Download presentation

Presentation is loading. Please wait.

1

Oil and Gas Industry: Encana & Penn West Beijing Mu Lihua Li Jason. Z. Fan Ben.Y.Fu Dingding Xu

2

Canadian Oil and Gas Industry Analysis Contents Industry Overview Oil Industry Gas Industry Interdependence bt Oil&Gas Risk Management

3

Industry Overview Energy Sector (all sources) contributed 5.9% to GDP in 2004. Of the $70.8 billion total energy GDP, crude oil and natural gas industries accounted for 78%; accounts for 2.3% of Canada ’ s GDP.

4

Industry Overview Important segment of Canada ’ s economy in terms of investment, trade and employment. Employment : Direct employment, excluding service stations and wholesale trade in petroleum products, was 240,827 people in 2004 or 1.5% of total employment in Canada. Investment: In 2004, new capital investments in energy-related industries represented 19.0% of total Canadian investment and 4.4% of GDP.

5

Industry Overview Trade (Exports) 1). Since oil prices bottomed out during the Asian crisis in 1998, the share of energy in exports has more than doubled from 7.3% to 16.1%. 2). In 2004, energy accounted for 17.5% of total merchandise exports, and the energy trade balance ranked first as a contributor to Canada's positive overall trade balance.

. In 2004, energy accounted for 17.5% of total merchandise exports, and the energy trade balance ranked first as a contributor to Canada s positive overall trade balance..")

6

Industry Overview The United States is Canada's major trade market for energy products Exports: Exports for energy products between US and Canada accounts for 99% ($66.7 billion) of all Canadian energy exports. Imports: In 2004, Canada imported $24.5 billion of energy products, mainly from the United States (28%), Norway (19%) and the UK (12%).

, Norway (19%) and the UK (12%)..")

7

Industry Overview Natural Gas: Canada exported 63% of natural gas ($27.0 billion) to the United States in 2004. In volume terms, Canada accounted for more than 84% of U.S. gas imports and had a 15% share of the U.S. market. Oil: The US accounts for 99% ($25.1 billion) of Canadian exported crude oil in 2004. In volume terms, Canadian crude oil held a accounted for more than 16% of U.S. crude imports and 14% share of the U.S. market in 2004.

of Canadian exported crude oil in In volume terms, Canadian crude oil held a accounted for more than 16% of U.S. crude imports and 14% share of the U.S. market in")

8

Canadian Oil Industry Production In 2004, Total Canadian production of crude oil averaged 3.1 million barrels per day. Reserve Canada has the s econd largest oil reserves in the world--179 billion barrels of proven reserve in 2005. Source: IEA

9

Canadian Oil Industry Exports: Nearly two thirds of Canadian crude oil is exported to the United States, accounting for 16% of total US crude imports. Canada is the largest crude oil exporter to the US.

10

Canadian Oil Industry Consumption Total oil demand in Canada averaged 2.29 million barrels per day in 2004. The transportation sector accounted for some 56% of this demand while 26% was attributed to industrial use. Source: IEA

11

Canadian Oil Industry Price (Demand&Supply Analysis) The growth in demand from emerging markets Oil supply control by OPEC member countries Conflict in the middle east storms and hurricanes

The growth in demand from emerging markets Oil supply control by OPEC member countries Conflict in the middle east storms and hurricanes")

