Download presentation

Presentation is loading. Please wait.

1

The BI Settlement Process and Structure of Negotiated Payments Richard A. Derrig Automobile Insurers Bureau of MA Herbert I. Weisberg Correlation Research Inc. NBER Insurance Group Meeting Cambridge, Massachusetts February 6-7, 2004

4

BI Settlement Issues I IRC Studies (1977+, latest 2002 CY) IRC Studies (1977+, latest 2002 CY) AIB Studies (1986+, latest 1996 AY) AIB Studies (1986+, latest 1996 AY) Medicals Dominate Medicals Dominate Injury Types Injury Types General Damages General Damages

IRC Studies (1977+, latest 2002 CY) AIB Studies (1986+, latest 1996 AY) AIB Studies (1986+, latest 1996 AY) Medicals Dominate Medicals Dominate Injury Types Injury Types General Damages General Damages")

5

BI Settlement Issues II Investigation Investigation Suspicion of Fraud and Build-up Suspicion of Fraud and Build-up Settlement Negotiation Settlement Negotiation Low Impact Collision Low Impact Collision Passengers Passengers Bad Faith Bad Faith Evolution Over Time Evolution Over Time

6

Comparison of Disability Distributions 1989 BI Claims vs. 1996 BI Claims * Not including 14% of claims with unknown disability.

7

Total Claimed Medical Charges by Type of Service

8

Injury Type Changes Inj8996 Fracture14%5% Inpatient7%4% Serious Visible 14%2% Prior Inj. 6%27% Source: AIB Final Report (2003)

.")

9

Total Claimed Medical Charges by Type of Service

10

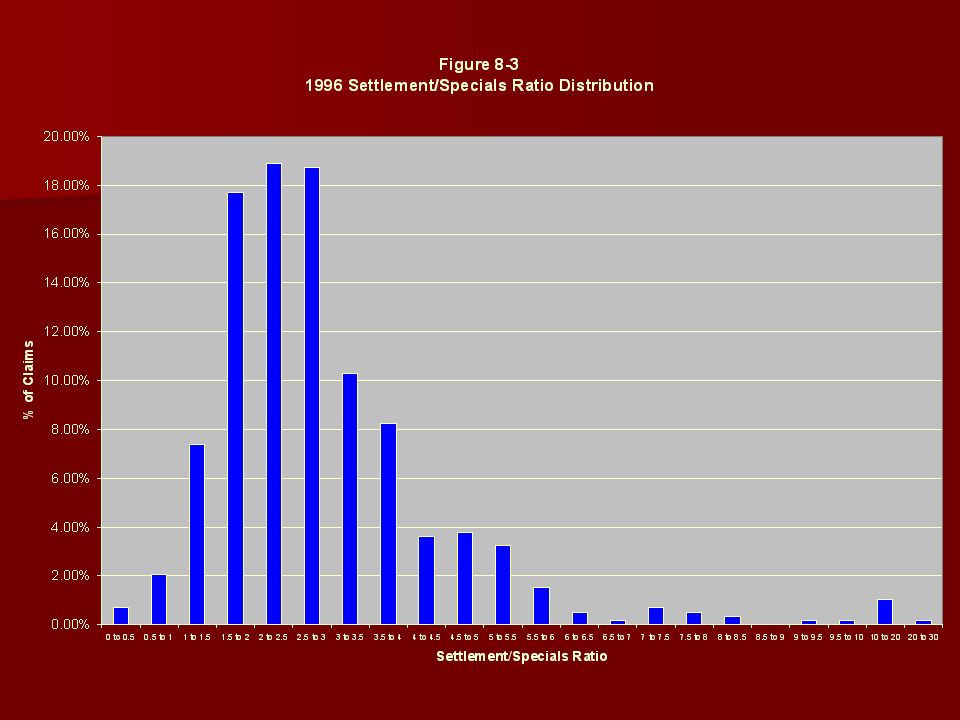

General Damages Special Damages are Claimant Economic Losses Special Damages are Claimant Economic Losses –Medical Bills –Wage Loss –Other Economic General Damages are Residual of Negotiated Settlement Less Specials General Damages are Residual of Negotiated Settlement Less Specials –“Three Times Specials” is a Myth

