Download presentation

Presentation is loading. Please wait.

1

National Innovation System and the Role of National Institute

Prof Otto C C Lin The Hong Kong University of Science & Technology Clear Water Bay, Kowloon, Hong Kong Tsing-Tech Innovations, Ltd New World Centre, Tsim-sha-Tsui, Kowloon, Hong Kong Six Countries Programme Conference, Canada June 5-6, 2003

2

Outline From science to industry: the myths

The Innovation process and the players The national innovation system A case study of Taiwan: The roots of hi-tech industry The way forward

3

Hi-Tech Industry Technology Science

4

Hi-Tech Industry National Vision Physical Infrastructure Strategy

Policy Commitment R&D Funding Taxation & Banking Legal System Regional Planning Physical Infrastructure Basic Sciences Education & Skilled Workforce Entrepreneurship Venture Capital Social Support Project Management

5

The Research to Commercialization Process

Basic Research Sales & Services Product & Process Development Pilot Production & Field Trial Applied Research Manufacturing Research Science Development Industrial Technology Mid-stream R&D Commercialization

6

Mission Jobs/Outputs Criteria Success Talents needed Difference

Commercialization Research Mission Jobs/Outputs Criteria Success Talents needed Rewards system Risk Difference Similarity Excellent People Excellent Management

7

The Innovation Process: Creating Wealth from Knowledge

Applied Research Product Development Process Development Pilot Production Technology Diffusion Developing Industrial Technology Scientific Research Product Commercialization Policy / Planning / RD Funding Taxation/Legal Systems Infrastructure Skilled Manpower VC Funding / Entrepreneurship Social Support and Stability Nurturing Business Environment

8

National Innovation System: the Players

© Professor Otto C C Lin March 2002 National Innovation System: the Players Developing Industrial Technology INSTITUTE BUSINESS INDUSTRY UNIVERSITY Nurturing Business Environment GOVERNMENT

9

The National Innovation System: The Dynamics

Technology Development INSTITUTE BUSINESS UNIVERSITY Scientific Research Product Commercialization GOVERNMENT

10

National Innovation System: The Role of the Institute

Business Government Pilot Production Product & Process Development Applied Research Technical Services Manufacturing Industrial Technology Basic Focus Funding UNIVERSITIES Institute ?? INDUSTRIES

11

National Innovation System: USA

Basic Research Industrial Technology Manufacturing Technical Services Focus Applied Research Product & Process Development Pilot Production Funding Government UNIVERSITIES NATIONAL INSTITUTES NATIONAL LABORATORIES INDUSTRIES Business

12

The Economic Growth of Taiwan

13

THE STRATEGY: A Case Study of Taiwan

A Developing Human Resources B Acquiring Foreign Technologies C Establishing Indigenous Technology Capability Converting Science / Technology to Industry Ref: O. C. C. Lin, in “Behind East Asian Growth: the political and social foundation of prosperity ,” Editor, H.S. Rowen. Rutledge, 1998

16

National Innovation System : Taiwan

Manufacturing Focus Basic Research Industrial Technology Technical Services Funding Applied Research Product & Process Development Pilot Production Government Academic Sinica Universities Industrial Technology Research Institute (ITRI) All INER, FIRDI, MIDC, CBD, III, TL, CPC Aerospace Pollution Control Industrial Safety Industrial Standards Materials Energy Chemicals Machinery Micro-Electronics Opto-Electronics Computer & Communications ITRI SCIENCE-BASED INDUSTRIAL PARK (Host for Hi-Tech Companies) Business Industrial Companies

All. INER, FIRDI, MIDC, CBD, III, TL, CPC. Aerospace. Pollution Control. Industrial Safety. Industrial Standards. Materials. Energy. Chemicals. Machinery. Micro-Electronics. Opto-Electronics. Computer & Communications. ITRI. SCIENCE-BASED INDUSTRIAL PARK. (Host for Hi-Tech Companies) Business. Industrial Companies.")

17

Industrial Technology Research Institute (ITRI)

Founded in 1973 A statutory national institute established by law A non-profit R&D corporation under the auspices of the Ministry of Economic Affairs (MOEA) The technical arm of the government’ s industrial policies A partner to local industries

The technical arm of the government’ s industrial policies. A partner to local industries.")

