Download presentation

Presentation is loading. Please wait.

1

TOPIC 14 GENERAL LEDGER

2

Unit 1: The double entry principle and T-accounts

WHAT ARE ACCOUNTS IN THE GENERAL LEDGER? An account is where all the information relating to the different transactions is entered. The General Ledger is made up of many different T- accounts. There is an account for every kind of asset, owner’s equity, liability, income and expense. E.g. bank account, stationery account, capital account etc. The accounts are in the shape of a ‘T’ (T accounts)with the left-side called the Debit (Dr) side and the right-hand side called the Credit (Cr) side.

with the left-side called the Debit (Dr) side and the right-hand side called the Credit (Cr) side.")

3

What is the double entry principle?

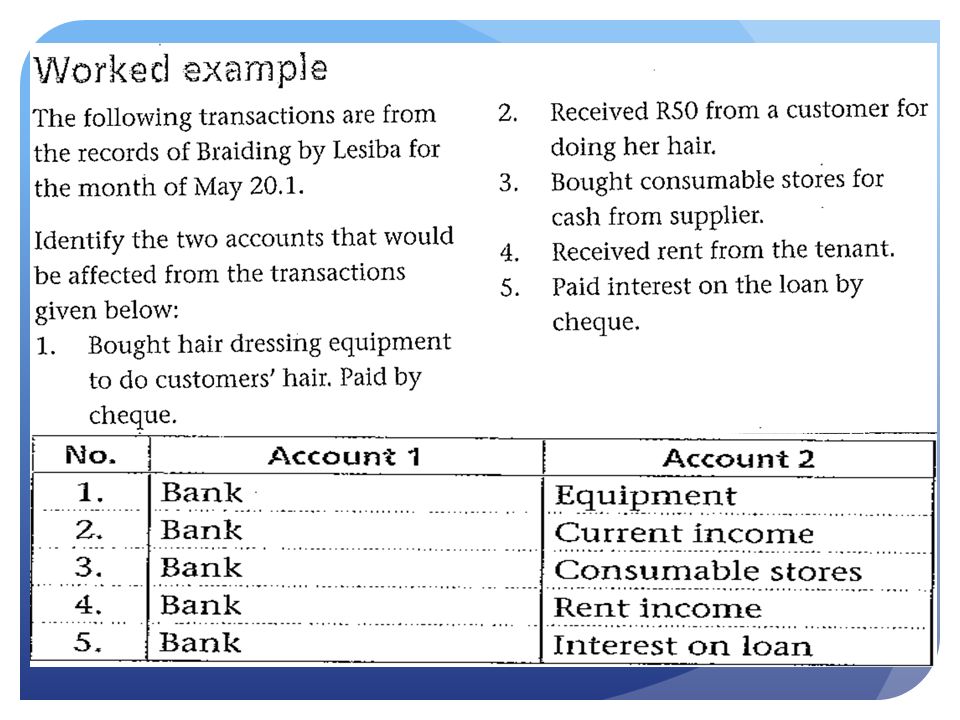

Every transaction will affect two accounts. It will affect one account on the debit side and another account on the credit side. This is called the double entry principle. For example, the owner invests R cash to start a business. The two accounts that would be affected are Bank and Capital. It is very important to firstly be able to identify the two accounts before worrying about the debit and credit.

5

Activity 14.1

6

When does an account get debited or credited?

