Download presentation

Presentation is loading. Please wait.

1

©2002 South-Western Publishing, A Division of Thomson Learning

Monopoly Del Mar College John Daly ©2002 South-Western Publishing, A Division of Thomson Learning

2

The Theory of Monopoly There is one seller

The single seller sells a product for which there is no close substitute There are extremely high barriers to entry

3

Barriers To Entry Legal Barriers: a Public Franchise is a right granted to a firm by government that permits the firm to provide a particular good or service and excludes all others from doing the same. Economies of Scale: In some industries, low average total costs are only obtained through large scale production. If only one firm can survive in that industry, the firm is called a Natural Monopoly. Exclusive Ownership of a Necessary Resource: Existing firms may be protected from entry of new firms by the exclusive or near-exclusive ownership of a resource needed to enter the industry.

4

Government Monopolies Vs. Market Monopolies

Some economists use the term government monopoly to refer to monopolies that are legally protected from competition and the term market monopoly to refer to monopolies that are not legally protected from competition.

5

Q & A John states that there are always some close substitutes for the product any firm sells, therefore the theory of monopoly (which assumes no close substitutes) cannot be useful. How do economies of scale act as a barrier to entry? How is a movie superstar like a monopolist?

cannot be useful. How do economies of scale act as a barrier to entry How is a movie superstar like a monopolist")

6

Monopoly Pricing and Output Decisions

A monopolist is a price searcher; that is, it is a seller that has the ability to control to some degree the price of the product it sells. In the theory of monopoly, the monopoly firm is the industry and the industry is the monopoly firm. They are the same

7

For Monopolists: Note that the price of the good being sold is greater than the marginal revenue. P>MR To sell an additional unit of a good (per time period), the monopolist must lower price. The monopolist gains and loses by lowering price. The gain equals the price of the product times one. The loss equals the difference between the new lower price and the old higher price times the units of output sold before the price was lowered. Marginal revenue can be defined as revenue gained minus revenue lost P=Revenue gained, MR=Revenue Gained – revenue lost, and revenue lost is >0. Therefore, P>MR

, the monopolist must lower price. The monopolist gains and loses by lowering price. The gain equals the price of the product times one. The loss equals the difference between the new lower price and the old higher price times the units of output sold before the price was lowered. Marginal revenue can be defined as revenue gained minus revenue lost. P=Revenue gained, MR=Revenue Gained – revenue lost, and revenue lost is >0. Therefore, P>MR.")

8

The Dual Effects of a Price Reduction on Total Revenue

To sell an additional unit of the good, a monopolist needs to lower price. This price reduction both gains revenue and loses revenue for the monopolist. In the exhibit, the revenue gained and revenue lost are shaded and labeled. Marginal revenue is equal to the larger shaded area minus the smaller.

9

P(Q) = a - bQ …linear demand…

Example: P(Q) = a - bQ …linear demand… TR(Q) = QP(Q) a. What is the equation of the marginal revenue curve? P/Q = -b MR(Q) = P + QP/Q = a - bQ + Q(-b) = a - 2bQ **twice the slope of demand for linear demand**

= a - bQ …linear demand… TR(Q) = QP(Q) a. What is the equation of the marginal revenue curve P/Q = -b. MR(Q) = P + QP/Q. = a - bQ + Q(-b) = a - 2bQ **twice the slope of. demand for linear. demand**")

10

b. What is the equation of the average revenue curve?

AR(Q) = TR(Q)/Q = P = a - bQ (you earn more on the average unit than on an additional unit…)

= TR(Q)/Q = P = a - bQ. (you earn more on the average unit than on an additional unit…)")

11

c. What is the profit-maximizing output if:

TC(Q) = Q + Q2 MC(Q) = Q AVC(Q) = 20 + Q AC(Q) = 100/Q Q P(Q) = Q MR = MC => Q = Q Q* = 20 P* = 80

= Q + Q2. MC(Q) = Q. AVC(Q) = 20 + Q. AC(Q) = 100/Q Q. P(Q) = Q. MR = MC => Q = Q. Q* = 20. P* = 80.")

12

Monopolist Demand and Marginal Revenue Curves

In monopoly, the firm’s demand curve is not the same as its marginal revenue curve. The monopolist’s demand curve lies above its marginal revenue curve.

13

Maximizing Profit, Monopolist Style

Maximizing revenues is the same as maximizing profits only when a firm has no variable costs. It is unlikely, though, that a firm will be without variable costs. The monopolist that seeks to maximize profits produces the quantity of output at which MR=MC and charges the highest price per unit at which this quantity of output can be sold.