15

BI Negotiation Leverage Points Adjuster Advantages Adjuster has ability to go to trial Company has the settlement funds Attorney, provider, or claimant needs money Adjuster knows history of prior settlements Adjuster can delay settlement by investigation Settlement authorization process in company Initial Determination of Liability Table 1

16

BI Negotiation Leverage Points Attorney/Claimant Advantages Attorney/Claimant can build-up specials Asymmetric information (Accident, Injury, Treatment) Attorney/Claimant can fail to cooperate Attorney has experience with company Investigation costs the company money Attorney can allege unfair claim practices (93A) Adjuster under pressure to close files Table 2

Attorney/Claimant can fail to cooperate Attorney has experience with company Investigation costs the company money Attorney can allege unfair claim practices (93A) Adjuster under pressure to close files Table 2")

17

Negotiated Settlements Specials may be Discounted or Ignored Specials may be Discounted or Ignored Medicals: Real or Built-up? Medicals: Real or Built-up? Information from Investigation Information from Investigation Independent Medical Exams (IMEs) Independent Medical Exams (IMEs) Special Investigation Special Investigation Suspicion of Fraud or Build-up Suspicion of Fraud or Build-up

Independent Medical Exams (IMEs) Special Investigation Special Investigation Suspicion of Fraud or Build-up Suspicion of Fraud or Build-up.")

18

Independent Medical Exams Policy Requirement (Mass) Policy Requirement (Mass) General Claim Information plus Medical Examination General Claim Information plus Medical Examination Outcomes Outcomes –No change recommended –Refused or no show –Damages mitigated or –Treatment curtailed Cost ($350, $75 no show) Cost ($350, $75 no show)

Policy Requirement (Mass) General Claim Information plus Medical Examination General Claim Information plus Medical Examination Outcomes Outcomes –No change recommended –Refused or no show –Damages mitigated or –Treatment curtailed Cost ($350, $75 no show) Cost ($350, $75 no show)")

19

IME Savings PIP & BI PIP Sample: 1996 CSE Net Savings (PIP) -0.8% Savings from IME Requ but not Comp Savings from IME Requ but not Comp0.7% Savings from Positive IMEs Savings from Positive IMEs-0.4% Cost of Negative IMEs Cost of Negative IMEs-1.1% PIP+BI Sample: 1996 CSE Net Savings (PIP+BI) 8.7% Savings from IME Requ but not Comp* Savings from IME Requ but not Comp*4.3% Savings from Positive IMEs Savings from Positive IMEs4.9% Cost of Negative IMEs Cost of Negative IMEs-0.5% *Inclusion of All PIP claims with IME requested but not completed. 4.2% of savings for 1993 AIB comes from PIPs with no matching BIs where IME requested but not completed. 2.1% savings for 1996 DCD. 2.7% savings for 1996 CSE.

20

Net IME Savings By Suspicion Level ClaimIME Suspicion Level PaymentTypeClaimsNone(0)Low(1-3)Mod(4-6)High(7-10)ALL PIP Suspicion Score (CSE Model) PIPPIP PIP & BI matching -8.1%-2.9%3.4%-1.6%-0.8% BI Suspicion Score (NHR Model) PIP+BIBest PIP & BI matching -8.0%0.5%14.4%-4.5%6.2%

Low(1-3)Mod(4-6)High(7-10)ALL PIP Suspicion Score (CSE Model) PIPPIP PIP & BI matching -8.1%-2.9%3.4%-1.6%-0.8% BI Suspicion Score (NHR Model) PIP+BIBest PIP & BI matching -8.0%0.5%14.4%-4.5%6.2%")

21

Settlement Ratios by Injury and Suspicion Variable PIP Suspicion Score = Low (0-3) PIP Suspicion Score = Mod to High (4-10) PIP Suspicion Score = All 1996 (N-336) 1996 (N-216) 1996 (N-552) Str/SP All Other Str/SP Str/SP SettlementSettlementSettlement 81%19%94%6%86%14% Avg. Settlement/Specials Ratio 3.013.812.583.612.823.77 Median Settlement/Specials Ratio 2.692.892.402.572.552.89

