Download presentation

Presentation is loading. Please wait.

1

University of the Free State OECD meeting Rabat – May 2008

PUBLIC-PRIVATE PARTNERSHIPS: AFFORDABILITY, RISK SHARING AND VALUE FOR MONEY Philippe Burger University of the Free State OECD meeting Rabat – May 2008

2

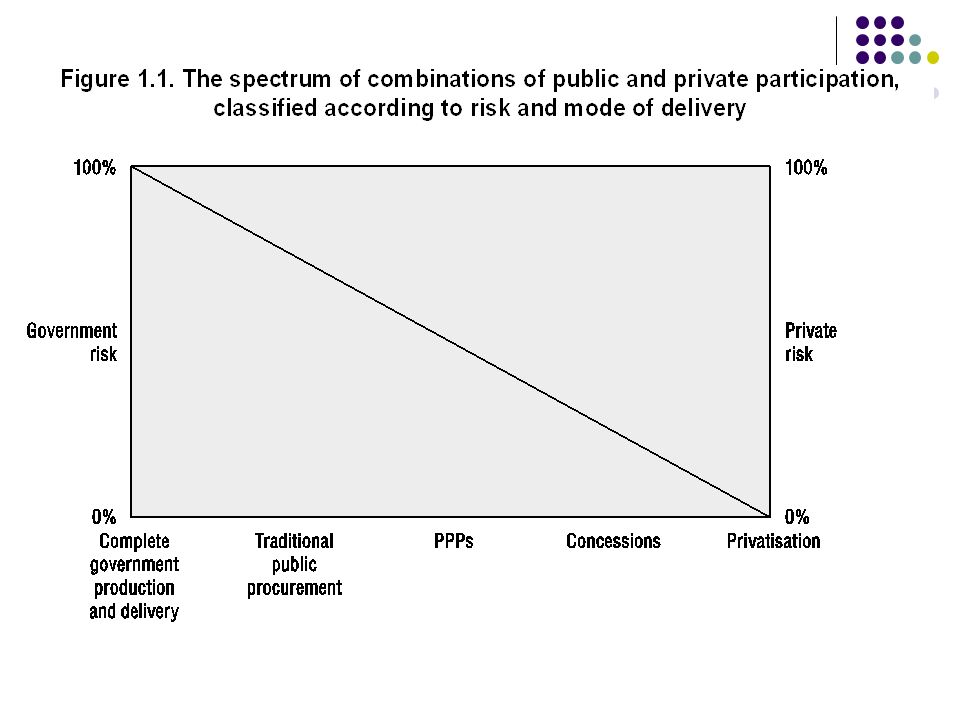

1. Defining PPPs Lack of definitional clarity.

Grimsey and Lewis (2005:346), “…fill a space between traditionally procured government projects and full privatization” Need to distinguish them clearly from traditional procurement and privatisation, but also from concessions.

, …fill a space between traditionally procured government projects and full privatization Need to distinguish them clearly from traditional procurement and privatisation, but also from concessions.")

3

IMF: PPPs refer to arrangements where the private sector supplies infrastructure assets and services that traditionally have been provided by the government. European Investment Bank: PPPs are relationships formed between the private sector and public bodies often with the aim of introducing private sector resources and/or expertise in order to help provide and deliver public sector assets and services.

4

Distinct from traditional procurement: role of risk.

Distinct from privatisation: define what is a partner. Distinct from concessions: demand risk and source of revenue.

5

OECD: PPP is an agreement between the government and one or more private partners (which may include the operators and the financers) according to which the private partners deliver the service in such a manner that the service delivery objectives of the government are aligned with the profit objectives of the private partners and where the effectiveness of the alignment depends on a sufficient transfer of risk to the private partners.

6

The private partners usually design, build, finance, operate and manage the capital asset, and then deliver the service either to government or directly to the end users. The private partners will receive as reward a stream of payments from government, or user charges levied directly on the end users, or both (Concessions vs PPPs). Government specifies the quality and quantity of the service it requires from the private partners. There is a sufficient transfer of risk to the private partners to ensure that they operate efficiently.

. Government specifies the quality and quantity of the service it requires from the private partners. There is a sufficient transfer of risk to the private partners to ensure that they operate efficiently.")

8

2. Affordability Do PPPs create more space in the budget?

Affordability in principle terms. Affordability in practical terms. Affordability and VFM: Relative vs. absolute affordability. Efficiency and the cost of capital. Affordability, limited budget allocations, legally imposed budgetary limits and fiscal rules.

9

2.1 Affordability in principle terms

Affordability and VFM are the benchmarks for PPP viability. Affordability and VFM determines whether the PPP route is the best alternative. Because of the off-balance sheet nature of PPPs, their use has led to some misconceptions regarding their impact on the affordability of projects. Confusion stems from the impression that because government not responsible for the acquisition of the asset, that PPPs are cheaper than traditional procurement – this is a fallacy.

