Download presentation

Presentation is loading. Please wait.

7

Kaizen is a daily process, the purpose of which goes beyond simple productivity improvement. It is also a process that, when done correctly, humanizes the workplace, eliminates overly hard work (" muri "), and teaches people how to perform experiments on their work using the scientific method and how to learn to spot and eliminate waste in business processes.

, and teaches people how to perform experiments on their work using the scientific method and how to learn to spot and eliminate waste in business processes..")

9

“the maintenance of present cost levels for products currently being manufactured via systematic efforts to achieve the desired cost level.” Kaizen Costing is a cost reduction system. Yashihuro Moden defines kaizen costing as :

10

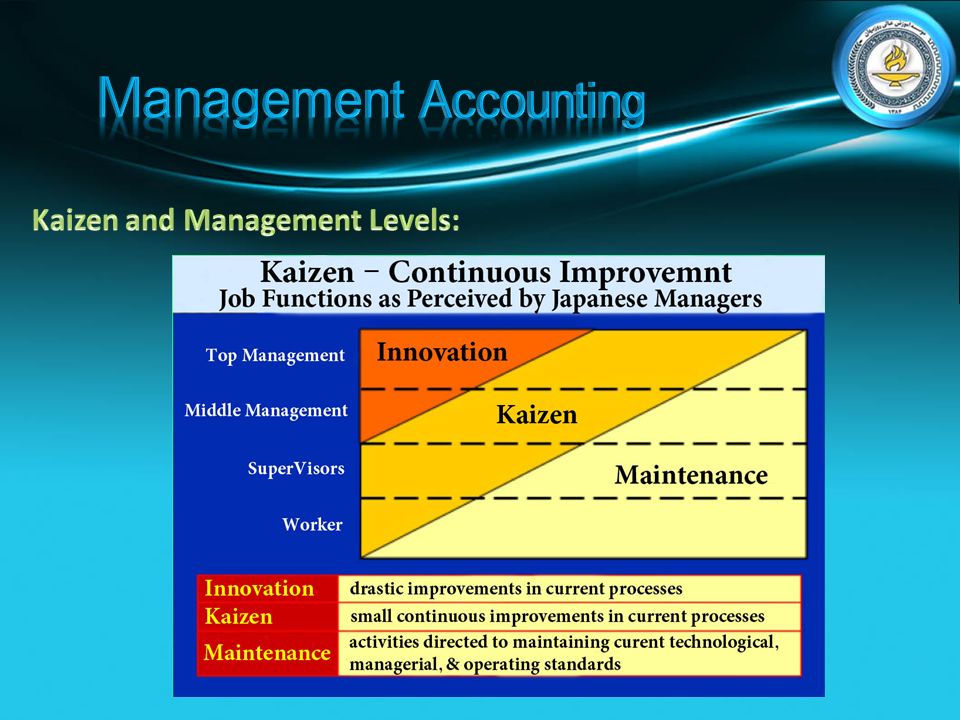

Moden has described two types of kaizen costing: 1. Asset and organisation specific kaizen costing : activities planned according to the exigencies of each deal 2. Product model specific costing : activities carried out in special projects with added emphasis on value analysis 1. Is a Cost reduction system whose Goal is to reduce final estimations to a level that is lower than standard costs. 2. Checks that costing targets have been reached. 3. Continuous review existing production conditions in order to reduce costs.

