Download presentation

Presentation is loading. Please wait.

1

2012 LOST Presentation May 21, 2012

2

To provide property tax rollback equal to the distribution of the LOST O.C.G.A. §48-8-91 Is the Condition Precedent for the existence of the tax May be expended to fund services Eaves Consulting Group L.L.C.2

3

Shall analyze local service delivery responsibilities Examine the existing allocation of resources Make rational the allocation of those resources POPULATION IS NOT ALWAYS IN DIRECT CORRELATION TO SERVICES O.C.G.A. §48-8-89 (D)(1) Eaves Consulting Group L.L.C.3

(1) Eaves Consulting Group L.L.C.3.")

4

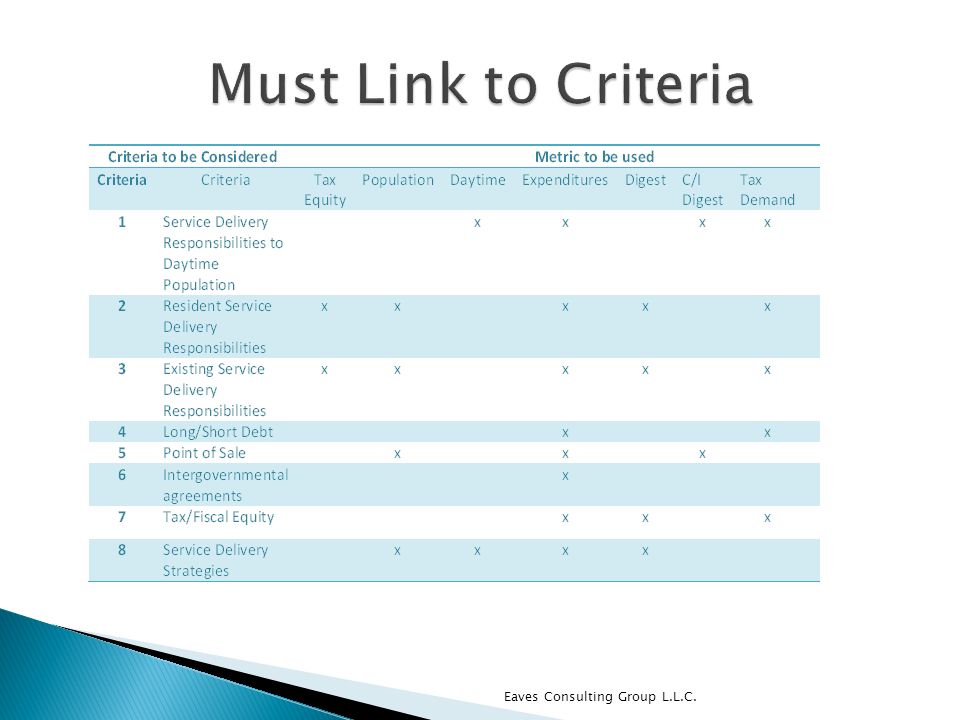

The sub-divisions shall at a minimum consider the criteria specified in subsection (b) of this Code section. §48-8-89 (d)(1) 1. Service Delivery Responsibility to daytime population 2. Service Delivery Responsibilities to resident population 3. Existing Service Delivery Responsibilities 4. Impact on Short and Long term debt 5. Point of Sale 6. Intergovernmental Agreements 7. Tax and Fiscal Equity 8. Service Delivery Agreements Eaves Consulting Group L.L.C.

(1) 1. Service Delivery Responsibility to daytime population 2. Service Delivery Responsibilities to resident population 3. Existing Service Delivery Responsibilities 4. Impact on Short and Long term debt 5. Point of Sale 6. Intergovernmental Agreements 7. Tax and Fiscal Equity 8. Service Delivery Agreements Eaves Consulting Group L.L.C..")

5

How to consider How to measure How to weight the criteria- Not all equal In mediation/arbitration both sides must be able to show that they did consider all of the criteria, how they measured, and make rational the linkage Eaves Consulting Group L.L.C.

6

Needs to be mutually exclusive Residential Service Population Daytime Service Population General Fund Expenditures Tax Digest Commercial/Industrial Digest Taxes Levied Tax Equity Eaves Consulting Group L.L.C.

8

the county whose geographical boundary is conterminous with that of the special district and each qualified municipality therein receiving any proceeds of the tax shall adjust annually the millage rate for ad valorem taxation of tangible property within such political subdivisions as provided in this subsection. O.C.G.A. §48-8-91 (a) See Martin v. Ellis 242 GA 340 for county wide roll-backs (Un-equal roll-backs disallowed) Eaves Consulting Group L.L.C.8

See Martin v. Ellis 242 GA 340 for county wide roll-backs (Un-equal roll-backs disallowed) Eaves Consulting Group L.L.C.8.")

9

O.C.G.A. § 48-8-81. Creation of special districts Pursuant to the authority granted by Article IX, Section II, Paragraph VI of the Constitution of this state, there are created within this state 159 special districts. The geographical boundary of each county shall correspond with and shall be conterminous with the geographical boundary of one of the 159 special districts.Article IX, Section II, Paragraph VI of the Constitution There is also case law on this point in Nielubowicz v. Chatham County 252 GA 330 Eaves Consulting Group L.L.C.