10

Though PPPs may enable some projects to become affordable, this does not stem from their off-balance sheet nature. The point is: Affordability not only relates to PPPs, but to government expenditure items in general.

11

In principle affordability is about whether or not a project falls within the long-term (intertemporal) budget constraint of government. If it does not, then the project is unaffordable. However, because the cash flows and balance sheet treatment of PPPs differ significantly from that of traditional procurement, some confusion exists about the effect of PPPs on affordability.

13

In principle terms, a traditionally procured project is affordable if the present value of the expected future revenue stream of government: equals or exceeds the present value of expected future capital and current expenditure of government, while a portion of such future expenditure streams is allocated to such a traditionally procured project.

15

In principle terms, a PPP is affordable if the present value of the expected future revenue stream of government: equals or exceeds the present value of expected future capital and current expenditure of government, while a portion of such future expenditure streams is allocated to such a PPP.

17

2.2 Affordability in practical terms

Even though the above is technically correct, it has one shortcoming: Although PPPs and the PSC used in PPPs involve detailed present value calculations over the whole life of a PPP contract, governments rarely use present value calculations for the rest of their activities. Governments also rarely budget for a longer horizon than the upcoming year (although some use medium term fiscal forecast). This raises the question: how should affordability of a PPP be assessed within an environment where the planning horizon is not very long?

. This raises the question: how should affordability of a PPP be assessed within an environment where the planning horizon is not very long")

18

As with other government activities in such an environment a PPP project is affordable if:

the expenditure it implies for government can be accommodated within current levels of government expenditure and revenue (as captured in the current budget and medium term forecasts) and if it can also be assumed that such levels will be and can be sustained into the future. This working definition of affordability allows for the use of present value calculations when estimating cost of a PPP vs that of traditional procurement (using a PSC), but to do so in an environment with a short planning horizon.

and if it can also be assumed that such levels will be and can be sustained into the future. This working definition of affordability allows for the use of present value calculations when estimating cost of a PPP vs that of traditional procurement (using a PSC), but to do so in an environment with a short planning horizon.")

19

2.3 Affordability and VFM Relative affordability: affordability of PPP compared to that of traditional procurement. Interest rate and efficiency differentials main determinants (of relative affordability and VFM). Absolute affordability: Can the project (delivered either trough a PPP or traditional procurement) be accommodated within the budget without violating the budget constraint.

. Absolute affordability: Can the project (delivered either trough a PPP or traditional procurement) be accommodated within the budget without violating the budget constraint.")

20

UK: Procuring authorities must complete affordability model for any planned PFI (it includes sensitivity analysis). The models based on agreed upon departmental figures for the years available and cautious assumptions about future dept spending envelopes.

21

Victoria: Decision about how a project is funded is separate from the decision about how it is to be delivered. Potential PPP compete with other capital projects for limited budget funding to ensure that they fall within what is considered affordable. Funding is approved on the preliminary Public Sector Comparator.

22

Brazil: Project studies must include a fiscal analysis for the next ten years. In addition, the commitment of the federal budget to PPP projects is limited by law to 1% of the net current revenue of the government. Hungary: From 2007 a limit on the amount of expenditure on PPPs within the budget, so that each program has to fit within this limit.

23

2.4 Affordability, limited budget allocations and legally imposed budgetary limits

Distinction between affordability, limited budget allocations and legally imposed budgetary limits In many countries there are: Limits on second- and third-tier government borrowing. Fiscal rules that limit government expenditure, deficits or debt. Thus, project might be affordable, but legally imposed budgetary limit prohibits borrowing. In some cases the opposite is also possible.

24

In addition: budgetary allocations of government departments and authorities that are done from a central budget and within which expenditure plans must be fitted. Even if a traditionally procured project would not violate the long-term budget constraint of government, a project may still exceed the future expected budgetary allocations of a specific government department.

25

Danger: less of a focus on VFM and create an incentive to get project off the books of government.

Two specific cases when there is an incentive to get project of the books of government. The first case is one where a project cannot be delivered through either traditional procurement or a PPP within budgetary limits.

26

Has 3 features, but a short-run focus on 1st and disregard for the 2nd and 3rd by gov creates incentive to go PPP route: Should gov use traditional procurement: Large initial capital outlay will cause a gov entity to exceed its allocated budget. Should entity then decide to go PPP route: May not be able to make future fee payments to private partners without exceeding expected future allocated budgets. In addition, private partner also cannot levy user charge on direct consumers of the service.

27

Second case occurs when gov operates under a fiscal rule that sets a limit on the overall fiscal balance of gov (or a dept operates under a budget allocation). Results from cash-flow vs accruals accounting. Traditional procurement: Capital outlays may contribute to breaking the budgetary limit in the year in which government undertakes outlays. PPP: Private sector responsible for initial capital outlay and government might be able to fit future payment of fees to private partner into its budget without exceeding the budget limit.