14

The Monopolist’s Profit-Maximizing Price and Quantity of Output

The monopolist produces the quantity of output (Q1) at which MR=MC, and charges the highest price per unit at which the quantity of output can be sold (P1). Notice that at the profit maximizing quantity of output, price is greater than marginal cost, P>MC.

at which MR=MC, and charges the highest price per unit at which the quantity of output can be sold (P1). Notice that at the profit maximizing quantity of output, price is greater than marginal cost, P>MC.")

15

This profit is positive. Why

This profit is positive. Why? Because the monopolist takes into account the price-reducing effect of increased output so that the monopolist has less incentive to increase output than the perfect competitor. Profit can remain positive in the long run. Why? Because we are assuming that there is no possible entry in this industry, so profits are not competed away.

16

X-INEFFICIENCY: Cost that is higher than it needs to be because a firm is operating inefficiently. This is most often seen for firms that have a great deal of market control, especially monopoly. The lack of competition allows a business to pad it's expenses, hire unneeded employees (like relatives), goof off instead of working, and all sorts of other things that lessen production and increase cost. The business is not penalized for these actions, because market control allows the company to extract whatever price is needed to cover cost.

, goof off instead of working, and all sorts of other things that lessen production and increase cost. The business is not penalized for these actions, because market control allows the company to extract whatever price is needed to cover cost..")

17

Competition Vs. Monopoly

For the perfectly competitive firm, P=MR; for the monopolist, P>MR. The perfectly competitive firm’s demand curve is its marginal revenue curve; the monopolist’s demand curve lies above its marginal revenue curve The perfectly competitive firm charges a price equal to marginal cost; the monopolist charges a price greater than marginal cost. A monopoly firm differs from a perfectly competitive firm in terms of how much consumers’ surplus buyers receive.

18

Using this formula: When demand is elastic ( > -1), MR > 0 When demand is inelastic ( < -1), MR < 0 When demand is unit elastic ( = -1), MR= 0

, MR= 0.")

19

Price Example: Elastic Region of the Demand Curve a Elastic region ( < -1), MR > 0 Unit elastic (=-1), MR=0 Inelastic region (0>>-1), MR<0 a/2b a/b Quantity

, MR<0. a/2b a/b. Quantity.")

20

Q & A Why does the monopolist’s demand curve like above its marginal revenue curve? Is a monopolist guaranteed to earn profits? Is a monopolist resource allocative efficient? A monopolist is a price searcher. Why do you think it is called a price searcher? What is it searching for?

21

The Case Against Monopoly

The Deadweight Loss of Monopoly: Greater output is produced under perfect competition than under monopoly. The net value of the difference in these two output levels is said to be the deadweight loss of monopoly. This is the amount buyers value the additional output over and above the opportunity costs of producing the additional output. Rent Seeking: If firm A tries to get the government to transfer “income” or consumers’ surplus from buyers to itself it is undertaking a transfer seeking activity. In economics, these activities are usually called Rent Seeking.

22

Deadweight Loss and Rent Seeking as Costs of Monopoly

The monopolist produces QM, and the perfectly competitive firm produces the higher output level QPC. The deadweight loss of the monopoly is the triangle (DCB) between these two levels of output. Rent seeking is a socially wasteful activity because resources are expended to affect a transfer and not to produce goods and services.

between these two levels of output. Rent seeking is a socially wasteful activity because resources are expended to affect a transfer and not to produce goods and services.")

23

The Welfare Economics of Monopoly

Since the monopoly equilibrium output does not, in general, correspond to the perfectly competitive equilibrium it entails a dead-weight loss. 1. Suppose that we compare a monopolist to a competitive market, where the supply curve of the competitors is equal to the marginal cost curve of the monopolist…

24

CS with competition: A+B+C CS with monopoly: A

PS with competition: D+E PS with monopoly:B+D DWL = C+E MC A PM B C Example: The Welfare Effect of Monopoly PC E D Demand QM QC MR

25

2.Dead-weight loss in a Natural Monopoly Market

Definition: A market is a natural monopoly if the total cost incurred by a single firm producing output is less than the combined total cost of two or more firms producing this same level of output among them. Benchmark: What would be the market outcome if the monopolist produced according to the same rule as a perfect competitor (i.e., P = MC)?

