Download presentation

Presentation is loading. Please wait.

1

Louisiana CPA-52 Economic and Social Considerations

2

SWAPA + H

3

Economic and Social Considerations: “It’s the policy of the Department of Agriculture and the NRCS that economic principles be included in all planning and agency resource allocation activities” (GM200-Economics, Subpart A, 400)

")

5

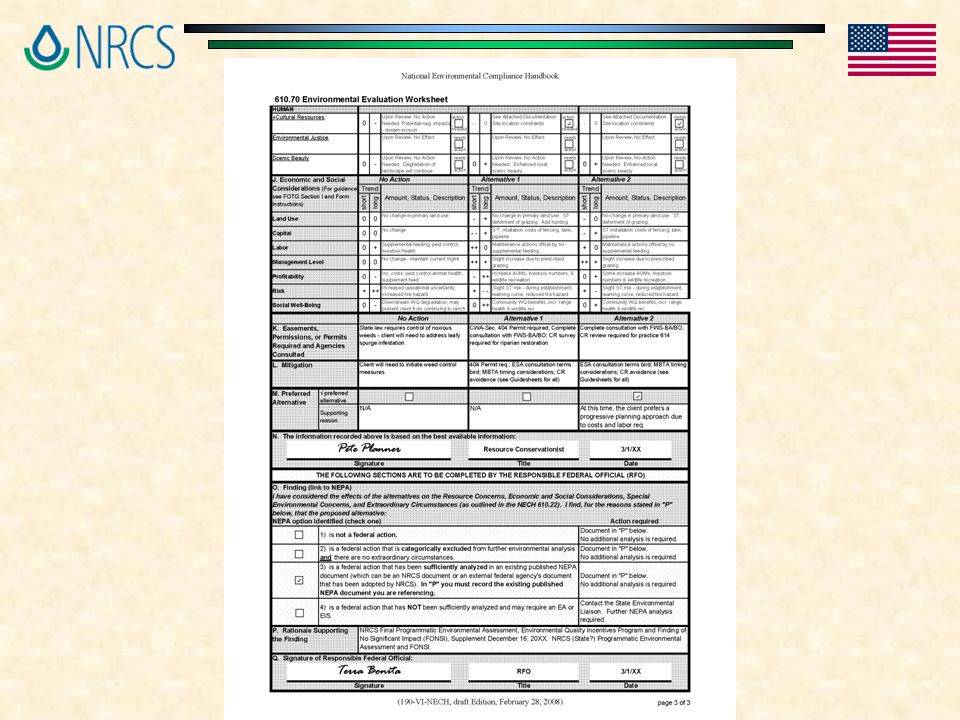

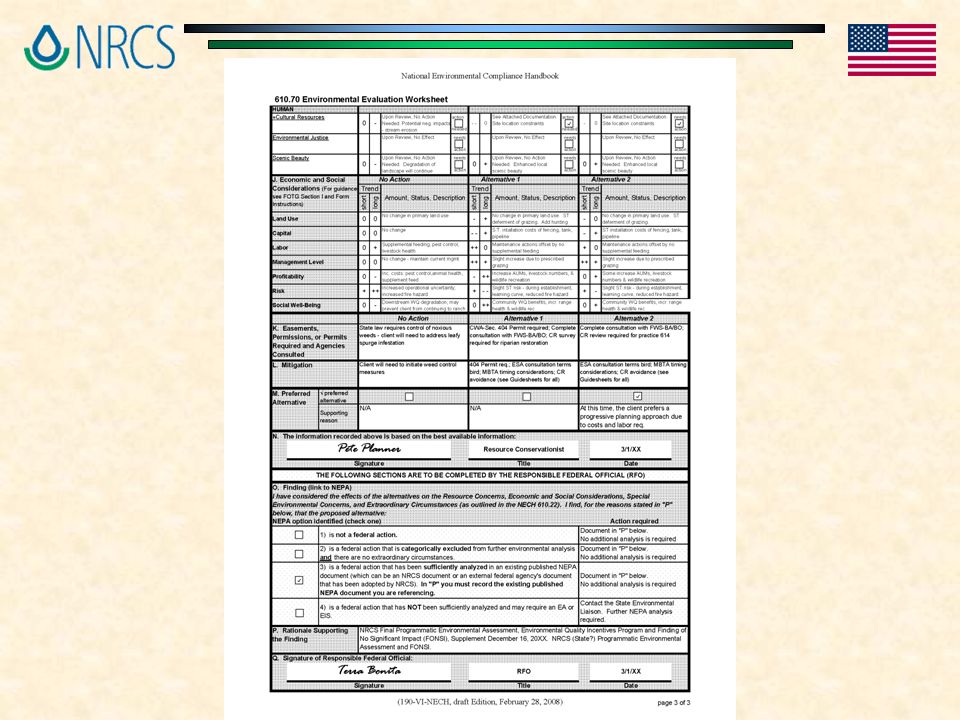

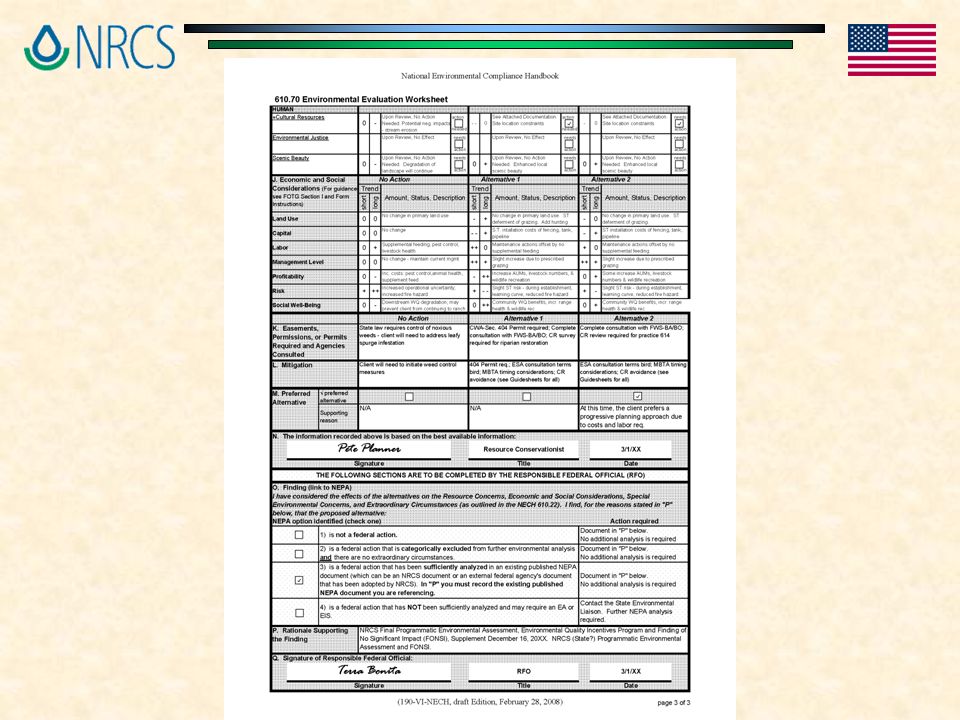

There are seven categories to evaluate when looking at Economic and Social Considerations - Land Use - Capital - Labor - Management Level - Profitability - Risk - Social Well-Being

6

Alternatives “No Action” “Alternative 1” Proposed action Etc.

7

Consider the Cumulative Effects

8

Short-term vs. Long-term (+) vs. (-)

vs. (-)")

10

Amount, Statue, Description “No change in primary land use”

12

Land Use Land is the Basic Unit of Production Where Crops are Grown, Livestock Graze Where Wildlife Live Land is Measured in Acres Productivity is Measured in Bushels, AUM’s, etc. Farm Machinery & Structures are Included

13

Land Use Is the present land use suitable for the proposed alternative? Will land use change after practice(s) installation? How will a change affect the operation? Will the action affect resources on which people depend for subsistence, employment or recreation? Will land be taken in or out of production?

installation. How will a change affect the operation. Will the action affect resources on which people depend for subsistence, employment or recreation. Will land be taken in or out of production .")

