Download presentation

Presentation is loading. Please wait.

1

Short-term Medical Insurance AN AFFORDABLE APPROACH TO HEALTHCARE FOR UNEXPECTED ILLNESS OR INJURY For Agent Training Use Only and Not For General Distribution

2

Freedom of Choice Choose your own Doctor or Hospital without network restrictions or penalties For additional savings PHCS Network is available at no additional cost

3

Affordable Choice Short-term Medical plans are affordable because they provide coverage options that make sense. By purchasing a Short-term Medical plan the insured pays for coverage that they need and can afford. This plan will pay benefits up to $250,000 per person during the selected benefit period. Short-term Medical pays for Unexpected Illness or Injury versus the more expense mandatory coverage options required by the Affordable Care Act (ACA).

..")

4

The Unaffordable Care Act The Affordable Care Act provides wonderful coverage at a price that is anything but Affordable. ACA Plans –10 Essential Benefits IncludingShort-term Medical MaternitySolid Basic Insurance Child Dental & VisionCoverage Preventive Routine Care Mental Illness -Very Expensive--Much Less Expensive-

5

The Unaffordable Care Act The Affordable Care Act provide wonderful coverage at a price that is anything but Affordable. ACA Plans – 10 Essential Benefits IncludingShort-term Medical MaternitySolid Basic Insurance Child Dental & VisionCoverage Preventive Routine Care Mental Illness -Very Expensive--Much Less Expensive-

6

Deductible Options Choice of four Deductible options designed to fit your needs. $1,000 $2,500 $5,000 $10,000 Maximum of two deductibles per policy Per Person

7

Coinsurance Benefit per Person Choice of two coinsurance options 75/25% 50/50% Out-of-pocket maximum is $2,500 per person with a maximum of two coinsurance amounts per policy. Out-of-pocket maximum is $5,000 per person with a maximum of two coinsurance amounts per policy. After coinsurance has been satisfied then the plan pays 100% of the additional eligible expenses up to the policy maximum

8

How Short-term Medical pays benefit Your client pays a Deductible of between $1,000 and $10,000 based on their plan selection. This is the amount they must pay before Philadelphia American pays. First Next 75%/25% COINSURANCE Your Client pays 25% of any additional covered charges, up to $2,500 out of their pocket. 50%/50% COINSURANCE Your Client pays 50% of any additional covered charges, up to $5,000 out of their pocket. Thereafter Philadelphia American pays all remaining eligible charges, up to the plan maximum per covered person OR

9

Benefit Summary Subject to Deductible and Coinsurance Inpatient Hospital Benefits Room, board and routine nursing services that are provided to all inpatients while confined in a semi-private room, ward, coronary care or other intensive care unit in a Hospital. Hospital Physician Services, Surgical and Anesthesia Services Surgical services, anesthesia services and Physician service (not including Physicians office visits). Physician Office Visits $30 Copayment; applies to 1st visit per Insured per Benefit Period; subject to an Office Visit Waiting Period of 30 days. Additional office visits thereafter per Insured per benefit period will be subject to the Deductible or Coinsurance without the application of a Copayment. Outpatient Services Services performed in a Hospital's outpatient department or in a Free-Standing Ambulatory Surgical Facility including Emergency room care

. Physician Office Visits $30 Copayment; applies to 1st visit per Insured per Benefit Period; subject to an Office Visit Waiting Period of 30 days. Additional office visits thereafter per Insured per benefit period will be subject to the Deductible or Coinsurance without the application of a Copayment. Outpatient Services Services performed in a Hospital s outpatient department or in a Free-Standing Ambulatory Surgical Facility including Emergency room care.")