11

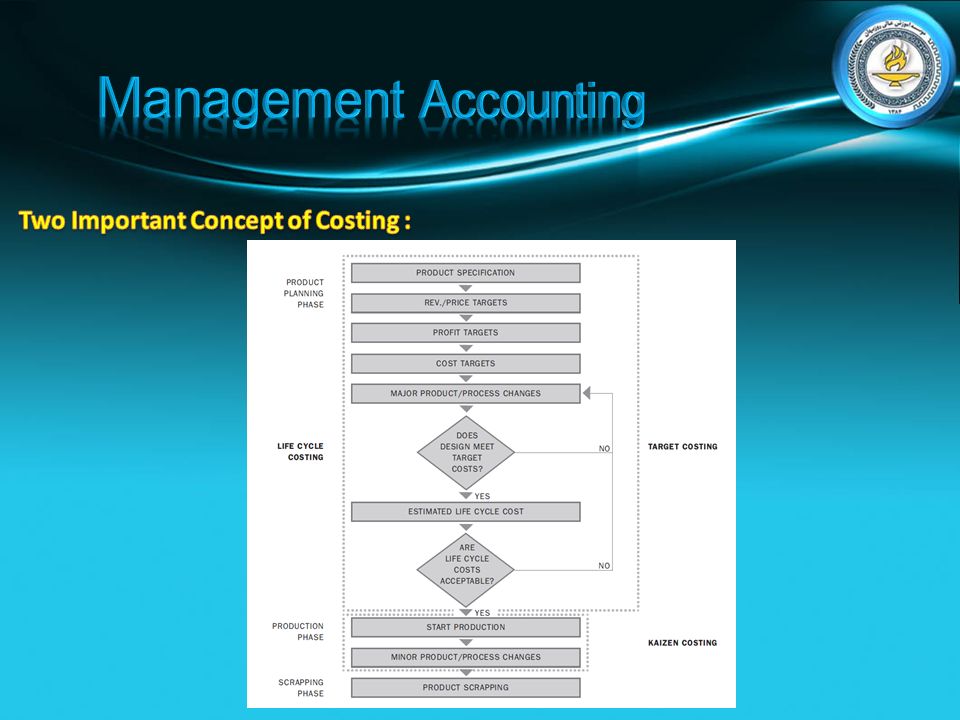

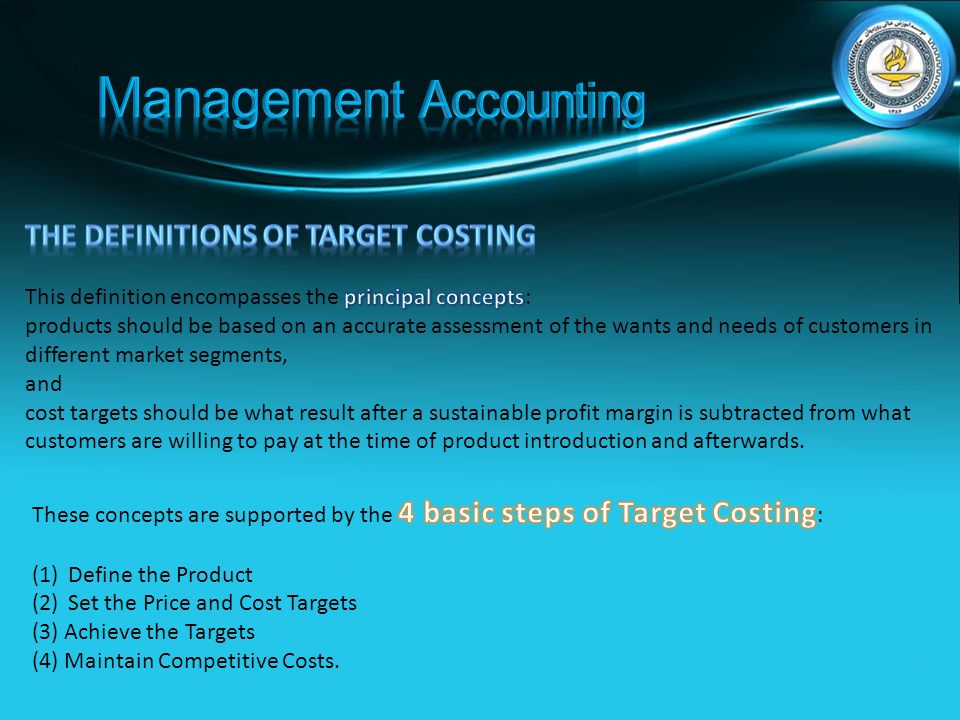

1. The Concept of Kaizen, meaning “improvements in small steps” was developed within quality assurance technology. Based on this Concept, Moden developed kaizen Costing, which can be translate as “enhancement estimation “. Kaizen costing is applied to a product that is already under production. 2. The time prior to kaizen costing is to called “ Target Costing” which involves searching for a target cost for a product before it reaches the market. Together, these two concepts make up Life Cycle Costing.