22

Breakdown of Same/Different Company Claims Count Total Pay Total Med % Injuries Serious Frac All Claims 429$13,346$4,7705.8% Same Company Claims Same Company Claims118$13,246$4,9699.3% Same Co./Same Policy-Clmt Same Co./Same Policy-Clmt is Pass is Pass41$11,029$5,26914.6% Same Co./Same Policy-Clmt Same Co./Same Policy-Clmt is Pedestr is Pedestr22$17,862$5,22413.6% Same Co./Same Policy- Same Co./Same Policy- Uninsured Clm Uninsured Clm16 $ 9,416 $3,9310.0% Same Co./Different Policy Same Co./Different Policy39$14,542$4,9365.1% Different Company Claims Different Company Claims311$13,383$4,6954.5%

23

Comparison of Known Disability Claims vs. Unknown Disability Claims No. / Percent of ClaimsMean* UnknownKnownUnknownKnown Total Paid63429$16,765$13,346 Medical Settlement64429$6,387$4,546 Wage Settlement0102$0$3,578 First Demand46376$26,298$23,924 Second Demand19240$22,342$12,745 Average Weekly Wage11116$455$569 Sprain/Strain Only58%61% Primary Provider CH PT MD 14% 31% 53% 46% 22% 31% BI Suspicion Score644294.25.2 PIP Suspicion Score604052.22.9 * mean calculation of non-zero entries

24

Settlement Modeling Major Claim Characteristics Major Claim Characteristics Tobit Regression for Censored Data Tobit Regression for Censored Data (right censored for policy limits) (right censored for policy limits) Evaluation Model for Objective “Facts” Evaluation Model for Objective “Facts” Negotiation Model for all Other “Facts”, including suspicion of fraud or build-up Negotiation Model for all Other “Facts”, including suspicion of fraud or build-up

(right censored for policy limits) Evaluation Model for Objective Facts Evaluation Model for Objective Facts Negotiation Model for all Other Facts , including suspicion of fraud or build-up Negotiation Model for all Other Facts , including suspicion of fraud or build-up")

25

Evaluation Variables Prior Tobit Model (1993AY) Claimed Medicals (+) Claimed Medicals (+) Claimed Wages (+) Claimed Wages (+) Fault (+) Fault (+) Attorney (+18%) Attorney (+18%) Fracture (+82%) Fracture (+82%) Serious Visible Injury at Scene (+36%) Serious Visible Injury at Scene (+36%) Disability Weeks (+10% @ 3 weeks) Disability Weeks (+10% @ 3 weeks) New Model Additions (1996AY) Non-Emergency CT/MRI (+31%) Non-Emergency CT/MRI (+31%) Low Impact Collision (-14%) Low Impact Collision (-14%) Three Claimants in Vehicle (-12%) Three Claimants in Vehicle (-12%) Same BI + PIP Co. (-10%) [Passengers -22%] Same BI + PIP Co. (-10%) [Passengers -22%]

[Passengers -22%] Same BI + PIP Co. (-10%) [Passengers -22%].")

