Download presentation

Presentation is loading. Please wait.

1

Great Decisions 2009 By Dr. Amy F. Blizzard Planning Program, Department of Geography East Carolina University

2

An introduction to global energy use

3

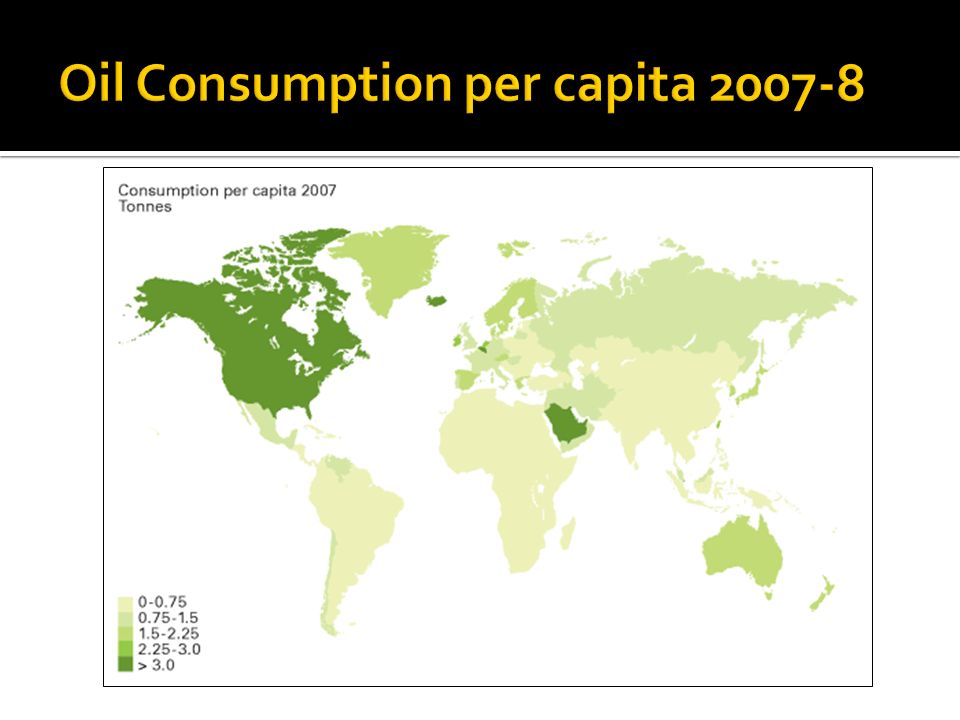

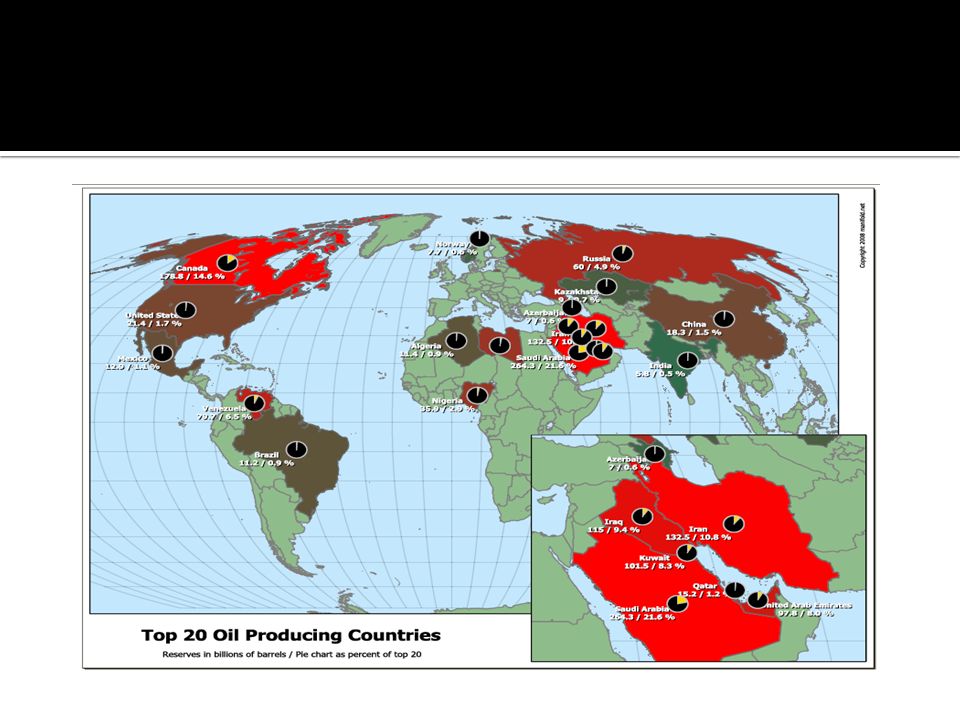