17

Target costing originated in Japan in the 1960s, though it remained a secret for years. Since the 1980s, however, when target costing was widely recognized as a major factor for the superior competitive position of Japanese companies, extensive efforts have been made to convey target costing to Western companies. Many large companies in North America and Europe have tried to adopt target costing to enhance their cost management and, thus, increase their competitiveness. Consequently, many variations of target costing have been developed and are being used in different countries.

20

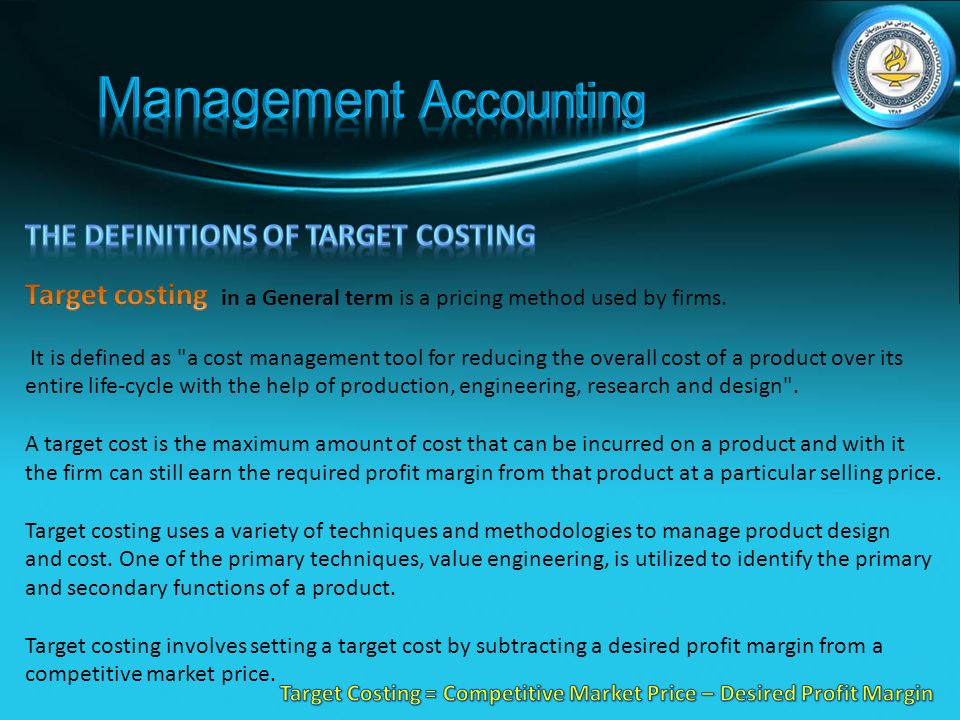

A lengthy but Complete Definition : “ Target Costing is a disciplined process for determining and achieving a full-stream cost at which a proposed product with specified functionality, performance, and quality must be produced in order to generate the desired profitability at the product’s anticipated selling price over a specified period of time in the future."

23

The uniqueness of Japanese target costing comes into play when strategic product positioning is completed in coordination with the company’s general strategy. This is also the point in time when the product-market mix has been determined and Information about what product attributes and what related prices consumers desire are collected through a market analysis. Up to that point, the Japanese way is similar to the traditional Western cost management. However, there are important differences between these two approaches in the way the market information is gathered and converted into an actual product.