26

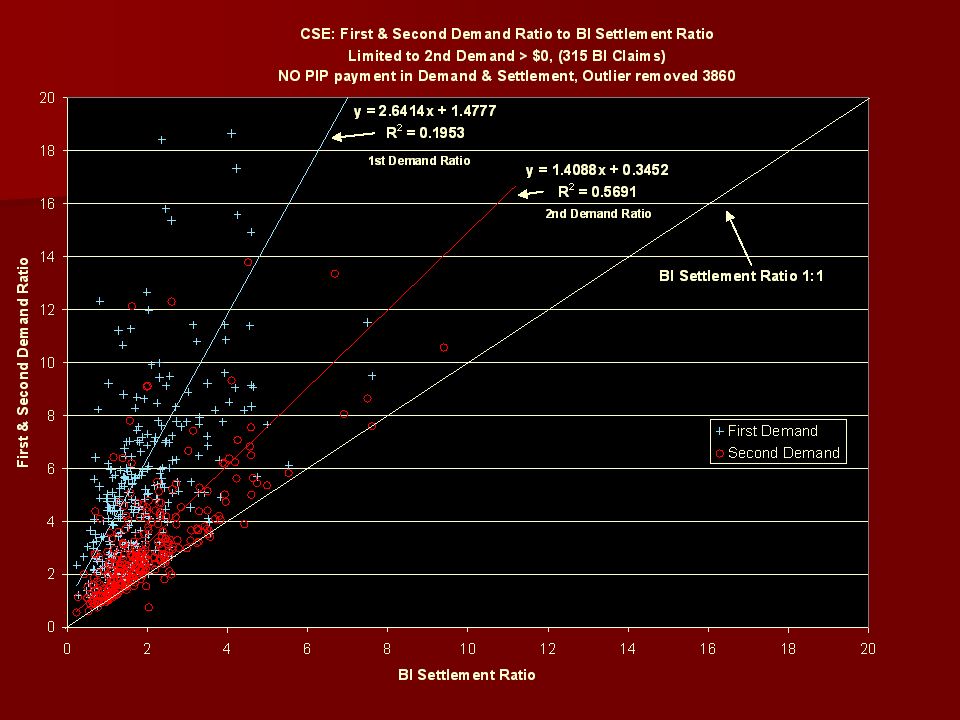

Negotiation Variables New Model Additions (1996AY) Atty (1st) Demand Ratio to Specials (+8% @ 6 X Specials) Atty (1st) Demand Ratio to Specials (+8% @ 6 X Specials) BI IME No Show (-30%) BI IME No Show (-30%) BI IME Positive Outcome (-15%) BI IME Positive Outcome (-15%) BI IME Not Requested (-14%) BI IME Not Requested (-14%) BI Ten Point Suspicion Score (-12% @ 5.0 Average) BI Ten Point Suspicion Score (-12% @ 5.0 Average) [1993 Build-up Variable (-10%)] [1993 Build-up Variable (-10%)] Unknown Disability (+53%) Unknown Disability (+53%) [93A (Bad Faith) Letter Not Significant] [93A (Bad Faith) Letter Not Significant] [In Suit Not Significant] [In Suit Not Significant] [SIU Referral (-6%) but Not Significant] [SIU Referral (-6%) but Not Significant] [EUO Not Significant] [EUO Not Significant] Note: PIP IME No Show also significantly reduces BI + PIP by discouraging BI claim altogether (-3%). discouraging BI claim altogether (-3%).

![Negotiation Variables New Model Additions (1996AY) Atty (1st) Demand Ratio to Specials 6 X Specials) Atty (1st) Demand Ratio to Specials 6 X Specials) BI IME No Show (-30%) BI IME No Show (-30%) BI IME Positive Outcome (-15%) BI IME Positive Outcome (-15%) BI IME Not Requested (-14%) BI IME Not Requested (-14%) BI Ten Point Suspicion Score 5.0 Average) BI Ten Point Suspicion Score 5.0 Average) [1993 Build-up Variable (-10%)] [1993 Build-up Variable (-10%)] Unknown Disability (+53%) Unknown Disability (+53%) [93A (Bad Faith) Letter Not Significant] [93A (Bad Faith) Letter Not Significant] [In Suit Not Significant] [In Suit Not Significant] [SIU Referral (-6%) but Not Significant] [SIU Referral (-6%) but Not Significant] [EUO Not Significant] [EUO Not Significant] Note: PIP IME No Show also significantly reduces BI + PIP by discouraging BI claim altogether (-3%).](http://images.slideplayer.com/24/7506467/slides/slide_26.jpg "discouraging BI claim altogether (-3%)..")