14

Capital The Landowner’s “Ability to Pay” Measured As Monetary Assets (Dollars) Physical Assets (Land & Machinery) Ability to Borrow Money (Credit) Obtain Financial Assistance (Cost-Share) Barter “Goods & Services” And in the long term some practices, particularly structural, may be considered capital.

Physical Assets (Land & Machinery) Ability to Borrow Money (Credit) Obtain Financial Assistance (Cost-Share) Barter Goods & Services And in the long term some practices, particularly structural, may be considered capital.")

15

Capital Does the Producer have the funds or ability to obtain the funds needed to implement the proposed alternative? What are the impacts of the cost of the initial investment for this alternative? What are the impacts of an additional annual cost for Operation and Maintenance (O&M)? Does he have, or obtainable? What possible impact does implementing this alternative have on the client’s future eligibility for farm programs?

. Does he have, or obtainable. What possible impact does implementing this alternative have on the client’s future eligibility for farm programs .")

16

Labor The “Ability to Work” or Hire “Workers” Measured in Units of Time (Hours, Years) Includes the Landowner, Family, Hired Help or Other Trained Workers

Includes the Landowner, Family, Hired Help or Other Trained Workers")

17

Labor Does the client understand the amount and kind of labor needed to implement, operate and maintain the proposed practice (s)? Does the client have the skills and time to carry out the conservation practice(s) as it is planned or will they have to hire someone? Rather, Is there adequate labor to implement, operate and maintain the conservation plan?

as it is planned or will they have to hire someone. Rather, Is there adequate labor to implement, operate and maintain the conservation plan .")

18

Management Level The Landowner’s “Knowledge, Skills and Ability” To Operate the Farm or Ranch Measured in Qualitative Units of Skill Level

19

Management Level Does the client understand the inputs needed to manage the practice(s) and the client’s responsibility in obtaining these inputs? Does the client understand their responsibility to maintain practice (s) as planned and implemented? Is it necessary for the client to obtain additional education, or hire a technical consultant, to operate and/or maintain the practice (s)? Rather, does the client have the knowledge to install and maintain the conservation plan? And if not, is he willing to learn?

as planned and implemented. Is it necessary for the client to obtain additional education, or hire a technical consultant, to operate and/or maintain the practice (s). Rather, does the client have the knowledge to install and maintain the conservation plan. And if not, is he willing to learn .")