24

Western and Japanese Cost Management

26

Target Costing and Kaizen Costing

34

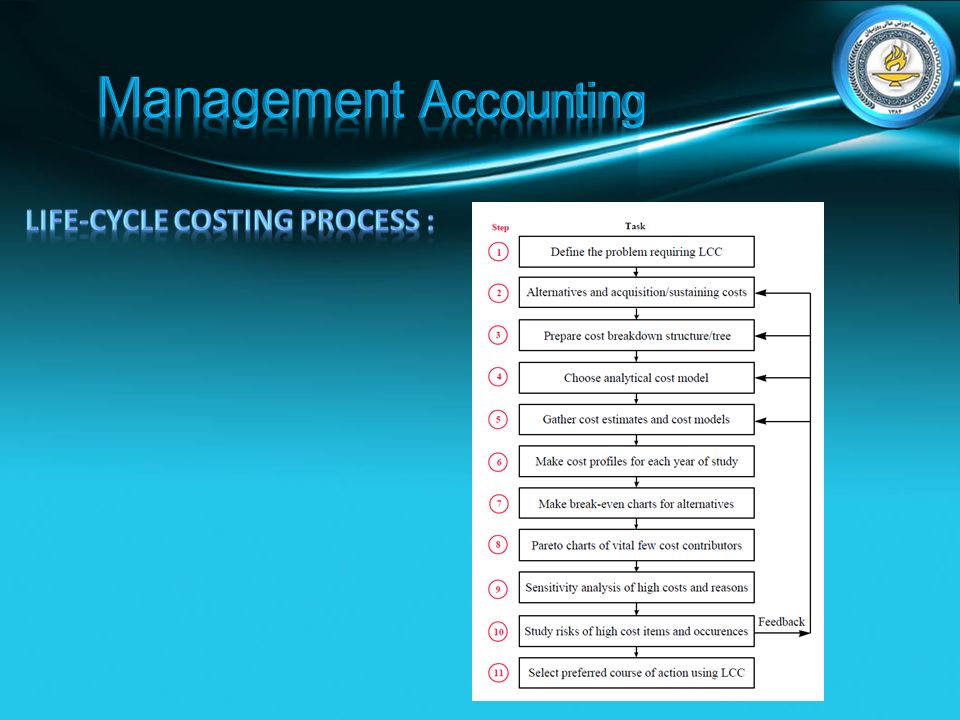

The process of life-cycle costing (LCC) fundamentally involves: assessing costs arising from an asset over its life cycle; and evaluating alternatives that have an impact on this cost of ownership. An asset can be any item that has a value to an organisation over time. Items such as buildings,physical plant and equipment and computer software are normally regarded as assets.

35

The life cycle of an asset is characterised by a number of key stages: initial concept definition; development of the detailed requirements, specification or documentation; construction, manufacture or purchase; defects liability period and early stages of usage or occupation; prime period of usage and functional support, with the associated series of upgrades and renewal processes; and the situation at the end of the asset’s useful life.

36

The diagram shows a typical life cycle cost profile for an asset, from its design to its disposal. The diagram is not drawn to a consistent time scale. The middle operational period is generally much longer than shown in the diagram.

37

The life-cycle cost of an asset can be expressed by the simple formula: LCC = capital cost + life-time operating costs + life-time maintenance costs + disposal cost -residual value. However, ascertaining a measure of each variable in the formula can be difficult. Future costs are usually subject to a level of uncertainty that arises from a variety of factors, including: the prediction of the pattern of use of the asset over time; the nature and scale of operating costs; the need for and cost of maintenance activities; the impact of inflation on individual and aggregate costs; the prediction of the length of the asset's useful life; and the significance of future expenditure compared with present day expenditure.

38

To estimate the total life-cycle costs of an asset, it is necessary to identify the key cost elements. The choice of an appropriate set of elements will reflect three specific issues: 1. The element must be a clearly defined activity that generates costs. As far as possible, elements should be independent. 2. The time line for the element's costs must be known. The significance of a cost generally depends on its position in time within the life of the asset. 3. The relationship between the resources used by the element and the resulting cost must be known. Changes in market conditions and price movements are more easily reflected through cost changes in specific resource types.

39

The information generated by a life-cycle cost analysis can assist managers at various stages in the life of an asset: planning and analysis of alternative solutions; selection of preferred options; securing funding; and review of predicted and actual outcomes.