27

Total Value of Negotiation Variables Total Compensation Variables Avg. Claim/Factor Evaluation Variables $13,948 Disability Unknown 1.05 1 st Demand Ratio 1.09 BI IME No Show 0.99 BI IME Not Requested 0.90 BI IME Performed with Positive Outcome 0.97 Suspicion0.87 Negotiation Variables 0.87 Total Compensation Model Payment $12,058 Actual Total Compensation $11,863 Actual BI Payment $8,551

28

Actual parameters for negotiation and evaluation models, with and without suspicion variable, are shown in the hard copy handout

29

References Derrig, R.A. and H.I. Weisberg [2003], Auto Bodily Injury Claim Settlement in Massachusetts, Final Results of the Claim Screen Experiment, Massachusetts DOI 2003-15. Derrig, R.A. and H.I. Weisberg [2003], Auto Bodily Injury Claim Settlement in Massachusetts, Final Results of the Claim Screen Experiment, Massachusetts DOI 2003-15. Derrig, R.A. and H.I. Weisberg, [2003], Determinants of Total Compensation for Auto Bodily Injury Liability Under No-Fault: Investigation, Negotiation and the Suspicion of Fraud, Working paper, Automobile Insurers Bureau of MA. Derrig, R.A. and H.I. Weisberg, [2003], Determinants of Total Compensation for Auto Bodily Injury Liability Under No-Fault: Investigation, Negotiation and the Suspicion of Fraud, Working paper, Automobile Insurers Bureau of MA. Derrig, R.A., H.I. Weisberg and Xiu Chen, [1994], Behavioral Factors and Lotteries Under No-Fault with a Monetary Threshold: A Study of Massachusetts Automobile Claims, Journal of Risk and Insurance, 61:2, 245-275. Derrig, R.A., H.I. Weisberg and Xiu Chen, [1994], Behavioral Factors and Lotteries Under No-Fault with a Monetary Threshold: A Study of Massachusetts Automobile Claims, Journal of Risk and Insurance, 61:2, 245-275. Ross, Lawrence H. [1980], Settled out of Court, (Chicago, III: Aldine). Ross, Lawrence H. [1980], Settled out of Court, (Chicago, III: Aldine). Insurance Research Council [1999], Injuries in Auto Accidents, An Analysis of Auto Insurance Claims. Malvern, PA Insurance Research Council [1999], Injuries in Auto Accidents, An Analysis of Auto Insurance Claims. Malvern, PA Insurance Research Council [ 2003], Auto Injury Insurance Claims. Countrywide Patterns in Treatment, Cost, and Compensation, Malvern PA Insurance Research Council [ 2003], Auto Injury Insurance Claims. Countrywide Patterns in Treatment, Cost, and Compensation, Malvern PA Abrahamse, A. and Stephen J. Carroll [1999], The Frequency of Excess Claims for Automobile Personal Injuries, Automobile Insurance: Road Safety, New Drivers, Risks, Insurance Fraud and Regulation, Claire Laberge-Nadeau, and Georges Dionne, Eds., Kluwer Academic Publishers, 131-151. Abrahamse, A. and Stephen J. Carroll [1999], The Frequency of Excess Claims for Automobile Personal Injuries, Automobile Insurance: Road Safety, New Drivers, Risks, Insurance Fraud and Regulation, Claire Laberge-Nadeau, and Georges Dionne, Eds., Kluwer Academic Publishers, 131-151.

. Ross, Lawrence H. [1980], Settled out of Court, (Chicago, III: Aldine). Insurance Research Council [1999], Injuries in Auto Accidents, An Analysis of Auto Insurance Claims. Malvern, PA Insurance Research Council [1999], Injuries in Auto Accidents, An Analysis of Auto Insurance Claims. Malvern, PA Insurance Research Council [ 2003], Auto Injury Insurance Claims. Countrywide Patterns in Treatment, Cost, and Compensation, Malvern PA Insurance Research Council [ 2003], Auto Injury Insurance Claims. Countrywide Patterns in Treatment, Cost, and Compensation, Malvern PA Abrahamse, A. and Stephen J. Carroll [1999], The Frequency of Excess Claims for Automobile Personal Injuries, Automobile Insurance: Road Safety, New Drivers, Risks, Insurance Fraud and Regulation, Claire Laberge-Nadeau, and Georges Dionne, Eds., Kluwer Academic Publishers, Abrahamse, A. and Stephen J. Carroll [1999], The Frequency of Excess Claims for Automobile Personal Injuries, Automobile Insurance: Road Safety, New Drivers, Risks, Insurance Fraud and Regulation, Claire Laberge-Nadeau, and Georges Dionne, Eds., Kluwer Academic Publishers,")

Similar presentations

Industrial Commission (IC)>")