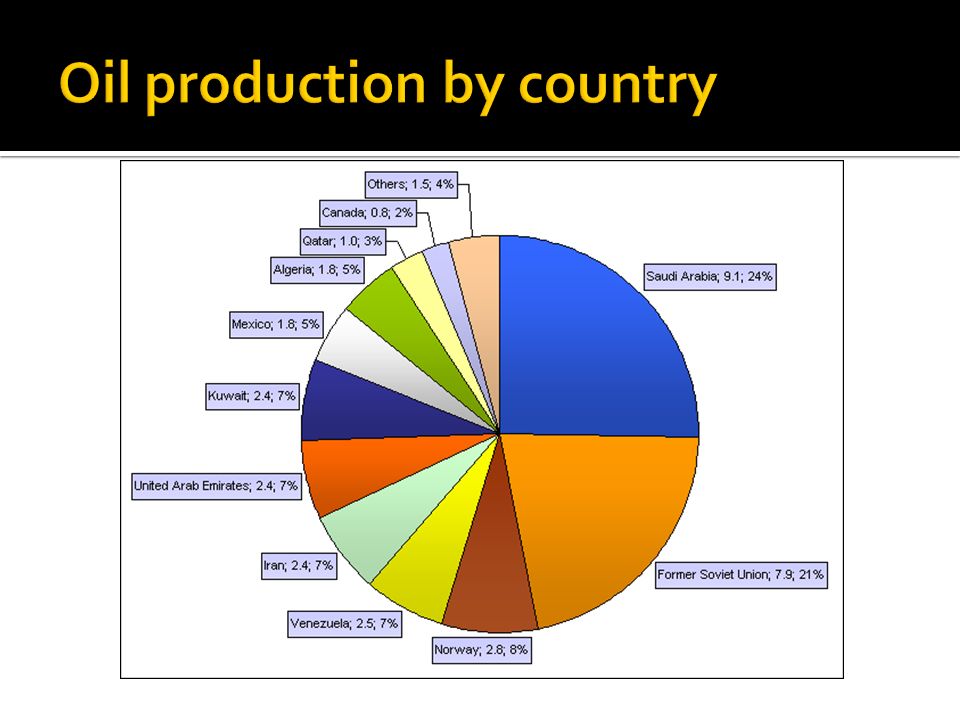

Source: BP Statistical Review of World Energy, 2008

5

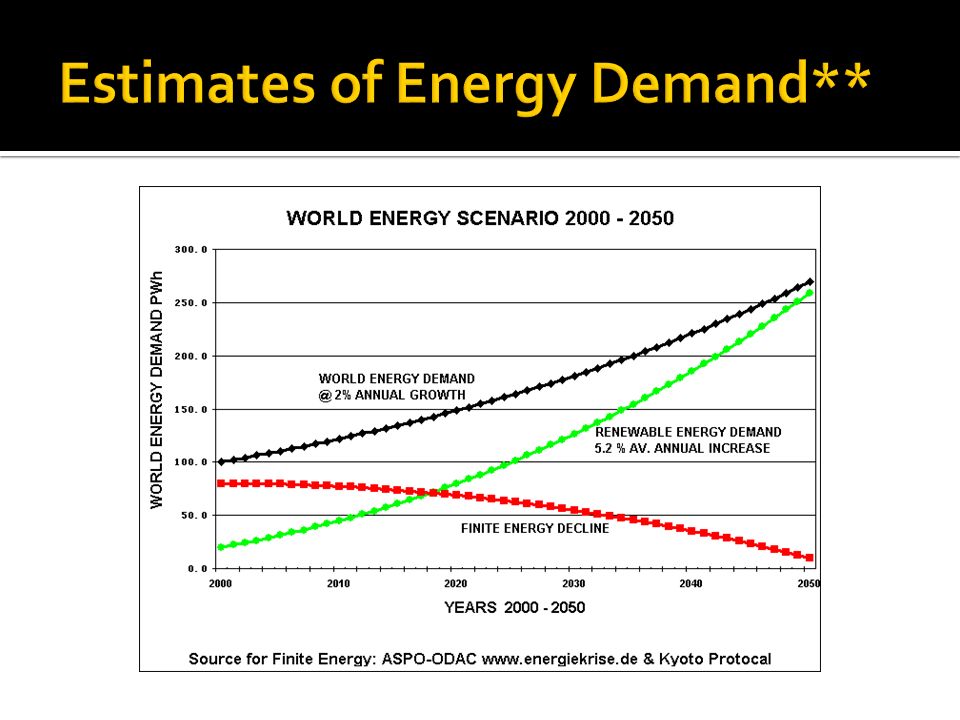

Total world consumption of marketed energy is projected to increase by 50 percent from 2005 to 2030. The largest projected increase in energy demand is for the non-OECD economies.