40

LCC helps change provincial perspectives for business issues with emphasis on enhancing economic competitiveness by working for the lowest long term cost of ownership. Consider these typical events observed in most companies: · Engineering avoids specifying cost effective, redundant equipment needed to accommodate expected costly failures so as to meet capital budgets, · Purchasing buys lower grade equipment to get favorable purchase price variances, · Project engineering builds plants with a 6 month view of successfully running the plant only during start-ups rather than the long term view of low cost operation, · Process engineering requires operating equipment in race car driver fashion using a philosophy that all equipment is capable of operating at 150% of its rated condition without failure and they have other departments to clean-up equipment abuse, · Maintenance defers required corrective/preventive actions to reduce budgets, and thus long term costs increase because of neglect for meeting short term management gains. · Reliability engineering is assigned improvement tasks with no budgets for accomplishing the goals.

41

There are broadly three stages at which LCC should be applied. These are: the conceptual stage - when initial proposals for investment are being considered; the acquisition stage - when tenders for the supply of equipment, facilities or software are being assessed; and the in-service stage - when decisions are being made on whether to maintain, improve or dispose of the asset.

43

LCC analysis should begin by developing a plan that addresses the purpose and scope of the analysis. The plan should be to: define the objectives; identify the cost drivers and establish their parameters; apply the formula, and choose the appropriate discount rate; and analyse the results.

44

“It’s unwise to pay too much, but it’s foolish to spend too little” The adage attributed to John Ruston: End users and suppliers of equipment can use life-cycle costs for: · Affordability studies- measure the impact of a system or project’s LCC on long term budgets and operating results. · Source selection studies-compare estimated LCC among competing systems or suppliers of goods and services. · Design trade-offs- influence design aspects of plants and equipment that directly impact LCC.

45

· Repair level analysis- quantify maintenance demands and costs rather than using rules of thumb such as “…maintenance costs ought to be less than _ ? _% of the capital cost of the equipment”. · Warranty and repair costs- supplier’s of goods and services along with end-users need to understand the cost of early failures in equipment selection and use. · Suppliers sales strategies- can merge specific equipment grades with general operating experience and end-user failure rates using LCC to sell for best benefits rather than just selling on the attributes of low, first cost.

49

Lean Accounting will: 1.Provide accurate, timely, and understandable information to motivate the lean transformation throughout the organization, and for decision-making leading to increased customer value, growth, profitability, and cash flow. 2.Use lean tools to eliminate waste from the accounting processes while maintaining thorough financial control. 3.Fully comply with generally accepted accounting principles (GAAP), external reporting regulations, and internal reporting requirements. 4.Support the lean culture by motivating investment in people, providing information that is relevant and actionable, and empowering continuous improvement at every level of the organization.

, external reporting regulations, and internal reporting requirements. 4.Support the lean culture by motivating investment in people, providing information that is relevant and actionable, and empowering continuous improvement at every level of the organization..")

