Download presentation

Presentation is loading. Please wait.

1

Restoring the Credibility of Casualty Actuaries Casualty Loss Reserve Seminar Boston, MA Panelists: Members of the Joint Task Force on Enhancing the Reputation of Casualty Actuaries

2

With you today…. Mary D. Miller – American Academy of Actuaries, VP Casualty Practice Council Mary Frances Miller – Actuarial Standards Board Mike Toothman – Actuarial Board for Counseling & Discipline Pat Teufel – Chair –CAS Board Task Force on Actuarial Credibility –CAS Representative to Joint Task Force

3

Objectives for the Session Provide Information –Background leading to commissioning of the CAS Task Force on Actuarial Credibility –Recommendations of the CAS Task Force –Active Involvement of other US organizations representing casualty actuaries HEAR WHAT YOU THINK ENCOURAGE YOUR PARTICIPATION!

4

Setting the Stage….

5

Actuaries Under Attack: Is the Profession Living Up to Its Responsibilities? Standard & Poors – “Whether through knavery or naiveté….” Morris Review – “Profession that has been too introspective, not forward-looking enough and slow to modernize” Litigation Against Actuaries On Rise – “Professional negligence and malpractice, misrepresentation and aiding and abetting breaches of fiduciary duties”

6

Turbulence is life force. It is opportunity. Let’s embrace turbulence and use it for change.

7

CAS Board Response Meetings with Standard & Poors and other rating agencies Board Retreat to discuss possible responses Task Force on Actuarial Credibility charged to: “Identify, prioritize and investigate the feasibility of possible strategies for enhancing the perceived credibility of the casualty actuarial profession and develop action plans for implementation of those strategies considered to have the greatest potential for high impact.”

8

CAS Task Force on Actuarial Credibility

9

Recommendations 1. To enhance the transparency of the actuary’s conclusions by clearly identifying within the statement of actuarial opinion differences, if any, that exist between management’s “best estimate” of the loss and loss adjustment expense reserves as of a valuation date and the actuary’s “best estimate” of the reserve need as of the valuation date.

10

Recommendations 2.To enhance the public’s understanding of actuarial estimates, including the “best estimate” and the range of reasonable reserve outcomes, as well as estimates of the range of all possible settlement outcomes. To refine actuarial methodologies for estimating the underlying probability distributions for the range of loss and loss adjustment expense reserves, facilitating greater consistency in the approaches used by actuaries and improved transparency of financial reporting disclosures.

11

Recommendations 3. To improve the transparency of disclosures by requiring that the actuarial report contain an exhibit that summarizes changes in the actuary’s estimates from one period to the next, with extended discussion of significant factors underlying the changes.

12

Recommendations 4. To enhance the quality of corporate governance for property/casualty insurers by educating audit committees or boards of directors or both on the roles and responsibilities of the appointed actuary. To increase the visibility of the appointed actuary within the corporate governance arena.

13

Recommendations 5. To enhance the self-governance of the actuarial profession with respect to property/casualty loss and loss adjustment expense reserve opinions by requiring the appointed actuary to provide an explanatory document with the Actuarial Board for Counseling and Discipline (ABCD) whenever the change in the actuary’s reserve estimates over a defined period exceeds certain predetermined thresholds. The explanatory document would discuss the changes in the actuary’s estimates, as well as the significant factors underlying the changes.

whenever the change in the actuary’s reserve estimates over a defined period exceeds certain predetermined thresholds. The explanatory document would discuss the changes in the actuary’s estimates, as well as the significant factors underlying the changes..")

14

Recommendations 6. To elevate the unique role of the appointed actuary within the statutory financial reporting environment by incorporating an Actuarial Statement within the Jurat Page of each property/casualty insurance company’s Annual Statement.

15

CAS Leadership Actuarial Standards Board

16

ASB Process on ASOP Changes 1.Recommendation to ASB to initiate review 2.ASB charges Casualty Committee to review 3.Casualty Committee or Subcommittee develops exposure draft for ASB review 4.ASB votes to expose to members for comments

17

ASB Process on ASOP Changes (continued) 5.Casualty Committee receives and reviews comments – considers and responds to all of the comments 6.Casualty Committee considers and responds to all of the input and revises draft accordingly 7.ASB reviews revision and comments. –If changes are significant, draft ASOP is re- exposed (step 4). –If not significantly changed, ASB can vote to adopt.

. –If not significantly changed, ASB can vote to adopt..")

18

American Academy of Actuaries

19

August 2001 – Casualty Actuarial Task Force (CATF) formed Actuarial Opinion Instructions Working Group (AOIWG) Monthly calls with input from AAA and other industry representatives Result – Revised content and format for 2004 Opinions This is not the only game in town !This is not the only game in town !

formed Actuarial Opinion Instructions Working Group (AOIWG) Monthly calls with input from AAA and other industry representatives Result – Revised content and format for 2004 Opinions This is not the only game in town !This is not the only game in town !")

