Download presentation

Presentation is loading. Please wait.

1

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Sarbanes-Oxley, Internal Control, and Cash Chapter 8

2

Learning Objectives 1. Describe the Sarbanes-Oxley Act of 2002 and its impact on internal controls and financial reporting. 2. Describe and illustrate the objectives and elements of internal control. 3. Describe and illustrate the application of internal controls to cash. 4. Describe the nature of a bank account and its use in controlling cash.

3

Learning Objectives (cont.) 5. Describe and illustrate the use of a bank reconciliation in controlling cash. 6. Describe the accounting for special-purpose cash funds. 7. Describe and illustrate the reporting of cash and cash equivalents in the financial statements. 8. Describe and illustrate the use of the ratio of cash to monthly cash expenses to assess the ability of a company to continue in business.

4

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Learning Objective Describe the Sarbanes-Oxley Act of 2002 and its impact on internal controls and financial reporting. 1

5

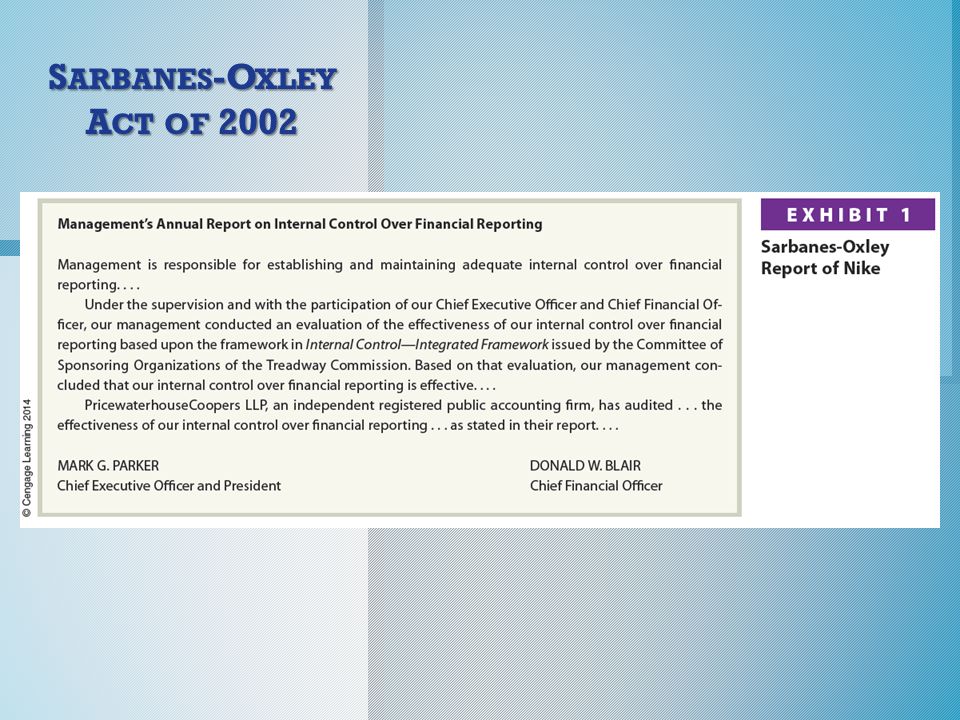

Sarbanes-Oxley Act of 2002 o The Sarbanes-Oxley Act of 2002 (often referred to simply as Sarbanes-Oxley) applies only to companies whose stock is traded on public exchanges. Its purpose is to restore public confidence and trust in the financial statements of companies.

6

Sarbanes-Oxley Act of 2002 o Sarbanes-Oxley requires companies to maintain strong and effective internal controls over the recording of transactions and the preparing of financial statements.

7

Sarbanes-Oxley Act of 2002 o Internal control is broadly defined as the procedures and processes used by a company to: Safeguard its assets. Process information accurately. Ensure compliance with laws and regulations.

8

S ARBANES -O XLEY A CT OF 2002

10

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Learning Objective Describe and illustrate the objectives and elements of internal control. 2

11

Internal Control

12

o Employee fraud is the intentional act of deceiving an employer for personal gain.