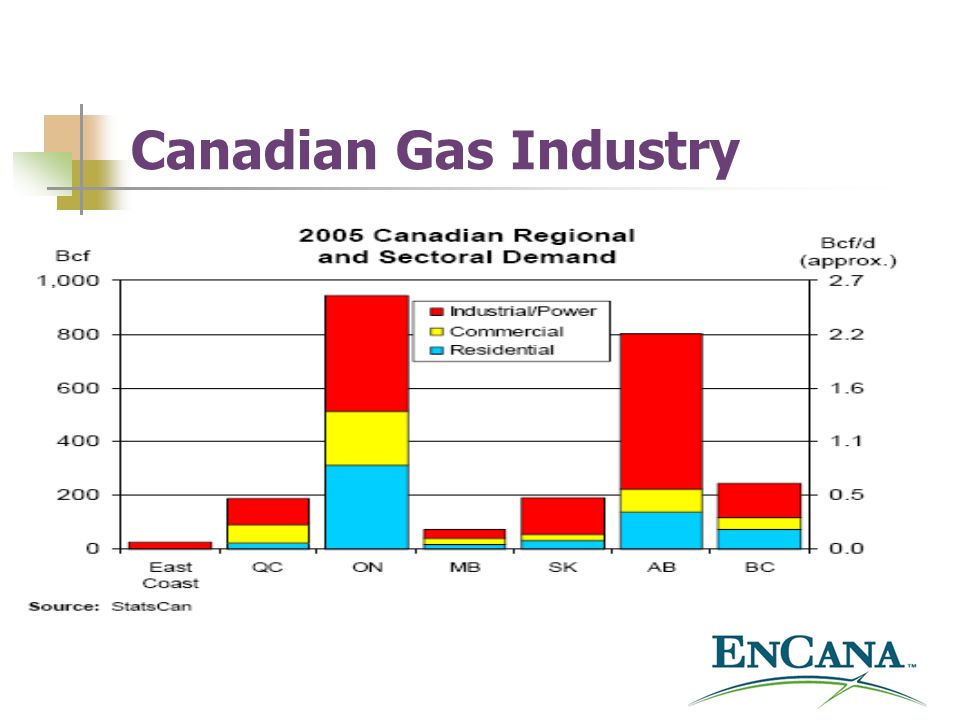

12

Canadian Gas Industry Canada is the world ’ s third largest producer of natural gas with annual production of 6.4 trillion cubic feet (tcf).

.")

13

Natural gas is the main source of energy for 51% of the manufacturing sector and 39% of the commercial sector. Division: Industrial sector 58%, residential sector 24% commercial sector 18%. Source: CGA Canadian Gas Industry

15

Demand: Natural gas industry meets 31% of Canada ’ s total energy demand, employs over 50,000 Canadians. Half between Eastern and Western Canada. Alberta leads the west in consumption while Ontario leads the east. Natural gas is the source of heating for 48% of Canadian homes. More efficient facility: natural gas water heater, natural gas clothes dryer and so on.

16

Canadian Gas Industry Exports: Canada is 2nd largest exporter in world About 50% or $20 billion worth of all natural gas produced in Canada is exported to the United States.

17

Interdependence of Natural Gas & Oil sands Oil sands operations require significant amounts of natural gas. Contrary to many industrial operations, oil sands demand for natural gas continues to increase despite higher natural gas prices.

18

Correlation between oil and natural gas prices

19

Global Oil Demand & Forecast Expected to grow by more than 50% in the next 20 years More than 50% are consumed by the transportation sector Emerging Asia, especially China is expected to more than double its demand in the next 20 years

20

Global Natural Gas Demand and Forecast

21

Risk Exposures Financial/Commodity Credit/Liquidity Operational Environmental/ Legal General Business

22

Risk Management Major Elements for risk management in oil&gas industry: Energy Futures traded in COMEX FX Futures traded in CME OTC Forward contracts (oil, gas, etc) Interest rate and FX SWAPS Options: Costless Collar

Interest rate and FX SWAPS Options: Costless Collar")

23

Risk Management Costless Collar A collar is a spread comprising a long (short) call and a short (long) put, both out-of-the-money and for the same expiration. A Costless Collar is where buying and selling respectively the related Call and Put are used to finance the Collar. A collar is usually set up with options, swaps, or by other agreements.

24

Risk Management Swap In general, Swap is the exchange of one asset or liability for a similar asset or liability for the purpose of lengthening or shortening maturities, or raising or lowering coupon rates, to maximize revenue or minimize financing costs. interest rate swap: An exchange of interest payments on a specific principal amount. This is a counterparty agreement, and so can be standardized to the requirements of the parties involved. An interest rate swap usually involves just two parties, but occasionally involves more.interest

25

Encana Agenda History and Background Management Team Company Overview Business Strategy Financial Analysis Risk Management Outlook

26

History and Background In 2002, merger agreement was reached between two energy companies: Alberta Energy (AEC) PanCanadian Energy (PCE) Alberta Energy is created by the government of Alberta in 1975 By 1993 Alberta government sold the entire ownership to make AEC as the public owned company By 1995, AEC put its growth strategy on oil and gas after selling off all other resource investment. By 2001, AEC has become the largest natural gas producer and also largest independent operator of gas storage.