7

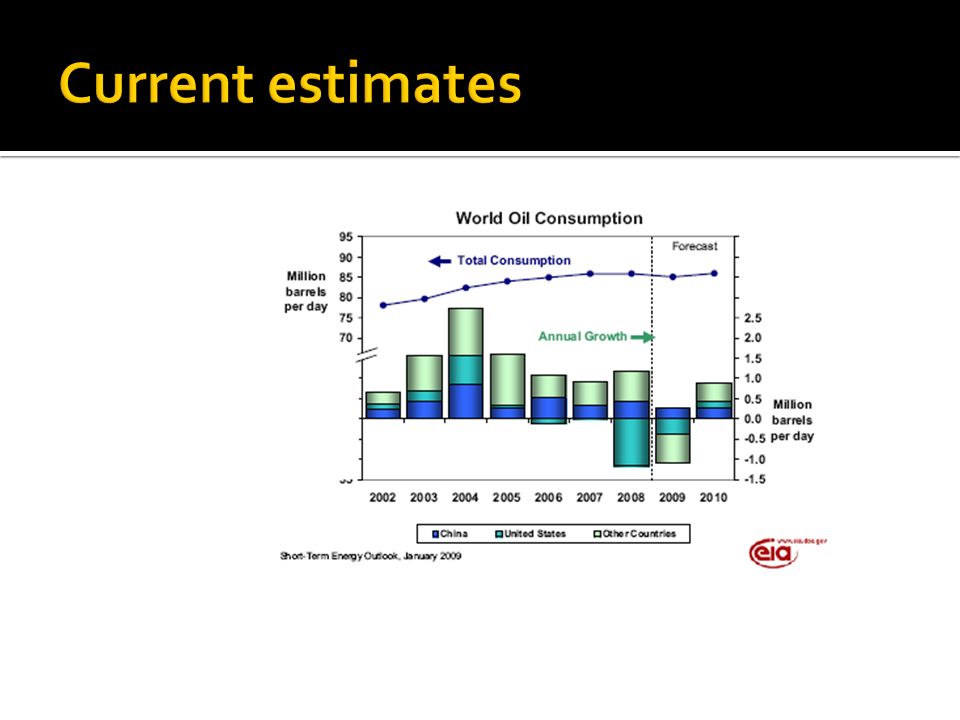

Oil demand declined in 2008 Demand for oil declined 300,000 barrels a day in 2008 and will fall by another 500,000 Global GDP growth has been roughly halved to 1.2 per cent Supply is increasing, demand is decreasing

