Download presentation

Presentation is loading. Please wait.

1

World Economic Outlook Warwick J. McKibbin ANU & The Brookings Institution Prepared for 1999 Conference of Economists Business Symposium

2

Overview An assessment of global forecasts in recent years Overall outlook Using a Global Model for Global Projections and Scenario Analysis The Consequences of a Wall St Collapse

3

An Assessment of Global Forecasts since the Asia crisis Most forecasters seem to have done pretty badly in 1998 and 1999 in the aftermath of the Asia crisis What happened to the global recession? –International capital flows misunderstood –Linkages between countries depend on the shock (a structural view of the world)

.")

4

Issues for the next year Asia Economies recovering quickly –consistent with model results for a risk shock rather than fundamental collapse

5

Issues for the next year Japan –fiscal stimulus is already passing though economy strong in 1999 but then weakens –need a significant monetary stimulus as part of the fiscal financing –exchange rate implications very different fiscal stimulus financed by bonds leads to strong Yen financed by money leads to a weak yen

6

Issues for the next year US - new economy or bubble? –New economy not convincing –(Robert J. Gordon results) Key is US stock market Likely scenario –capital flowing back to Asia lowers asset prices in the US which causes a reassessment of the equity risk premium

Key is US stock market Likely scenario –capital flowing back to Asia lowers asset prices in the US which causes a reassessment of the equity risk premium.")

7

Simulating a large adjustment on Wall Street

8

Using a DIGE model for forecasts The G-Cubed model so far has done a good job in projecting the consequences of the Asia crisis both for Asian economies and for the rest of the world. New World Bank study uses the model to look at a variety of internal and external risks to a sustainable recovery.

9

A number of models available The MSG2 Multi-country Model The G-Cubed Multi-country model –G-Cubed –G-Cubed (Asia Pacific) –G-Cubed (Agriculture)

–G-Cubed (Agriculture)")

10

The MSG2 Model Dynamic, Intertemporal, General Equilibrium Multi-Country Macroeconomic Keynesian short run with unemployment Mix of forward looking & rule of thumb behavior See WWW.MSGPL.COM.AU

11

Key dynamic features annual frequency physical capital is accumulation is endogenous but subject to adjustment costs forward looking agents in goods, factor and financial markets full accounting of stock flow relations combination of intertemporal optimization by agents plus liquidity constraints sticky nominal wages

12

Some Important Issues Trade, capital flows and adjustments in domestic financial markets are central to global adjustment to shocks; Agents arbitrage between different assets within countries and across countries - taking into account the adjustment costs of changing the physical capital stock in each sector.

13

What are Financial Assets? Each financial asset represents a claim over real resources –Money over purchasing power –Bonds are claims over future tax collections –Equity is a claim over the future dividend stream of a firm –Foreign assets are a claim over the future exports of the debtor country Asset values embody expectations of future real activities

14

Countries United States Australia Japan Germany United Kingdom Rest of EMU Rest of OECD High Income Asia Low Income Asia Oil Exporting Developing Countries Eastern Europe and the former Soviet Union Other Developing Countries