27

History and Background PanCanadian was created by Canadian Pacific and gas company in 1958 PanCanadian roots go back to the construction of the nation first transcontinental railways Canadian Pacific Railways made natural gas discovery in 1883 and later create Canadian Pacific and gas company in 1958 which later create PanCanadian in 1973 In 2000, PanCanadian launches one of the continent largest CO2 miscible flood project at Weybury, Saskatchewan In 2002, Gwyn Morgan and David O’Brien announced the merger agreement between AEC and PanCanadian. Each AEC Share was converted to 1.472 PanCanadian Share. On April 8, Encana began trading on the TSX and NYSE under the symbol ECA. Its enterprise value now is around 52 billion.

28

Management team Gwyn Morgan, President & CEO Education : Northern Alberta Institute of Technology and University of Wyoming Key architect of the company North America ’ s resource play strategy More than 25 years of experience Served as Chief of Operating Officer before elected as CEO in January 1, 2006 John D. Watson,Executive Vice-President & Chief Financial Officer Education: He holds a BA from Concordia University in Montreal, an MBA from Queen's University. Responsible for EnCana's capital markets, financial reporting, financial compliance, financial risk management and internal audit, as well as the tax and treasury functions Been in EnCana for 30 years

29

Management team John D. Watson plans to step down on February 28, 2006, following completion of the 2005 year-end financial statements. Watson will remain with the company as Advisor to the Chief Financial Officer until the end of 2006. Brian C. Ferguson CA became Executive Vice-President & Chief financial Officer on March 1, 2006. Brian Ferguson, Executive Vice President & CFO Education : University of Alberta and University of Western Ontario Member of CICA, CICA ’ s risk management and governance board More than 22 years of experience

30

Company Overview Primary goal Target Strategic Focus Competitive Advantage

31

Company Overview Primary goal Continue to increase net asset value per share by balancing capital investment between: Disciplined development of resources play Share buyback

32

Company Overview Target An average 10% annual sales growth per share Strategic Focus North American natural gas Canadian in-situ oilsands

33

Company Overview Competitive Advantages Large land base with huge undeveloped resources Leading technical competencies 30 years of experiences with unconventional reservoir development Low operating cost High working interest and infrastructure control

34

Company Overview Mission Energy for People Vision EnCana will be the world's High Performance Benchmark independent oil and gas company. Our Shared Principle Strong character, ethical Behaviour, high performance, great expectation, dynamic discipline.

35

Business Strategies EnCana operates two continuing businesses: Upstream :exploration, development and production of natural gas, crude oil, and natural gas liquids ( “ NGLs ” ) and other related activities. Market Optimization: includes activities to enhance the sale of Upstream ’ s production.

36

Consolidated Financial Results

37

Cash flow

38

Cash Flow The increase resulted from: Average North American natural gas prices North American natural gas sales volumes increased Average North American liquids prices, excluding financial

39

Cash Flow The increase in cash flow was partially reduced by: Operating expenses increased Interest expense increased The current tax provision increased

40

Net earnings EnCana ’ s 2005 total net earnings were $3,426 million compared with $3,513 million in 2004: Net earnings from discontinued operations decreased from $823 million to $597 million EnCana ’ s 2005 net earnings from continuing operations were $2,829 million, an increase of 35 percent compared with 2004

41

Market Optimization

42

Stock Options Exercise prices approximate the market price for the Common Shares Fully exercisable after three years and expire after five years Expire up to ten years if it is granted under predecessor and/or related company replacement plans

43

Stock Option Summary

44

Risk Exposure Financial risks Operational risks Environmental, health, safety and security risks Reputational risks

45

Risk Management Philosophy EnCana partially mitigates its exposure to financial risks through the use of various financial instruments and physical contracts. EnCana does not use derivative financial instruments for speculative purposes.

