Download presentation

Presentation is loading. Please wait.

2

Explicit Implicit Economic cost: total cost of choosing one action over another. (Explicit + Implicit costs) (explicit costs). Accounting costs: the actual expenses incurred in the production process (explicit costs). Explicit costs: Explicit costs: the monetary payments for the factors of production and other inputs bought or hired by the firm. Eg. – rent, raw materials, wages, electricity. Implicit costs: Implicit costs: those opportunity costs which are not reflected in monetary payments. Eg. – salary that could have been earned.

(explicit costs). Accounting costs: the actual expenses incurred in the production process (explicit costs). Explicit costs: Explicit costs: the monetary payments for the factors of production and other inputs bought or hired by the firm. Eg. – rent, raw materials, wages, electricity. Implicit costs: Implicit costs: those opportunity costs which are not reflected in monetary payments. Eg. – salary that could have been earned..")

3

accountingeconomic costs A quick story to explain accounting and economic costs… Bob is a teacher who earns R100 000 a year (this includes his salary, medical aid and pension benefits). He also has R50 000 in a savings account. Bob decides to retire from teaching and start his own business making bean bags. He uses R50 000 from his savings account to purchase the machinery and equipment required to start his business. What are the accounting (explicit) costs involved in this decision? What are the accounting (explicit) costs involved in this decision? What are the economic (explicit + implicit) costs involved in this decision? What are the economic (explicit + implicit) costs involved in this decision?

costs involved in this decision. What are the accounting (explicit) costs involved in this decision. What are the economic (explicit + implicit) costs involved in this decision. What are the economic (explicit + implicit) costs involved in this decision .")

4

Profit: revenue – cost of producing it. Total (accounting) profit: total revenue – total explicit costs Normal profit: equal to the best return that the firm’s resources could earn elsewhere Economic profit: total revenue - total explicit and implicit costs (including normal profit).

profit: total revenue – total explicit costs Normal profit: equal to the best return that the firm’s resources could earn elsewhere Economic profit: total revenue - total explicit and implicit costs (including normal profit)..")

5

Total revenueR320 000 Raw material costsR30 000 Wages and salariesR85 000 Interest paid on bank loanR30 000 Salary that the owner could have earned elsewhereR32 000 Interest forgone on capital invested in the businessR20 000 a) Normal Profit b) Economic Profit Calculate… a) Normal Profit b) Economic Profit

Normal Profit b) Economic Profit Calculate… a) Normal Profit b) Economic Profit")

7

Production: the physical transformation of inputs into output. Short run production: a period of time when there is at least one fixed factor input. Fixed factor usually quantity of plant / machinery Long run production: a time period in which all of the factors of production can change.

8

input whose quantity cannot be altered in the short run. Fixed input: input whose quantity cannot be altered in the short run. input whose quantity can be changed in the short run (as well as the long run). Variable input: input whose quantity can be changed in the short run (as well as the long run).

. Variable input: input whose quantity can be changed in the short run (as well as the long run)..")

9

The firm produces only one product. units of input are identical/homogeneous. Inputs can be used in infinitely divisible amounts. Prices of the product and of inputs are given. Firm uses fixed inputs and one variable input.

10

Length of time between the short and the long run will vary from industry to industry.