13

Elements of Internal Control o Management is responsible for designing and applying five elements of internal control to meet the three internal control objectives. These elements are as follows: Control environment Risk assessment Control procedures Monitoring Information and communication

14

Elements of Internal Control

15

Control Environment o The control environment is the overall attitude of management and employees about the importance of controls. Three factors influencing a company’s control environment are as follows: Management’s philosophy and operating style The company’s organizational structure The company’s personnel policies

16

Control Environment

17

Control Procedures o Control procedures provide reasonable assurance that business goals will be achieved. Control procedures include the following: Competent personnel, rotating duties, and mandatory vacations Separating responsibilities for related operations Separating operations, custody of assets, and accounting Proofs and security measures

18

Control Procedures

19

Monitoring o Monitoring the internal control system is used to locate weaknesses and improve controls.

20

Monitoring o Monitoring often includes observing employee behavior and the accounting system for indicators of control problems.

21

Monitoring

22

Monitoring

23

Limitations of Internal Control o Internal controls can provide only reasonable assurance for safeguarding assets, processing accurate information, and compliance with laws and regulations. This is due to the following factors: The human element of controls Cost-benefit considerations

24

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Learning Objective Describe and illustrate the application of internal controls to cash. 3

25

Cash Controls Over Receipts and Payments o Cash includes coins, currency (paper money), checks, and money orders. Money on deposit with a bank or other financial institution that is available for withdrawal is also considered cash. Cash is the asset most likely to be stolen or used improperly in a business.

26

Control of Cash Receipts o Businesses normally receive cash from two main sources: Customers purchasing products or services Customers making payments on account

27

Cash Received from Cash Sales o One of the most important controls to protect cash received in over-the-counter sales is a cash register.

28

C ASH R ECEIVED FROM C ASH S ALES

29

Control of Cash Receipts o A predetermined amount of money that is given to each cash register clerk in a cash drawer is called a change fund.

30

Control of Cash Receipts o Salespersons may make errors in making change for customers or in ringing up cash sales. As a result, the amount of cash on hand may differ from the amount of cash sales. Such differences are recorded in a cash short and over account.

31

Cash Received from Cash Sales o Cash sales for May 3 totaled $35,690 per the cash register tape. After removing the change fund, only $35,668 was left in the cash drawer. The cash sales and shortage would be recorded as follows:

32

Cash Received from Cash Sales o If there had been cash over, Cash Short and Over would have been credited for the overage.

33

Cash Received in the Mail o Cash is received in the mail when customers pay their bills. Most companies design their invoices so that customers return a portion of the invoice, called a remittance advice, with their payment.

34

Cash Received by EFT o Cash may also be received from customers through electronic funds transfers (EFT). Customers may authorize automatic electronic transfers from their checking accounts to pay monthly bills.

35

Cash Received by EFT o Companies encourage customers to use EFT for the following reasons: EFTs cost less than receiving cash payments through the mail. EFTs enhance internal controls over cash since the cash is received directly by the bank without any employees handling cash. EFTs reduce late payments from customers and speed up the processing of cash receipts.

36

Control of Cash Payments o The control of cash payments should provide reasonable assurance that: Payments are made for only authorized transactions. Cash is used effectively and efficiently.

37

Voucher System o A voucher system is a set of procedures for authorizing and recording liabilities and cash payments. It may be either manual or computerized.

38

Voucher System o A voucher is any document that serves as proof of authority to pay cash or issue an electronic funds transfer.

39

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Learning Objective Describe the nature of a bank account and its use in controlling cash. 4

40

Bank Accounts o A major reason that businesses use bank accounts is for internal control. Some of the control advantages of using bank accounts are as follows: Bank accounts reduce the amount of cash on hand. Bank accounts provide an independent recording of cash transactions. Use of bank accounts facilitates the transfer of funds using EFT systems.

