Download presentation

Presentation is loading. Please wait.

1

Financial Accounting II Lecture 04

2

Preparation and Presentation of Financial Statements Companies Ordinance 1984 (4 th and 5 th Schedule) International Accounting Standards (IAS) OR International Financial Reporting Standards (IFRS)

International Accounting Standards (IAS) OR International Financial Reporting Standards (IFRS)")

3

Companies Ordinance 1984 The Companies Ordinance 1984 is an Ordinance issued by Government of Pakistan It regulates establishment and management of Limited Companies.

4

4 th and 5 th Schedule 4 th Schedule of The Companies Ordinance 1984 provides disclosure requirement for the Listed Companies. 5 th Schedule of The Companies Ordinance 1984 provides disclosure requirement for the Non-Listed Companies.

5

4 th and 5 th Schedules of The Companies Ordinance 1984 consist of three parts: Part I – Definitions and general requirements for preparation and presentation of financial statements. Part II – Requirements for Balance Sheet. Part III – Requirements for Profit and Loss Account. 4 th and 5 th Schedule

6

International Accounting Standards International Accounting Standards (IAS) are issued by International Accounting Standard Board (IASB).

are issued by International Accounting Standard Board (IASB).")

7

International Accounting Standards Only those IAS are applicable in Pakistan that are recommended by The Institute of Chartered Accountants of Pakistan and adopted and notified by Securities and Exchange Commission of Pakistan (SECP).

.")

8

Book of Accounts to be Kept by Companies Every company shall keep at its registered office proper books of account with respect to: a)All sums of money received and expended by the company and the matters in respect of which the receipt and expenditure takes place; b)All sales and purchases of goods by the company;. c)All assets of the company:

All assets of the company:.")

9

Book of Accounts to be Kept by Companies d) All liabilities of the companies: and e) In the case of a company engaged in production, processing, manufacturing or mining activities, such particulars relating to utilisation of material or labour or to other inputs or items of cost as may be prescribed, if such class of companies is required by the Authority by a general or special order to include such particulars in the books of accounts:

All liabilities of the companies: and e) In the case of a company engaged in production, processing, manufacturing or mining activities, such particulars relating to utilisation of material or labour or to other inputs or items of cost as may be prescribed, if such class of companies is required by the Authority by a general or special order to include such particulars in the books of accounts:")

10

Annual Accounts It is the responsibility of the directors of every company to prepare annual accounts of the company.

11

Preparation of Accounts [Section 233] Directors of every company should lay before the Annual General Meeting, Balance Sheet, Profit and Loss or Income and Expenditure Account as the case may be.

![Preparation of Accounts [Section 233] Directors of every company should lay before the Annual General Meeting, Balance Sheet, Profit and Loss or Income and Expenditure Account as the case may be.](http://images.slideplayer.com/24/7514777/slides/slide_11.jpg "Preparation of Accounts [Section 233] Directors of every company should lay before the Annual General Meeting, Balance Sheet, Profit and Loss or Income and Expenditure Account as the case may be.")

12

First annual accounts of the company will be prepared within eighteen (18) months of the incorporation of the company. Preparation of Accounts [Section 233]

13

Subsequently annual accounts will be prepared every year. In addition listed companies are required to prepare Quarterly and Half Yearly accounts. Preparation of Accounts [Section 233]

14

Presentation of Balance Sheet

18

Title and Reporting Currency Name of the entity. Date on which the balance sheet is being drawn. Currency in which balance sheet is presented. Reporting period if it is less or more than one year.

