Download presentation

Presentation is loading. Please wait.

1

Chapter 12 Principles of Bond Valuations and Investments Copyright © 2008 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

2

Objectives 1. Describe how the valuation of a bond is based on present value techniques. 2. Explain the differences among various concepts of yield such as yield to maturity, yield to call, and anticipated realized yield. 12-2

3

Objectives continued 3. Describe the techniques for anticipating changes in interest rates. 4. Develop an investment strategy for investing in bonds. 5. Describe how bond swaps may be used to increase after-tax returns. 12-3

4

Principles of Bond Valuation and Investment Fundamentals of the Bond Valuation Process Fundamentals of the Bond Valuation Process Rates of Return Rates of Return The Movement of Interest Rates The Movement of Interest Rates Investment Strategy: Interest Rate Considerations Investment Strategy: Interest Rate Considerations Bond Swaps Bond Swaps 12-4

5

Fundamentals of the Bond Valuation Process The price of a bond represents the present value of future interest payments plus the present value of the par value of the bond at maturity 12-5

6

Fundamentals of the Bond Valuation Process V =Market value or price of the bond n =Number of periods t =Each period C t =Coupon or interest payment for each period, t P n =Par or maturity value i =Interest rate in the market 12-6

7

Fundamentals of the Bond Valuation Process Assume a bond pays 10% interest or $100 for 20 years and has a par or maturity value of $1,000. Assume a bond pays 10% interest or $100 for 20 years and has a par or maturity value of $1,000. The interest rate in the marketplace is assumed to be 12%. The interest rate in the marketplace is assumed to be 12%. The present value of the bond, using annual compounding, is: The present value of the bond, using annual compounding, is: 12-7

8

Fundamentals of the Bond Valuation Process Assume a bond pays 10% interest or $100 for 20 years and has a par or maturity value of $1,000. Assume a bond pays 10% interest or $100 for 20 years and has a par or maturity value of $1,000. The interest rate in the marketplace is assumed to be 12%. The interest rate in the marketplace is assumed to be 12%. The present value of the bond, using annual compounding, is: The present value of the bond, using annual compounding, is: 12-8

9

Present Value of an Annuity of $1 (coupon payments) 12-9

12-9")

10

Present Value of an Single Amount of $1 (par or maturity value) 12-10

12-10")

11

Calculating Bond Prices U sing Tables Present Value of Coupon Payments (C t ) Present value of Maturity Value (P n ) (from Table 12-1 or Appendix D) (from Table 12-2 or Appendix C) n = 20, i = 12 % n = 20, i = 12% $100 x 7.469 = $746.90 $1,000 x 0.104 = $104.00 Present value of coupon payments = $746.90 Present value of maturity value = $104.00 Value of bond = $850.90 12-11

Present value of Maturity Value (P n ) (from Table 12-1 or Appendix D) (from Table 12-2 or Appendix C) n = 20, i = 12 % n = 20, i = 12% $100 x = $ $1,000 x = $ Present value of coupon payments = $ Present value of maturity value = $ Value of bond = $")

12

Calculating Bond Prices Using Excel Please click on the Excel icon 12-12

13

Other Methods of Calculating Bond Prices Using financial calculator Using financial calculator Using the Internet (Online bond calculations) Using the Internet (Online bond calculations) 12-13

Using the Internet (Online bond calculations) 12-13")

14

Fundamentals of the Bond Valuation Process Assume a bond pays 10% interest (5% semiannually, or $50 every six months, for 20 years and has a par or maturity value of $1,000. Assume a bond pays 10% interest (5% semiannually, or $50 every six months, for 20 years and has a par or maturity value of $1,000. The interest rate in the marketplace is assumed to be 12%. The interest rate in the marketplace is assumed to be 12%. The present value of the bond, using semiannual compounding, is: The present value of the bond, using semiannual compounding, is: 12-14

15

Fundamentals of the Bond Valuation Process Assume a bond pays 10% interest (5% semiannually, or $50 every six months, for 20 years and has a par or maturity value of $1,000. Assume a bond pays 10% interest (5% semiannually, or $50 every six months, for 20 years and has a par or maturity value of $1,000. The interest rate in the marketplace is assumed to be 12%. The interest rate in the marketplace is assumed to be 12%. The present value of the bond, using semiannual compounding, is: The present value of the bond, using semiannual compounding, is: 12-15