9

Energy and the GDP Energy and food Energy and government services

13

A standard measure of national economic health Usually measured as a comparison (%) GDP - total cost of all finished goods and services produced within the country in a stipulated period of time (usually a 365-day year) GDP = C + I + G + (X − M)

GDP - total cost of all finished goods and services produced within the country in a stipulated period of time (usually a 365-day year) GDP = C + I + G + (X − M)")

15

Overall power of countries to invest declines Less private investment Less credit extended Developing regions affected more directly Less employment opportunities in the developed world Remittances and other transfers into developing regions

17

When GDP falls, and investments decline, leads to a decline in the Consumer Price Index November 2008- greatest decline (1.7%) since we started keeping records in 1947 Deflation may mean lower costs, but is generally bad for the economy So why are food costs still so high???

since we started keeping records in 1947 Deflation may mean lower costs, but is generally bad for the economy So why are food costs still so high")

19

Since the financial crisis, 40 Million people were added to the ranks of the malnourished. 963 Million people now considered hungry. 907 million - live in developing countries, 65 percent live in only seven countries: India, China, the Democratic Republic of Congo, Bangladesh, Indonesia, Pakistan and Ethiopia.. In sub-Saharan Africa, one in three people - or 236 million (2007) - are chronically hungry

- are chronically hungry.")

20

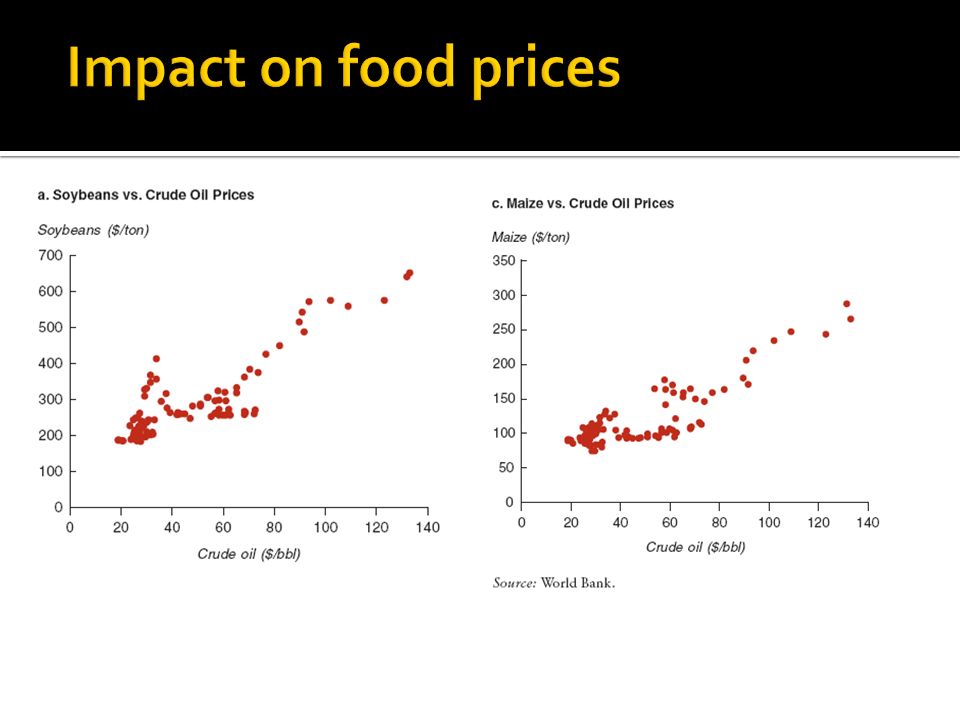

Food costs are dependent on energy and other commodity prices. Food is also subject to credit/investment to farmers and for markets Food is also at the mercy of mother nature Landless and powerless suffer the most

21

Tax reductions in fuel and food to offset higher prices Increased spending on subsidies and income support December 2008 IMF Survey of 161 countries: 575 reduced taxes on food 27% reduced taxes on fuels 20% increased food subsidies 22% increased fuel subsidies