18

ITRI Missions To spearhead the development of high-tech industry in Taiwan To upgrade the competitiveness of traditional industries in the global market

19

ITRI: Scope of R&D Activity

ELECTRONICS MATERIALS CHEMICALS VLSI Fabrication IC Design Flat Planel Display Microwave Technology Electronics Packaging Material Design Material Application Material Reliability Improvement New Material Chemical Engineering Process Applied Chemistry Speciality Chemicals and Pharmaceuticals Polymera and Fibers COMPUTER & COMMUNICATIONS ENERGY & RESOURCES Computer Communication Consumer Electronics Energy Conservation Systems Design Resource Application Environment Engineering ITRI OPTO-ELECTRONICS MACHINERY Optical Information Electro-Optical Components & Materials Optical Components & Systems Automation Precision Machinery Power Machinery Precision Parts & Components METROLOGY INDUSTRIAL SAFETY & HEALTH INDUSTRIAL POLLUTION CONTROL National Measurement Standards Laboratory Accreditation Industrial Quality Assurance & Service Measurement Technology & Instrumentation AEROSPACE Chemical Accident Prevention Industrial Hygiene Engineering Safety Treatment & Control Waste Reduction & Reuse Pollutant Analysis & Monitoring Quality Assurance Aviation System & Components Inspection/Testing Market & Technology Information

20

Impacts of ITRI Technology I. Establishing New Technology / Industry

VLSI Computing Communication Materials Sp. Chemicals Automation Opto-Electronics IC: CMOS DRAM/SRAM PC Peripherals Telecom, ISDN PLC Auto Engine ELE Components & Parts

21

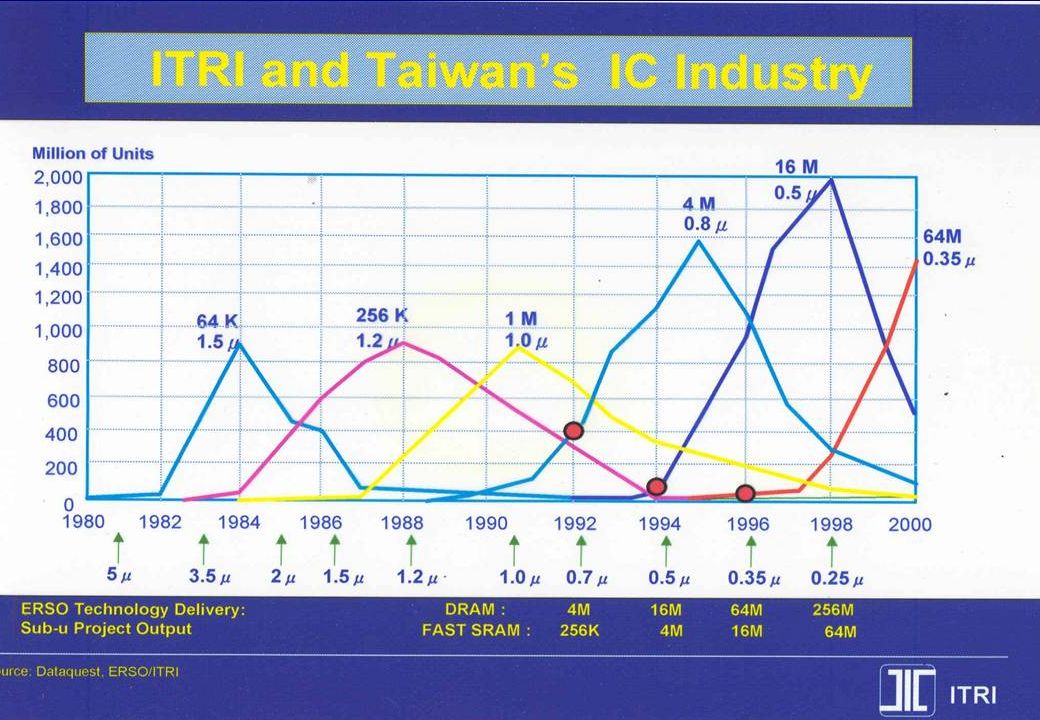

Taiwan IC Company Family Tree (Ref: Dr. F.C. Tseng, 2002)

1980 : First IC Co. UMC Team 2μm , CMOS Team 3.5μm , CMOS TSMC 1987 : First Foundry 6-inch Fab. IC Products Team 2μm , CMOS 7μm , CMOS ERSO /ITRI Winbond 1987 : First IDM RCA IC Products (3-inch Fab.) Team 0.5μm , CMOS 1974 :Technology Transfer Vanguard 1994 :First DRAM 8-inch Fab. SRAM/DRAM Products TI IPR TI-Acer 1992 :First JV DRAM DRAM Tech.

