Download presentation

Presentation is loading. Please wait.

1

A Presentation for the European Real Estate Society Annual Conference Stockholm, 2009 Qiulin Ke* and Michael White** *Nottingham Trent University, Nottingham **Heriot-Watt University, Edinburgh

2

Motivations for the research There is a rich body of literature on office market analysis in western developed economies such as the US and UK. Limited empirical studies on emerging markets such as Shanghai, though they have experienced rapid growth and attracted global capital.

3

Research objectives: Extend analysis of Shanghai office market to examine submarket behaviour To identify Long run relationships Short run rent adjustment and Interaction between Shanghai office submarkets Does disequilibrium in one submarket affect other submarkets? Is there convergence in rental performance between submarkets?

4

Literature and methodology Grigsby (1963 and 1987) defined sub-markets in terms of the “close substitutability” of dwellings and properties within submarkets should be more “similar” than properties across submarkets Property market is segmented into two distinct categories, spatial and structural. Hedonic model applied in office market research (e.g. Glascock, et al.1990 and 1993; Mills, 1992; Wheaton and Torto, 1994; Bollinger et al. 1998), with submarkets denoted by dummy variables. These studies failed to test substitutability across submarkets. Stevenson (2007) adopted error correction modelling to examine the rental adjustment in four submarkets in central London and modelled the interactive effects among the submarkets.

, with submarkets denoted by dummy variables. These studies failed to test substitutability across submarkets. Stevenson (2007) adopted error correction modelling to examine the rental adjustment in four submarkets in central London and modelled the interactive effects among the submarkets..")

5

Methods of Analysis Long-run equilibrium model Short-run dynamic adjustment model Model linking error correction terms across submarkets Testing for Convergence

6

Shanghai Office Submarkets: Puxi and Pudong Source: DTZ Shanghai Nanjing Road West Huaihai Road People’s Square Lujiazui, Pudong Huangpu River

7

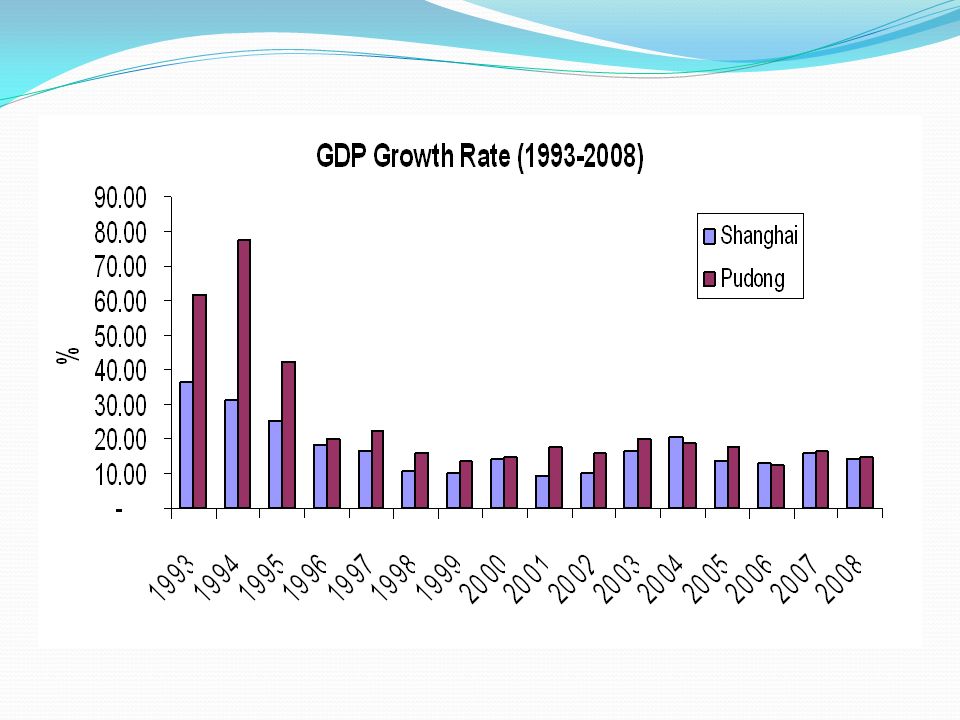

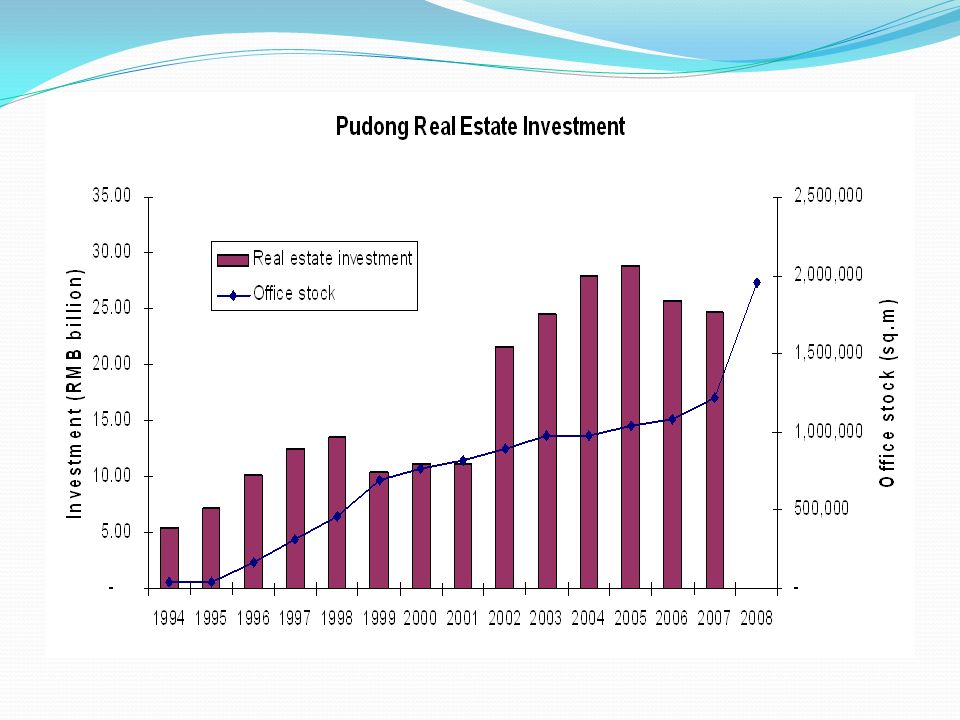

Central Puxi submarket Traditional CBD. Multi-national companies regional headquarter office and large professional services companies’ location. Representing 30% of total Grade A Shanghai office stock. Lujiazui, Pudong submarket Emerged since 1990 and was driven by government planning and development strategy to build it as Financial and Trade Centre of China Over 500 financial institutions settled there. Representing 30% of total Grade A Shanghai office stock.

10

Real Rents in Puxi and Pudong Source: DTZ, Shanghai

11

Vacancy rate in Puxi and Pudong Source: DTZ, Shanghai

12

Long Run Models

13

Short Run Models

14

Market Convergence Is there any evidence that the submarkets are converging in terms of rental performance? Consider relative rent as a function of a long run equilibrium differential and deviations around this. Rents converge if the deviations are non -permanent. The test takes the following form:

15

Test for Convergence

16

Conclusions We find no interaction between the two submarkets in Shanghai. Cointegration tests do not support evidence of a valid long run relationship in Pudong. We did not find convergence in rental performance between the two submarkets. These findings may be due to the shortness of the time series available and or be due to differences in the submarkets that imply a lack of substitutability for office occupiers.

Similar presentations

Fred Joutz (George Washington University) September.>")