Download presentation

Presentation is loading. Please wait.

1

D’Ann Johnson Director © 2015 Texas C-BAR

2

* Dinner with silent auction * Garage sales * Raffles * Travel tour * Web sales

3

* Is the organization: * Properly registered? * Reporting donations to the IRS? * Providing the proper acknowledgments to donors? * Generating income from a business venture? * Paying taxes on the income? * Complying with state laws?

4

* Soliciting from the general public * Creative fundraising * Raffles/gambling * Sales taxes * Events * Federal tax issues * Donations * Earned income/UBIT * Special donations * Funding diversity/disclosure

6

* Sales taxes * Health permit * Alcohol permit * Child care permit * Liability for injuries

7

* Does a nonprofit have to pay taxes on the entrance fee in a charity golf tournament?

9

* Amusement Services/participatory sports * Circuses, live performances, motion pictures, antique or craft shows, rodeos, bowling, boxing, boat excursions, swimming pools * Publications by the NP, Passbooks * Auctions, Rummage Sales, and Other Fundraisers * Two, one-day (24 consecutive hours), events per calendar year * College or University student organizations can hold a one day, tax-free sale each month.

, events per calendar year * College or University student organizations can hold a one day, tax-free sale each month.")

10

Maybe. Food, bottled water, soft drinks, and candy are not subject to sales tax if: ◦ Served by schools, PTA’s; ◦ Sold by church or at church function; ◦ Served to permanent resident of retirement community; ◦ Served by prison or hospital; ◦ Sold by nonprofit devoted to education, religious, or physical training.

11

* But, sodas will also be taxable if served in a cup or with a straw, even if they fall within one of the prior exemptions.

12

* No. But, food IS TAXABLE if sold or packaged for IMMEDIATE CONSUMPTION and * Heated * Unheated if heating facilities are provided * Utensils included * 2+ food ingredients mixed or combined * Sold at a concession stand

13

No tax required on bread, rolls, bagels, doughnuts, cakes, pies, cookies, pretzels, tortillas as long as sold without plates or eating utensils. No tax on cookie dough, pizza kits, cheese spreads, meat sticks, jelly, salsa, and mixes packaged for preparation at home.

14

* Washing Cars * Coupon Books * Boxes of fresh fruit * Puppies at an animal shelter * Book Fairs * Cake Sales (whole, without utensils) * Cookbooks (if organization publishes and distributes the book itself)

* Cookbooks (if organization publishes and distributes the book itself)")

15

Since they are heated, sales tax collection is required. Does FIF need a health permit? Permits may be needed for food sales, and local authorities may conduct inspections if a temporary food establishment permit is required.

16

* Yes, unless this is one of the tax-free day sales. * NPs should not call sales donations to avoid paying sales taxes.

17

* Yes. Alcohol sales are subject to sales tax. * Permits are required for alcohol sales. A nonprofit may obtain up to 10 temporary permits in one calendar year at a cost of $50 each with a surcharge of $201. www.tabc.state.tx.us.www.tabc.state.tx.us * Ten days after the event, file a report with TABC on the amount of beer sold. * What if you give the beer away? * Since it is a ticketed event, FIF should obtain a permit and have a licensed bartender.

18

A person or entity may purchase items to donate to an exempt entity without paying sales tax. Complete a donor ’ s sales and use tax exemption certificate on back of Form 01-339.