Team. 0.5μm , CMOS :Technology Transfer. Vanguard :First DRAM. 8-inch Fab. SRAM/DRAM. Products. TI. IPR. TI-Acer :First JV DRAM. DRAM Tech.")

22

Taiwan IC Outperform WW IC

$M USD Source: ITIS/IEK, Nov-2001; SIA, Jan-2002

24

Foundry Business Model

IDM/ASIC Fabless Co. IDM/ASIC IDM/ASIC Fabless Co. System Co. System Design System Design System Design IP System Design IC Design IC Design IC Design IC Design IC Design System/IC Design Design Services Foundry Fab Fab Fab Foundry Assembly & Test Assembly & Test Contract Assembly & Test Assembly & Test Assembly & Test Before 1986 1990s After 2000

25

Outlook Taiwan IC Industry

M US$ 23% 36% 31% CAGR= 31% 40,000 IC Testing 34,721 IC Package 35,000 IC Design IC Fab 30,000 25,332 25,000 18,056 20,000 15,558 15,000 10,000 5,000 - 2001(e) 2002(f) 2003(f) 2004(f) Source: ITIS/IEK, Mar-2002

2002(f) 2003(f) 2004(f) Source: ITIS/IEK, Mar")

26

Fabless Industry Growth

Numerous Fabless Companies Were Formed Since 1987 Taiwan From 10 to over 200 Many successful IPOs: VIA, Acer Lab, SIS, Realtek, Sunplus etc. US Several hundreds Many successful IPOs: Cirrus, Trident, ISSI, S3, nVidia, ATI, Broadcom, Oak, ESS, C-Cube, Mosys, Altera, PMC-Sierra etc. China Emerging with more than 100 companies

27

Taiwan IC Key Success Factors (Ref.Dr. F. C. Tseng, 2002)

1. Insightful Government Policies and Effective Execution Industry Policies Strategic Industries ITRI Financial Policies Government VC arms IPO for hi-tech companies Successful Commercialization Tax shelters and RD incentives Shielded from government bureaucracy Science park

28

Taiwan IC Key Success Factors (Ref: Dr. F. C. Tseng, 2002)

3. Good Model of Innovation Technology Continued own development to be among the leaders Business Model Foundry/Fabless model Human Resources Many local universities and technical institutes. Thorough training in fundamentals Advanced degrees in US universities RD/management experiences in leading SC companies

29

Notebook PC Consortium

Project Management Project Leaders The Team Motherboard (Hitran) Components (King Tel) CCL EMI / Battery (Wiso) Mechanical Design (Tek Star) ITRI CCL TEAM A Software (Cal Roc) Testing (CCL) Reliability (CCL) PARTNERS System Integration (CCL) Promotion (TEAMA)

Components (King Tel) CCL. EMI / Battery (Wiso) Mechanical Design (Tek Star) ITRI. CCL. TEAM A. Software (Cal Roc) Testing (CCL) Reliability (CCL) PARTNERS. System Integration (CCL) Promotion (TEAMA)")

30

* Reference: MIC / IDC * Estimated for 2000

31

CD-ROM/DVD-ROM Production Scale Forecast World v.s. Taiwan

The Taiwanese forecast volume will reach 45 Million units, at 40% world market share

32

The Industrial Strength

34

Impacts of ITRI Technology

II. Upgrade Existing / Traditional Industry • Design • Sporting: Bicycles, Tennis rackets, Golf clubs • Material • Plated Plastics • Manufacturing • Machine Tools / Parts • Quality - EHS • Fashion Fabrics • Pharmaceuticals • Green processes

35

30

36

31

37

Composite Materials Technology

CAD Design Polymer Matrix Fibre Reinforcement Processing Fabrication New Product Metal Parts Materials Joining Non- Destructive Evaluation Performance Testing

38

ITRI: Characteristics of Projects

Specificity Niche Advantage Market Orientation Economic Feasibility Industry Participation Transfer Mechanism Championship

39

ITRI: Technology Diffusion

Technology Licensing Contract Services Technology Spin-off Strategic Alliances Workshops and Training Programs Technical Publication

40

ITRI: Technology Output

Item 1994 1995 1996 1997 1998 Technology Transferred to Industry Technologies Companies 264 452 280 418 304 465 332 499 340 510 Services Contracts Number 904 1,004 1,019 1,050 General Services to Industry 20,177 27,061 26,253 27,811 28,000 Patents Granted 368 381 447 548 560 Technology Conferences and Training Programs Cases Attendees 898 52,074 880 59,492 830 56,572 957 68,918 69,000