46

Derivative Financial Instruments Forward Foreign Exchange Swaps Interest Rate Natural Gas Foreign Exchange Option Natural Gas Crude Oil

47

Commodity Price Risk Natural gas price risk Swaps Fix the AECO and Rockies price differential from the NYMEX price Collars and other options Company ’ s proprietary production management Crude oil price risk Fixed price swaps and call options Participation at higher WTI levels

48

Gains and Losses on Risk Management Activities Natural Gas

49

Gains and Losses on Risk Management Activities Crude Oil

50

Interest Rates risk Mix of both fixed and floating rate debt Partially mitigates its exposure to interest rate changes Interest rate swap Manage the fixed/floating rate debt portfolio mix.

51

Gains and Losses on Risk Management Activities Interest Rate Risk

52

Foreign exchange risk Forward exchange contract Mitigating the exposure to fluctuations in the U.S. to Canadian exchange rate Hedges its foreign currency exposures on foreign currency denominated long-term debt Hedge anticipated sales to customers in the United States Mix of both U.S. dollar and Canadian dollar debt Offset the exposure to the fluctuations in the U.S./Canadian dollar exchange rate Cross currency swaps Managing the U.S./Canadian dollar debt mix

53

CREDIT RISK & OPERATIONAL RISKS This credit exposure is mitigated through the use of Board-approved credit policies Limit transactions to counterparties of investment grade credit quality and transactions that are fully collateralized EnCana mitigates operational risk through a number of policies and processes. Projects are evaluated on a fully risked basis Lookback and Learning process Maintaining a comprehensive insurance program

54

Other Risks Regulatory environment risk The Kyoto protocol commits Canada to reducing greenhouse gas emissions to 6 percent below 1990 levels over the period 2008 – 2012. Reputation risks EnCana takes a pro-active approach to the identification and management of issues that affect the Company ’ s reputation and has established consistent and clear procedures, guidelines and responsibility for identifying and managing these issues.

55

Sensitivity analysis

56

Out Look Volatility in crude oil prices is expected to continue throughout 2006 as a result of market uncertainties over supply and refining disruptions on the U.S. Gulf Coast Continued demand growth in China, OPEC actions, demand destruction from high energy prices and the overall state of the world economies. Natural gas prices are primarily driven by North American supply and demand, with weather being the key factor in the short term. North American conventional gas supply has peaked in the past two years and EnCana believes that unconventional resource plays can offset conventional gas production declines.

57

PENN WEST Energy Trust

58

Introduction Penn West Energy Trust is the largest conventional oil and natural gas producing income trust in North America. Penn West ’ s production averaged 129,915 boe per day at December 31, 2006, of which just under half was natural gas. Based in Calgary, Alberta, Penn West operates in three core areas throughout the Western Canada Sedimentary Basin. Penn West is an actively managed trust with a large and diversified asset portfolio, experienced and specialized technical teams, and an extensive inventory of internal opportunities.

59

Penn West is an actively managed trust that reinvests a substantial proportion of operating cash flow to pursue new value through development of its asset base. The Trust conducts a substantial capital program funded by retaining a proportion of cash flow. In addition, Penn West ’ s extensive undeveloped lands (3.7 million net acres at the end of December 31, 2006) create a source of additional value through land monetization, farm-outs and exploration joint ventures. Introduction

create a source of additional value through land monetization, farm-outs and exploration joint ventures. Introduction.")

60

Penn West ’ s management team is committed to a strategy of distributions stability and maximizing value for unitholders over the long term. The management team has a 15-year track record of operational and financial success. This includes accretive acquisitions and consistent financial discipline. In 2006, Penn West had a budgeted $400-500 million capital program to pursue capital efficient opportunities that levered existing Trust infrastructure including: field optimization, suspended well reactivations, plant consolidation, well stimulations and recompletions, and low risk infill drilling, down spacing and horizontal drilling.