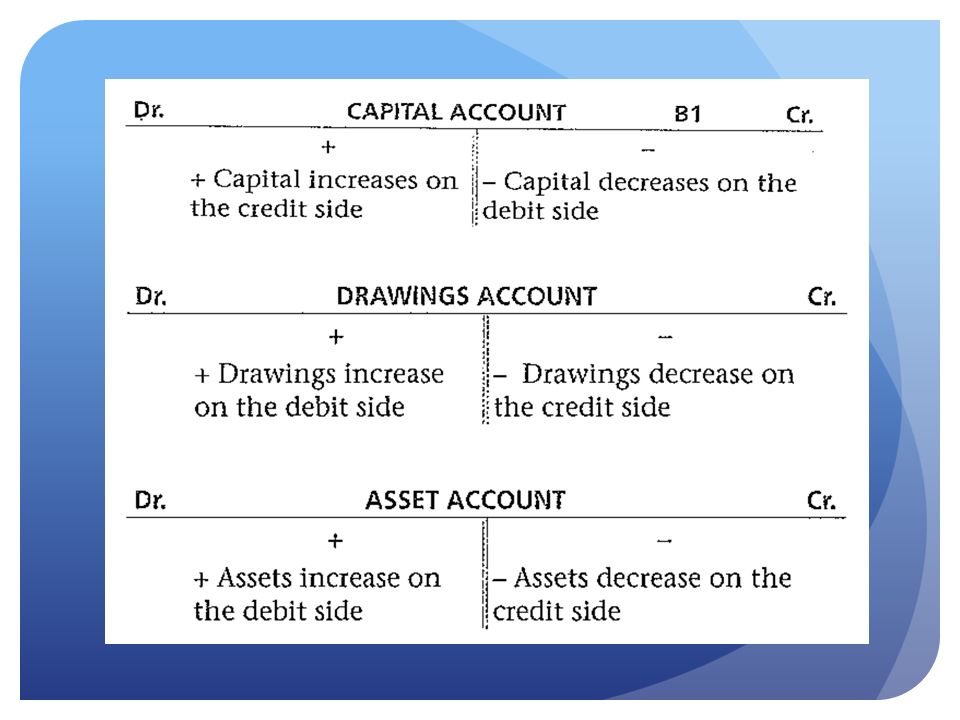

In order to decide whether an account is to be debited or credited, there are rules which must be applied. There are different debit and credit rules for different kinds of accounts. Owner’s equity is split into Capital, Drawings, Incomes and Expenses. This is because drawings and expenses have a negative effect on the owner’s equity and the rule will be different to capital and income which have a positive effect on owner’s equity.

8

For every debit there must be an equal and corresponding credit!

The debit side of all the ledger accounts must ALWAYS equal the credit side.

9

Contra accounts

12

Activity 14.2

13

Unit 2: Format of the General Ledger

15

Sections within the General Ledger

The General Ledger is divided into two sections: The Balance Sheet Section – is the first section in the General Ledger and all the business’s Assets, Owner’s Equity and Liability accounts will appear here. The Nominal Accounts Section – consists of the Income and Expense accounts of the business. It makes it easier to determine the business’s profit it these accounts appear in the same section of the General Ledger.

16

Activity 14.3

17

Activity 14.4

18

Activity 14.5

19

Unit 3: Opening accounts in the General Ledger

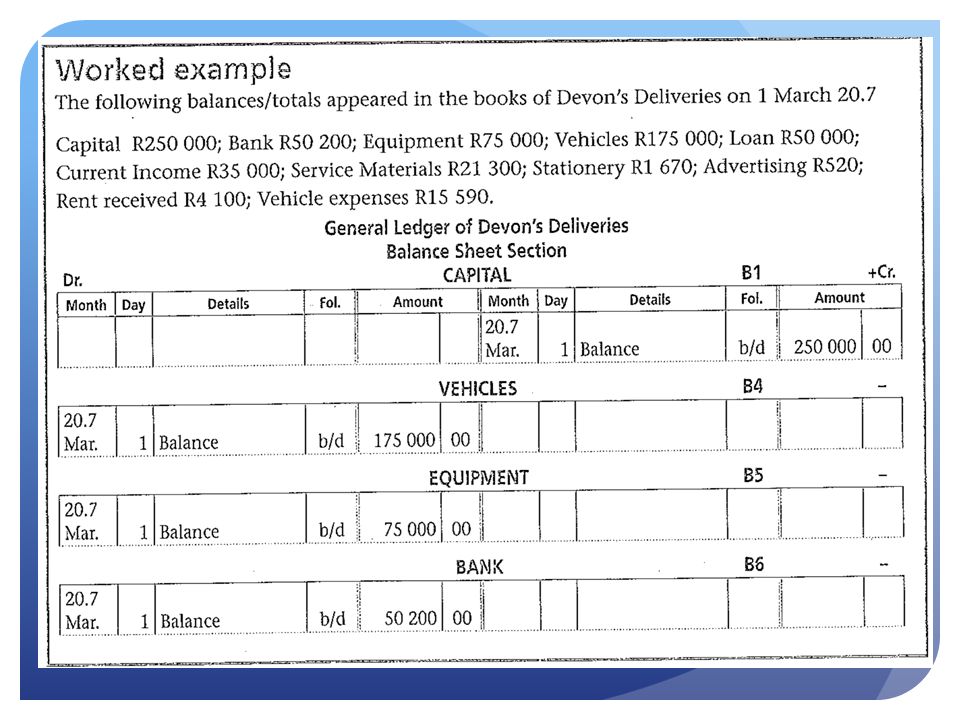

Businesses do not run for one month only, they can operate for years depending on how successful they are. Therefore ledger accounts will already exist and have entries from previous months. For our exercises we need to bring the amount that was in the account from the previous month into the account. The amount is known as the opening balance. Once the balance has been put in the account at the beginning of the month the account is open and the new month’s transactions can be added.

