Download presentation

Presentation is loading. Please wait.

1

ITS IMPROVED COMPETITIVENESS

INDONESIA ECONOMY AND ITS IMPROVED COMPETITIVENESS Mahendra Siregar Vice Minister of Trade Republic of Indonesia Business Forum Taipei, July 9, 2010 1 1

2

Asia Leads the World Economy Out of Recession

2

3

World Output Source: World Economic Outlook, IMF 3

4

Note : green column is estimated

Asia GDP Growth Indonesia GDP growth forecast remain increase for the next five years …. Note : green column is estimated

5

The “Factory East Asia”

Some are member of the 20 largest economies in the world East Asia (excluding Japan) exported US$3.5 trillion of goods, more than one-fifth of the World’s exports East Asia region itself is a market of approaching 2 billion people; Source: Gill, Kharas (2006)

exported US$3.5 trillion of goods, more than one-fifth of the World’s exports. East Asia region itself is a market of approaching 2 billion people; Source: Gill, Kharas (2006)")

6

Trade Integration in Asia Differs with Europe

Trade integration in Asia is unique; More than 70% of East Asia exports growth are manufacturing products in which machineries, electronics and transport equipment contribute more than 3/5; Source: staff calculation from UN-COMTRADE

7

The Asian noodle bowl* FTAs under negotiation

Jagdish Bhagwati invented “spaghetti bowl” to illustrate the complexity web and rules of free trade agreements which is proliferating Source: Haddad (2007)

")

8

Almost all have trade deficits with China

Source: ASEAN Secretariat

9

But increasing surplus with all other trade partners

Trade surplus (billion $) Source:UN-COMTRADE

Source:UN-COMTRADE.")

10

Updates on Indonesia Economy

10

11

Indonesia GDP Growth 2005 – 2010 Consumption and Government Expenditure Replace by Trade and Investment Expenditure 2005 2006 2007 2008 2009 Q-I Household Consumption 3,9 3,2 5,0 5,3 4,9 Government Consumption 8,1 9,6 10,4 15,7 -8,8 Gross Fixed Capital Formation 9,9 2,9 9,2 11,7 3,3 7,9 Export of Goods and services 8,6 8,0 9,5 -9,7 19,6 Reduced Imports of Goods and Services 12,35 7,6 8,9 10,0 -15,0 22,6 Gross Domestic Product 5,6 5,5 6,3 6,1 4,5 5,7 11 11

12

Indonesia has Diversified Exports Destination

Share of Exports by Country in 2000 Share of Exports by Country in 2009 2000 Japan 23% USA 14% Singapore 11% Korea 7% China 4% Others 41% 2009 (annualized) Japan 16% USA 9% Singapore Korea 7% China 10% Others 49% Source: Indonesia’s Central Board of Statistics Indonesia has succeeded in export market diversification. In 2000 the contribution of the top five countries of destination was amounting to 59%. The figure fell to 51% in 2009. Diversification of export destination countries has to be continued in order to reduce too much dependence on a small number of countries.

Japan. 16% USA. 9% Singapore. Korea. 7% China. 10% Others. 49% Source: Indonesia’s Central Board of Statistics. Indonesia has succeeded in export market diversification. In 2000 the contribution of the top five countries of destination was amounting to 59%. The figure fell to 51% in Diversification of export destination countries has to be continued in order to reduce too much dependence on a small number of countries.")

13

Indonesia Export Products Diversified

Source: BPS (processed by TREDA)

")

14

Imports reflect investment picking up

Source: BPS (processed by TREDA)

")

15

Effective Policy Responses in 2010

15

16

Fiscal Incentive to Support Real Sector 2010

Incentive on Taxation Income tax rate decrease 3% and 5% further and for listed companies in ISX Non-taxable primary agriculture product Abolishment part of Luxury Tax Income tax facilities for special industry and location. Energy Geothermal: Income Tax, VAT and Financing Oil and Gas: VAT exploration Bio-energy: Subsidy and VAT Govt. guarantee: Electricity MW (phase I and II) Infrastructure Funding for land acquisition and land capping Operational funding for Infrastructure Fund and Guarantee Fund Guarantee for State Water Company and clean water subsidy Housing Finance Trade and Industry NSW enactment, 24/7 services in major terminals, and import early warning Import duties -DTP special industry Import duties 0% for capital goods Revitalization fund for plantation and sugar refinery industry 5. Other Sector – Local Incentive for local government (Unqualified Opinion and Local budget submission) Bureaucracy Reformation Fund for 11 ministries/institution (laws, finance and national security) Capital injection for Indonesia Exim Bank and Indonesia Credit Insurance Company 16

Infrastructure. Funding for land acquisition and land capping. Operational funding for Infrastructure Fund and Guarantee Fund. Guarantee for State Water Company and clean water subsidy. Housing Finance. Trade and Industry. NSW enactment, 24/7 services in major terminals, and import early warning. Import duties -DTP special industry. Import duties 0% for capital goods. Revitalization fund for plantation and sugar refinery industry. 5. Other Sector – Local. Incentive for local government (Unqualified Opinion and Local budget submission) Bureaucracy Reformation Fund for 11 ministries/institution (laws, finance and national security) Capital injection for Indonesia Exim Bank and Indonesia Credit Insurance Company. 16.")