10

Service Delivery Responsibilities to Daytime population Daytime Population and General Fund Expenditures Eaves Consulting Group L.L.C.10

11

Service Delivery Responsibilities to Residential Population Residential Service Population and General Fund Expenditures Eaves Consulting Group L.L.C.11

12

Uniformity and Equity RSP validated by equal impact Eaves Consulting Group L.L.C.12

13

Existing Service Delivery Responsibilities General Fund Expenditures Eaves Consulting Group L.L.C.13

14

Total Tax Demand to pay for Services Eaves Consulting Group L.L.C.14

15

Cost to service infrastructure Measured by Total Digest Share Eaves Consulting Group L.L.C.15

16

Impact on Short and Long term debt Used General Fund expenditures including annual debt service Do not consider debt tied to revenues bonds or enterprise funds Eaves Consulting Group L.L.C.16

17

Point of Sale Sales measured at County Level by Department of Revenue No independent, verifiable accurate information for POS at municipal level Not mutually exclusive every sale in city also in county How to consider? Eaves Consulting Group L.L.C.17

18

Commercial/Industrial Digest Cost of Community Services for Commercial and Industrial services cost.40 for every dollar of revenue Revenue producer for Municipalities Eaves Consulting Group L.L.C.18

19

Sales Tax is a transaction tax on the consumer not the collector Benefit accrues to the taxpayer not collector How not to measure- ◦ Self reported economic surveys ◦ Zip Codes do not follow municipal boundaries ◦ Data that uses estimates and administrative records ◦ Non Mutually Exclusive Data Eaves Consulting Group L.L.C.19

20

Eaves Consulting Group L.L.C.20

21

Gives County credit for Unincorporated only County sub-division is entire area Reflects accurate Service Delivery Responsibilities Mutually Exclusive Data Data still based on estimates from 2007 Brunswick Calculation County Calculation Eaves Consulting Group L.L.C.21

22

County funds Economic Development $800,000 from General Fund Two new restaurants opening in Brunswick ◦ Olive Garden ◦ Red Lobster Pinova expansion King and Prince Seafood expansion County is building point of sales and city digest value Eaves Consulting Group L.L.C.22

23

Intergovernmental Agreements ◦ Needed to Cover “Supplemental Powers” ◦ None that currently affect LOST distribution Tax Collection for City Sidney Lanier Bridge Lights Animal control center Tourism Eaves Consulting Group L.L.C.23

24

Fiscal Equity- ◦ Do Municipal taxpayers pay for any Countywide services? None Identified ◦ Do Unincorporated taxpayers pay for any municipal services? Identified two Fiscal Equity issue that need to be addressed Eaves Consulting Group L.L.C.24

25

Library- Supplemental Power under Constitution Ga. Const. Art. IX, § II, Para. III(10) SDS states service is countywide and paid jointly by City and County County pays $275,000 City pays -0- City Share should be $53,000 based on population percent .30 credit to LOST Formula Eaves Consulting Group L.L.C.25

SDS states service is countywide and paid jointly by City and County County pays $275,000 City pays -0- City Share should be $53,000 based on population percent .30 credit to LOST Formula Eaves Consulting Group L.L.C.25.")

26

Traffic Control Devices- Supplemental Power under Constitution Ga. Const. Art. IX, § II, Para. III(4) SDS states service in incorporated area will be provided by Brunswick County provides maintenance ◦ County residents paying for Municipal Services Eaves Consulting Group L.L.C.26

SDS states service in incorporated area will be provided by Brunswick County provides maintenance ◦ County residents paying for Municipal Services Eaves Consulting Group L.L.C.26.")

27

Does the unincorporated taxpayer pay for all services delivered “exclusively” in the unincorporated area? ◦ Unincorporated Expenditures=$5,497,531 ◦ Unincorporated Revenues= $5,801,008 No Tax Equity Issue Identified In fact, Fiscal Equity Issue- Unincorporated Revenues paying for Countywide Services Eaves Consulting Group L.L.C.27

28

Existing Service Delivery Strategies ◦ Negotiated in Good Faith in 1999 ◦ Amended in 2008 ◦ No overlap or duplication of services ◦ No Double Taxation issues Consider impact of changes since last LOST Negotiations ◦ City stopped funding library services.3% Credit Offset ◦ City stopped funding Development Authority.87% Credit Offset Eaves Consulting Group L.L.C.28

29

If any differential county services exist the remedy is in the Service Delivery law: ◦ Special Taxing District ◦ Rollback on county tax millage for incorporated area ◦ Re-designation of unincorporated revenue The remedy is not to give municipalities more LOST revenue for city services Eaves Consulting Group L.L.C.29

30

Eaves Consulting Group L.L.C.30

31

Property Tax Relief- Dollar for Dollar rollback ◦ Benefits fair and balanced ◦ Equal benefit for all taxpayers under the law ◦ Uniformity Primary reason Glynn County and Brunswick needs to change current distribution formula Eaves Consulting Group L.L.C.31

32

Current Distribution- Need to equalize Eaves Consulting Group L.L.C.32

33

Eaves Consulting Group L.L.C.33 Two: One ratio is fair. It covers differential service paid for by two digest- Three: One distribution ratio is inherently unfair

34

Considering all Criteria Using available measurements County Position Eaves Consulting Group L.L.C.34

Similar presentations