19

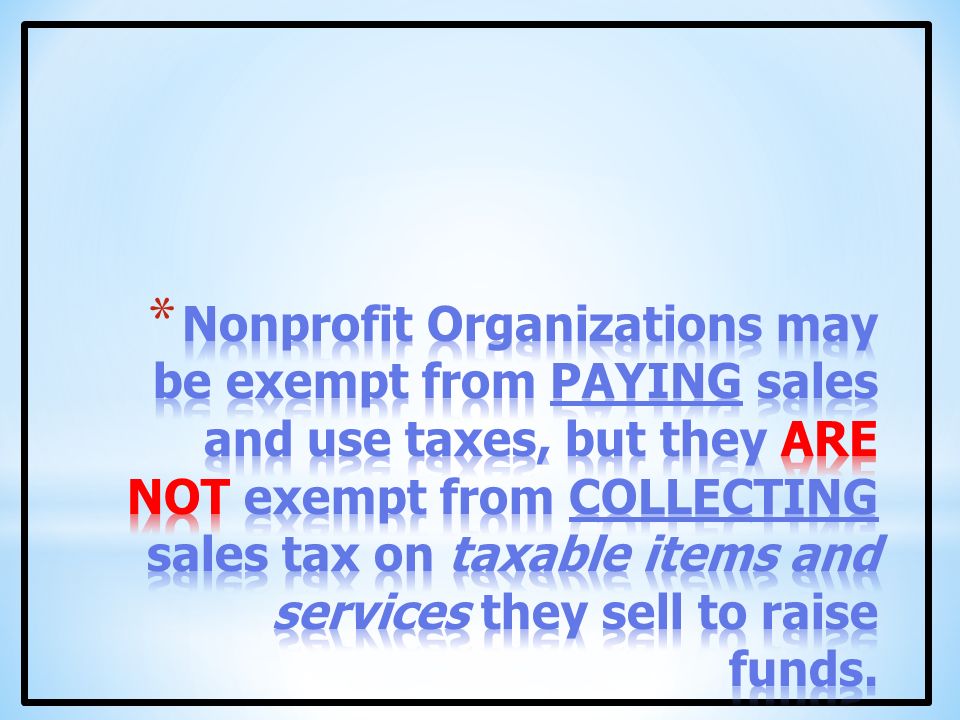

* Obtain Sales and Use Tax Permit * Collect the Correct Amount of Tax * Sales price of taxable item * Sales Tax Rate * Sales tax rate = 6.25% + Supplemental tax * Keep Accurate Records * File Returns * Submit Collected Taxes

20

* Selling without Permit * Class C Misdemeanor; 3rd conviction: $4000 fine & 1 year in jail * Knowingly Altering /Failing to Keep Accurate Records * Third Degree Felony * Failure to File Returns or Submit Taxes * Comptroller can estimate tax liability and/or suspend sales and use tax permit * Collection Actions, Penalties, Liens, Property Seizure, and Criminal Charges

21

Permits may be needed for food sales. Local authorities may conduct inspections if a temporary food establishment permit is required. Permits are required for alcohol sales. Permits are required to close streets for fun runs.

22

* The state does not mandate minimum health and safety standards for gatherings of less than 5,000 people. * Local ordinances may establish standards. * For over 5,000, the host must have: * one water outlet for every 100 people; * two toilets-gender marked-for every 50 people; * trash cans emptied twice a day; * 50 square feet per person; * 70 decibel limit on sound.

23

* Yes. * A nonprofit can provide short term child care without obtaining a permit if the care is not offered more than two days a week, is less than 24 hours a day, and is not part of an ongoing program that is required to be licensed. * FIF should screen any volunteers helping with children.

24

* Check general liability policy. * Consider purchasing special event insurance.

26

* Raffle laws * Solicitation and registration laws * Federal income taxes * IRS rules on vehicle donations

27

CREA defines a raffle as: “the award of one or more prizes by chance at a single occasion among a single pool or group of persons who have paid or promised a thing of value for a ticket that represents a chance to win a prize.” A charitable organization must be in existence for at least three years. Proceeds from raffle must be used for charitable purposes.

28

* Yes, but value and whether car is donated are issues. * Can offer any prize, except money. If nonprofit purchases a prize, its cost cannot exceed: * $50,000 for personal property or * $250,000 for a residential dwelling. No value limit on prizes donated to the organization. Texas lottery tickets may be offered as prizes. The organization must have each prize in its possession or ownership or post a bond for the full value with the county clerk of the county where the raffle will be held.