16

Excerpts from Bond Value Table 12-16

17

Rates of Return Current Yield Current Yield Yield to Maturity Yield to Maturity Yield to Call Yield to Call Anticipated Realized Yield Anticipated Realized Yield Reinvestment Assumption Reinvestment Assumption 12-17

18

Current Yield Annual interest payment divided by price of bond Annual interest payment divided by price of bond Example: Example: 10% coupon rate $1,000 par value bond selling at $95010% coupon rate $1,000 par value bond selling at $950 Ignores capital gains or losses Ignores capital gains or losses 12-18

19

Yield to maturity (YTM) Measure of return that considers Measure of return that considers Annual interest rate receivedAnnual interest rate received Difference between current bond price and maturity valueDifference between current bond price and maturity value Number of years to maturityNumber of years to maturity The interest rate at which you can discount the The interest rate at which you can discount the Future coupon payments andFuture coupon payments and Maturity valueMaturity value To arrive at quoted price of the bondTo arrive at quoted price of the bond Assumption: all coupons are reinvested at the same (YTM) rate. Assumption: all coupons are reinvested at the same (YTM) rate. 12-19

rate")

20

Yield to Maturity Example Assume the market price of the bond is $850.90, coupon or interest payment is $100, maturity value is $1,000 and number of periods is 20. Assume the market price of the bond is $850.90, coupon or interest payment is $100, maturity value is $1,000 and number of periods is 20. What interest rate will force the future cash inflows to equal $850.90? What interest rate will force the future cash inflows to equal $850.90? 12-20

21

The Formula for Approximate Yield to Maturity 12-21

22

Yield to Call To the extent a debt instrument may be called in before maturity, a separate calculation for yield to call may be necessary To the extent a debt instrument may be called in before maturity, a separate calculation for yield to call may be necessary Yield to call value is determined by: Yield to call value is determined by: the coupon rate,the coupon rate, the length of time to the call date,the length of time to the call date, the call price, andthe call price, and the market price.the market price. 12-22

23

Yield to Call Example 20-year bond was initially issued at 11.5% interest rate, and was callable at $1,090 five years after issue 20-year bond was initially issued at 11.5% interest rate, and was callable at $1,090 five years after issue Two years later, the yield to maturity on the bond is 9.48%, and the bond is selling for $1,180 Two years later, the yield to maturity on the bond is 9.48%, and the bond is selling for $1,180 An investor who buys the bond two years after issue can have his bond called back after three more years at $1,090 An investor who buys the bond two years after issue can have his bond called back after three more years at $1,090 To compute yield to call, determine the approximate interest rate that will equate a $1,180 investment today with $115 (11.5%) per year for the next three years plus a payoff or call price value of $1,090 at the end of three years. To compute yield to call, determine the approximate interest rate that will equate a $1,180 investment today with $115 (11.5%) per year for the next three years plus a payoff or call price value of $1,090 at the end of three years. 12-23

per year for the next three years plus a payoff or call price value of $1,090 at the end of three years")

24

Yield to Call Example continued Yield to call = 7.43% Yield to call = 7.43% 205 basis points less than yield to maturity205 basis points less than yield to maturity If market price is equal to or greater than call price, investor should do a separate calculation for yield to call If market price is equal to or greater than call price, investor should do a separate calculation for yield to call 12-24

25

Click on the Bonds icon Yield to Call Calculation - An Alternative Method Click on the Bonds icon Y = yield to maturity expressed in % R = coupon rate (or i) P = price of the bond. M = the number of years to Call date. The relation is: 12-25

26

Anticipated Realized Yield Return over the expected holding period Return over the expected holding period 12-26

27

The Formula for Approximate Anticipated Realized Yield = == = = Coupon payment = Realized price V = Market price Y r = Anticipated realized yield C t = Coupon payment C t = Coupon payment P r = Realized price P r = Realized price V = Market price V = Market price n r = Number of periods to realization n r = Number of periods to realization 12-27