53

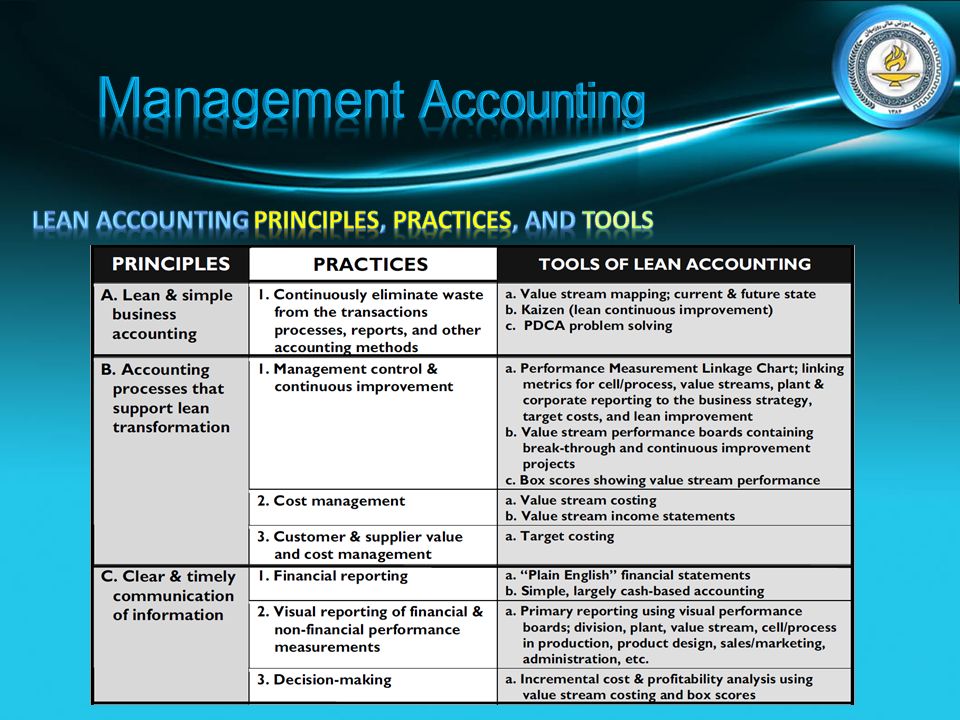

A. Lean and Simple Business Accounting This can also be stated as "applying lean methods to the accounting processes.“ Some accounting processes contain muda type 1 (waste that can not be eliminated at the moment) but most accounting processes are muda type 2 (waste that can be eliminated). The tools of lean must be rigorously applied to our accounting, control, and measurement processes so that waste is relentlessly driven out. B. Accounting Processes that Support the Lean Transformation Lean accounting reports and methods actively support the lean transformation. This information drives continuous improvement. The financial and nonfinancial reporting reflects the overall value stream flow, not individual products, jobs, or processes. Lean accounting focuses on measuring and understanding the value created for the customers, and uses this information to enhance customer relationships, product design, product pricing, and lean improvement.

but most accounting processes are muda type 2 (waste that can be eliminated). The tools of lean must be rigorously applied to our accounting, control, and measurement processes so that waste is relentlessly driven out. B. Accounting Processes that Support the Lean Transformation Lean accounting reports and methods actively support the lean transformation. This information drives continuous improvement. The financial and nonfinancial reporting reflects the overall value stream flow, not individual products, jobs, or processes. Lean accounting focuses on measuring and understanding the value created for the customers, and uses this information to enhance customer relationships, product design, product pricing, and lean improvement..")

54

Value Stream Costing Cost and profitability reporting is done using value stream costing, a simple Summary direct costing of the value streams. The value stream costs are typically collected weekly and there is little or no allocation of "overheads." This provides financial information that can be clearly understood by everybody in the value stream which in turn leads to good decisions, motivation to lean improvement across the entire value stream, and clear accountability for cost and profitability. Weekly reporting also provides excellent control and management of costs because they can be reviewed by the value stream manager while the information is still current. Target Costing Target Costing is the tool for understanding how the company creates value for the customer and what must be done to create more value. Target Costing is used when new products are being designed and/or when the value stream team needs to understand the changes required to increase value for the customers. The outcome of this highly cross-functional and cooperative process is a series of initiatives to create more value for the customer and to bring the product costs into line with the company's need for short-term and long-term financial stability. These improvement initiatives encompass sales and marketing, product design, operations, logistics, and administrative processes within the company.

55

C. Clear and Timely Communication of Information Lean accounting provides financial reports that are readily understandable to anyone in the company. The income statements are in "plain English" and the information is presented in a way that is no more complicated than a household budget. Plain English income statements are easy to use because they do not include misleading and confusing data relating to standard costs together with hosts of incomprehensible variance figures. When used in meetings, plain English financial statements change the question from "What does this mean?" to, "What should we do?" Visual Management Visual management is a cornerstone of lean management. Lean accounting requires visual presentation of both financial and non-financial measurements. The "Box Score" format commonly used in lean accounting provides a one-sheet summary for a value stream showing the operational performance, the financial performance, and how well the capacity is being used. Figure 2 shows an example of box score used for weekly performance reporting.