61

Advantages Large Scale Financial Strength (including access to capital and strong balance sheet) High quality diversified producing assets Extensive management team experience Depth in employee knowledge both in the field and head office

High quality diversified producing assets Extensive management team experience Depth in employee knowledge both in the field and head office")

62

As the largest conventional oil and natural gas producing trust in North America, Penn West has a high quality base of production and long life reserves diversified by geography, size, capital intensity, commodity and play type. Penn West ’ s large scale mitigates risks and contributes to stability and sustainability. 99,807 boe /day 360 mm boe A V E R A G E D A I L Y P R O V E D P R O D U C T I ON + P R O B A B L E R E S E R V E S Big Energy

63

Penn West is an actively managed trust that reinvests a substantial proportion of operating cash flow to pursue new value through development of its asset base. That means Penn West ’ s people are key to maintaining and adding value for unitholders. 327 381 Head Office Staff Field Staff Big People

64

Penn West ’ s high quality asset base generates the cash flows needed for the Trust to meet its distributions target. Distributions per unit have increased by 30 percent since the Trust ’ s inception, to a rate of $0.34 per unit, effective for our February 2006 distribution. 36.2% $0.34 2005 Return on Monthly distribution Capital employed Per unit Big Value

65

As an exploration and production company, Penn West Petroleum Ltd. delivered growth in production, reserves, cash flow and share price to create shareholder value. As an energy trust, Penn West focuses on maintaining value for unitholders over the long term. Performance means sustainable production, reserves, cashflow and distributions. Big Performance

66

Big Future Penn West’s asset base is diversified by commodity, geographical region and risk profile. Cash flow maximizing oil and natural gas properties are balanced by longer life properties with lower declines. Penn West’s extensive inventory of internal opportunities includes short term exploitation and optimization, medium term development drilling, and long-term enhanced recovery and oil sands projects. 9.9 ye a r s 4.1 mi l l ion ne t a c re s Reserve Life Undeveloped land

67

Financial Profile

68

Strong Balance Sheet

69

Operational Profile

70

Property Overview

71

Strong Production Base

72

Risk Analysis The Trust is exposed to normal market risks inherent in the oil and natural gas business, including credit risk, commodity price risk, interest rate risk and foreign currency risk. The Trust, from time to time, attempts to minimize exposure to these risks using financial instruments.

73

Risk Analysis-Credit Risk Credit risk is the risk of loss if purchasers or counterparties do not fulfill their contractual obligations. All of the Trust ’ s receivables are with customers in the oil and natural gas industry and are subject to normal industry credit risk. In order to limit the risk of nonperformance of counterparties to derivative instruments, the Trust transacts only with financial institutions with high credit ratings and obtains security in certain circumstances.

74

Risk Analysis- Commodity Price Risk Commodity price risk is the Trust ’ s most significant exposure. Crude oil prices are influenced by worldwide factors such as OPEC actions, supply and demand fundamentals, and political events. Natural gas prices are generally influenced by oil prices and North American natural gas supply and demand factors. Pursuant to policy, the Trust may, from time to time, manage these risks through the use of costless collars or other financial instruments up to a maximum of 50 percent of sales volumes. The Trust maintains an active hedging program. Other financial instruments include Alberta electricity contracts with positive mark- to-market values.

75

Risk Analysis-Interest Rate Risk The Trust maintains its debt in floating-rate bank facilities, resulting in exposure to fluctuations in short-term interest rates. From time to time, the Trust may increase the certainty of future interest rates by using financial instruments to swap floating interest rates for fixed rates or to collar interest rates. The Trust had no financial instruments in place at December 31, 2005 that affected its future interest rate exposure.

76

Risk Analysis-Foreign Exchange Rate Risk Prices received for sales of crude oil and certain bank loans are referenced to, or denominated in, US dollars. Accordingly, realized oil prices, interest costs and debt levels may be impacted by CAD/USD exchange rates. When considered appropriate, the Trust may use financial instruments to fix or collar future exchange rates. At December 31, 2005 the Trust had no financial instruments outstanding related to foreign exchange rates.