29

* Donor should provide an appraisal (form 8283)for the new vehicle. * The deduction for a motor vehicle, boat or airplane donated to a charity is usually limited to the gross proceeds from its sale if claimed value is greater than $500. * Exemptions: * Significant use by nonprofit. * Material improvement by nonprofit * If sold below-market rate to provide access for transportation for a low-income person. * Form 1098-C or a similar statement must be provided to the donor by the organization and attached to the donor’s tax return.

30

* No. CREA has very specific requirements that the following be printed on the tickets: * The name of the organization conducting the raffle. * The address of the organization or of a named officer of the organization. * The ticket price. * A general description of each prize with a value greater than $10. * The date on which the raffle prize(s) will be awarded.

will be awarded..")

31

* Only members of the organization or persons authorized by the organization may sell tickets. * No one may be compensated directly or indirectly for organizing or conducting a raffle or for selling raffle tickets.

32

Federal law makes it a crime to knowingly deposit in the mail material concerning a scheme offering prizes dependent on chance, which applies to raffle tickets. The penalty is a fine and imprisonment for up to two years. Subsequent violations includes imprisonment up to five years. Apparently you can send advertisements, but not tickets.

33

* Yes. A qualified organization may hold two raffles per year and but only one raffle at a time. * TAT can raffle a Mercedes for $50k and a boat for $35K in one raffle.

34

* Unauthorized Raffles are considered gambling under the Texas Penal Code * Conducting an unauthorized raffle is Class A Misdemeanor * (1) a fine not to exceed $4,000; * (2) confinement in jail for a term not to exceed one year; or * (3) both such fine and confinement. * Participating in an unauthorized raffle is a Class C Misdemeanor * a fine not to exceed $500.

35

* Texas Law Enforcement Telephone Solicitation Act * Certain law enforcement organizations that raise funds through telephone solicitation * Registration fee with AG and $50 fee * Commercial telephone solicitor must post $50,000 surety bond with SOS. * Public Safety Solicitation Act * Certain public safety organizations. * Public safety publications and their solicitors, and Promoters must register, pay fee, and post a bond. * Veteran’s Solicitation Act * Certain organizations must register and pay fee * Professional solicitors must post a surety bond.

36

Definitions vary by city and state. – Most cities and states regulate fundraising through solicitation laws. – Organized around comprehensive reporting by nonprofits and professionals fundraisers they engage to solicit funds. Usually broadly defined. Examples: – Letters – Phone calls – Newspaper ads requesting financial assistance – Email messages requesting contributions

37

* Work sites-special rules related to public employees. Charity must not have made an election under 510 (h) - Sec. 572.060 Government Code * Solicitation by pedestrian-local authority may regulate and require a written application, charge a fee, and require insurance. Ch. 552 Transportation Code.

- Sec Government Code * Solicitation by pedestrian-local authority may regulate and require a written application, charge a fee, and require insurance. Ch. 552 Transportation Code..")

38

Yes. TAT must withhold the taxes if the value of the prize exceeds $5,000. TAT should obtain a W-9 and Form 5754 from the winner and file an IRS Form 945 and W-2G. Officers and employees maybe personally liable if they do not withhold taxes. TAT must report raffle prizes on Form W-2G if a the prize is $600-5000 and is at least 300 times the amount of the raffle ticket.

39

Regular gambling withholding for cash and non cash prizes over $5,000 = 25% Back-up withholding for prizes over $600 if the winner will not provide a correct tax ID= 28%

41

Gambling if: ◦ A fee is charged to play; ◦ Winner decided by game of chance; and ◦ Prizes are awarded to the winner with the best hand. Private residence exception if no house cut.

42

Casino nights where entry fee charged and door prizes given-not related to winning hands Entry fee charged and get sponsors Entry fee charged and sell food and drink

43

Texas Live Music Trail wants to hold a gala event and dinner at a downtown hotel with a Willie Nelson performance, a live and silent auction, and gift bags. Individual tickets will be $125. They also want to have corporate sponsorships, sell chances for a cash prize, and have an independent contractor make calls to sell tables.