20

Result – AOS required in 2005 Result – Regulatory Guidance Briefs are published annually starting in 2004 in AAA P&C Practice Note Result – Specific Requirement for auditor to consult with actuary regarding data relied on This is not the only game in town !This is not the only game in town !

21

Result – Increased regulator involvement in CLRS and other professional meetings Result – Better Opinions - More Disclosures This is not the only game in town !This is not the only game in town !

22

CAS Committee on Reserves URIL Subcommittee and AAA Financial Soundness and Risk Management Committees both researching company failures and large reserve increases AAA sponsoring 1 st Opinion ‘Boot Camp’ next month – sold out quickly – 2 nd day added This is not the only game in town !This is not the only game in town !

23

Unprecedented AAA/CAS/CATF cooperation on Risk Transfer Project Increased COPLFR and CATF presence at regional affiliate meetings New Standard on Unpaid Claim Liabilities on the horizon This is not the only game in town !This is not the only game in town !

24

Actuarial Board for Counseling & Discipline

25

Code of Professional Conduct Professional Integrity - Precept 1 Qualification Standards - Precept 2 Standards of Practice - Precept 3 Communications and Disclosure - Precepts 4, 5, and 6 Conflict of Interest - Precept 7 Control of Work Product – Precept 8 Confidentiality – Precept 9 Courtesy and Cooperation – Precept 10 Advertising – Precept 11 Titles and Designations – Precept 12 Violations of the Code of Professional Conduct – Precepts 13 and 14 The Code of Professional Conduct identifies the professional and ethical standards required of actuaries who belong to the Academy. The SOA, ASPA, the CAS, and the CCA have adopted identical codes.

26

Counseling and Discipline Overview AAAASPACAS CCA SOA Actuarial Organizations ABCD “Interpreter“ “Enforcer” Professional Integrity Qualification Standards Standards of Practice Communications and Disclosure Conflict of Interest Control of Work Product Confidentiality Courtesy and Cooperation Advertising Titles and Designations Violations of the Code Actuarial Standards of Practice (Develop, Revise, and Adopt) Violations of the Code of Professional Conduct ASB “Standard Setter” Drafted Qualification Standards Code of Professional Conduct

Violations of the Code of Professional Conduct ASB Standard Setter Drafted Qualification Standards Code of Professional Conduct")

27

Role of the ASB The ASB is an independent entity established in 1988 as the single board promulgating standards of practice for the entire actuarial profession in the US. The ASB has the sole authority to develop, obtain comment on, revise, and adopt standards of practice in the actuarial profession. The ASB is comprised of nine persons representing a broad range of backgrounds and areas of actuarial practice, with members from the AAA, ASPA, CAS, CCA, and SOA. Members of the ASB are appointed by a selection committee composed of the Presidents and Presidents-Elect of the AAA, ASPA, CAS, CCA, and SOA. ASB AAASOACCACAS ASPA Areas of Practice: Casualty, Health, Life, Pension, and General

28

Role of the ABCD The ABCD was formed to serve the five US-based organizations representing actuaries. The ABCD also serves the CIA relative to practice by its members in the US. These organizations have delegated authority for counseling and discipline to the ABCD. This includes the authority to investigate and evaluate possible violations of the Code of Professional Conduct. –Counseling –Discipline –Requests for guidance –Mediation CIA ABCD AAASOACCACAS ASPA Members “practicing” in the US

29

The ABCD’s board members represent all main areas of actuarial practice. Members of the ABCD are appointed by a Selection Committee composed of the Presidents and Presidents-Elect of the AAA, ASPA, CAS, CCA, and SOA. Current ABCD Board Members William J. Falk, Chairperson Frank S. Irish, Vice Chairperson Lawrence A. Johansen, Vice Chairperson Linda L. Bell Edward E. Burrows Julia T. Philips Richard S. Robertson Carol R. Sears Michael L. Toothman Staff Liaison: Thomas C. Griffin ABCD Board Members

