Download presentation

Presentation is loading. Please wait.

1

Political Winds, Financing Constraints and Pharmaceutical Innovation Joshua Linn (UIC) and Robert Kaestner (UIC and NBER) November 9, 2007 Presentation for the DIME Workshop on Finance, Innovation and Inequality

and Robert Kaestner (UIC and NBER) November 9, 2007 Presentation for the DIME Workshop on Finance, Innovation and Inequality")

2

Public Policy and Pharmaceutical Prices Recent policy debates in the US –Price controls, Canadian imports –Medicare Part D –Should the government negotiate prices? –Common theme: prices are too high What are the welfare effects? –Static effect on consumer surplus (holding fixed available drugs) –Dynamic effect (innovation) –Tradeoff between consumer surplus today and tomorrow

–Dynamic effect (innovation) –Tradeoff between consumer surplus today and tomorrow.")

3

Profits, Policy and Pharmaceutical Innovation Recent empirical evidence that innovation responds to profit opportunities –Acemoglu and Linn (2004), Finkelstein (2004) and Qian (2007) –Relative profit opportunities (potential market size, regulation or patent protection) drive innovation Prices should create similar incentives –The evidence suggests a large effect, but it is difficult to calculate directly –Magnitude is important for policy questions

, Finkelstein (2004) and Qian (2007) –Relative profit opportunities (potential market size, regulation or patent protection) drive innovation Prices should create similar incentives –The evidence suggests a large effect, but it is difficult to calculate directly –Magnitude is important for policy questions")

4

Empirical Evidence on Prices and Innovation Separately estimate different stages from prices to innovation –Prices → R&D → new drugs → consumer surplus –Golec and Vernon (2005), Lichtenberg (2002) –Alternative: structural model of supply and demand Conclusion –Hughes, Moore and Snyder (2002) and Santerre and Vernon (2006) –Dynamic effect is much larger Difficulties –Estimates combined from many studies –Identification –Interpretation

, Lichtenberg (2002) –Alternative: structural model of supply and demand Conclusion –Hughes, Moore and Snyder (2002) and Santerre and Vernon (2006) –Dynamic effect is much larger Difficulties –Estimates combined from many studies –Identification –Interpretation")

5

Existing Empirical Evidence Identification usually relies on time series or cross- country evidence –Correlation between prices and R&D –Variables move slowly over time –Other differences between countries? What causes the relationship between prices and R&D? –Expected profitability or financing constraints? (Scherer, 2001) –Are current prices correlated with future prices? –Does an increase in prices allow firms to invest more in developing new drugs? Different policy implications for raising drug prices in countries with less developed financial markets

–Are current prices correlated with future prices. –Does an increase in prices allow firms to invest more in developing new drugs. Different policy implications for raising drug prices in countries with less developed financial markets.")

6

Open Questions How do pharmaceutical prices affect innovation? –Would price regulation affect the types of new drugs? –How does the dynamic effect compare with static effect? –Expected prices vs. financing constraints Our approach –Focus on firms’ asset values –A firm’s assets include marketed and pre-market drugs –How does a price decrease affect the values of both types of assets? –How strong is the effect of prices on profit incentives? –Separate financing constraints from other effects

7

Policy Context Medicare Prescription Drug, Improvement, and Modernization Act (MMA) passes in 2003 –Subsidizes prescription drug insurance for the elderly –Passes narrowly (in House) after many years of debate, and along party lines Should the government negotiate prices? –Rangel-Dingell Amendment would have required government to negotiate prices –Amendment would have resulted in lower prescription drug prices, but fails Midterm election (2006) –Before election, Democratic position was well known –Democratic victory was unexpected (Iowa Electronic Market) –Large change in expected drug prices

–Before election, Democratic position was well known –Democratic victory was unexpected (Iowa Electronic Market) –Large change in expected drug prices.")