10

Benefit Summary Subject to Deductible and Coinsurance Home Health Care Home health care visits provided by a state licensed or Medicare certified home health agency. One visit consists of up to 4 hours of services provided within a 24-hr. period. Outpatient Physical Medicine Services Physical, speech or occupational therapy; pulmonary or cardiac rehabilitation therapy; or adjustments and manipulations provided in the outpatient department of a Hospital, by a licensed or certified home health care agency or by a licensed therapist in Your home. Ambulance Ambulance service for one trip to the nearest Hospital that is able to treat the sickness or Injury. Maximum benefit for air ambulance services is $1,000 per Benefit Period. Prescription Drugs Drugs and medicines that are received on an outpatient basis, with written prescription of a Physician for treatment of a condition that is a Covered Expense under the policy and are dispensed by a licensed pharmacy.

11

Benefit Summary Subject to Deductible and Coinsurance Skilled Nursing Facility Care Care in a Skilled Nursing Facility when the confinement is in lieu of acute hospitalization or when admitted to the Skilled Nursing Facility within 14 days after a Hospital confinement of at least 3 days for the same condition. Durable Medical Equipment and Supplies Rental, up to the purchase price, or purchase of a non-electric wheelchair, basic hospital bed or crutches; the initial permanent basic artificial limb or eye; oxygen and the equipment needed to administer oxygen; casts, orthopedic braces, splints, dressings and sutures. Other Important Benefits – Subject To Deductible and Coinsurance X-ray, Radiation Therapy, Chemotherapy and Laboratory Charges. Blood Product Transfusions: Whole blood, Blood plasma and Blood products if not replaced.

12

Affordable Premiums

13

Single Pay Option Save 20% when you pay up front. Monthly total they would have paid $1,019.46 vs $815.58 Single Pay

14

How many months of coverage can I purchase? You may select a specific period of coverage from 1 month to 12* months for your Short-term Medical plan. The coverage for the 12 th month will end on the 364 th day of the benefit period. Issue age is 0-64. If your needs for coverage extend beyond this plan, you may apply for additional short term plans. This requires a new application and is not an extension of your current plan. Any illness or condition developed while covered by the current plan would be considered “preexisting” when applying for a new short term plan as such, will not be a covered expense. *Coverage months may vary by state.

15

Does the plan pay benefits for a Pre-Existing Condition? Since Short-term Medical covers unexpected illnesses and injuries, it does not cover pre-existing conditions. While the definition of pre-existing conditions may vary by state, In general it means a condition for which medical treatment was rendered or recommended by a Physician or for which drugs or medicine was prescribed within 24 months prior to a Covered Person’s Effective Date. If the applicant has a pre-existing condition for which they need coverage for, they may want to purchase a metallic plan that includes health care reform benefits.

16

Does the plan require Hospital Pre-Certification? Yes. Authorization of a Hospital admission is mandatory. Failure to authorize will result in a penalty equal to $1000 ($500 Texas). If the admission is elective, notification is required at least 72 hours before the scheduled date and time of admission. If the admission is non-elective or due to an Emergency, notification is required within 48 hours after the date and time of admission. All admissions will be reviewed for medical necessity by the Company

. If the admission is elective, notification is required at least 72 hours before the scheduled date and time of admission. If the admission is non-elective or due to an Emergency, notification is required within 48 hours after the date and time of admission. All admissions will be reviewed for medical necessity by the Company.")

17

Does the plan have a waiting period for benefits? Yes. There is a 15 day waiting period for expenses incurred due to a Sickness that manifests itself before the Effective Date of coverage. Benefits are available from the 1 st day for covered expenses that are incurred for an Injury that is sustained on or after the Effective Date of coverage.

18

Is Short-term Medical considered minimum essential coverage? Short Term Medical is not minimum essential coverage. That means if your client insures themselves with Short Term Medical instead of a metallic plan that meets reform requirements, they may have to pay a tax penalty, depending on their income and the cost of available metallic plans.

19

Is termination of the STM plan considered a Qualifying Life Event? No, Short-term Medical policies are nonrenewable, and plan termination is not considered a qualifying life event for purposes of enrolling in a metallic plan. Therefore, depending on the plan’s termination date and when the Short Term Medical plan expires, there may be a gap in insurance coverage until your client can begin coverage with a new Short Term Medical or other health insurance plans.