15

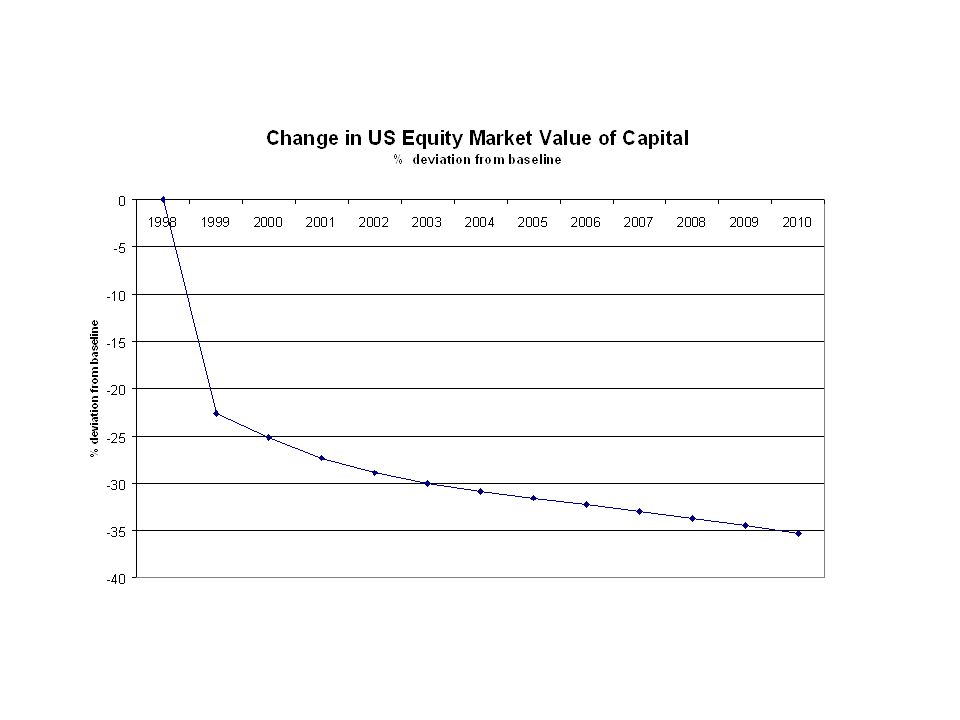

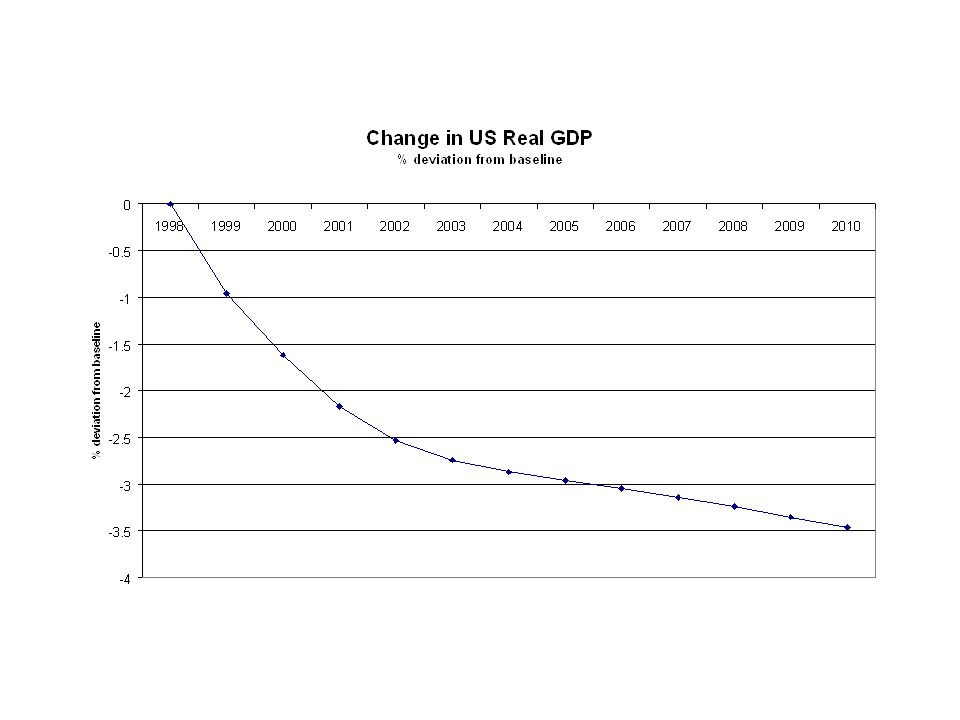

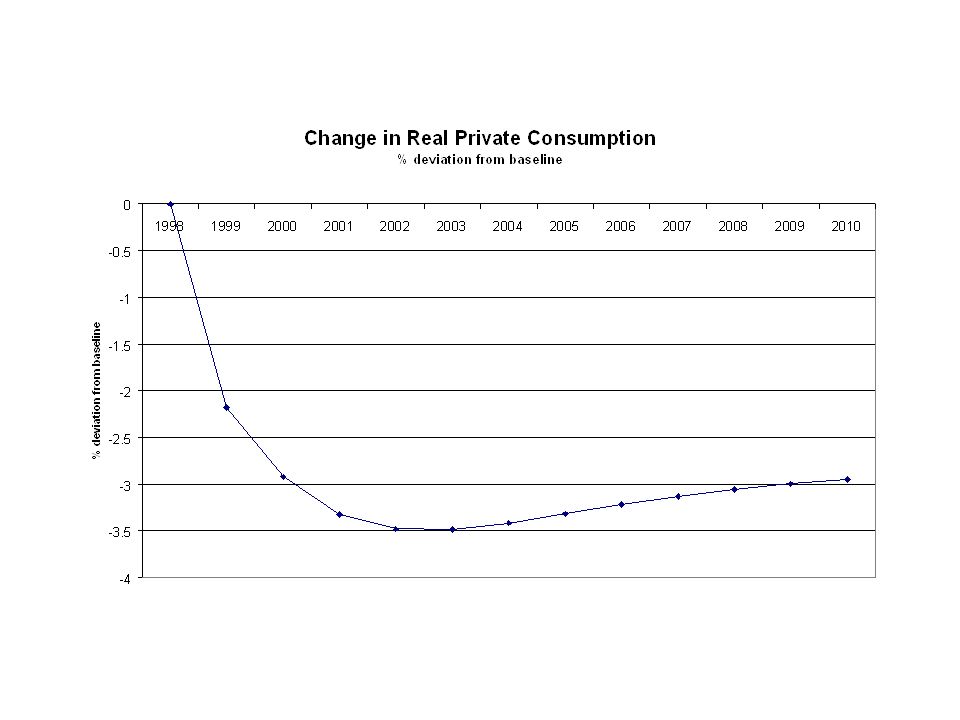

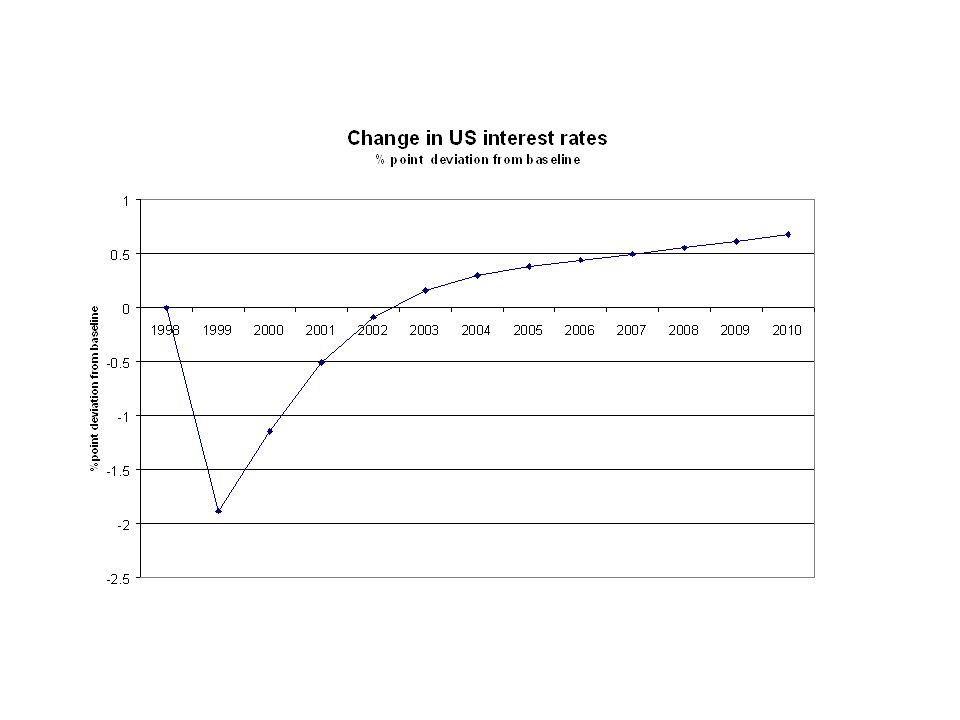

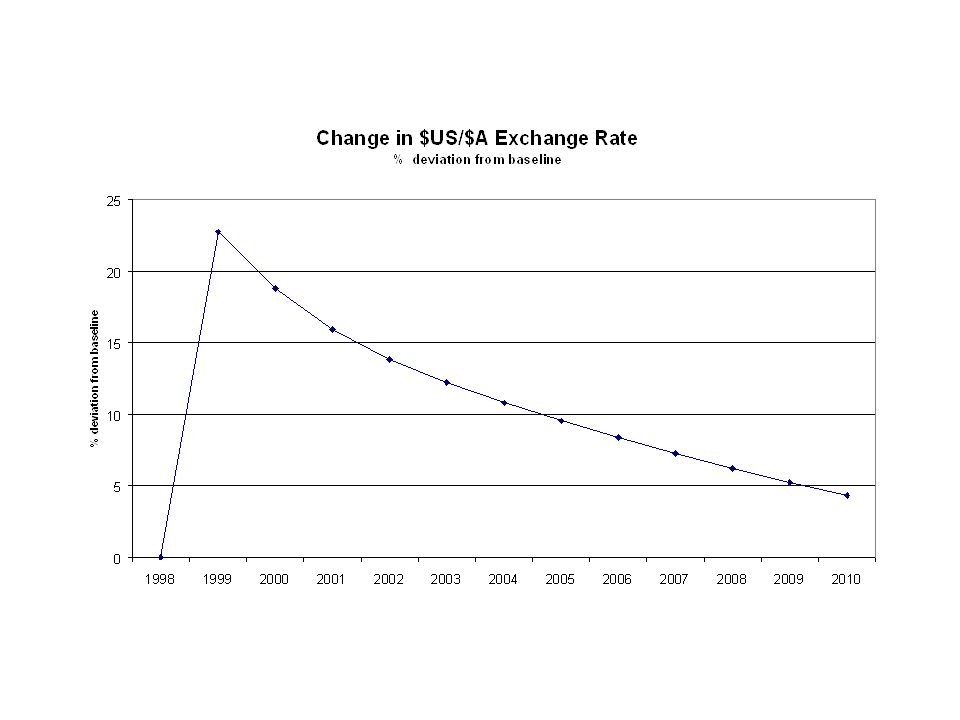

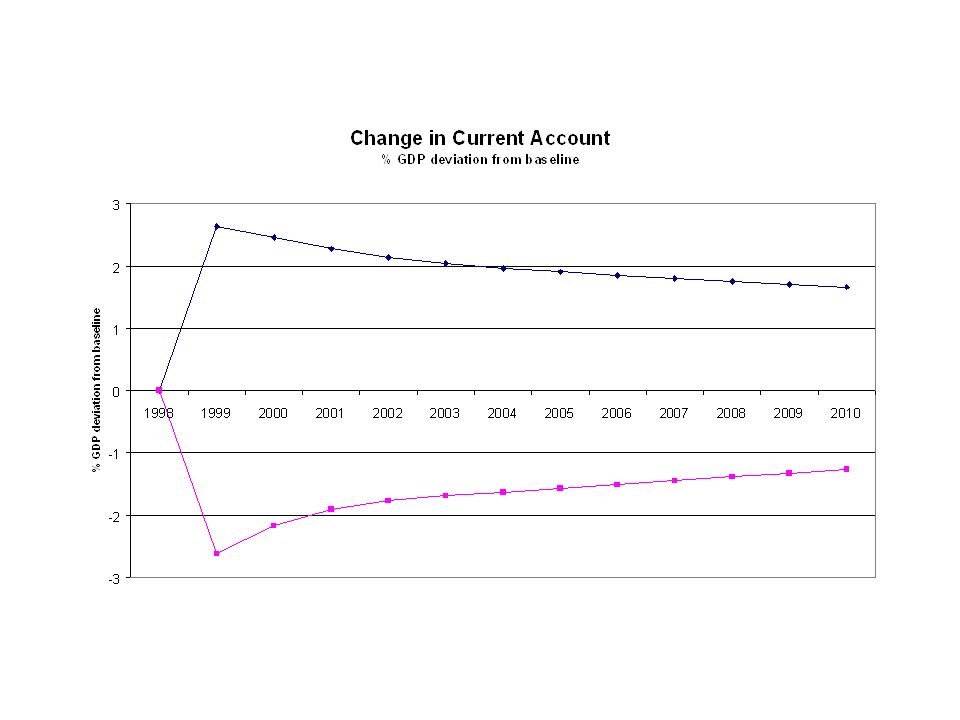

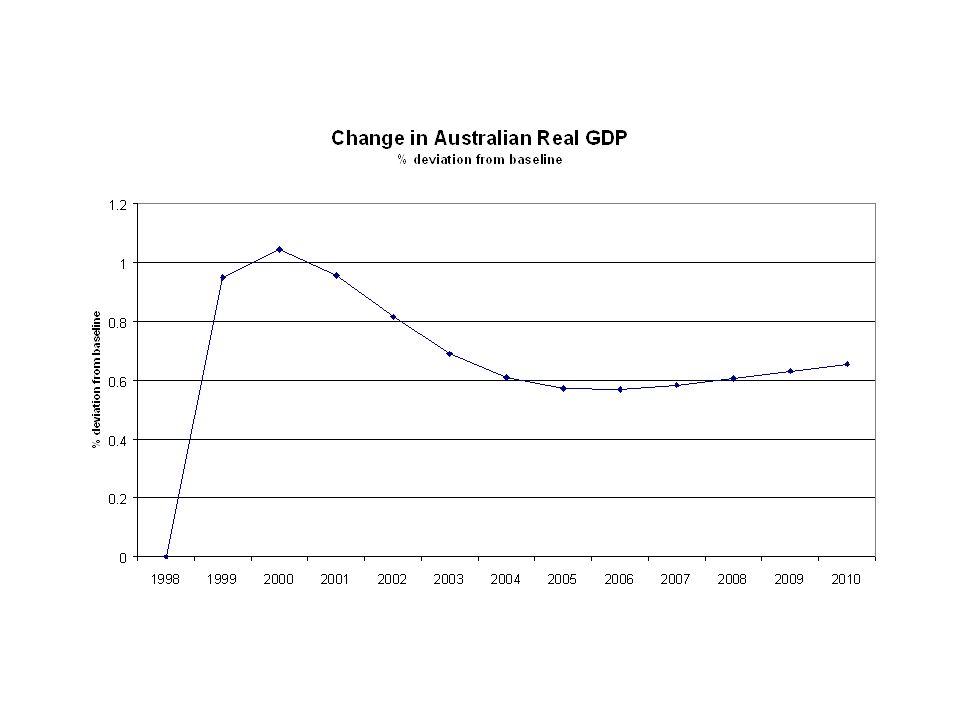

Simulating a Wall St fall Part of the current adjustment on Wall St is due to capital flowing back into Asia Simulation is an increase in the Equity risk premium in the US only from 0 to 5% in 1999

23

Summary The US economy slows but doesn’t go into recession because of stabilizing offsets –interest rates (lower) –exchange rates (weaker $US) Transmission to other countries is not necessarily negative because of capital flow effect versus trade effect

–exchange rates (weaker $US) Transmission to other countries is not necessarily negative because of capital flow effect versus trade effect")

24

Summary Critical what happens to risk premia in other countries –if no change in risk premia outside the US then small effect and positive for Australia –if all risk premia rise then significant global slowdown

25

Papers can be downloaded from: WWW.MSGPL.COM.AU WWW.BROOK.EDU

Similar presentations

International financial system The rise, crisis, and.>")

–is corrected.>")

Pertemuan 3-4.>")