8

A Closer Look at Financing Constraints Evidence from the pharmaceutical industry –External cost of capital is greater than the internal cost –Lerner, Shane and Tsai (2003) and Metrick and Nicholson (2006) Value of a project depends on expected price and available cash –Asymmetric information or agency problems create wedge –Invest available cash and external funds –The firm is constrained, so an increase in cash raises investment Two effects of a price decrease on the value of a pre- market drug –Cost of marketing the drug is higher if less cash is available –Potential revenue from the drug also decreases if expected output price is lower

and Metrick and Nicholson (2006) Value of a project depends on expected price and available cash –Asymmetric information or agency problems create wedge –Invest available cash and external funds –The firm is constrained, so an increase in cash raises investment Two effects of a price decrease on the value of a pre- market drug –Cost of marketing the drug is higher if less cash is available –Potential revenue from the drug also decreases if expected output price is lower")

9

Empirical Strategy Election causes a discrete change in asset values –Age profile varies widely across therapeutic categories (antibiotics vs. cardiovascular) –Price negotiation (mainly) affects drugs used by elderly –Value of marketed drugs declines because expected revenue falls –Value of pre-market drugs (pipeline) also falls, because of revenue and financing effect Effect of election on asset values varies across firms –Change in value of marketed drugs proportional to sales of drugs to elderly –Average revenue effect for pre-market drugs proportional to number of drugs in elderly therapeutic classes (e.g., cardiovascular) –Firms with large decrease in cash flow should experience large decline in average value of pre-market drugs

–Price negotiation (mainly) affects drugs used by elderly –Value of marketed drugs declines because expected revenue falls –Value of pre-market drugs (pipeline) also falls, because of revenue and financing effect Effect of election on asset values varies across firms –Change in value of marketed drugs proportional to sales of drugs to elderly –Average revenue effect for pre-market drugs proportional to number of drugs in elderly therapeutic classes (e.g., cardiovascular) –Firms with large decrease in cash flow should experience large decline in average value of pre-market drugs.")

10

Empirical Strategy (cont.) Link abnormal returns to firm assets –Estimate abnormal returns over seven days following election –Construct measures of elderly drug sales and R&D capital stock –Relate abnormal returns to asset measures and interaction (financing effect) –Assume changes in asset values uncorrelated with unobserved variables Interpretation of results –Discrete change in expected prices –Distinguish financing effect from price effect –How valuable is the average pre-market drug?

Link abnormal returns to firm assets –Estimate abnormal returns over seven days following election –Construct measures of elderly drug sales and R&D capital stock –Relate abnormal returns to asset measures and interaction (financing effect) –Assume changes in asset values uncorrelated with unobserved variables Interpretation of results –Discrete change in expected prices –Distinguish financing effect from price effect –How valuable is the average pre-market drug")