19

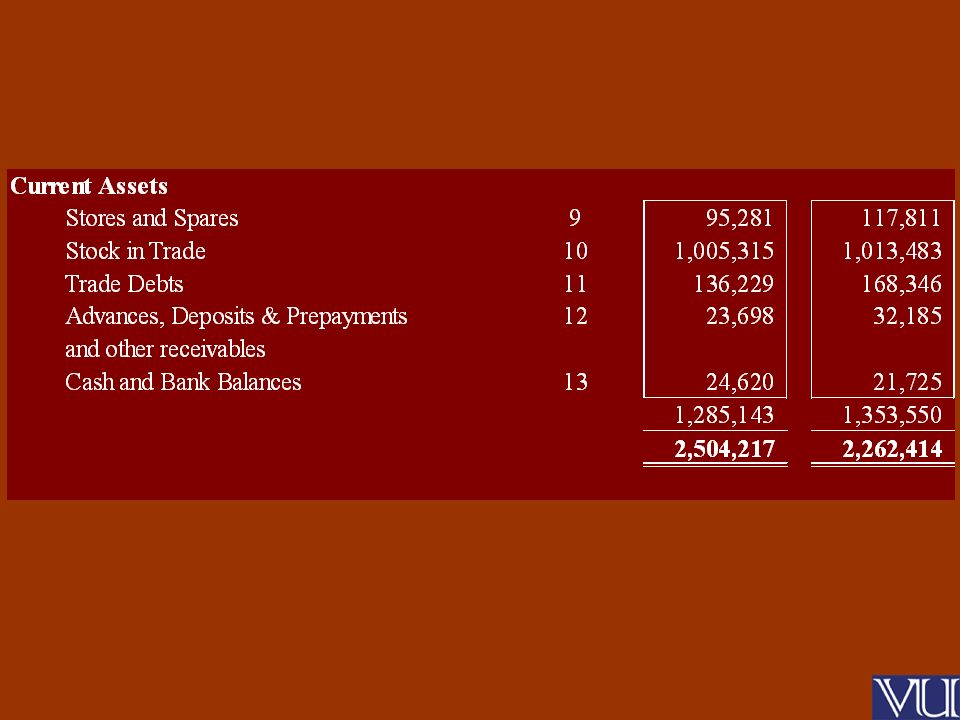

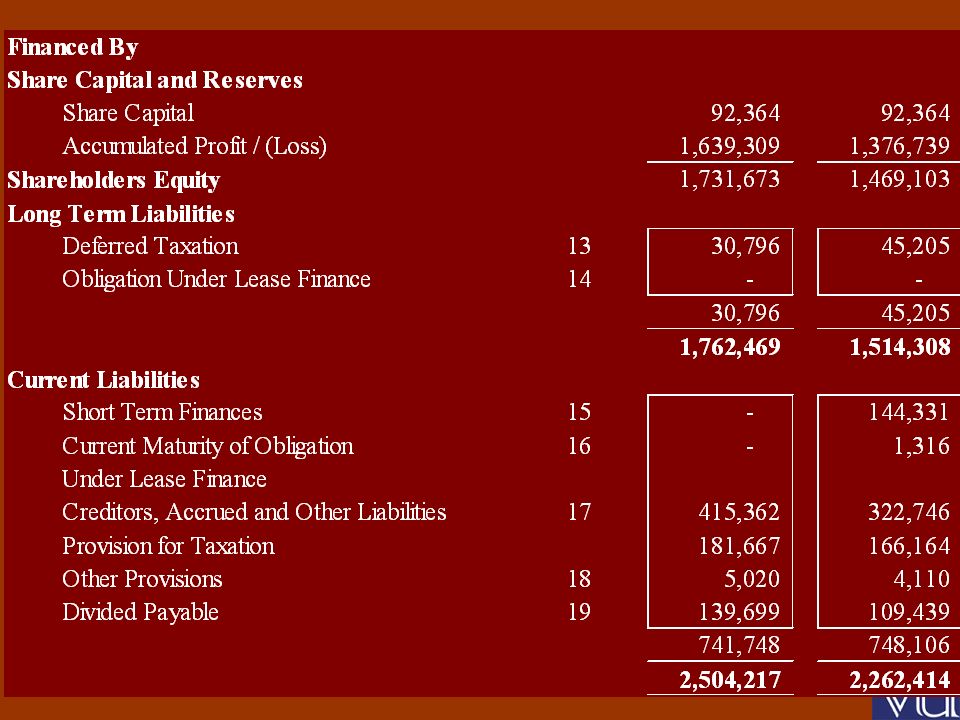

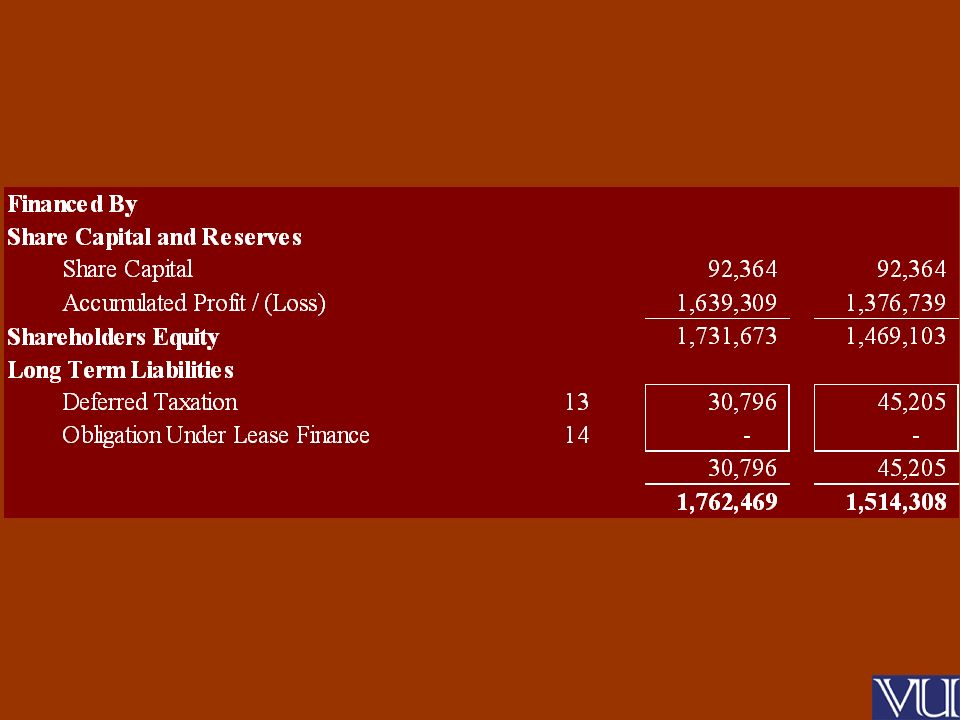

Comparative Figures Clause 6 of Part I of Fourth Schedule: Except for the first financial statements laid before the company, financial statements shall also give the corresponding figures for the immediately preceding financial year.

23

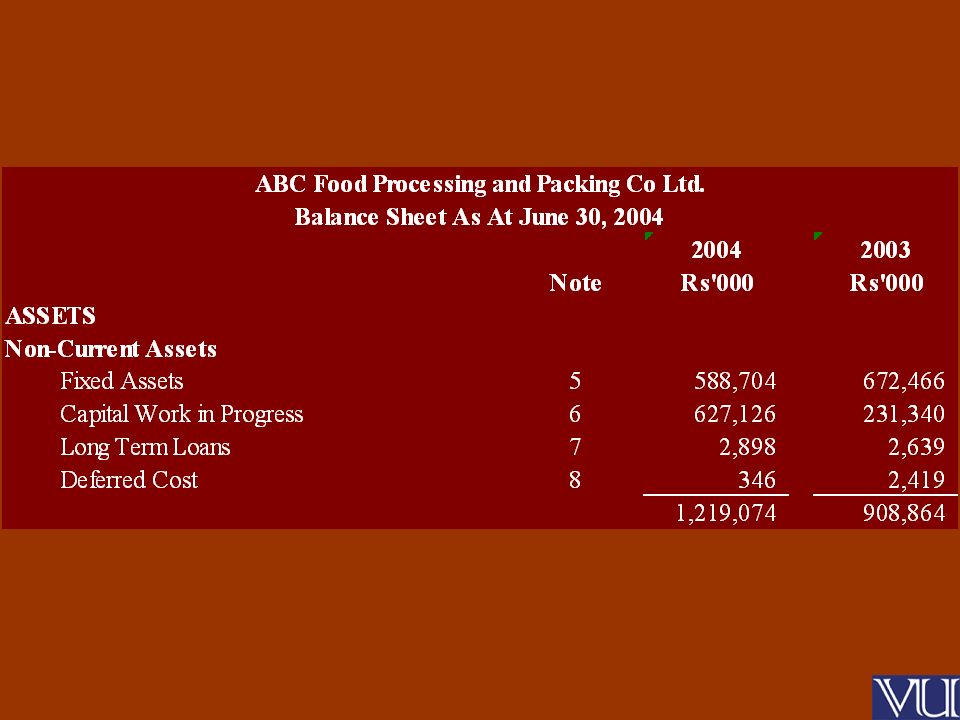

Heading for Non-Current Assets Companies OrdinanceIAS Fixed Assets Property Plant and Equipment Intangible Assets Long Term InvestmentsInvestment in Associates Long Term Loans & Advances Other Financial Assets Long-term Deposits, Prepayments and Deferred Costs

24

Fixed Assets Fixed assets (other than investments) shall be distinguished between tangible and intangible and shall be classified under appropriate sub-heads, duly itemized such as-

shall be distinguished between tangible and intangible and shall be classified under appropriate sub-heads, duly itemized such as-")

25

Fixed Assets Tangible; Land Buildings Plant and Machinery Furniture and Fittings Vehicles Capital Work in Progress Others (to be specified);

;")

26

Fixed Assets Intangible: Goodwill; Patents, Copyright, Trade Marks and Designs; and Others (to be specified).

.")

Similar presentations

>")

. WHAT IS LISTING AGREEMENT? AGREEMENT BETWEEN STOCK EXCHANGE AND THE COMPANY DESIROUS OF GETTING THEIR SECURITIES LISTED.>")

- 3 Cash Flow Statements - Pratap Karmokar (ACA)>")

>")

. Accounting: “Accounting is an art of recording, classifying, summarizing the financial transactions and interpreting.>")