23

GDP in East Asia and the Pacific increased 8.5% Rising oil and food prices boosted median inflation in the region to 9 percent in 2008 Prospects for 2009 and 2010 have dimmed with the deterioration in the external environment. Private sector investment in particular stands at risk. Decline in oil and food prices will support external positions and provide some relief on the inflation front, but…

24

GDP growth in South Asia eased to an estimated 6.3 percent in 2008 Deterioration in trade balances, however, has been offset in large part by large remittance inflows, particularly for Bangladesh, Nepal, and Sri Lanka, where remittances represent 8 percent of GDP or more. The global financial crisis is placing further downward pressure on growth. Food and fuel price subsidies have pushed fiscal outlays higher, reversing recent progress in fiscal consolidation.

25

In Europe and Central Asia, output is likely to increase by 5.3 percent in 2008 (but a downward trend) Deteriorating external positions and new risks from the global banking crisis are likely to depress prospects for vulnerable countries, and the downside risks are substantial. Most countries have experienced strong growth in domestic demand, but net trade has remained a drag on growth. Medium-term outlook points to a sharp decline in regional growth.

26

2008 headline inflation jumped in response to higher oil and food prices, and policy makers in countries such as Brazil and Chile raised interest rates. Gross capital inflows to the region compressed by 45 percent between January and September 2008, compared with the same period in 2007. GDP growth in the region is expected to drop to 2.1 percent in 2009

27

Developing countries of the Middle East and North Africa represent wide extremes in their economies Exports slowed in 2008 as growth turned sluggish among key trading partners in Europe and the United States. The region’s oil exporters will face the challenge of diminished revenues in 2009. For the region’s oil-importing economies, lower energy prices will reduce the import bill and provide some breathing space on the inflation front.

28

GDP Growth in Sub-Saharan Africa, outside of South Africa, increased 7 % in 2007 GDP advances have become more broad-based and less volatile in recent years, especially among oil importers. outside of South Africa remained strong at 6.6 percent as GDP gains among oil-producing countries eased moderately to 7.8 percent, joining the larger group of oil-importing countries where GDP gains slowed to 4.2 percent in the year. The region’s growth is expected to decline to 4.6 percent in 2009

30

Roller Coasters Rides, Rough Seas, and Dark Skies Hold on Folks, its going to get bumpy!

31

World trade volumes are expected to contract in 2009 for the first time since 1982. The global credit crunch is likely to affect private investment especially, which is the most cyclical and most internationally traded component of GDP. No one vision of where this will take us

32

As credit dries up, export receipts are more difficult to insure Combined with slowing demand = slowing exports Trickle across(?) Effect - countries that experienced a slowing of exports because of low U.S. demand growth benefited from higher commodity prices ( but this is inflation) More gradual building in the economic slowdown, but has not peaked yet

More gradual building in the economic slowdown, but has not peaked yet.")

33

Higher commodity prices have raised the current account deficits of many oil-importing countries to worrisome levels. International reserves of oil-importing developing countries are now declining as a share of their imports. Moreover, inflation is high, and fiscal positions have deteriorated both for cyclical reasons and because government spending has increased to alleviate the burden of higher commodity prices.

34

Globally, GDP growth is expected to improve in 2010. Many economists see this as a necessary correction, so now the PPP will increase in developed and developing nations May actually help us to reduce consumption and invest in the planet.

35

What is the role of US Energy Policy? Increase Supply or Lessen Demand? Cornucopian or Neo-Malthusian? What is the role of fuel subsidies for the current economy? How do we address declines in tax revenue due to declined demand? Should the US look to foreign sources as a way to boost the commodity? Or… Should the US look to domestic sources to improve the industry ?

36

For thoughts, questions, criticisms and ideas: Dr. Amy Blizzard, AICP Assistant Professor Planning Program, Department of Geography East Carolina University Greenville, NC 252-328-1270 Email: blizzarda@ecu.edu

Similar presentations

Muthanna Investment Company (MIC)>")