11

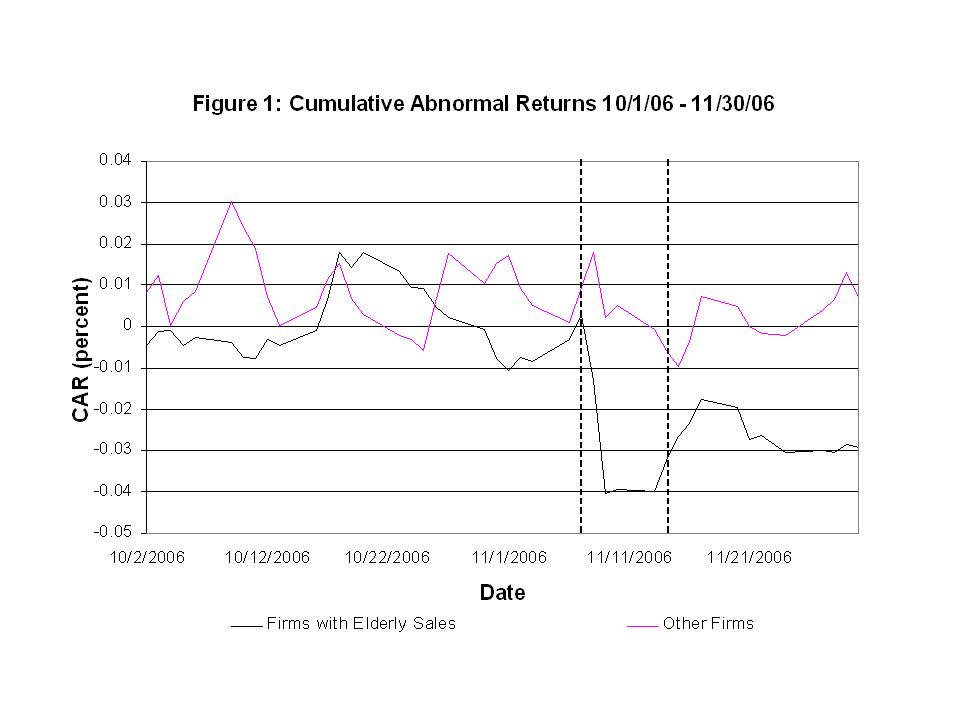

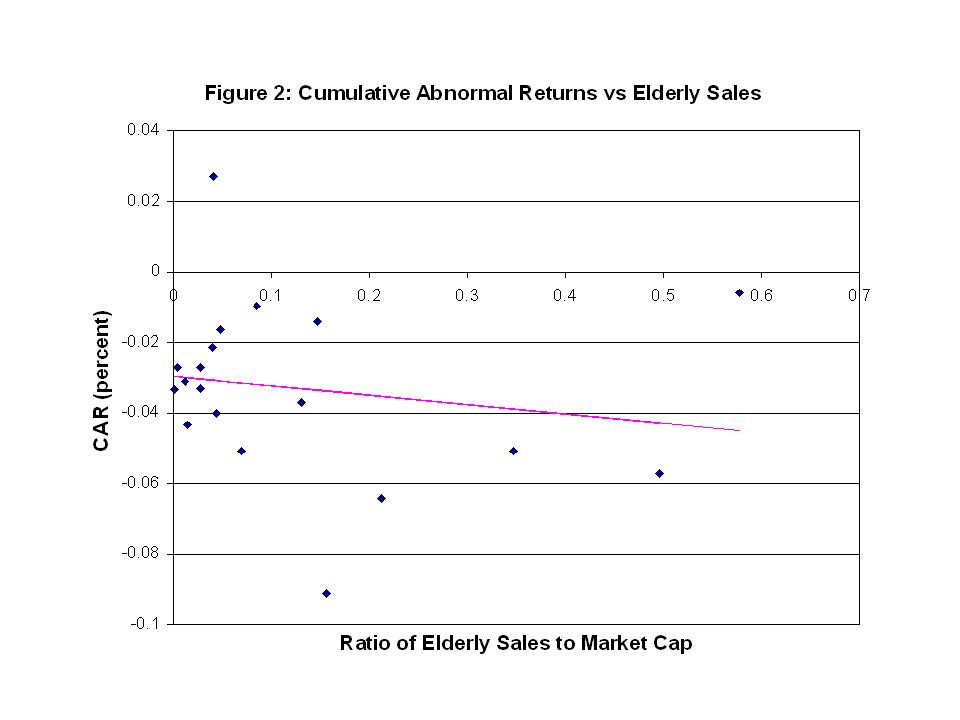

Post-Election Stock Returns Compute abnormal returns for two months surrounding election –Construct value-weighted index of two samples of firms –Firms with prescription drug sales to the elderly (2004 MEPS) –Large pharmaceutical and biotech firms with zero elderly drug sales Decrease in stock prices for pharmaceutical firms with elderly drug sales (Figure 1) –Large, statistically significant decrease for first sample –No change for firms without elderly drug sales Change in stock price negatively correlated with elderly drugs sales (Figure 2)

–Large pharmaceutical and biotech firms with zero elderly drug sales Decrease in stock prices for pharmaceutical firms with elderly drug sales (Figure 1) –Large, statistically significant decrease for first sample –No change for firms without elderly drug sales Change in stock price negatively correlated with elderly drugs sales (Figure 2)")