11

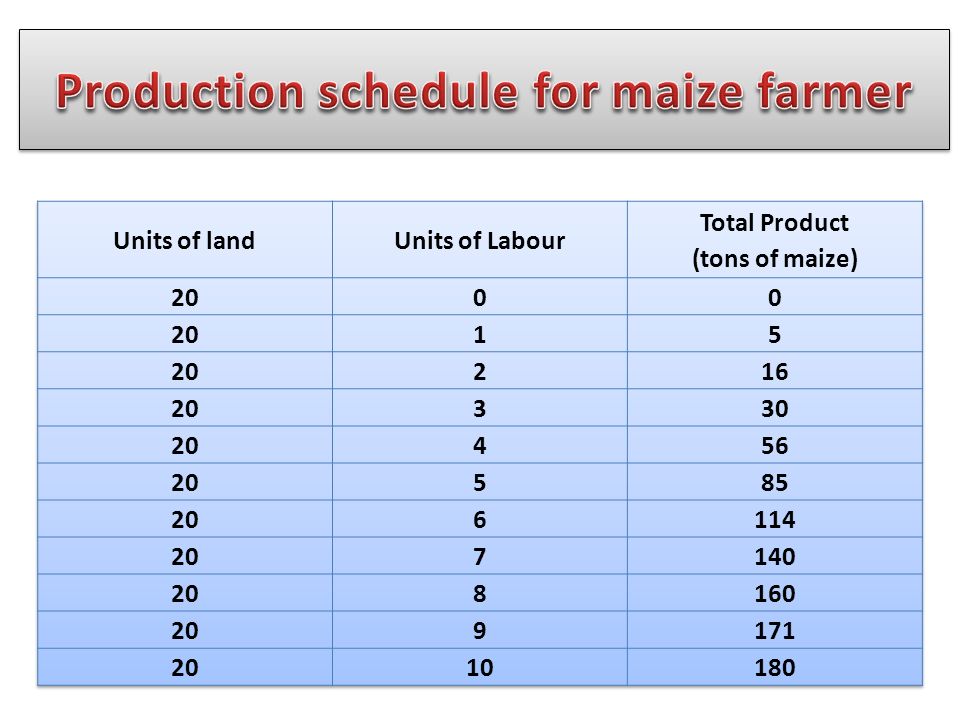

Fixed quantity of land = 20 units Variable input = labour

13

Units of labour

14

ACTIVITY: ACTIVITY: investigate relationship between output (total product) and quantities of variable factors of production used.

and quantities of variable factors of production used.")

15

By the end of this simulation you must understand… The law of diminishing returns The difference between total, average and marginal concepts The difference between 'production' and 'productivity' The difference between short run and long run

16

You have an imaginary factory. You have to move hockey balls from one bucket to another. On successful transfer of a ball from one bucket to the other, your firm generates one unit of output. Fixed factors (capital) Fixed factors (capital) - 2 buckets, batch of hockey balls & land. Variable factor – labour Variable factor – labour (that’s where you come in!) At the end of each production run, the firm will add an extra unit of labour to production. Production levels will be recorded at the end of each production run. Your must monitor the output levels with each different combination of inputs.

Fixed factors (capital) - 2 buckets, batch of hockey balls & land. Variable factor – labour Variable factor – labour (that’s where you come in!) At the end of each production run, the firm will add an extra unit of labour to production. Production levels will be recorded at the end of each production run. Your must monitor the output levels with each different combination of inputs..")

17

You may not throw the balls. Balls must not be dropped into the bucket - if they are, they are counted as damaged goods and do not count towards final output. Any balls dropped between the buckets also become damaged goods. Each production run lasts for 30 seconds - you must keep strictly to this time limit.

20

Can you explain the law of diminishing returns using our maize farmer example?

21

Marginal product: the number of additional units of output produced by adding one additional unit of the variable input. Average product: the average number of total output produced by each unit of variable input.