41

ITRI: Intellectual Property Rights - Patents Awarded and Inventions

42

ITRI: Contributions to Taiwan

Establishing new high-tech industries Upgrading traditional industries Developing human capital Protecting the environment & increasing industry safety

43

Structural Change of Manufacturing Industry: Taiwan (1986 - 1998)

1995 1998 Manufacturing, as %GDP As % of Manufacturing: Capital Intensive Labour Intensive Technology Intensive Technology Manpower % of (Total Employment) R&D, as % Sales (7.73M) (9.04M) (9.17M) Source: Cheng Sun, “Development of Knowledge Economy in Taiwan” (Chinese) 2001, Sun Min Books, Taipei, 2001 Data from (MOEA & NSC)

R&D, as % Sales (7.73M) (9.04M) (9.17M) Source: Cheng Sun, Development of Knowledge Economy in Taiwan (Chinese) 2001, Sun Min Books, Taipei, Data from (MOEA & NSC)")

44

Shares of Taiwan’s Manufacturing Enterprises 1971-1996 (Unit: %)

Employment size (persons) 1-99 >500 By number of enterprises By persons engaged By value added Data Source: Industrial & Commercial census, Executive Yuan, Taiwan, ROC, Reference: M-W Hu, Futures 35 (2003)

>500. By number of enterprises By persons engaged By value added Data Source: Industrial & Commercial census, Executive Yuan, Taiwan, ROC, Reference: M-W Hu, Futures 35 (2003)")

46

Source : Lee, Miller and Rowen, “ The Silicon Valley Edge”, 2000

47

The Features of the Silicon Valley Habitat

Knowledge intensity High quality and mobile work force Result Oriented meritocracy Climate that rewards risk-taking and tolerates failure Favorable government policies Open business environment University-Institute-Industry interactions Collaboration : business, government and non-profits High quality of life Specialized business infrastructure Ref: Lee, Miller, Hancock, Rowen, “The Silicon Valley Edge,” Stanford University Press, 2000

48

The Roots of Hi-Tech Industry Resources Knowledge Network Capital Infrastructure Human Leadership

49

The Roots of High Tech Industry

LEADERSHIP RESOURCES National vision Strategy content Policy commitment KNOWLEDGE RESCOURCES Basic research R&D support Technology capacity HUMAN RESOURCES Education Training & Re-education Entrepreneurship Project management CAPITAL RESOURCES Taxation Banking practices Venture capital INFRASTRUCTURE RESOURCES Physical infrastructure Legal system Social support Effective governance NETWORK RESOURCES Globalization culture Regional planning Marketing Channel

50

The Changing World. Three axes of change:. Technology. Globalization

The Changing World! Three axes of change: * Technology * Globalization * Democracy

51

New Environment: Science,Technology, Society

* Accelerated speed of change * Ubiquity of personal computer * Internet and wireless technologies * Overlapping manufacturing and service * Compressed and transformed “middleman” trade * Prominence of small and medium enterprises * Globalization based on localization * Competition and cooperation * Life time learning and continued education * Participative management

52

The old vertical computer industry, circa 1980

IBM DEC Spery Univac Wang sales and distribution application software operating systems computer chips The transformation of the computer industry FROM Only the paranoid Survive, by Andrew S. Grove, © 1996 by Andrew S. Grove Used by permission of Doubleday, a division of Random House, Inc. Source : Lee, Miller and Rowen, “The Silicon Valley Edge”, 2000

53

The new horizontal computer industry, circa 1995

sales and distribution application software operating systems computer chips The transformation of the computer industry FROM Only the paranoid Survive, by Andrew S. Grove, © 1996 by Andrew S. Grove Used by permission of Doubleday, a division of Random House, Inc. Source : Lee, Miller and Rowen, “The Silicon Valley Edge”, 2000

54

Concluding Remarks Establish a national innovation system with clear goals and responsibility for the players Nurture the roots of hi-tech industry Strengthen national institute as linkage Improve effectiveness of national institute by project selection, project management, and technology diffusion Enable SMEs to take lead in innovation and technology entrepreneurship Re-educate people for creativity & innovation

55

Thank You! occlin@ust.hk occlin@tsing-tech.com.hk

Similar presentations

Grants Chapter 6.>")