14

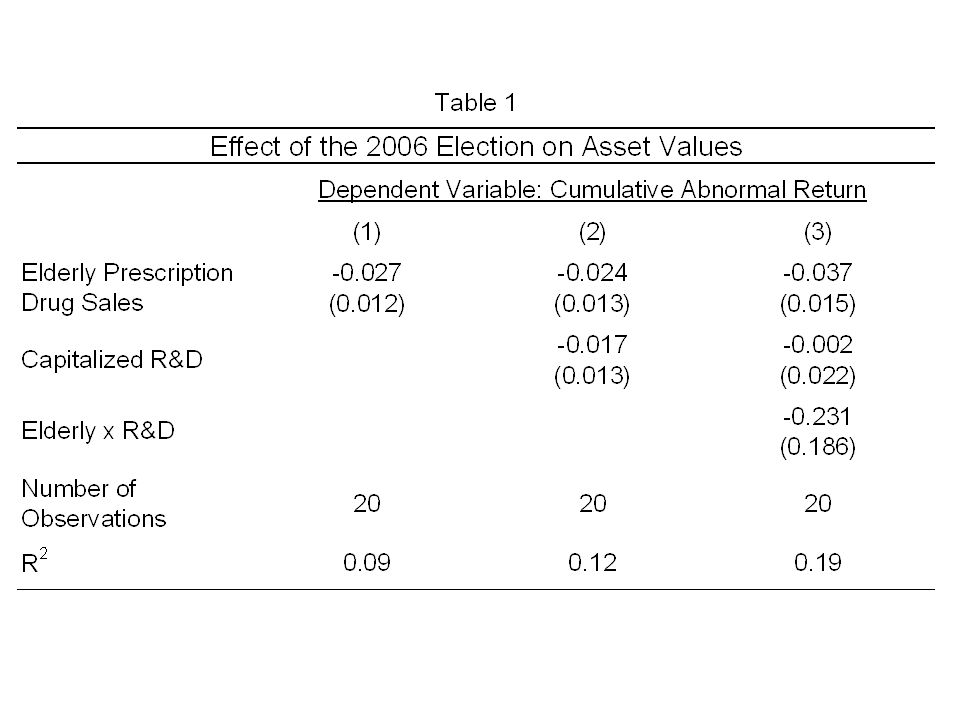

Estimation Results Estimating equation: Relate cumulative abnormal returns (CAR) to firm assets: –Dependent variable is post-election CAR – is firm’s sales to elderly (65+) (from MEPS) –RD i is firm’s capitalized R&D (from Compustat) –Final variable is the interaction of elderly drug sales and R&D Interpretation: –β 1 is percent change in elderly drug sales –β 2 is percent change in value of capitalized R&D –β 3 is the financing effect: do firms with a large decline in elderly drug sales also experience a large decline in the value of their R&D stock?

to firm assets: –Dependent variable is post-election CAR – is firm’s sales to elderly (65+) (from MEPS) –RD i is firm’s capitalized R&D (from Compustat) –Final variable is the interaction of elderly drug sales and R&D Interpretation: –β 1 is percent change in elderly drug sales –β 2 is percent change in value of capitalized R&D –β 3 is the financing effect: do firms with a large decline in elderly drug sales also experience a large decline in the value of their R&D stock")

16

Conclusions How does prescription drug price regulation affect innovation? –Expect innovation to follow profit opportunities –Regulation affects revenue from a potential innovation and cash available for investment Focus on stock prices –2006 election provides a discrete change in expected profitability –Stock prices immediately incorporate change in profitability –Disentangle two effects on return to innovation Evidence that regulation affects revenue of current and future drugs, and that financing effect is important

Similar presentations

>")

Previous research establishes that in new industries, price falls, market output rises, and the number of firms initially rises and then.>")

Fall, 2010.>")