41

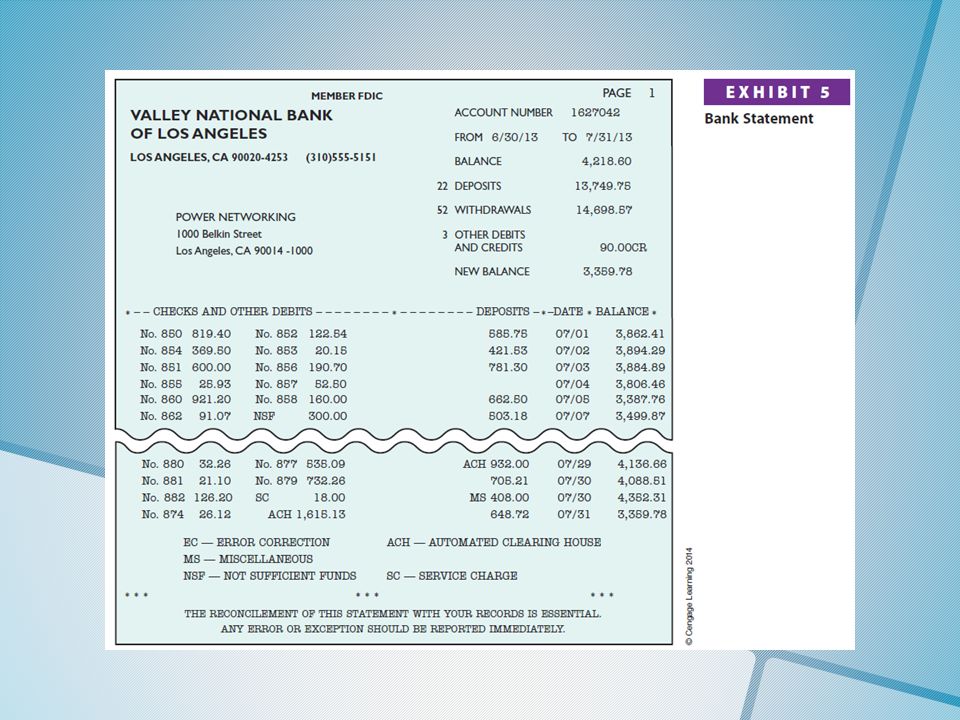

Bank Statement o A summary received from the bank (usually monthly) of all checking account transactions is called a bank statement. It shows the beginning balance, additions, deductions, and the ending balance.

43

Impact of Debit and Credit Memos

44

Bank Statement o The following types of credit or debit memo entries are found on a bank statement:

45

Using the Bank Statement as a Control Over Cash

46

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Learning Objective Describe and illustrate the use of a bank reconciliation in controlling cash. 5

47

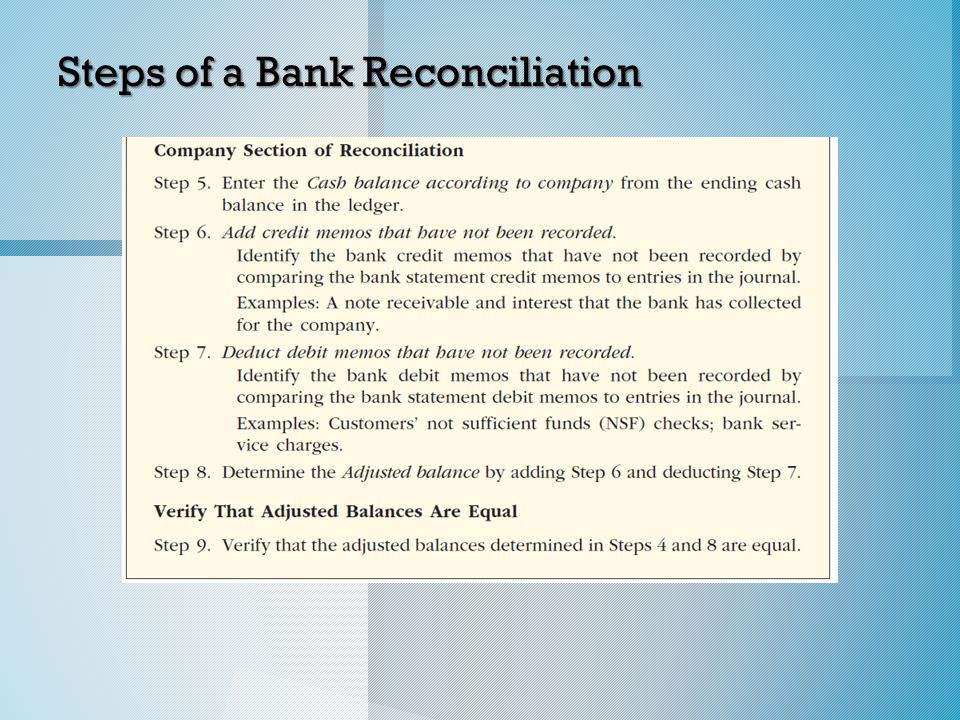

Bank Reconciliation o A bank reconciliation is an analysis of the items and amounts that cause the cash balance reported in the bank statement to differ from the balance of the cash account in the ledger. This is used to determine the adjusted cash balance.