20

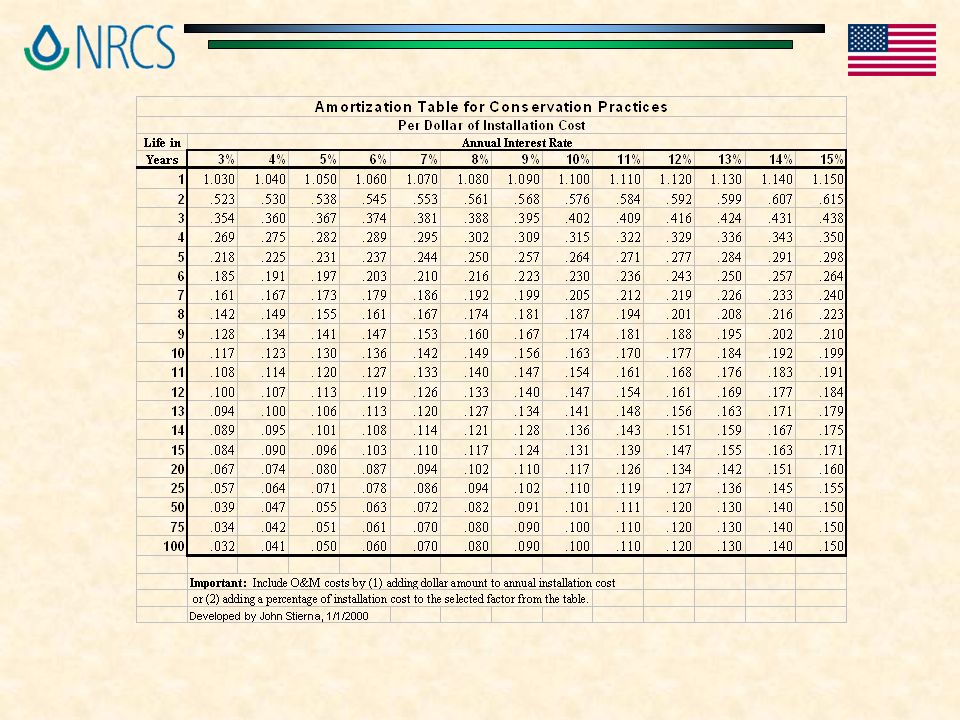

Profitability The Benefits and Costs of the Operation Often Measured in Dollars Profitable if Benefits Exceed Costs

21

Profitability Is the alternative needed and feasible? Do the benefits of improving the current operation outweigh the installation and maintenance costs (positive benefit/cost ratio)? Is there a reasonable expectation of long-term profitability/benefits for the operation if implemented? Will crop, livestock, or wildlife yield increase/decrease?

. Is there a reasonable expectation of long-term profitability/benefits for the operation if implemented. Will crop, livestock, or wildlife yield increase/decrease .")

22

Risk Adverse risk is the potential for monetary loss, physical injury, or damage to resources or the environment

23

Risk Will the proposed alternative aid/risk client participation in USDA programs? How about regulatory action? What are the possible impacts due to a change in yield? Is there flexibility in modifying the conservation plan at a future date? What issues are involved with the timing of installation and maintenance? What are the cash flow requirements of this alternative? What, if any, are the hazards involved? Rather, will the conservation plan contribute to the minimization of cash flow disruptions or debt?

24

Social Well-Being Represents the current social, cultural and economic situation of both the client and local community A combination of the previous categories of Client and Community Well Being

25

Social Well-Being What effect (both positive and negative) will the action have on the client and community with regard to: * Health and Safety * Family and community life (e.g. What will this mean for their children? Will it cause/resolve community conflict?) * Employment (e.g. Will this prevent/allow the client to keep farming, fishing, etc?) Are the proposed alternatives compatible with the client’s values? The community’s values? What is the social climate of the community in which you are working? Will the action affect community institutions, traditions or values, or the way of life for individuals in the community (what are the off-site effects)?

* Employment (e.g. Will this prevent/allow the client to keep farming, fishing, etc ) Are the proposed alternatives compatible with the client’s values. The community’s values. What is the social climate of the community in which you are working. Will the action affect community institutions, traditions or values, or the way of life for individuals in the community (what are the off-site effects) .")

26

The Planner must know the landowner and community so well that when it is time to implement the plan, it satisfies everyone’s need so exactly that incentives or regulation are not necessary.

27

NRCS Policy prohibits employees from obtaining financial information beyond what is provided voluntarily by the client. Remember: Confidential financial information is not for public use…. Always use good judgment in using information that may be of a private nature.

28

Sources of Data “CPPE Tables”, Section V, eFOTG “Practice Payment Schedules”, Cost Data, Section I, eFOTG “Projected Commodity Cost and Returns” Budgets, LSU Ag Center “Louisiana’s Master CSP Average County Cost List”, Cost Data, Section I eFOTG “National Resources Economics Handbook, Part 610, Conservation Planning”