22

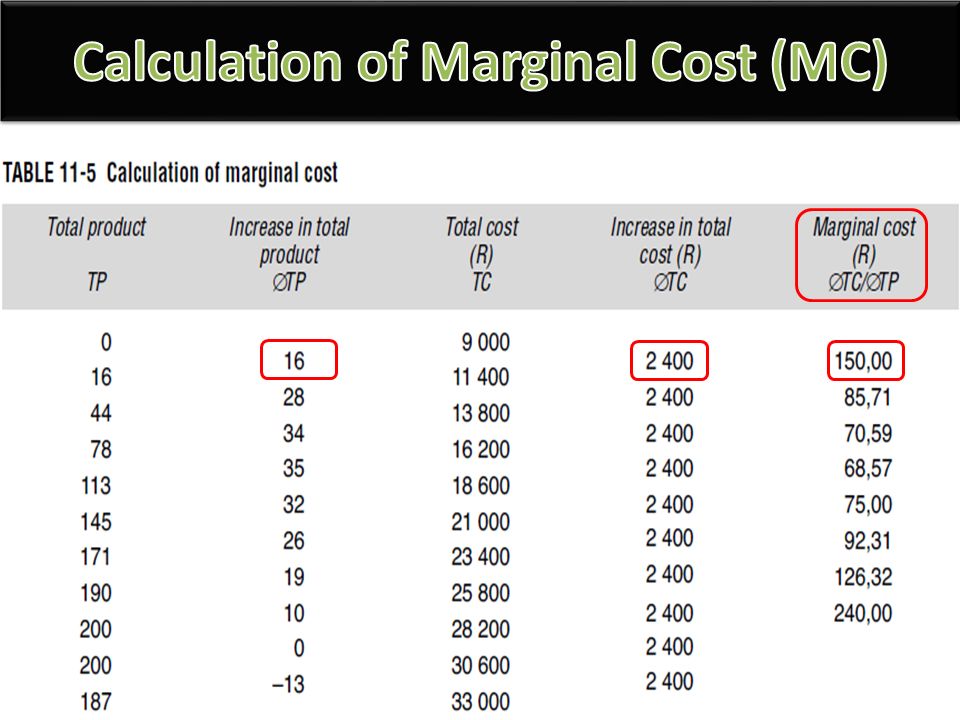

Marginal product of 1 st unit of labour 16 – 0 = 16 tons Total product of first 2units of labour = 44 tons Marginal product of 2 nd unit of labour 44 – 16 = 28 tons Highest marginal product 113 – 78 = 35 tons (N = 4) Once maximum MP reached - it keeps on declining. 9 th unit of labour adds nothing 200 – 200 = 0 tons

23

AP of 1 st unit of labour 16 ÷ 1 = 16 tons Highest AP 145 ÷ 5 = 29 tons

24

TP will continue to increase as long as MP is positive AP & MP shaped like inverted “U”s rise at declining rates - reach max - decrease at increasing rates AP & MP shaped like inverted “U”s rise at declining rates - reach max - decrease at increasing rates increases AP increases when MP > AP decreases AP decreases when MP < AP increases AP increases when MP > AP decreases AP decreases when MP < AP MP equals AP at its maximum point. MP equals zero where TP reaches its maximum.

25

BOX 6-1 TOTAL, AVERAGE AND MARGINAL MAGNITUDES

26

Costs: expenses faced by a business when producing a good or service for a market. Short run - fixed and variable costs. Fixed Costs Fixed costs: cost that remains constant irrespective of the quantity of output produced. Examples of fixed costs include: Rent Insurance charges. Salaries Interest charges on borrowed money. The costs of purchasing new capital equipment. Marketing and advertising costs.

27

Variable Costs Variable costs: costs that vary directly with output. As production rises - higher total variable costs as extra resources purchased. Examples of variable costs for a business include: The costs of raw materials Labour costs Consumables and components used directly in the production process.