48

Bank Reconciliation o A bank reconciliation is usually divided into two sections as follows: The bank section begins with the cash balance according to the bank statement and ends with the adjusted balance. The company section begins with the cash balance according to the company’s records and ends with the adjusted balance.

49

Bank Reconciliation

50

Steps of a Bank Reconciliation

52

Step 1 Power Networking Bank Reconciliation o Power Networking prepares to reconcile the monthly bank statement as of July 31. The bank statement shows an ending cash balance of $3,359.78.

53

Bank’s Records Cash balance $3,359.78 Power Networking’s Records Step 1 Power Networking Bank Reconciliation

54

Step 2 Power Networking Bank Reconciliation o A deposit on July 31 of $816.20 is not recorded on the bank statement.

55

Bank’s Records Power Networking’s Records Cash balance$3,359.78 Add deposit not recorded by bank 816.20 $4,175.98 Step 2 Power Networking Bank Reconciliation

56

Step 3 Power Networking Bank Reconciliation o Three checks that were written during the month did not appear on the bank statement: No. 812, $1,061; No. 878, $435.39, No. 883, $48.60.

57

Bank’s Records Power Networking’s Records Step 3 Add deposit not recorded by bank 816.20 $4,175.98 Cash balance$3,359.78 Deduct outstanding checks: No. 812$1,061.00 No. 878435.39 No. 883 48.60 1,544.99 Power Networking Bank Reconciliation

58

Add deposit not recorded by bank 816.20 $4,175.98 Bank’s Records Power Networking’s Records Cash balance$3,359.78 Deduct outstanding checks: No. 812$1,061.00 No. 878435.39 No. 883 48.60 1,544.99 $2,630.99 Adjusted balance Step 4 Power Networking Bank Reconciliation

59

Step 5 Power Networking Bank Reconciliation o The cash balance in Power Networking’s ledger on July 31 is $2,549.99.

60

Add deposit not recorded by bank 816.20 $4,175.98 Bank’s Records Power Networking’s Records Cash balance$3,359.78 Deduct outstanding checks: No. 812$1,061.00 No. 878435.39 No. 883 48.60 1,544.99 Step 5 Cash balance$2,549.99 $2,630.99 Adjusted balance Power Networking Bank Reconciliation

61

Step 6 Power Networking Bank Reconciliation o A credit memo on the bank statement indicates that the bank collected a note in the amount of $400 and the related interest of $8 for Power Networking.

62

Add deposit not recorded by bank 816.20 Cash balance$3,359.78 $4,175.98 Bank’s Records Power Networking’s Records Cash balance$2,549.99 Deduct outstanding checks: No. 812$1,061.00 No. 878435.39 No. 883 48.60 1,544.99 Add note and interest collected by bank 408.00 $2,957.99 Step 6 $2,630.99 Adjusted balance Power Networking Bank Reconciliation

63

Step 7 Power Networking Bank Reconciliation o A check from a customer (Thomas Ivey) for $300 was returned by the bank because of insufficient funds (NSF) as indicated by a debit memo. A bank service charge of $18 was also indicated by a debit memo.

64

Add deposit not recorded by bank 816.20 $4,175.98 Bank’s Records Power Networking’s Records Cash balance$3,359.78 Cash balance$2,549.99 Deduct outstanding checks: No. 812$1,061.00 No. 878435.39 No. 883 48.60 1,544.99 Add note and interest collected by bank 408.00 $2,957.99 $2,630.99 Adjusted balance Deduct NSF check$300.00 Bank service charges18.00 Step 7 Power Networking Bank Reconciliation

65

Error Power Networking Bank Reconciliation o Check No. 879 for $732.26 to Taylor Company on account was erroneously recorded in the journal as $723.26. When an error is made, two questions are asked: (1) Who made the error? (2) Does correcting the error cause the cash account to go up or down? o Power Networking made the error, so the item is placed on the company’s side of the reconciliation. By correcting the error, the cash account goes down. (Thus, it is a deduction on the reconciliation.)