")

26

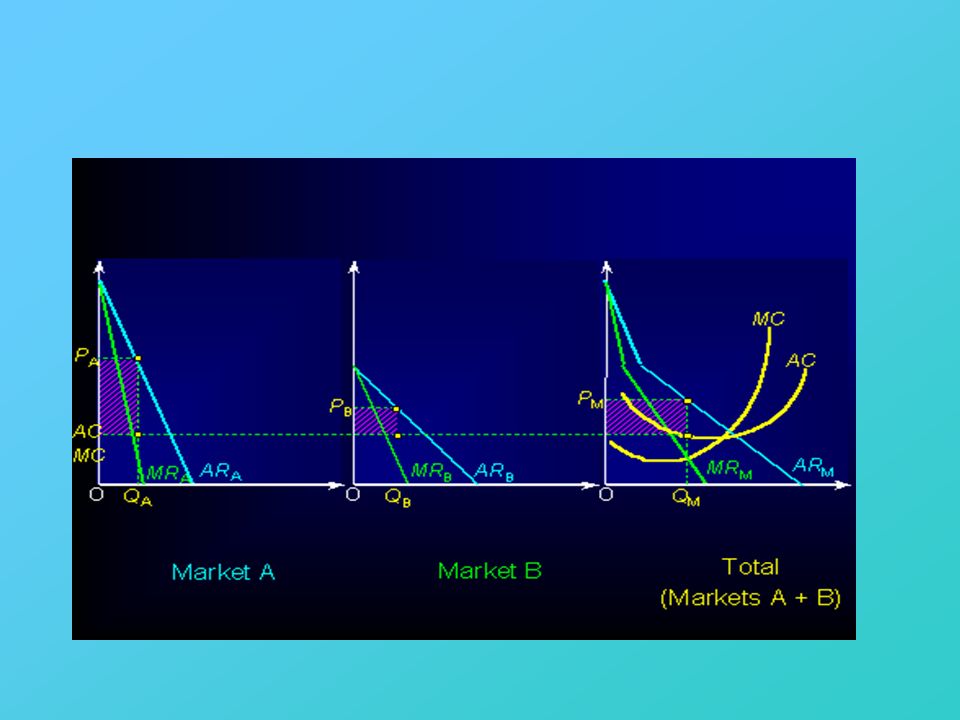

Price Discrimination Price discrimination occurs when the seller charges different prices for the product it sells, and the price differences do not reflect costs. Perfect Price Discrimination: sells each unit separately and charges the highest price each consumer would be willing to pay for the product. Second Degree Discrimination: it charges a uniform price per unit for one specific quantity, a lower price for an additional quantity, and so on. Third Degree Discrimination: it charges a different price in different markets or charges a different price to different segments of the buying population

27

Why Price Discrimination?

For the monopolist who practices perfect price discrimination, price equals marginal revenue. Conditions of Price Discrimination: The seller must exercise some control over price; it must be a price searcher. The seller must be able to distinguish among buyers who would be willing to pay different prices. It must be impossible or too costly for one buyer to resell the good at other buyers. The possibility of arbitrage, or “buying low and selling high” must not exist. The perfectly price discriminating monopolist and the perfectly competitive firm both exhibit resource allocative efficiency.

31

Price Discrimination The perfectly price-discriminating monopolist tries to get the highest price for each customer, irrespective of what other customers pay. One of the uses of the cents-off coupon is to make it possible for the seller to charge a higher price to one group of customers than to another group.

32

Q & A What are some of the “costs” or shortcomings of monopoly?

What is the deadweight loss of monopoly? Why must a seller be a price searcher (among other things) before he can price discriminate

before he can price discriminate.")

33

Summary 1. A monopoly market consists of a single seller facing many buyers (utilities, postal services). 2. A monopolist's profit maximization condition is to set the marginal revenue of additional output (or a change in price) equal to the marginal cost of additional output (or a change in price). 3. Marginal revenue generally is less than price. How much less depends on the elasticity of demand. 4. A monopolist generally never produces on the inelastic portion of demand since, in the inelastic region, raising price and reducing quantity make total revenues rise and total costs fall! 5. The Lerner Index is a measure of market power, often used in antitrust analysis.

equal to the marginal cost of additional output (or a change in price). 3. Marginal revenue generally is less than price. How much less depends on the elasticity of demand. 4. A monopolist generally never produces on the inelastic portion of demand since, in the inelastic region, raising price and reducing quantity make total revenues rise and total costs fall! 5. The Lerner Index is a measure of market power, often used in antitrust analysis.")

Similar presentations