Download presentation

Presentation is loading. Please wait.

1

Chapter 9 The Client Funds Trust Account

2

Funds in a Client Fund Trust Account

Retainers – fee advances Costs and expenses Estate proceeds Escrow funds Settlements Judgment payments Funds from third parties to pay client

3

Retainers /Fee Advances

A fee advance is deposited into the trust account. The fee may not be withdrawn until it is earned. Does not apply to “true” retainers

4

Escrow Funds Real estate transactions

Reasons a firm will receive escrow funds: Real estate transactions When a debtor's payments are made to a creditor If there is a dispute regarding a debt

5

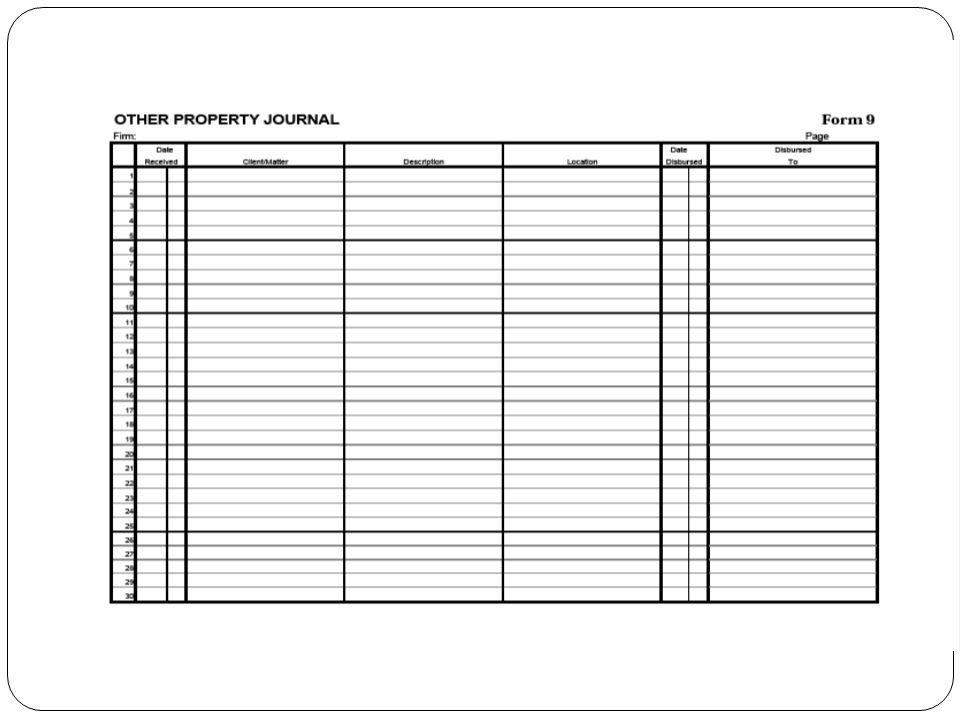

Client’s Property Property other than cash must be accounted for

Securities, stock certificates Personal property

6

Two Types of Client Trust Accounts

IOLTA Accounts Non-IOLTA Account

7

Interest on Lawyers Trust Accounts IOLTA Accounts

Mandatory deposit to IOLTA account: “Nominal” funds Funds held for “short period of time” Compliance is mandatory Interest goes to state bar association Funds legal service programs for indigent Funds client security fund Generally, IOLTA accounts or unsegregated accounts Different client’s funds are deposited in same account

8

Non-IOLTA Client Trust Accounts

An interest bearing client trust account where the interest is payable to the client May be segregated or unsegregated POINTER: Better practice to establish individual segregated accounts for each client Difficult to account for and allocate the interest between several clients in a segregated account Assign client’s SSN or EIN to the account

9

Rules Applicable to All Trust Accounts

The account must be clearly identified as a “Trust Account” or “Client Trust Account” Signatories on the account should be licensed attorneys Cannot deposit law firm funds in the account Cannot keep law firm funds in the account Cannot withdraw trust funds and apply to a disputed fee (cont.)

")

10

Rules Applicable to All Trust Accounts (cont.)

If a client asks for trust funds you must deliver promptly Must account to the client for funds held in trust Must account to the State Bar if requested Must keep trust account records for five (5) year following completion of representation

year following completion of representation.")