20

What happens if I’m in the hospital when the plan terminates? We will extend coverage for a loss which began while an Insured person was insured under the policy and who is Totally Disabled as a result of Injury or Sickness. The extension of coverage will end on the earliest of: An insured under this policy, is considered Totally Disabled if confined as a patient in a Hospital. 1. The date on which treatment is no longer required; or 2. The date which is 90 days after the date on which the insurance would ….. have otherwise ended; or 3. The date on which the person is no longer disabled; or 4. The date $10,000 maximum benefit for Covered Expenses is incurred under ….. this Extension of Benefits provision.

21

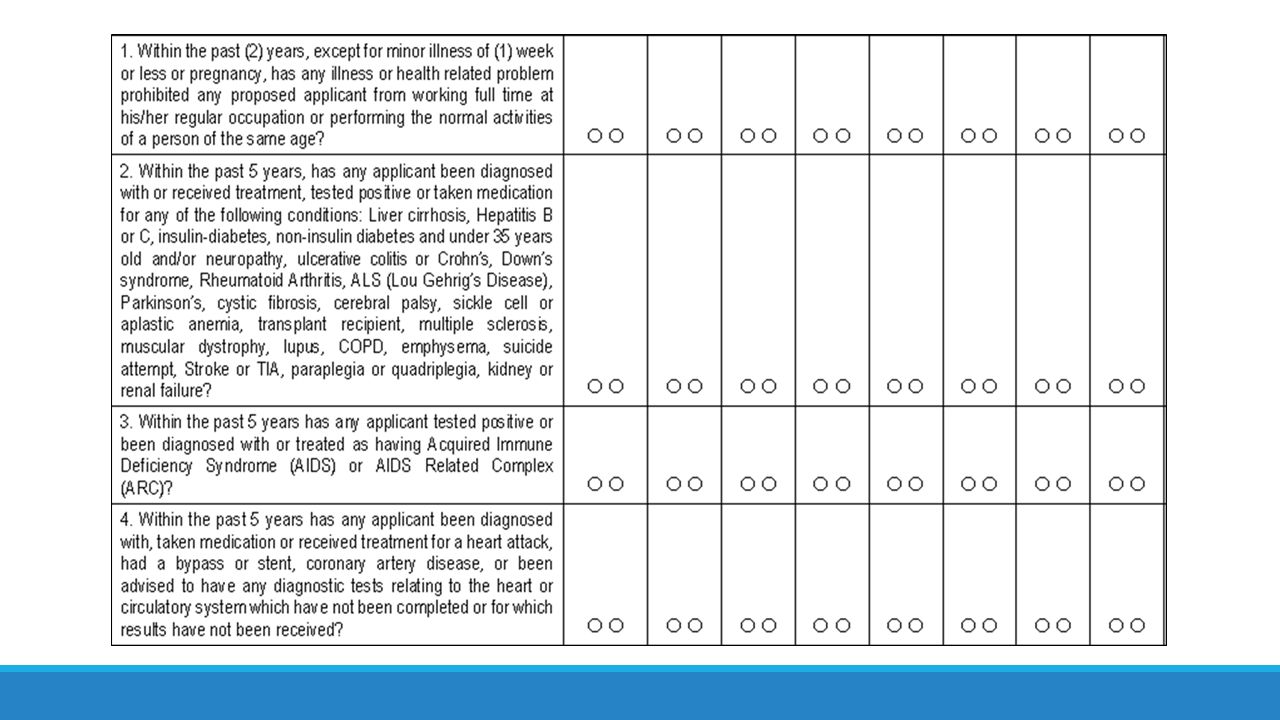

Underwriting Simplified Issue Application

25

Thank You

Similar presentations

Everything You Need to Know.>")

MKT0052 0607 Sensible Insurance for Today’s Lifestyles.>")

and limitations Medicare.>")