28

Total product

31

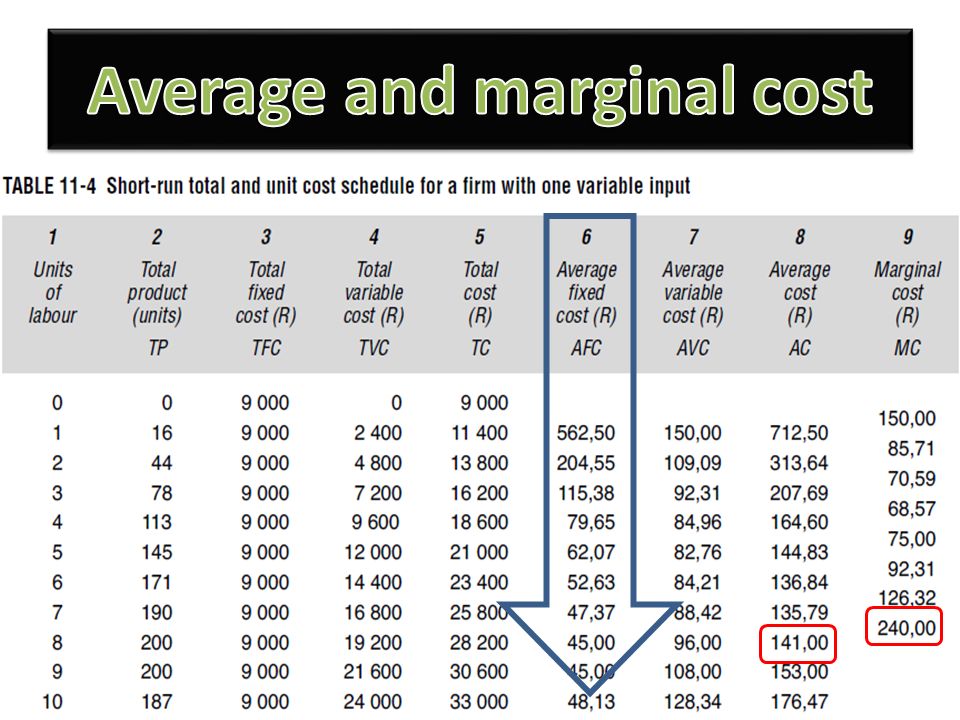

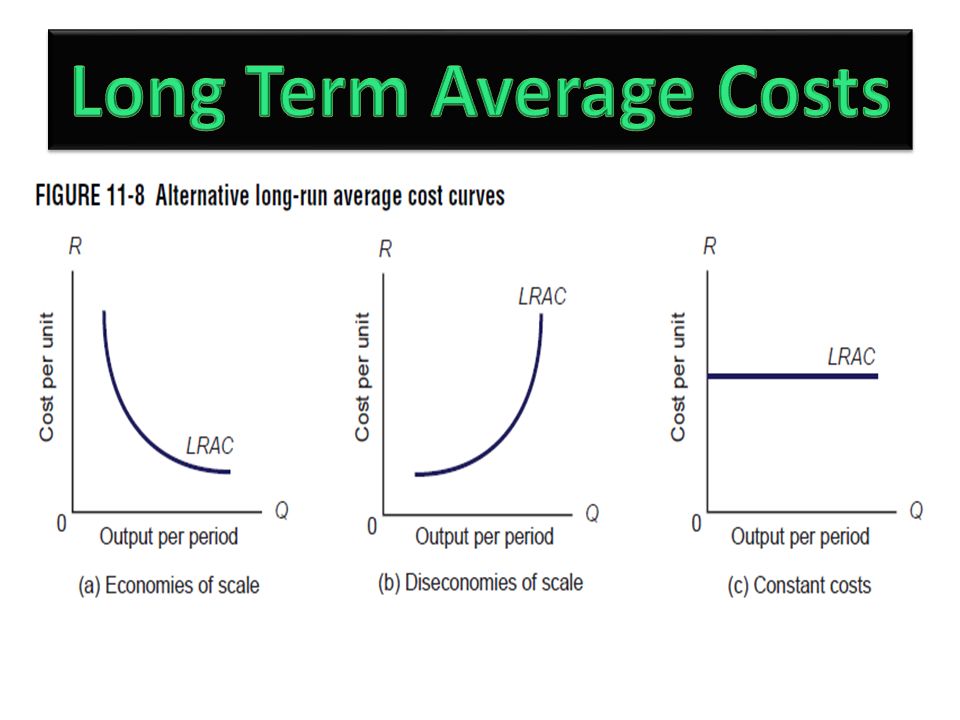

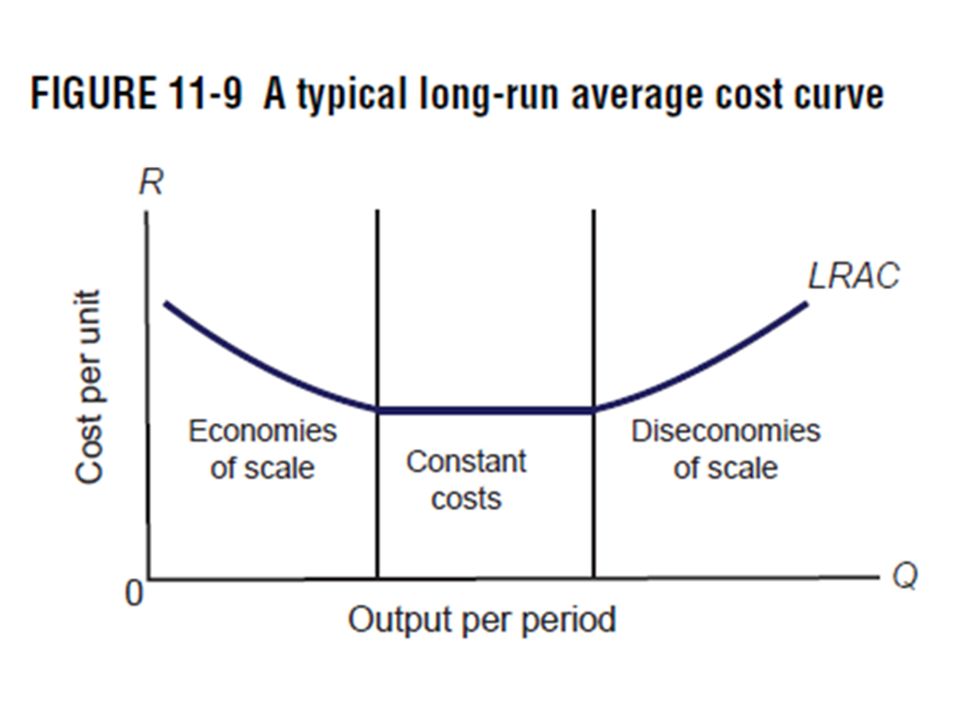

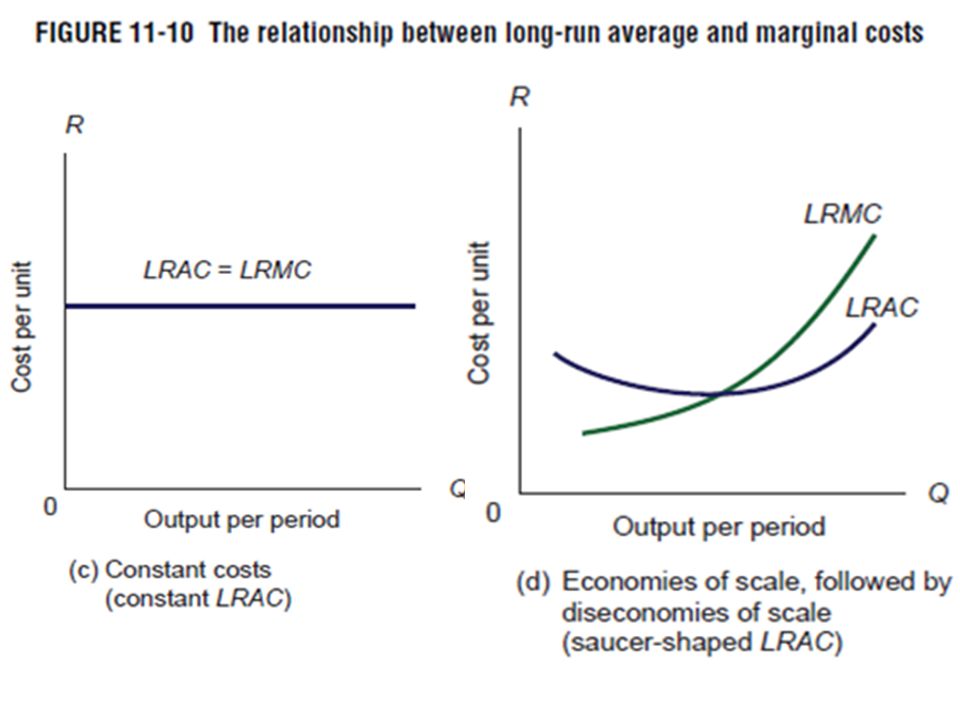

AFC is L-shaped starts very high - declines till max TP reached AVC, AC & MC are U-shaped start high - decline at decreasing rates - reach minimum points - increase at increasing rates AC lies above AFC and AVC because it includes them both MC equals AVC and AC at their respective minimum points

32

The shape of the unit cost curves is determined by the shape of the unit product curves.

33