29

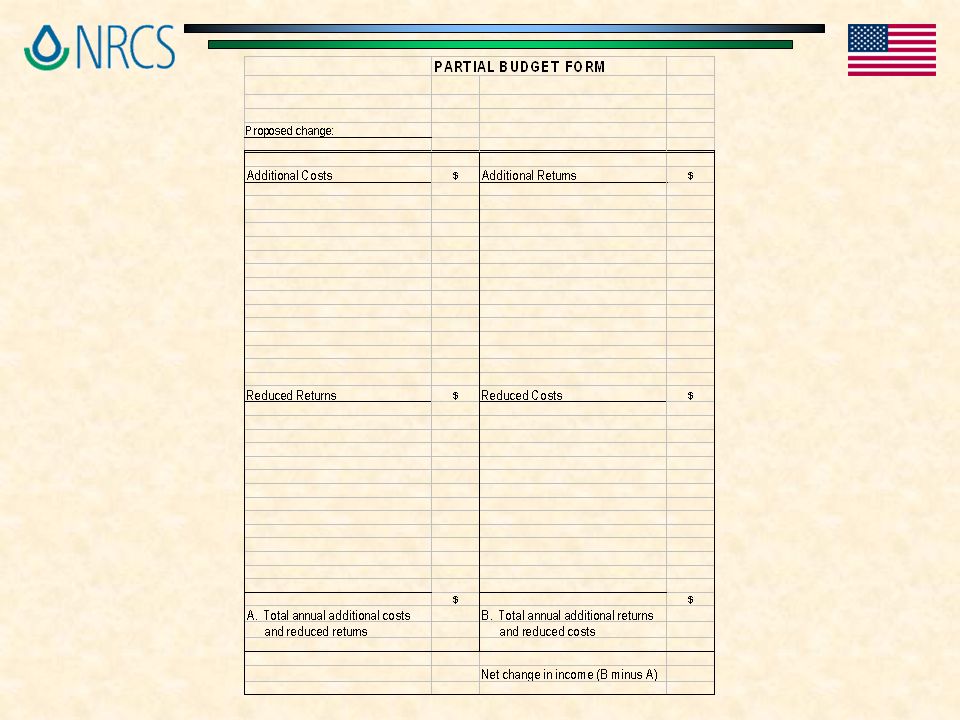

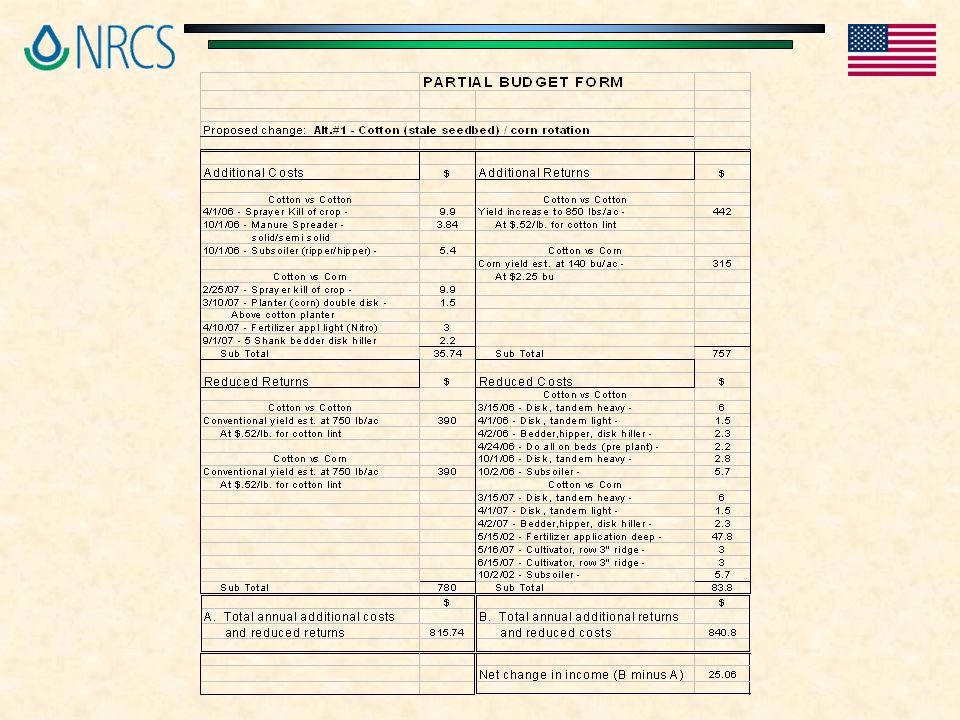

Economic Tools For Evaluating Conservation Alternatives Breakeven Analysis Cost Effectiveness Marginal Analysis Conservation Effects for Decision-making Economic threshold Partial Budget Analysis

