Download presentation

Presentation is loading. Please wait.

1

The Costs of Production

Explicit and Implicit Costs Explicit Costs: Money payments that a firm makes for the use of resources owned by others (labor, materials, fuel, etc.) Implicit Costs: The opportunity costs of self-owned resources. The value of the next best thing you could do with your labor, time, tools, entrepreneurial talent, etc. Things you could have gotten paid to do.

Implicit Costs: The opportunity costs of self-owned resources. The value of the next best thing you could do with your labor, time, tools, entrepreneurial talent, etc. Things you could have gotten paid to do.")

2

Walt and Jesse make peanut brittle in their lab.

Explicit Costs: the equipment, electricity, the ingredients, rent for the building, transportation to ship the product, etc. Implicit Costs: all the money they could have made cooking something else in the lab.

3

Accounting Profit, Normal Profit, and Economic Profit

Accounting Profit – Business makes enough to cover its explicit costs. Any more is accounting profit. Normal Profit – business makes enough to cover its explicit costs plus implicit costs, including enough to pay the entrepreneur an amount equal to what he or she could make running a business of a similar scope. Economic Profit – profit over and above normal profit. It is an added reward to the entrepreneur and what lures new companies into an industry.

4

Jesse: “This is awesome, Mr. White

Jesse: “This is awesome, Mr. White. We spent $2000 on ingredients and materials, $10,000 to rent the lab and equipment for the month. We sold our peanut brittle for $20,000. That’s an $8000 profit!” Walt: “Jesse you’re an idiot!!! …”

6

Short Run vs. Long Run Short run: To little time for a firm to change its plant capacity, but enough to change production levels by varying the amounts of resources (material, labor, etc.). Long Run: Enough time for a firm to alter plant capacity. For an industry, it’s also enough time for new firms to enter the business or existing firms to exit. Short run = Fixed Plant Long Run = Variable Plant

. Long Run: Enough time for a firm to alter plant capacity. For an industry, it’s also enough time for new firms to enter the business or existing firms to exit. Short run = Fixed Plant. Long Run = Variable Plant.")

7

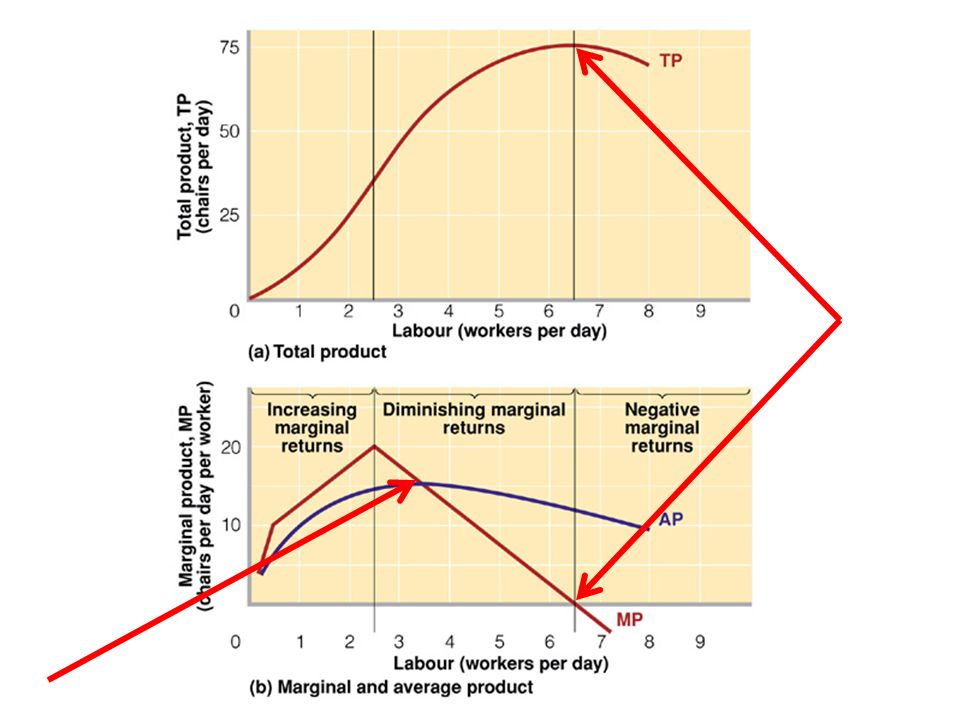

Short-Run Production Relationships

Total Product (TP) – Total quantity produced. Marginal Product (MP) – The extra output achieved by adding one more unit of some variable resource (one more worker, one more bag of peanuts, one more barrel of molasses) Average Product (AP) – Output per unit of labor. So if we have 20 employees and produce 100 tons of peanut brittle, our average output is 5 tons.