44

* Copyright * Federal taxes * Sales taxes * Raffle laws * Auctioneer restrictions * Solicitation and registration laws

45

Copyright protection attaches when the work is created. Protection also applies to derivative works. There is no need for creator to register. Works are protected for life of author plus 70 years.

46

Question whether work for hire. Job description for creative positions should indicate that brochures, photos, or other creative works are property of organization. Use of copyrighted materials is not excused because organization is a nonprofit.

47

Yes. Federal tax law applies if a person receives a benefit. The invitation should clearly state the amount of ticket price that qualifies as a charitable deduction. ($75) Provide the donor with a good faith estimate of the goods or services. ◦ Cost of dinner ($25) ◦ Good faith estimate of concert ($25) ◦ Cost of gift bag items ($0)

Provide the donor with a good faith estimate of the goods or services. ◦ Cost of dinner ($25) ◦ Good faith estimate of concert ($25) ◦ Cost of gift bag items ($0).")

48

* The goods or services given to a donor have insubstantial value - See Revenue Procedures 90-12 and 92-49 * FMV of Token items less than 2% of donation or $102, whichever is less; * Logo items cost less that $10.50 if donation of at least $52.50; * Unsolicited merchandise (e.g. address labels). * There is no donative element involved * Visitor’s purchase from museum gift shop

. * There is no donative element involved * Visitor’s purchase from museum gift shop.")

49

* A penalty is imposed on a charity that does not make the required disclosure of a quid pro quo contribution of more than $75. * The penalty is $10 per contribution, not to exceed $5,000 per fundraising event or mailing. * The charity can avoid the penalty if it can show that the failure was due to reasonable cause.

50

* No. * Selling chances is a raffle. * CREA allows any raffle prize except money.

51

Money means “coins, paper currency or a negotiable instrument that represents or is easily convertible to coins or paper currency”. Money includes: – a certificate of deposit, – money orders, – travelers’ checks, and – cashier’s checks. Money does not include: – a prepaid credit card or – a savings bond.

52

Yes. There are no special registration requirements for professional fundraisers in Texas unless they are making calls on behalf of veterans, or law enforcement and public safety organizations.

53

Charitable pledges may be enforceable under state contract law if the elements of offer, acceptance, and consideration are met. Directors may owe a fiduciary duty to pursue collection of legally enforceable pledges.

54

Donors are required to obtain a written acknowledgement of contributions over $250 for federal income tax purposes. The acknowledgment should contain: ◦ Name of nonprofit; ◦ Amount of contribution or description; and ◦ Whether any goods or services were provided in return for the donation.

55

* To deduct a charitable donation of money, a taxpayer must have a bank record or a written communication from the charity showing: * The name of the charity * Date and amount of the contribution * Bank record includes canceled checks, bank or credit union statements and credit card statements.

56

* Yes. * An organization may pay a licensed auctioneer a reasonable fee for conducting the auction. * However, the fee may not exceed 20 % of gross receipts.

57

A nonprofit can auction alcohol if they obtain a temporary permit from TABC. The permit currently costs $25 and is limited to one a calendar year. The auction can only be held in a location where the alcohol could be sold or served. The alcohol must be donated. The organization must notify the nearest office of TABC of the details of the event. No person may be compensated for assisting with the auction or securing the alcoholic items for auction.

58

Yes. But you may simply describe the donation and the amount it garnered at the auction. If donor submits IRS Form 8283, file 8282 upon sale. Donors need contemporaneous written acknowledgement.

59

* Since 1969, artists may deduct only costs-not FMV. * Art collectors/estate may deduct FMV.