20

The opening balance is the balance that was carried over from the previous month. The balance will either go on the debit side or the credit side of the account. To know whether the account must be debited or credited we refer to the General Ledger rules. The opening balance always appears on the positive side of the account: Drawings, Assets and Expenses – the opening balance goes on the debit side. Capital, Income and Liabilities – the opening balance goes on the credit side.

23

Activity 14.6

24

Unit 4: Posting the Cash Journals of a service business to the General Ledger

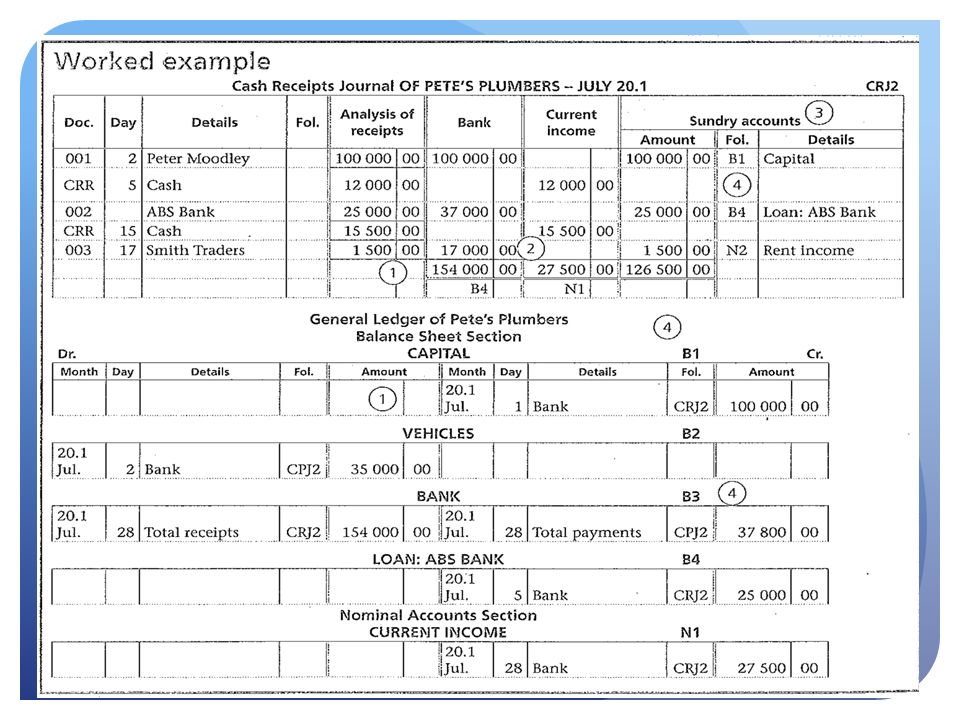

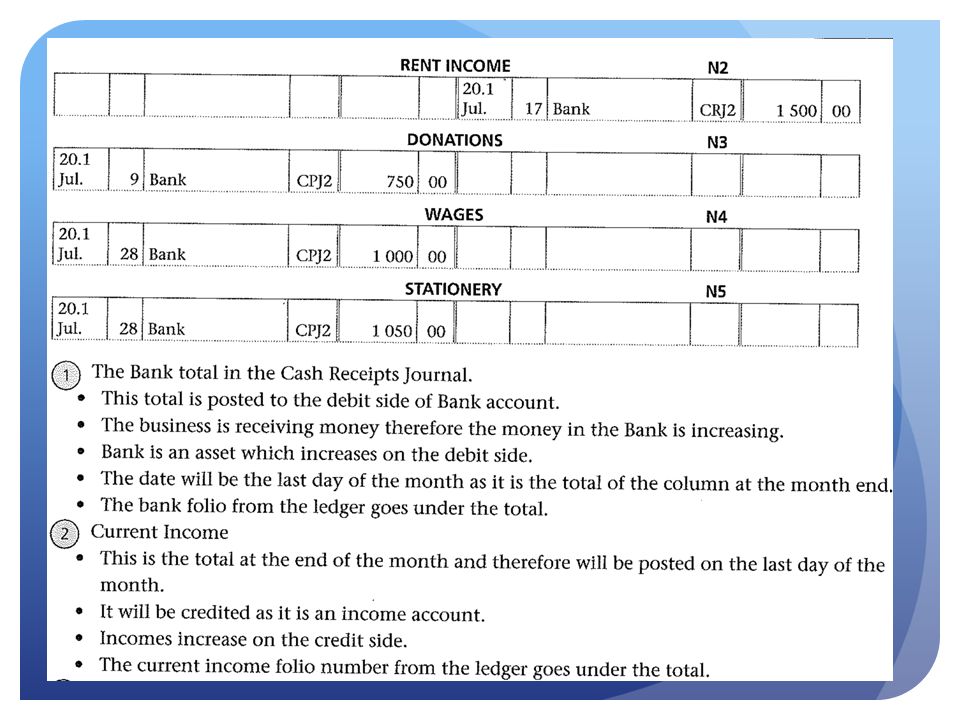

THE ACCOUNTING CYCLE According to the Accounting Cycle, the journals of the business are posted to the General Ledger, not only the individual transactions. The source document is the evidence that the transaction took place. These documents are then recorded into the journals daily. At the end of the month the journals are then posted to the General Ledger. POSTING THE JOURNALS TO THE GENERAL LEDGER At the end of each month the information in the journals is taken to the ledger. In Accounting this is called posting to the ledger. Remember the double entry rule!

25

Posting the Cash Payments to the ledger