30

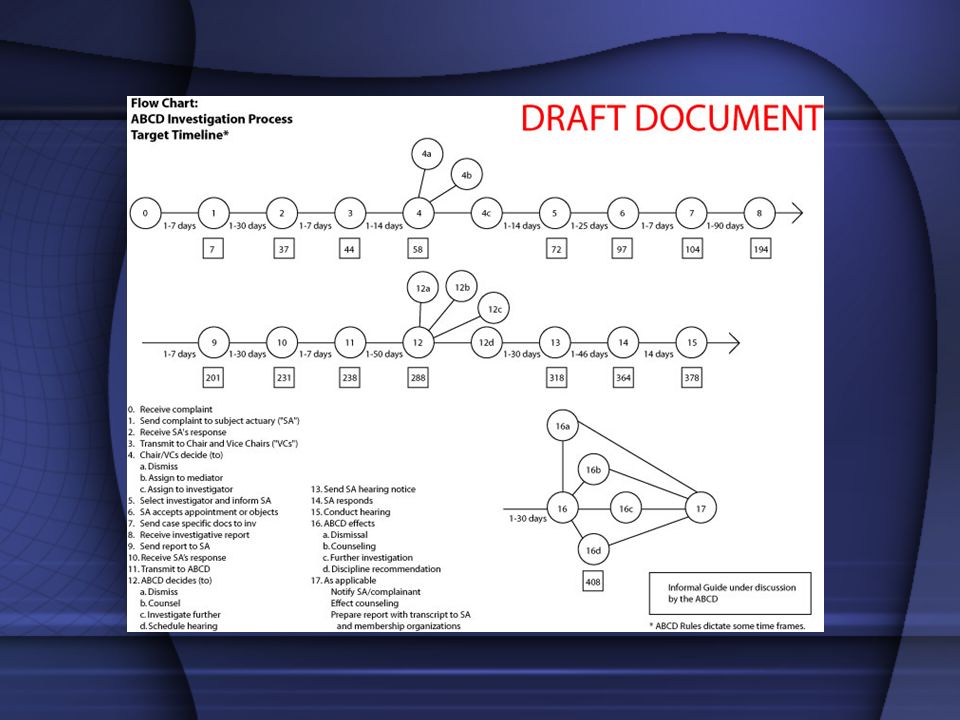

Details of Counseling and Discipline Process

31

The ABCD addresses complaints of possible Code violations, but also answers informal inquiries and requests for guidance from actuaries who have questions concerning professional matters. Complaints and Matters for Inquiry Process for addressing formal complaints: Complaints may come from an actuary or others using actuarial services. ABCD staff completes the initial review. If not dismissed, staff refers complaint to the “subject actuary”. The ABCD Chairs review the subject actuary’s response and either dismiss the case or appoint a mediator or investigator. Investigation can take many months. How Cases/Complaints Arise Informal Inquiries and Requests for Guidance In many cases, requests of the ABCD are informal: Generally answered by individual ABCD member. Response represents individual ABCD member’s opinion and not necessarily the ABCD’s view. ABCD also responds to formal requests for guidance: These matters are considered by the ABCD as a whole. If appropriate, written formal guidance is provided.

32

Complainant ABCD Subject Actuary ABCD “Full Group” Matters for Inquiry Matters for Inquiry ABCD “Chairs Committee” Information Received Information Received Complaints Initial Processing Initial Processing Dismiss Gather Further Information Gather Further Information Response by Subject Actuary Response by Subject Actuary Reviewed by Chairs Committee Reviewed by Chairs Committee Dismiss Mediate Investigate ABCD Formal Complaint Process Flow

33

Complainant ABCD Subject Actuary ABCD “Full Group” ABCD “Chairs Committee” Response by Subject Actuary Response by Subject Actuary Reviewed by Full ABCD Reviewed by Full ABCD Dismiss Provide Counsel Provide Counsel Recommend Discipline Recommend Discipline Dismiss Mediate Investigate ABCD Formal Complaint Process Flow

35

ABCD Case Resolution ABCD cases considered during 2004: Type of Case Pending from 2003 and Earlier Received in 2004 Total Conduct6612 Practice448 Conduct & Practice 415 Requests for Guidance 24446 Total165571 Cases by Practice Area Pending from 2003 and Earlier Received in 2004 TotalCasualty51419 Health2911 Life21113 Pension72128 Total165571

36

ABCD Case Resolution ABCD cases considered during 2004: CASES CLOSED Action by Individual ABCD members Replied to requests for guidance46 Disposition by Chairperson and Vice Chairpersons Dismissed 4 (Referred to Investigators in 2004—4) Disposition by Whole ABCD after investigation Dismissed 1 Dismissed with guidance 2 Counseled 1 Counseled after hearing 0 Recommended suspension 0 Total54 CASES IN PROGRESS (as of 12/31/03) Pending investigation 3 Pending hearing 7 Pending receipt of more information 3 Request for Guidance pending 4 Total17

Disposition by Whole ABCD after investigation Dismissed 1 Dismissed with guidance 2 Counseled 1 Counseled after hearing 0 Recommended suspension 0 Total54 CASES IN PROGRESS (as of 12/31/03) Pending investigation 3 Pending hearing 7 Pending receipt of more information 3 Request for Guidance pending 4 Total17")