77

Risk Analysis-Business Risk The Trust ’ s exploration, development, production and asset acquisition/disposition activities are conducted in the Western Canada Sedimentary Basin and involve a number of business risks. These risks include the uncertainty of replacing annual production and finding new reserves on an economic basis, the potential instability of commodity prices, exchange rates and interest rates, and other factors discussed under “ Notice Regarding Forward-Looking Statements. ”

78

Hedging Strategy Penn West considers price hedging of oil and natural gas production to be a useful tool of risk management. Its uses include protecting planned capital budgets, safeguarding the economics of acquisitions and providing downside cash flow protection to support planned distributions. During 2006, the Trust continued to employ derivative instruments on a portion of its production volumes spanning several quarters into the future. The Trust also secured hedges to fix the costs of electric power at its oilfield operations, improving its ability to project operating costs, netbacks and cash flows. Penn West is careful and judicious in its hedging activities in order to preserve exposure to commodity price upside and avoid unreasonable opportunity costs.

79

Hedging Strategy Balancing the production portfolio between oil and natural gas; Pursuing low risk development and production optimization projects and implementing a phased approach to significant projects such as the Pembina/Swan Hills CO2 enhanced oil recovery project and the Seal oil sands project; Pursuing strategic acquisitions, dispositions and the farm-out of undeveloped land; Maintaining high average capital efficiency and low operating and general and administrative costs.

80

Hedging Strategy-Financial Instrument All of the accounts receivable are with customers in the oil and natural gas industry and are subject to normal industry credit risk. The Trust, from time to time, uses various types of financial instruments to reduce its exposure to fluctuating oil and natural gas prices, electricity costs, exchange rates and interest rates. The use of these instruments exposes the Trust to credit risks associated with the possible non-performance of counterparties to derivative instruments. The Trust limits this risk by transacting only with financial institutions with high credit ratings and by obtaining security in certain circumstances.

81

Hedging Strategy-Financial Instrument The Trust ’ s revenue from the sale of crude oil, natural gas liquids and natural gas are directly impacted by changes to the underlying commodity prices. To ensure that cash flows are sufficient to fund planned capital programs and distributions, costless collars, or other financial instruments, may be utilized. Collars ensure that commodity prices realized will fall into a contracted range for a contracted sales volume. Forward power contracts fix a portion of future electricity costs at levels determined to be economic by management.

82

Hedging Strategy-Financial Instrument Variations in interest rates directly impact interest costs. From time to time, the Trust may increase the certainty of future interest rates using financial instruments to swap floating interest rates to fixed rates.

83

Hedging Strategy-Financial Instrument Crude oil sales and certain bank loans are referenced to or denominated in U.S. dollars. Accordingly, realized crude oil prices and debts in Canadian dollars are directly impacted by CAD/USD exchange rates. From time to time, the Trust may use financial instruments to fix future exchange rates.

84

Hedging

85

Production and Netbacks

86

Collar

87

Consolidated Statements of Cash Flow

88

Stock Option Until May 31, 2005, the Company had a stock option plan for the benefit of its employees and directors. Stock options vested over a five-year period and, if unexercised, expired six years from the date of grant. The stock option plan included a cash payment alternative and stock- based compensation costs were recorded based on changes to the share price at the end of each quarter and any changes to the number of outstanding options. Pursuant to the plan of arrangement, all stock options outstanding on the date of conversion were settled for cash of $84.77 per share or by issuing shares.

89

The continuity of the compensation liability and outstanding options to the date of cancellation was as follows Stock Option

90

Returns on Equity

91

Sensitivity Analysis This MD&A includes forward-looking statements (forecasts) under applicable securities laws. These statements are based on assumptions related to, but not limited to, commodity prices, the capital markets, the performance of producing wells and reservoirs, and the regulatory and legal environment. Forward-looking statements are subject to known or unknown risks and uncertainties that could cause actual results to differ materially from those anticipated or implied in the forward-looking statements. The Trust assumes no responsibility to publicly update or revise any forward-looking statements. Sensitivities to selected key assumptions, excluding hedging impacts, are outlined in the table below.

92

Sensitivity Analysis

93

Sensitivity Analysis 2007 Forecast

94

Thank you !

Similar presentations

Foreign Exchange MarketsProduct MarketsSubsidiaries International Financial Markets Dividend Remittance & Financing Exporting.>")