60

IRS Publication 526 – Charitable Contributions – http://www.irs.gov/pub/irs-pdf/p526.pdf http://www.irs.gov/pub/irs-pdf/p526.pdf IRS Publication 561 – Determining the Value of Donated Property – http://www.irs.gov/pub/irs-pdf/p561.pdf http://www.irs.gov/pub/irs-pdf/p561.pdf

62

Check state laws. 39 states regulate solicitation; 35 states accept a uniform registration form (URS). – Requirements vary, but most require: Registration required before solicitation begins. Annual reporting with an emphasis on fundraising outcomes and practices. Disclosure to potential donors about where to find more information or file complaints. Nonprofits that comply as soon as notified by AG’s office will often be given a grace period. Cost is approximately $1500-3000.

. – Requirements vary, but most require: Registration required before solicitation begins. Annual reporting with an emphasis on fundraising outcomes and practices. Disclosure to potential donors about where to find more information or file complaints. Nonprofits that comply as soon as notified by AG’s office will often be given a grace period. Cost is approximately $")

63

* What legal issues should Model Train Foundation consider if it wants to start operating daily train trips to raise money?

64

Nonprofits are prohibited from ongoing commercial or business activities that benefit an individual interest. However, nonprofits must be profitable or they will be out of business and unable to carry on their charitable mission!!!!

65

Will the nonprofit be subject to additional taxes for unrelated business income (UBIT)? Is the organization likely to lose its tax exempt status due to the type of activities the business will conduct?

66

A tax on all income over $1,000 generated from unrelated business activity. If such activity is substantial, a nonprofit can lose its tax-exempt status.

67

Usually not more than 15% of income or effort can be expended in an unrelated business activity but it is a very fact-specific determination.

68

An income-generating activity that is: ◦ Regularly carried on; ◦ Not performed entirely by volunteers; and ◦ Does not include the sale of donated merchandise.

69

Activities directly related to the mission; Activities indirectly related to the mission; or Activities not related to the mission. Those activities that are farther away from your mission are more likely to fail due to lack of expertise and to create problems with taxation.

70

A related business activity is related to the exercise of the nonprofit’s charitable purpose.

71

T5PB collects clothing in bins that are displayed throughout town. The clothing is picked up by a reseller that takes the clothing and resells them on both sides of the border. The nonprofit receives a per poundage fee for the items that it collects. Is this related or unrelated business activity?

72

* Review articles of incorporation and bylaws. * Review Form 1023 application to IRS.

73

How the income is earned; Fee structure; Nature and size of business(not larger than necessary to achieve goals); Population served; Scale consistent with charitable rather than profit- making purpose; and Whether the business operates like a for-profit business. ◦ operated to maximize charitable goals at the expense of commercial profit.

74

Goodwill thrift shops Girl Scout cookie sales Emancipet-low cost spay neuter services Travel tours-IRS guidance Advertising income on web-IRS guidance

76

There is no bright line between corporate sponsorship donations and advertising, but the difference is important. Corporate sponsorships are tax deductible to donor and NP is not taxed on funds. Advertising is unrelated business income to NP and a business expense rather than donation.

78

* Texas Attorney General has the authority to investigate and initiate legal action against charitable organizations, their directors and/or their professional fundraisers to ensure that charitable donations and assets are lawfully raised and expended * IRS can revoke tax exempt status for violation of federal laws.

79

Broad common law, constitutional, and statutory authority to oversee nonprofits General authority to inspect and examine corporate books and records Specific enforcement authority ◦ Bingo Enabling Act ◦ Charitable Raffle Enabling Act ◦ Solicitation: To Veterans and Public Safety Organizations and Via Telephone Authority to file actions against charities for violations of the Texas Deceptive Trade Practices –Consumer Protection Act

80

www.texascbar.org D’Ann Johnson 512-374-2760 djohnson@texascbar.orgjohnson@texascbar.org

Similar presentations

3s and Compliance For DCs and Treasurers. Pony Club – DC and Treasurer Training Organization and Structure USPC, Inc. is an IRS 501(c)(3) tax exempt.>")

CORPORATION REUBEN S. SEGURITAN 7 Penn Plaza, Suite 222 New York, NY 10001 Tel. No. (212)>")