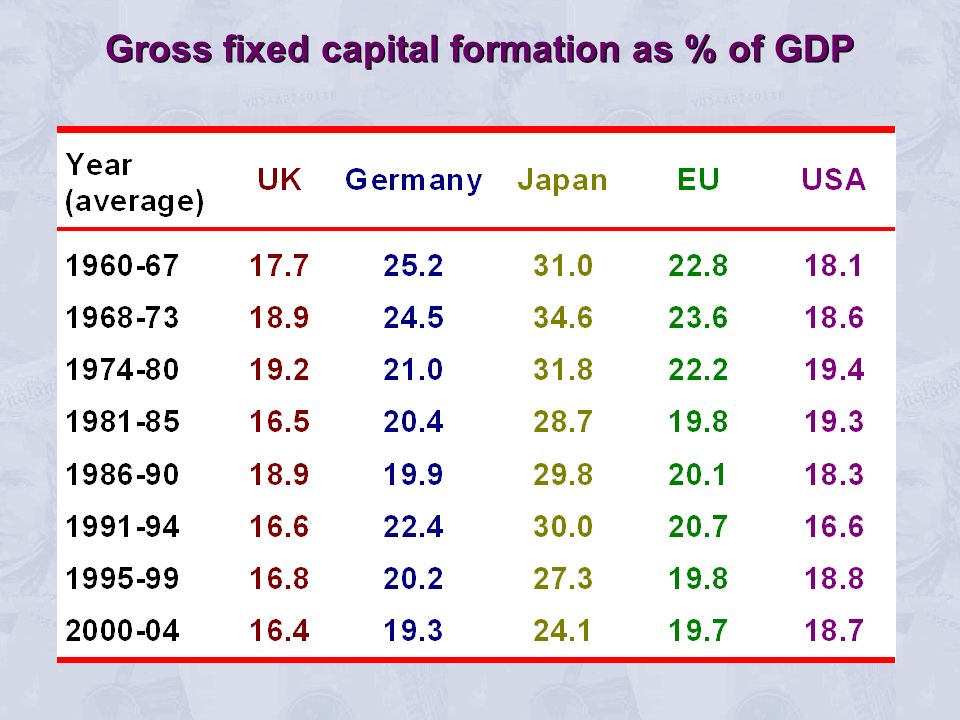

83

Gross fixed capital formation as % of GDP

89

Supply-side Policy Interventionist supply-side policy –failure of the market to provide adequate training, R&D and investment –help to firms direct provision finance for research and development assistance to small firms advice and persuasion information –infrastructure development –training and education Interventionist supply-side policy –failure of the market to provide adequate training, R&D and investment –help to firms direct provision finance for research and development assistance to small firms advice and persuasion information –infrastructure development –training and education

Similar presentations

>")

>")

>")