56

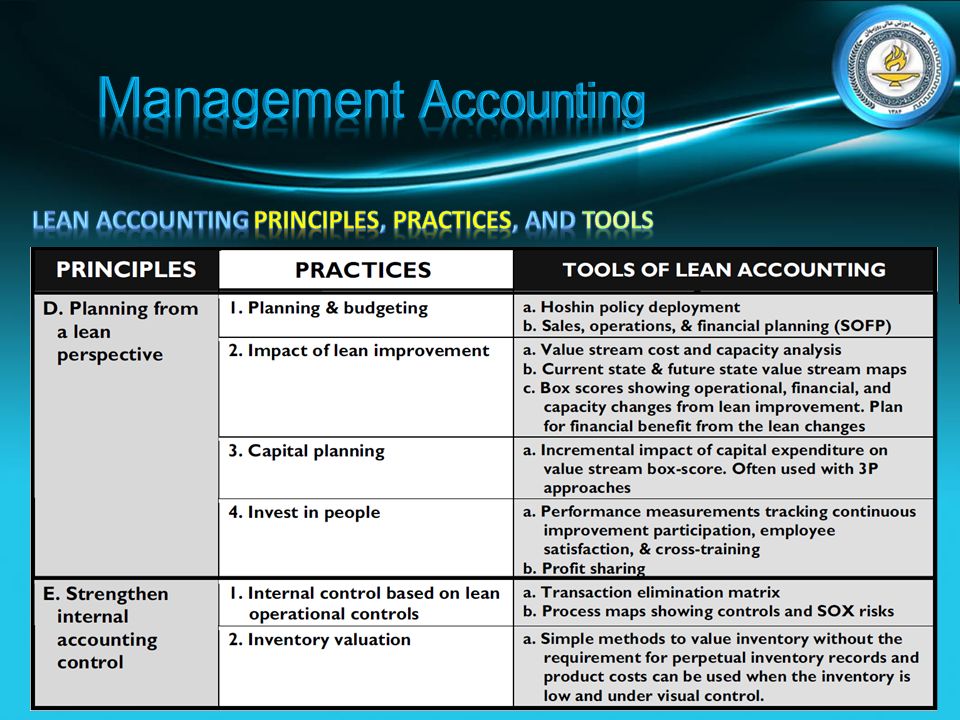

E. Strengthen Internal Accounting Controls Accounting controls have always been important, and it is essential that Lean Accounting enhance these controls, and does not weaken them. It is important to bring the company's auditors into the Lean Accounting process at the earliest stages. A primary tool to ensure that Lean Accounting changes are made prudently is the Transaction Elimination Matrix. Using the transaction elimination matrix we can determine what lean methods must be in place to enable us to eliminate traditional, transaction-based processes without Jeopardizing financial (or operational) control. These decisions are made ahead of time and become a part of the overall lean transformation; in some cases driving the lean changes and improvements.

control. These decisions are made ahead of time and become a part of the overall lean transformation; in some cases driving the lean changes and improvements..")

57

Conclusion While Lean Accounting is still a workin- process, there is now an agreed body of knowledge that is becoming the standard approach to accounting, control, and measurement. These principles, practices, and tools of Lean Accounting have been implemented in a wide range of companies at various stages on the journey to lean transformation. These methods can be readily adjusted to meet your company's specific needs and they rigorously maintain adherence to GAAP and external reporting requirements and regulations. Lean Accounting is itself lean, low-waste, and visual, and frees up finance and accounting people's time so they can become actively involved in lean change instead of being merely "bean counters." Companies using Lean Accounting have better information for decision-making, have simple and timely reports that are clearly understood by everyone in the company, they understand the true financial impact of lean changes, they focus the business around the value created for the customers, and Lean Accounting actively drives the lean transformation. This helps the company to grow, to add more value for the customers, and to increase cash flow and value for the stock-holders and owners.

Similar presentations

Assistant Professor CTI Office: Room 735 CTI 7th Floor Phone: 312-362-8231 Fax:>")

relationships and break-even analysis break-even chart – low fixed costs, high variable.>")

of business plan.>")