28

Reinvestment Assumption Yield to Maturity Yield to Maturity Yield to Call Yield to Call Anticipated Realized Yield Anticipated Realized Yield Assume that the determined rate also represents an appropriate rate for reinvestment of funds. 12-28

29

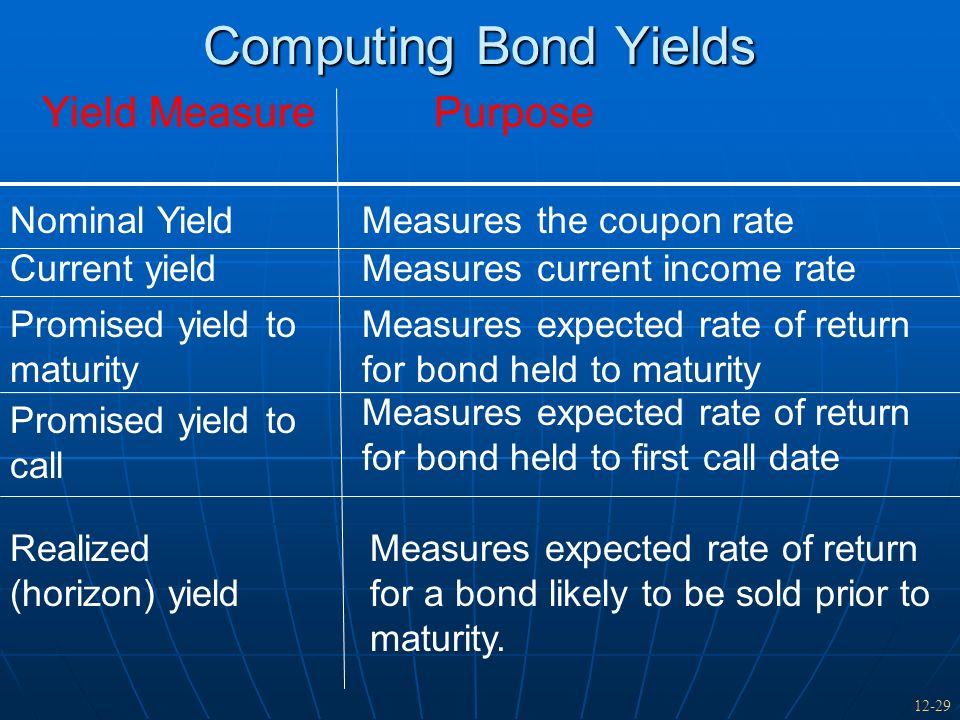

Computing Bond Yields Yield Measure Purpose Nominal YieldMeasures the coupon rate Current yieldMeasures current income rate Promised yield to maturity Measures expected rate of return for bond held to maturity Promised yield to call Measures expected rate of return for bond held to first call date Realized (horizon) yield Measures expected rate of return for a bond likely to be sold prior to maturity. 12-29

30

The Movement of Interest Rates Investors wishing to make substantial profit in bond market must try to anticipate direction of interest rates Investors wishing to make substantial profit in bond market must try to anticipate direction of interest rates Short-term rates may not move in the same direction as long-term rates Short-term rates may not move in the same direction as long-term rates Interest rates — coincident indicator Interest rates — coincident indicator 12-30

31

Factors Influencing Interest Rates Inflationary expectations Inflationary expectations Demand for funds by: Demand for funds by: IndividualsIndividuals BusinessesBusinesses GovernmentGovernment Desire for savings Desire for savings Federal Reserve policy Federal Reserve policy 12-31

32

Term Structure of Interest Rates Depicts the relationship between maturity and interest rates Depicts the relationship between maturity and interest rates Sometimes called the yield curve Sometimes called the yield curve 12-32

33

Maturity Yield c Maturity Yield a Maturity b Yield d Normal Figure 12-1 Term Structure of Interest Rates Inverted Humped Flat 12-33

34

Investment Strategy: Interest- Rate Considerations Bond-Pricing Rules Bond-Pricing Rules Example of Interest-Rate Change Example of Interest-Rate Change Deep Discount verses Par Bonds Deep Discount verses Par Bonds Yield Spread Considerations Yield Spread Considerations 12-34