30

Useful Economic Tools? Partial Budget Analysis

31

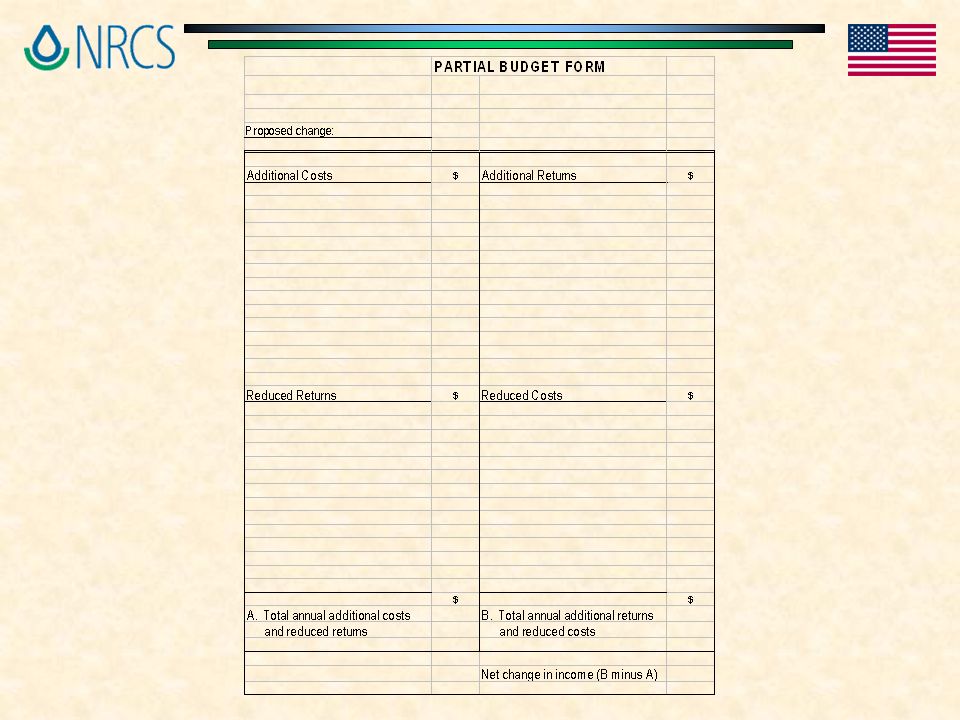

PARTIAL BUDGETING Is a technique where only the relevant changes in income and production costs are identified, listed, and used in the analysis.

32

Not a complete/whole-farm budget analysis Key words: Partial & Change

33

Analysis and computations are held to a minimum … Only those costs and returns that change as a result of the conservation practice or system are considered.

34

These changes, based upon the effects and impacts identified through the decision making process, can have four possible effects:

35

They can be: A. Income reducing effects 1.Additional costs 2.Reduced Returns B. Income increasing effects 1.Additional returns 2.Reduced costs

36

Remember, when gathering information for a partial budget: 1. Include each item of income that will be changed by the action. 2. Include each cost item that will be affected by the change. 3. Use realistic standards to evaluate your proposed change.

37

Also remember : A partial budget tells you only if a change or investment will be more profitable than the present situation to which it is compared.

40

Upon completion of the Partial Budget Analysis we have? The estimated net change in profitability from the proposed alternative. An analysis of the answer, and how it was estimated. A basis for deciding about operational and practice changes.

41

Time and Money Project feasibility can be determined using either capital values as of a common point in time, or by using the average annual of these values. NRCS uses average annual values for comparison and feasibility determination.