Who made the error. (2) Does correcting the error cause the cash account to go up or down. o Power Networking made the error, so the item is placed on the company’s side of the reconciliation. By correcting the error, the cash account goes down. (Thus, it is a deduction on the reconciliation.).")

66

Add deposit not recorded by bank 816.20 $4,175.98 Bank’s Records Power Networking’s Records Cash balance$3,359.78 Cash balance$2,549.99 Deduct outstanding checks: No. 812$1,061.00 No. 878435.39 No. 883 48.60 1,544.99 Add note and interest collected by bank 408.00 $2,957.99 Deduct check NSF$300.00 Bank service charges18.00 $2,630.99 Adjusted balance Error Error recording Chk. No. 879 9.00 Power Networking Bank Reconciliation

67

Add deposit not recorded by bank 816.20 $4,175.98 Bank’s Records Power Networking’s Records Cash balance$3,359.78 Cash balance$2,549.99 Deduct outstanding checks: No. 812$1,061.00 No. 878435.39 No. 883 48.60 1,544.99 Add note and interest collected by bank 408.00 $2,957.99 Deduct check NSF$300.00 Bank service charges18.00 $2,630.99 Adjusted balance Error recording Chk. No. 879 9.00327.00 $2,630.99 Adjusted balance Step 8 Power Networking Bank Reconciliation

68

Bank’s Records Power Networking’s Records Add deposit not recorded by bank 816.20 $4,175.98 Cash balance$3,359.78 Cash balance$2,549.99 Deduct outstanding checks: No. 812$1,061.00 No. 878435.39 No. 883 48.60 1,544.99 Add note and interest collected by bank 408.00 $2,957.99 Deduct check NSF$300.00 Bank service charges18.00 $2,630.99 Adjusted balance $2,630.99 Adjusted balance Step 9 Error recording Chk. No. 879 9.00327.00 Power Networking Bank Reconciliation

69

o The journal entries for Power Networking, based on the bank reconciliation, are as follows:

70

Power Networking Bank Reconciliation

71

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Learning Objective Describe the accounting for special-purpose cash funds. 6

72

Petty Cash Fund o It is usually not practical for a business to write checks to pay small amounts. Thus, it is desirable to control such payments by using a special cash fund, called a petty cash fund.

73

Petty Cash Fund o A petty cash fund of $500 is established on August 1. The entry to record the transaction is as follows:

74

IMPORTANT! Petty Cash Fund o The only time Petty Cash is debited is when the fund is initially established or when the fund is increased. The only time Petty Cash is credited is when the fund is being decreased.

75

Petty Cash Fund o At the end of August, the petty cash receipts indicate expenditures for the following items: o The entry to replenish the petty cash fund is shown below.

76

Special-Purpose Funds o Companies often use other cash funds for special needs, such as payroll or travel expenses. Such funds are called special- purpose funds.

77

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Learning Objective Describe and illustrate the reporting of cash and cash equivalents in the financial statements. 7

78

Financial Statement Reporting of Cash o A company’s excess cash is normally invested in highly liquid investments. These investments are called cash equivalents.

79

Financial Statement Reporting of Cash o Companies that have invested excess cash in cash equivalents usually report Cash and cash equivalents as one amount on the balance sheet.

80

Financial Statement Reporting of Cash o Banks may require depositors to maintain minimum cash balances in their bank accounts. Such a balance is called a compensating balance.

81

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Learning Objective Describe and illustrate the use of the ratio of cash to monthly cash expenses to assess the ability of a company to continue in business. 8

82

Ratio of Cash to Monthly Cash Expenses o A cash ratio that is especially useful for startup companies or companies in financial distress is the ratio of cash to monthly cash expenses. The ratio is computed as shown below: Ratio of Cash to Monthly Cash Expenses = Cash as of Year-End Monthly Cash Expenses

83

Ratio of Cash to Monthly Cash Expenses o The cash, including any cash equivalents, is taken from the balance sheet as of year-end. The monthly cash expenses, sometimes called cash burn, are estimated from the operating activities section of the statement of cash flows as follows: Monthly Cash Expenses = Negative Cash Flow from Operations 12

84

c. 2014 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, or posted to a publicly accessible website, in whole or in part. Sarbanes-Oxley, Internal Control, and Cash The End

Similar presentations

applies only to companies whose stock is traded on public exchanges. Its purpose.>")