29

In all three cases the budgetary limit may be main reason why government might want to get projects off its books. However, main reason should be higher VFM. This is not an argument against budgetary limits and rules – rather it is an argument in favour of emphasising VFM as the main rationale for going the PPP route.

30

3. VFM and risk transfer Reason for going the PPP route: Value for money, but effective risk transfer to the private partner prerequisite to ensure VFM. UK National Audit Office (2003): 22% of UK PFI deals experienced cost overruns and 24% delays; compared to 73% and 70% of public sector projects. Scottish Executive and CEPA study (HM Treasury 2006): Authorities: 50% received good VFM, 28% reported satisfactory VFM. KPMG survey (2007) among private project managers in the UK: 59% of respondents said performance of their projects in 2006 was very good, compared to 49% in 2005.

: 22% of UK PFI deals experienced cost overruns and 24% delays; compared to 73% and 70% of public sector projects. Scottish Executive and CEPA study (HM Treasury 2006): Authorities: 50% received good VFM, 28% reported satisfactory VFM. KPMG survey (2007) among private project managers in the UK: 59% of respondents said performance of their projects in 2006 was very good, compared to 49% in")

31

However, having private partner is not in itself sufficient to ensure VFM: need transfer of risk.

VFM: optimal combination of quality, features and price, calculated over the whole of the project’s life. Studies confirmed importance of risk transfer. Risk: The measurable probability that the actual outcome will deviate from the expected (or most likely) outcome. Private partner carries risk if its income and profit is linked to the extent that its actual performance complies or deviates from expected (and contractually agreed) performance.

outcome. Private partner carries risk if its income and profit is linked to the extent that its actual performance complies or deviates from expected (and contractually agreed) performance.")

33

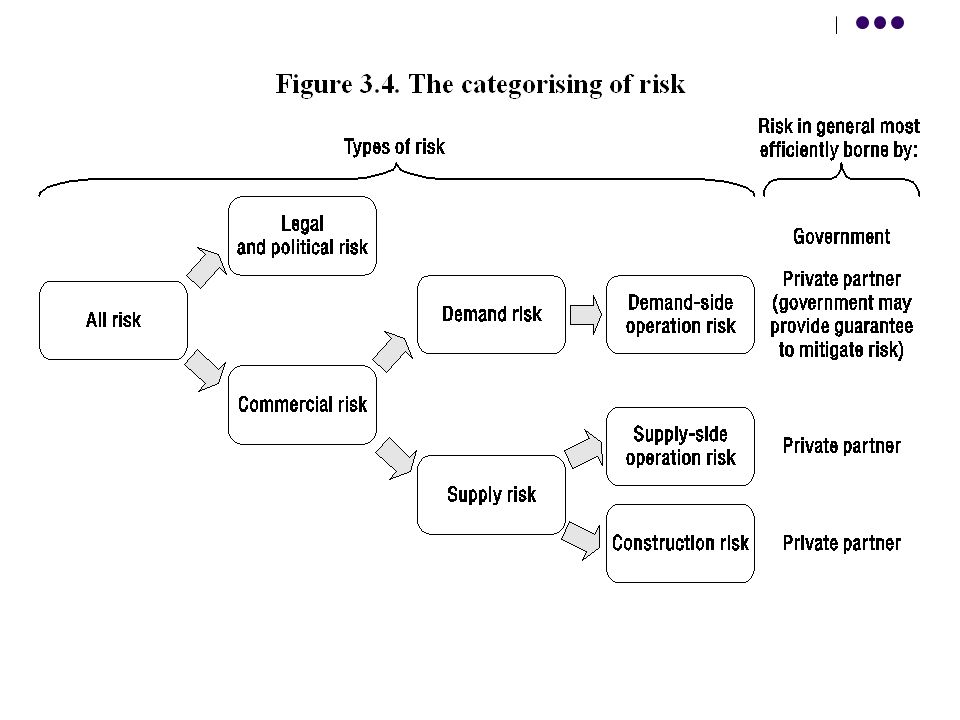

Many factors that may affect its actual performance

Some can be managed, others not. Thus, need to distinguish between endogenous and exogenous risk. Transfer endogenous risk: Company can influence the extent to which actual outcome deviates from expected outcome. Key question: Is whether the adverse outcome is foreseeable and if it is, can it be managed?