42

Benefits and Costs must be considered in the same time frame! So, what about one-time values such as installation costs? How do we get them into the same time frame? How do we convert them to average annual?

43

By a process called amortization Multiply the one-time value by the appropriate amortization factor. An amortization factor based upon the value/practices useful life and appropriate interest rate. Selected from NRCS compound interest and annuity tables or amortization key/card.

46

THE END Questions?

47

ENVIRONMENTAL JUSTICE

48

Environmental Justice means that, to the greatest extent practical and permitted by law, all populations are provided the opportunity to comment before decisions are rendered on proposed federal actions. Furthermore, the principles of environmental justice require that populations are allowed to share in the benefits of, are not excluded from, and are not affected in a disproportionately high and adverse manner by, government programs and activities affecting human health or the environment.

49

Executive Order 12898 issued February 11, 1994 requires each Federal Agency to make Environmental Justice a part of its mission. Agencies are to identify and address disproportionately high and adverse human health or environmental effects of its programs, policies, and activities on minority populations, low-income populations, and Indian Tribes. Environmental Justice must be applied throughout the United States, its territories and possessions, the District of Columbia, the Commonwealths of Puerto Rico and the Mariana Islands.

50

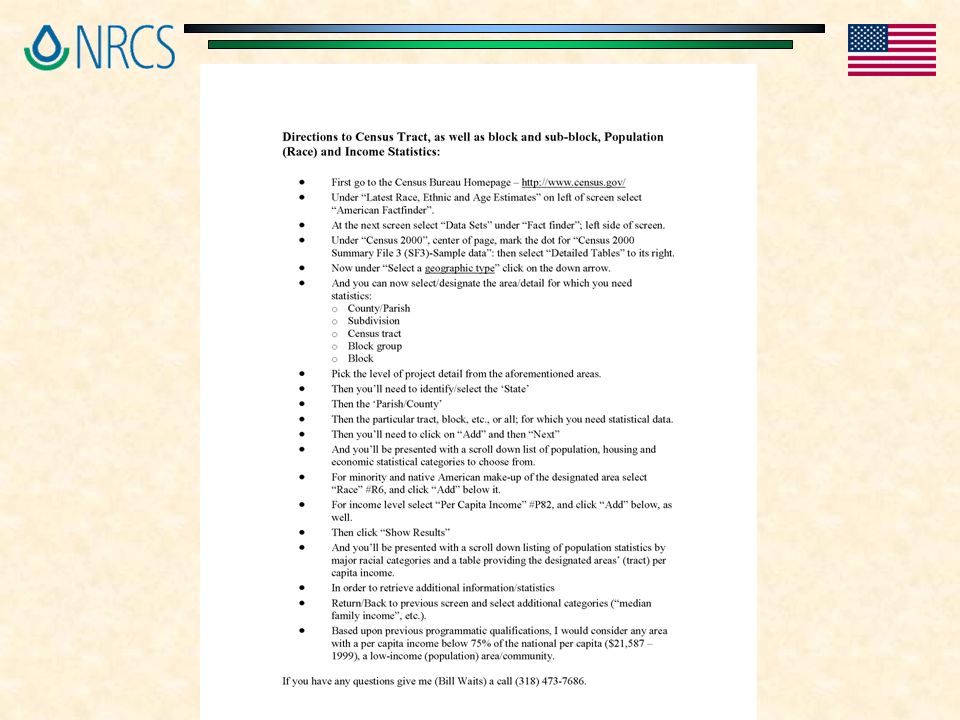

Environmental Justice issues encompass a broad range of impacts covered by NEPA, including impacts on the natural or physical environment and related social, cultural, and economic impacts. A social impact assessment can be an important way to identify environmental justice issues. The primary means to attain compliance with environmental justice considerations is through the inclusion of low-income, minority and tribal populations in the planning process and by translating documents into other languages when members of the affected area are not English- speaking.

56

THE END Any questions concerning Environmental Justice and the CPA-52?

Similar presentations

Instructor : Dr. Abed Al-Majed Nassar 2009-2010.>")