– Total quantity produced. Marginal Product (MP) – The extra output achieved by adding one more unit of some variable resource (one more worker, one more bag of peanuts, one more barrel of molasses) Average Product (AP) – Output per unit of labor. So if we have 20 employees and produce 100 tons of peanut brittle, our average output is 5 tons.")

9

The Law of Diminishing Returns

30 TP Total product, TP 20 10 1 2 3 4 5 6 7 8 9 The law of diminishing returns states as a variable resource (labor) is added to fixed amounts of other resources (land or capital). The total product that results will eventually increase by diminishing amounts, reach a maximum, and then decline. Marginal product is the change in total product associated with each new unit of labor. Average product is simply output per labor unit. Note that marginal product intersects average product at the maximum average product. Increasing Marginal Returns Diminishing Marginal Returns Negative Marginal Returns 20 Marginal product, MP 10 AP 1 2 3 4 5 6 7 8 9 MP LO2

is added to fixed amounts of other resources (land or capital). The total product that results will eventually increase by diminishing amounts, reach a maximum, and then decline. Marginal product is the change in total product associated with each new unit of labor. Average product is simply output per labor unit. Note that marginal product intersects average product at the maximum average product. Increasing. Marginal. Returns. Diminishing. Marginal. Returns. Negative. Marginal. Returns. 20. Marginal product, MP. 10. AP MP. LO2.")

10

Law of Diminishing Returns

As more and more variable resources are added, additional production gains will eventually decline.

11

Homework Do Ch. 22 Study Questions #1, 2, & 3.

Read p. 398 – 403 (stop at “Long-Run Production Costs) Do the quick quiz on 401 and check answers. Explain IN YOUR OWN WORDS why the marginal cost curve intersects the AVC and ATC curves at their minimum points. This is a key idea. Spend some serious time trying to wrap your head around this if you don’t get it at first. Do Study Questions 4 (complete the table and graph only), 6, and 7a.

Do the quick quiz on 401 and check answers. Explain IN YOUR OWN WORDS why the marginal cost curve intersects the AVC and ATC curves at their minimum points. This is a key idea. Spend some serious time trying to wrap your head around this if you don’t get it at first. Do Study Questions 4 (complete the table and graph only), 6, and 7a.")

12

30 # of Lawns Cut/Day 20 Total Product Area of increasing marginal returns. 10 Area of decreasing marginal returns. Area of negative marginal returns. Quantity of Labor (# of workers) 7 Average Product Marginal Product -3

7. Average Product. Marginal Product")

13

1 2 3 4 5 6 7 8 9 10 Total Cost Total Variable Cost Total Fixed Cost

550 500 450 400 350 300 250 200 150 100 50 1 2 3 4 5 6 7 8 9 10 Total Cost Total Variable Cost Total Fixed Cost

14

A B C 1 2 3 4 5 6 7 8 9 10 Cost ($) 50 Quantity (units) 450 400 350

550 500 450 400 350 300 250 200 150 100 50 1 2 3 4 5 6 7 8 9 10 A B Cost ($) C Quantity (units)

C. Quantity (units)")

15

Total Cost 4 200 1 2 3 5 6 7 8 9 10 Cost ($) Quantity (units) 100 50

550 500 450 400 350 300 250 150 100 50 1 2 3 4 5 6 7 8 9 10 Total Cost Cost ($) 200 Quantity (units)

200. Quantity (units)")

16

MC2 MC1 ATC2 ATC1 1 2 3 4 5 6 7 8 9 Cost ($) Quantity (units) 90 80 70

105 100 90 80 70 60 50 40 30 20 10 1 2 3 4 5 6 7 8 9 MC2 MC1 Cost ($) ATC2 ATC1 Quantity (units)

ATC2. ATC1. Quantity (units)")

17

AVC2 AVC1 ? 1 2 3 4 5 6 7 8 9 Cost ($) Quantity (units) 90 80 70 60 50

105 100 90 80 70 60 50 40 30 20 10 1 2 3 4 5 6 7 8 9 Cost ($) AVC2 AVC1 ? Quantity (units)

AVC2. AVC1. Quantity (units)")

Similar presentations