34

Examples of endogenous risk:

Equipment and physical structure (e.g. buildings, roads) deterioration. Wasteful use of inputs (i.e. x-inefficiency) – includes wasteful use of raw materials, appointment of too many personnel. Failure to manage risk related to input prices (e.g. failure to negotiate best price of raw materials and labour services; failure to use hedge prices through use of future and forward contract). Failure to implement accounting and auditing procedures that leads to theft, fraud and corruption.

deterioration. Wasteful use of inputs (i.e. x-inefficiency) – includes wasteful use of raw materials, appointment of too many personnel. Failure to manage risk related to input prices (e.g. failure to negotiate best price of raw materials and labour services; failure to use hedge prices through use of future and forward contract). Failure to implement accounting and auditing procedures that leads to theft, fraud and corruption.")

35

Examples of exogenous risk:

Unforeseen technological redundancy (e.g. ICT). Unforeseen demographic changes (e.g. migration, changes in labour force participation, changes in population composition). Unforeseen changes in preferences (e.g. high-speed trains vs. airplanes). Unforeseen environmental changes (e.g. costs arising from pollution management and pursuit of cleaner energy use). Unforeseen natural and manmade disasters (e.g. costs arising from floods, wildfires or political acts). Unforeseen exchange rate movements driven by speculation.

. Unforeseen demographic changes (e.g. migration, changes in labour force participation, changes in population composition). Unforeseen changes in preferences (e.g. high-speed trains vs. airplanes). Unforeseen environmental changes (e.g. costs arising from pollution management and pursuit of cleaner energy use). Unforeseen natural and manmade disasters (e.g. costs arising from floods, wildfires or political acts). Unforeseen exchange rate movements driven by speculation.")

36

Transfer of risk in PPP does not imply the maximum transfer of risk to the private partner.

It means that the party best able to carry the risk, should do so.

38

Confusion about what ‘best able to carry risk’ means

Leiringer (2005): Is this the party with largest influence on the probability of an adverse occurrence happening, or the party that can best deal with the consequence after an adverse occurrence? Corner (2006): To best manage risk means to manage it at least cost. If cost of preventing an adverse occurrence is less than cost of dealing with consequences of the adverse occurrence, then risk should be allocated to the party best able to influence the probability of occurrence.

: Is this the party with largest influence on the probability of an adverse occurrence happening, or the party that can best deal with the consequence after an adverse occurrence Corner (2006): To best manage risk means to manage it at least cost. If cost of preventing an adverse occurrence is less than cost of dealing with consequences of the adverse occurrence, then risk should be allocated to the party best able to influence the probability of occurrence.")

39

Cases where cost of preventing occurrence (incurred by private partner) is lower than cost dealing with fallout (incurred by both private partner and government): Example 1: Cost of road maintenance vs. rebuilding sections of road once it degraded and damages paid because of accidents – probably cheaper to maintain road. Cases where cost of preventing occurrence (incurred by private partner) is higher than cost dealing with the consequences (incurred by both private partner and government): Example 2: Cost of maintaining some types of ICT equipment vs. cost of dealing with the consequences of broken equipment – cost of dealing with broken equipment is cheaper than to maintain it.

is higher than cost dealing with the consequences (incurred by both private partner and government): Example 2: Cost of maintaining some types of ICT equipment vs. cost of dealing with the consequences of broken equipment – cost of dealing with broken equipment is cheaper than to maintain it.")

40

6. Competition and Value for Money

Why is competition important? Competition for the market. Competition in the market. Contestability and competition.

41

Monopolistic behaviour and lack of competition: no VFM.

Competition important in pre- and post-contract phases. Pre-contract phase competition occurs in the bidding process. Zitron: 86 recent UK PPPs at tender stage: on average 3 bidders for each contract. However, 20% of 86 PPPs less than 3 bidders. Few bidders increase danger of opportunistic (monopolistic) behaviour by the bidders.

behaviour by the bidders.")

42

Too few bidders: VFM is not attained.

How does government end up with too few bidders? Paradox of many potential and few actual bidders. With many bidders: probability of being preferred bidder is small. Given bidding cost, this may cause strong potential private partners not to bid, even if the project itself and the risks that it entails are acceptable to them. Few specialist companies. Danger is that just a small group of companies may bid for every project that comes along.

43

Can address this by having government cover the bidding cost. However:

Distinction should be made between bidding risk and the risk of the project itself. Can address this by having government cover the bidding cost. However: Government will have to enter this subsidy as as part of the total project cost. Before agreeing to pay a private company’s bidding cost, that company must first demonstrate that they have the capacity to bid and to deliver the service in the event that they should get the contract.

44

Competition in the post-contract phase also a complex issue.

Once preferred bidder is announced and the contract is signed, the unsuccessful bidders move on, some leaving the industry. Thus, once the contract is signed, the preferred private partner becomes a monopolist supplier. Exception if the market is contestable.

45

While risk transfer is the driver of efficiency and VFM, competition and contestability ensures effective risk transfer. In the absence of competition or potential entry it will be difficult to attain higher efficiency and VFM.

Similar presentations

Marcin Woronowicz European Commission, Eurostat, Unit C.3 – Public finance.>")

A funding & operational.>")