37

ABCD Case Resolution Since its inception in 1992, the ABCD completed its cases as follows: Dispositions1992199319941995199619971998199920002001200220032004Total Dismissed122491181113105201675151 Dismissed with guidance 6103__51528542253 Counseled__281625__2324136 Mediated311________1__4__1__11 Recommended private reprimand ________________11______2 Recommended public discipline __12__3__1__3____1__11 Replied to requests for guidance 88810283122313621473046326 Total29463122504546445554694554590

38

Challenges/ Weakness 1.Lack of understanding within the profession of the counseling and discipline process and the role of the ABCD (exacerbated by confidentiality issues) 2.Reliance on practitioners to self-police in many cases 3.Timing of the process Challenges/Weakness in the Current System

2.Reliance on practitioners to self-police in many cases 3.Timing of the process Challenges/Weakness in the Current System")

39

Questions???

40

Joint Task Force for Enhancing the Reputation of Casualty Actuaries

41

Role & Responsibilities Oversee implementation of Task Force recommendations by the various organizations representing casualty actuaries Communicate progress to each of the actuarial organizations Work through “hurdles”, if any, encountered during implementation

42

Progress to Date Confirmed agreement of all organizations on general direction for the initiative Changed Name for Task Force from: –Joint Task Force for Restoring Actuarial Credibility to –Joint Task Force for Enhancing the Reputation of Casualty Actuaries Discussed recommendation for public disclosure of “best estimate” at length Preparing Survey of Opinion Writers

43

NOW IT’S YOUR TURN

44

In your opinion, based on facts and circumstances that were known or knowable as of the valuation date, was the property/casualty insurance industry under-reserved as of December 31, 2004? A.Yes, by more than 10% of the industry’s carried reserves B.Yes, by 1 - 9% of the industry’s carried reserves C.No D.No Opinion. I don’t have enough facts.

45

In your opinion, would a thorough reading of the statements of actuarial opinion rendered as of December 31, 2004 have identified to the users of those opinions those companies that contributed most significantly to the industry’s overall reserve position (either favorably or unfavorably)? A.Yes B.No C.No Opinion. I don’t have enough facts.

46

The following factors have been identified as potential contributing factors to the property/casualty industry’s perceived reserve deficiency position. In your opinion, what is the most significant factor contributing to industry’s perceived US reserve deficiency? A.Vague Accounting Terms and Guidance B.Corporate Governance Issues (Dominance Risk) C.Quality and/or Clarity of Actuarial Conclusions D.Earnings Pressure E.Unforeseeable events F.There isn’t a problem; Why are we wasting so much time on this topic?

C.Quality and/or Clarity of Actuarial Conclusions D.Earnings Pressure E.Unforeseeable events F.There isn’t a problem; Why are we wasting so much time on this topic .")

47

The following factors have been suggested as potential contributing factors to the perceived decline in the reputation of casualty actuaries with respect to the actuary’s role in determining appropriate reserve levels and in evaluating the reasonableness/adequacy of reserves recorded by management. In your opinion, what is the most significant factor contributing to the perceived decline in the reputation of casualty actuaries with respect to reserves? A.Lack of clarity on what the actuarial estimate means B.Need for further refinement of actuarial models C.Inexperience of the appointed actuary D.Insufficient or ineffective communication by the actuary to management and/or Audit Committee/Board E.“Reasonableness” standard allows the actuary to sign off on reserves that he/she believes likely may be deficient F.Accounting standards need to be revised to minimize adverse reserve emergence G.Other

48

Agree or Disagree? Clarifying the term “best estimate” and differentiating the actuarial point estimate from management’s recorded “best estimate” will help to provide increased clarity with respect to the actuary’s conclusions on reserves. The Actuarial Standards Board should consider a revision to ASOP 36, requiring that the carried reserve be at least equal to the actuary’s estimate of the indicated reserves in order for the reserves to be considered reasonable.

49

Agree or Disagree? Management of public companies is more likely today to record at its actuary’s point estimate, due to the Sarbanes Oxley Act requirement for public companies to document and test the adequacy of their internal controls. Most actuaries today develop a point estimate for the reserves, whether or not that point estimate is displayed in the actuarial report.

50

Agree or Disagree? Public disclosure of differences between the actuary’s point estimate and management’s recorded reserve likely will place additional pressures on the actuary to change his/her estimate. A procedure for periodic, independent peer review of actuarial workpapers supporting the statements of actuarial opinion, with formal reports of the peer reviewer’s conclusions and/or observations to be made either to the regulator or to an independent actuarial review board, should be implemented.

Similar presentations