11

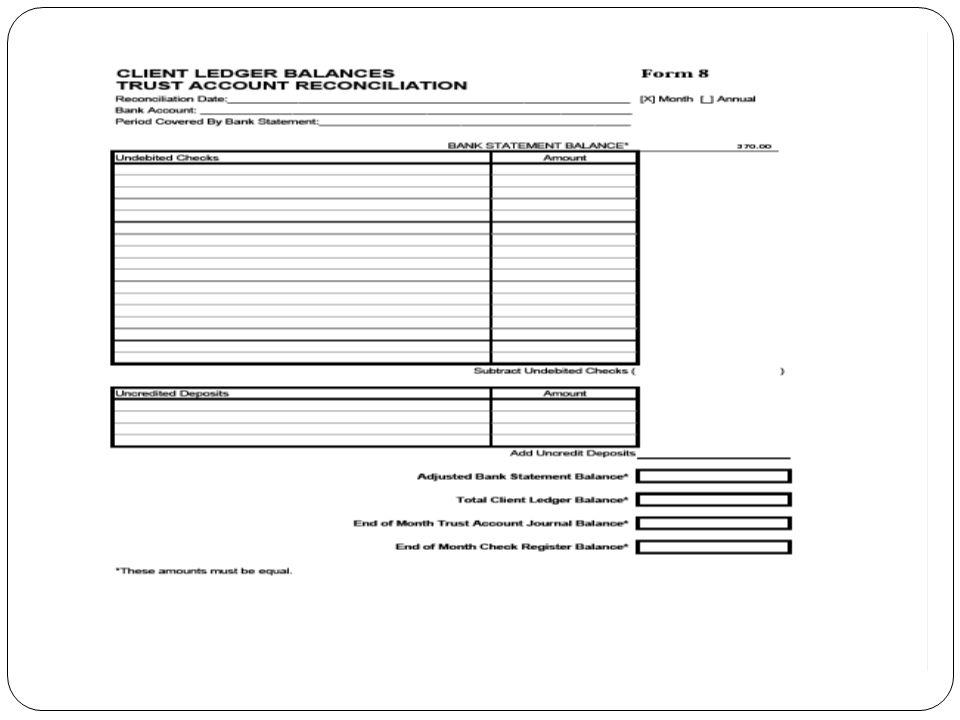

Trust Account Accounting Rules

Manual vs. Computerized systems Minimum Requirements Client Ledger Account Journal Bank Statements and cancelled checks Reconciliation Report Journal of Other Non-cash Properties held

12

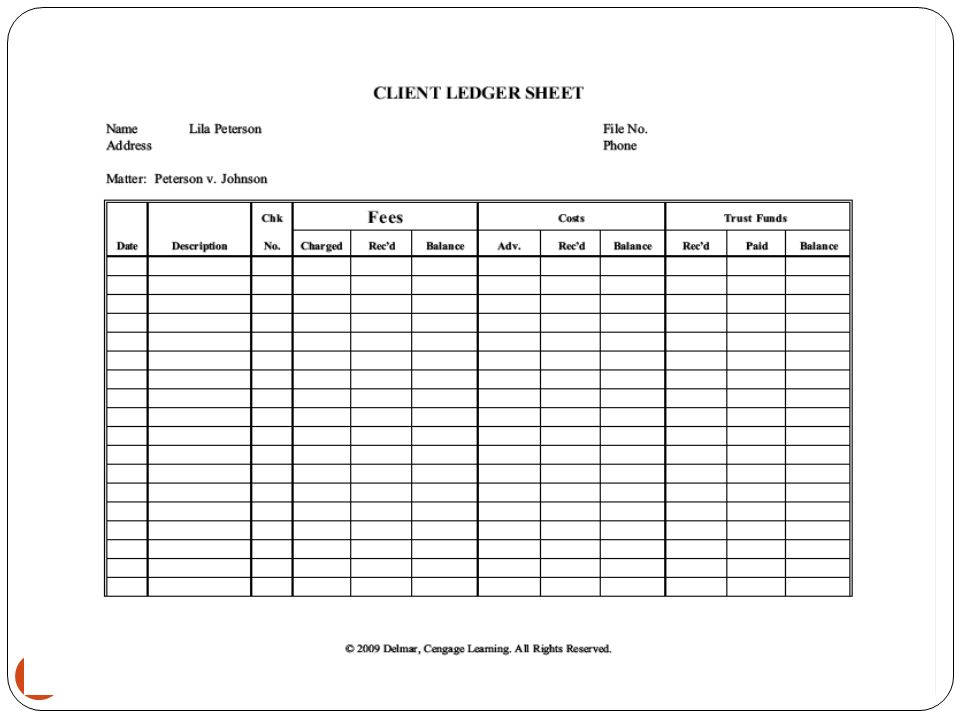

Client Ledger A written ledger for each client that includes:

Date of transaction Source of deposit and amount Payee and purpose of payments and amount Running balance of client’s account Useful where trust account holds several client’s funds

14

Chk Fees Costs Trust Funds Date Description No. Charge Rec’d Balance Adv. Paid 2/25 Client Deposit 2434 $2,500 2,500.00 3/1 Legal Fees $475.00 Fee Payment 467 475.00 -0- 2,025.00 3/10 Filing fee 470 120.00 1,905.00 4/1 Legal fees & costs 860.00 145.00 474 795.00 5/1 525.00 27.80 482 552.80 242.20 5/5 2564 5/15 Deposition Svc 491 345.00 897.20 6/1 Fees & costs 395.00 15.20 500 410.20 487.00

15

Account Journal Similar to the Client Journal

Records all transactions for the account Includes all interest paid and bank charges deducted Keeps a running balance of the account If you have a segregated trust account Client Ledger is sufficient

18

Trust Account Abuses Misappropriation

Using trust funds for personal purposes Overdrawing trust account Using one client’s funds to pay another clients obligation – Example: Client A $1,000 Client B Firm writes a check for $600 for Client B

19

Trust Account Abuses (cont.)

Comingling Client’s funds are intermingled with attorney’s Leaving a buffer or reserve in the trust account Depositing a “true retainer” in trust account Failure to pay fees when earned Failure to promptly disburse funds in trust Settlement proceeds Client expenses Attorney’s fees

20

Trust Account Abuses (cont.)

Failure to account to client for trust funds Failure to notify client of receipt of trust funds Use of Trust account to assist client in secreting assets Creditors Other owners – spouse in divorce, partner, shareholder

Similar presentations

>")

requires that you reconcile the two records by the 25th of each month relating to all trust.>")