Output Q1 is the total output produced by N1 units of labour. Output Q2 is the total output produced by N2 units of labour

34

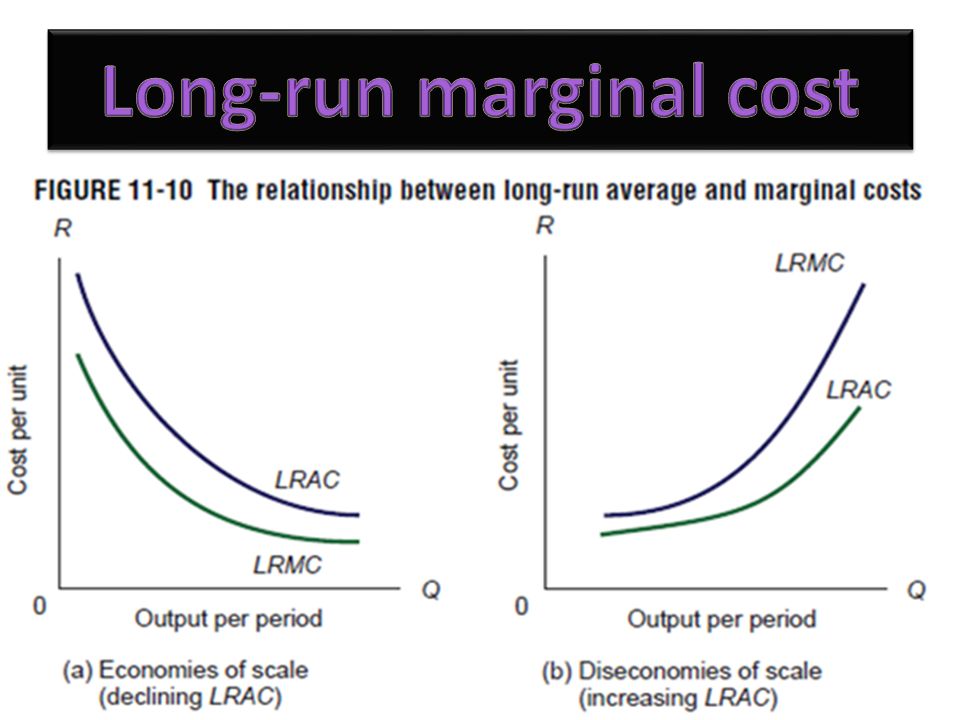

Long run: a time period where there are no fixed inputs – all the inputs (including all the factors of production) are variable. Enough time to build a new factory, install new machines, use new techniques of production etc… Law of diminishing returns does not apply - all the costs are variable. Marginal product has no meaning - can only be calculated if all the other inputs are held constant.

35

Returns to scale: long-run relationship between inputs and output. all Measured by varying all inputs by a certain % and comparing resulting percentage in production. Three possible situations can result… Constant Constant returns to scale Given % increase in inputs = same % increase in output Increasing Increasing returns to scale Given % increase in inputs = larger % increase in output Decreasing Decreasing returns to scale Given % increase in inputs = smaller % increase in output

36

Decreasing returns to scale (long run concept) – ALL inputs increase by the same proportion. only variable input increases. Diminishing marginal returns (short-run concept) - only the variable input increases.