When posting from the CPJ to the ledger: Only the totals columns are posted, not each individual transaction. The date is shown as the last date of the month. If a transaction is recorded in the Sundry Accounts column, it is posted separately and the actual date of the transaction is recorded in the ledger. The ‘contra’ or ‘other’ account in the Bank account is Total Payments because more than one account is debited, and we do not want to repeat accounts again in the Bank account. This means that the General Ledger is smaller in size and provides a summary of the journals.

29

Activity 14.7

30

Activity 14.8

31

Posting to the Cash Receipts Journal to the ledger

When posting from the CRJ to the ledger: Only the totals of the columns are posted, not each individual transaction. The date is the last day of the month. If the transaction is recorded in the Sundry accounts column, it is posted separately and the actual date of the transaction is recorded in the Ledger. The ‘contra’ or ‘other’ account in the Bank account is Total Receipts because more than one account is represented as we received money from various sources, and we do not want to repeat accounts again in the Bank account.

35

Activity 14.9

36

Activity 14.10

37

Activity 14.11

38

Activity 14.12

39

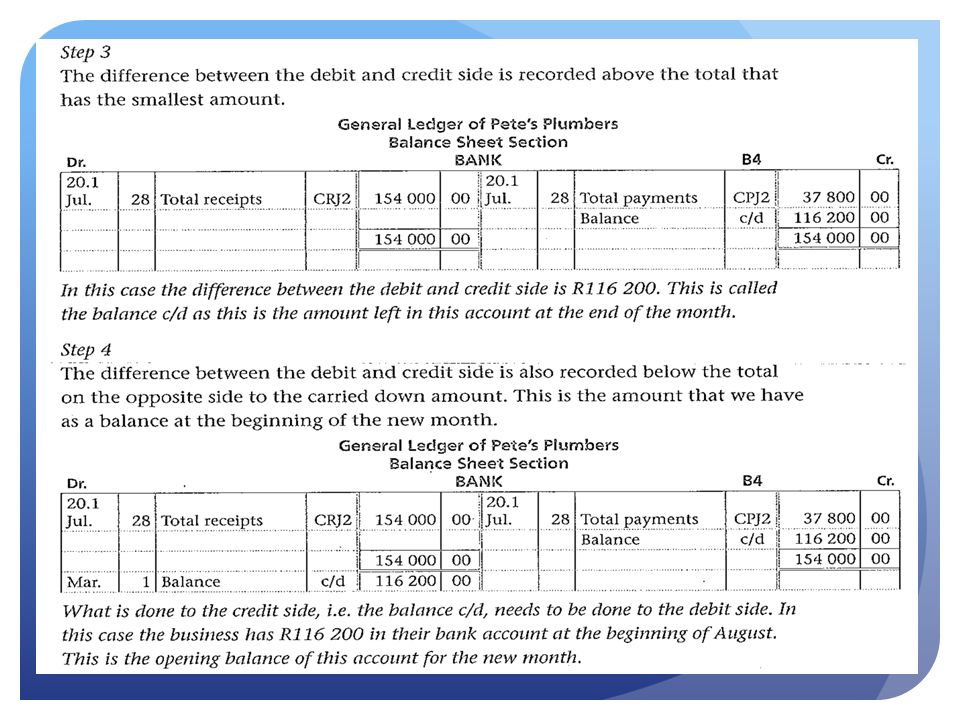

Unit 5: Balancing/totalling ledger accounts at the end of the month

42

Activity 14.13

43

Totalling Nominal Section accounts

Similar presentations