35

Expectations Hypothesis Any long-term rate is an average of the expectations of future short-term rates over the applicable time horizon Any long-term rate is an average of the expectations of future short-term rates over the applicable time horizon 12-35

36

Liquidity Preference Theory The shape of the term structure curve tends to be upward sloping more than any other pattern. The shape of the term structure curve tends to be upward sloping more than any other pattern. Reflects recognition that long maturity obligations are subject to greater price-change movements when interest rates change Reflects recognition that long maturity obligations are subject to greater price-change movements when interest rates change Investors demand higher return for holding longer-term maturitiesInvestors demand higher return for holding longer-term maturities 12-36

37

Market Segmentation Theory Banks prefer short-term liquid securities Banks prefer short-term liquid securities Life insurance companies prefer long-term bonds Life insurance companies prefer long-term bonds These two institutions often put pressure on short-term and long- term rates These two institutions often put pressure on short-term and long- term rates 12-37

38

Relative Volatility of Short-Term and Long-Term Interest Rates 12-38

39

Investment Strategy: Interest Rate Considerations When investor believes interest rates will fall When investor believes interest rates will fall Buy long-terms bonds to maximize price movement with rate changeBuy long-terms bonds to maximize price movement with rate change 12-39

40

Change in Market Prices of Bonds for Shifts in Yields to Maturity 12 Percent Coupon Rate 6 Percent Coupon Rate 12-40

41

Bond Pricing Rules 1.Bond prices and interest rates are inversely related. 2.Prices of long-term bonds are more sensitive to change in YTM than short- term bonds. 3.Bond price sensitivity increases at a decreasing rate as maturity increases. 12-41

42

4.Bond prices are more sensitive to a decline in market YTM than to a rise in market YTM 5.Prices of low-coupon bonds are more sensitive to a change in YTM than high- coupon bonds. 6.Bond prices are more sensitive when YTM IS low than when YTM is high. Bond Pricing Rules continued 12-42

43

Deep Discount versus Par Bonds Significant discount from par value Significant discount from par value Coupon rate significantly less than the prevailing rates of fixed-income securities with similar risk profiles Coupon rate significantly less than the prevailing rates of fixed-income securities with similar risk profiles Generally trade at lower YTM than bonds selling at close to par Generally trade at lower YTM than bonds selling at close to par 12-43

44

Yield Spread Considerations Yield spread between different grades of bonds Yield spread between different grades of bonds At certain phases of business cycle, yield spread changes At certain phases of business cycle, yield spread changes Higher during recessionHigher during recession Lower during recoveryLower during recovery 12-44

45

Yield Spread Differentials on Long- Term Bonds 12-45

46

Bond Swaps Investor sells one bond and uses the proceeds to purchase another bond, often at the same price. Investor sells one bond and uses the proceeds to purchase another bond, often at the same price. Investors engage in bond swaps Investors engage in bond swaps to take a tax loss by selling one bond at a loss but then preserve their investment by simultaneously buying a similar bond.to take a tax loss by selling one bond at a loss but then preserve their investment by simultaneously buying a similar bond. to obtain a higher yield and return on their bond investments.to obtain a higher yield and return on their bond investments. : Click on the bonds icon for : An Investor's Guide to Bond Swapping An Investor's Guide to Bond Swapping 12-46

47

A detailed tutorial of the more complex concepts and calculations for trading bonds. Additional/advanced Bond PricingBond Pricing YieldYield Current Yield Current Yield Yield to Maturity Yield to Maturity Term Structure of Interest RatesTerm Structure of Interest Rates Duration and much moreDuration and much more Click on the investopedia 12-47

48

Yield to Maturity – HYPERLINK Additional/advanced What is my yield to maturity? What is my yield to maturity? Click on the Bonds icon 12-48

49

– A sample of the numerous useful bond websites – click on the icons New York Stock Exchange ------ New York Stock Exchange ------ Terms Used in bond Calculators -----------> 12-49

50

Click on the following hyperlinks 1. Treasury Direct 1. Treasury Direct 2. Public debt 2. Public debt 3. Online Financial 3. Online Financial Tutorial Tutorial 12-50

Similar presentations