- only the variable input increases..")

37

Economies of scale: occur when costs per unit of output fall as the scale of production increases. Diseconomies of scale: occur when unit costs rise as output increases. Both can be internal and external Internal: Internal: specific to a firm –can be controlled. External: External: outside the firm’s control – affects entire industry/economy.

38

Technical economies: Technical economies: modern technology suited to mass production Managerial, organisational or administrative economies: Managerial, organisational or administrative economies: specialisation and division of labour Marketing economies: Marketing economies: bulk discounts & CPT decreases Financial economies: Financial economies: easier/cheaper to raise. Average fixed charges decline. Spreading overheads: Spreading overheads: Average fixed costs lower as firm grows.

39

Internal diseconomies of scale Managerial diseconomies: Managerial diseconomies: longer lines of communication, management less directly involved. Worker alienation: Worker alienation: specialised, boring and repetitive jobs – motivation & productivity affected. Deteriorating industrial relations: Deteriorating industrial relations: increased work stoppages and strikes.

40

Industry economies: Industry economies: Specialised markets – benefits raw materials, selling finished product; specialised labour skills General economies: General economies: general infrastructural development & better workers and may lower the effective cost of labour.

41

Shortage: Shortage: raw materials, skilled labour – unit costs rise Congestion: Congestion: land prices, traffic, pollution.

42

Economies of scope: the cost savings achieved by producing related goods in one firm rather than in two.

47

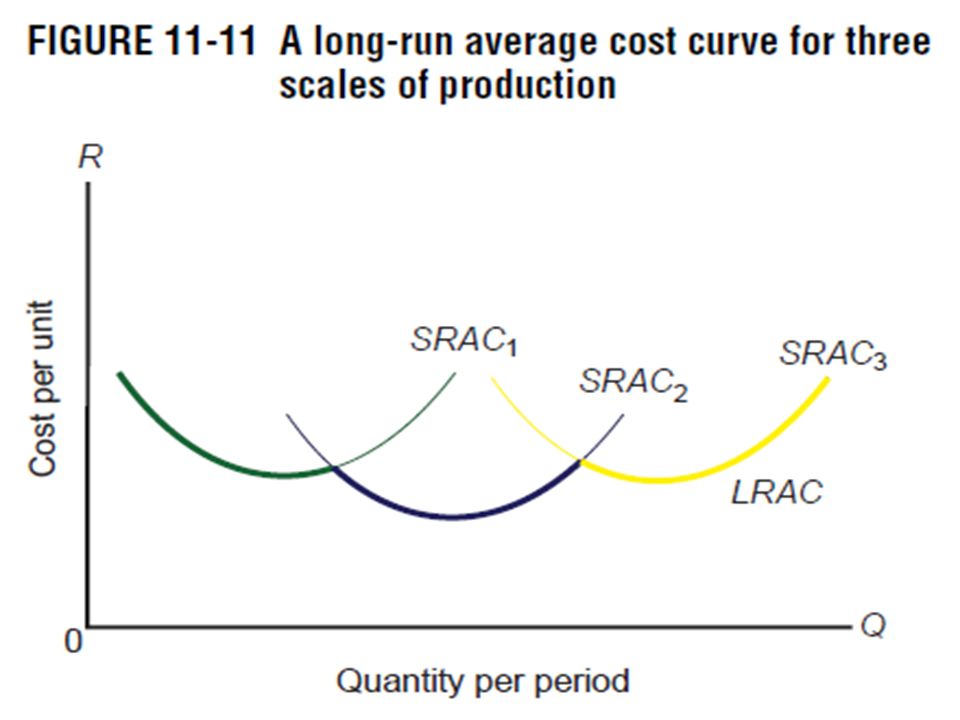

variablelongruntotal averagefixedcosts All inputs variable in long run therefore no total or average fixed costs. The long run can be seen as a set of alternative short-run situations between which the firm can choose.

Similar presentations