17

Fiscal Policy to Promote Economic Recovery

Fiscal policy aims to promote economic recovery by providing tax incentives to various sectors and businesses which further promotes private consumption and investment spending Fiscal Policy for 2010 to Promote Economic Recovery Reduce income tax rate for corporations from 28% to 25% Reduce income tax rate by 5% for listed companies with 40% public ownership Provide income tax facilities for businesses in specific industries or areas Free VAT for primary agriculture products Eliminate many luxury tax items Provide tax and custom incentive for special areas in accordance with law on tax and customs Eliminate non tax revenue for export and import documentation Incentives on General Taxation Energy Incentives Provide incentive for geothermal energy through income tax and VAT Provide tax incentive on imports (both income tax and VAT on imports) for the oil and gas exploration sector Provide incentive for green energy through VAT and subsidy Incentives for Industry Provide custom incentives for selected industries Provide custom incentives for imported capital goods and capex

for the oil and gas exploration sector. Provide incentive for green energy through VAT and subsidy. Incentives for Industry. Provide custom incentives for selected industries. Provide custom incentives for imported capital goods and capex.")

18

Fiscal Policy to Enhance Indonesia’s Competitiveness

The Indonesia government continues to support the development of infrastructure and enhance social welfare through effective fiscal policy and incentives for specific sectors Fiscal Policy for 2010 to Enhance Indonesia’s Competitiveness Infrastructure Development and Social Welfare Guarantee for 10,000 MW electricity program and IPP Additional funds for land clearing for toll road building Guarantee obligation for State Water Company; subsidy on interest for clean water, and interest credit for State Water Company Subsidy and VAT for people’s housing (low income housing) Credit for green fuel development Credit for farming and cow growers Subsidy for fertilizers, seeds and inventory Direct assistance for seeds at competitive price in order to revitalize plantation for cocoa and sugar industry Additional capital for Indonesia Exim Bank to finance export related activities, including for SMEs Provide incentives for high performance regions (e.g. performance on financial, economic and social welfare) Resolution for troubled asset at SOEs, and SMEs loans Assistance to Support Specific Sectors 18

Credit for green fuel development. Credit for farming and cow growers. Subsidy for fertilizers, seeds and inventory. Direct assistance for seeds at competitive price in order to revitalize plantation for cocoa and sugar industry. Additional capital for Indonesia Exim Bank to finance export related activities, including for SMEs. Provide incentives for high performance regions (e.g. performance on financial, economic and social welfare) Resolution for troubled asset at SOEs, and SMEs loans. Assistance to Support Specific Sectors. 18.")

19

Bilateral Trade Relations

20

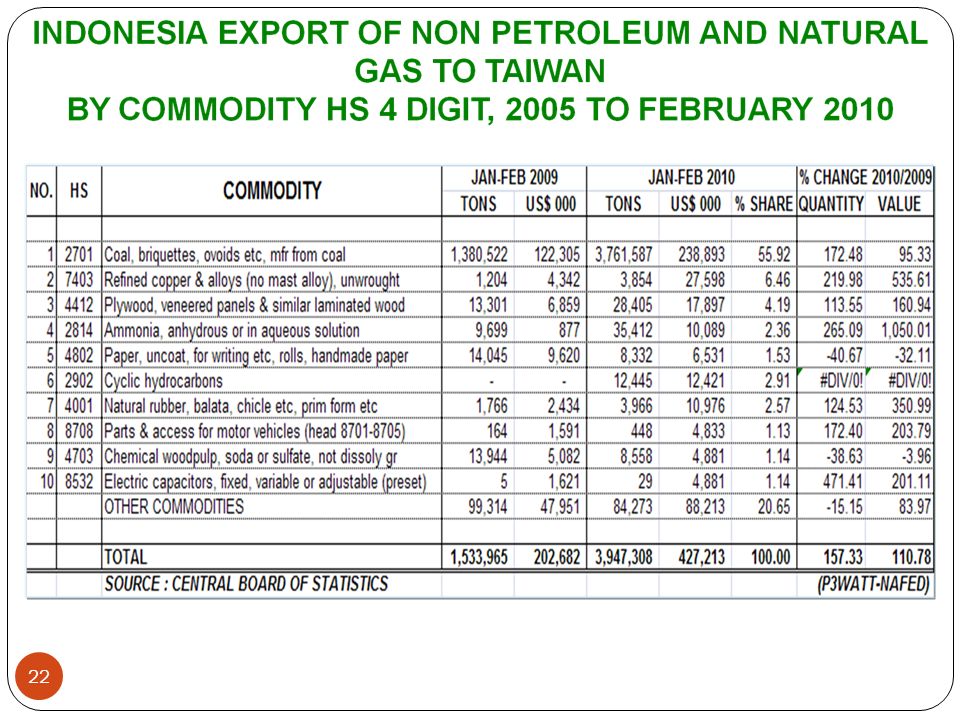

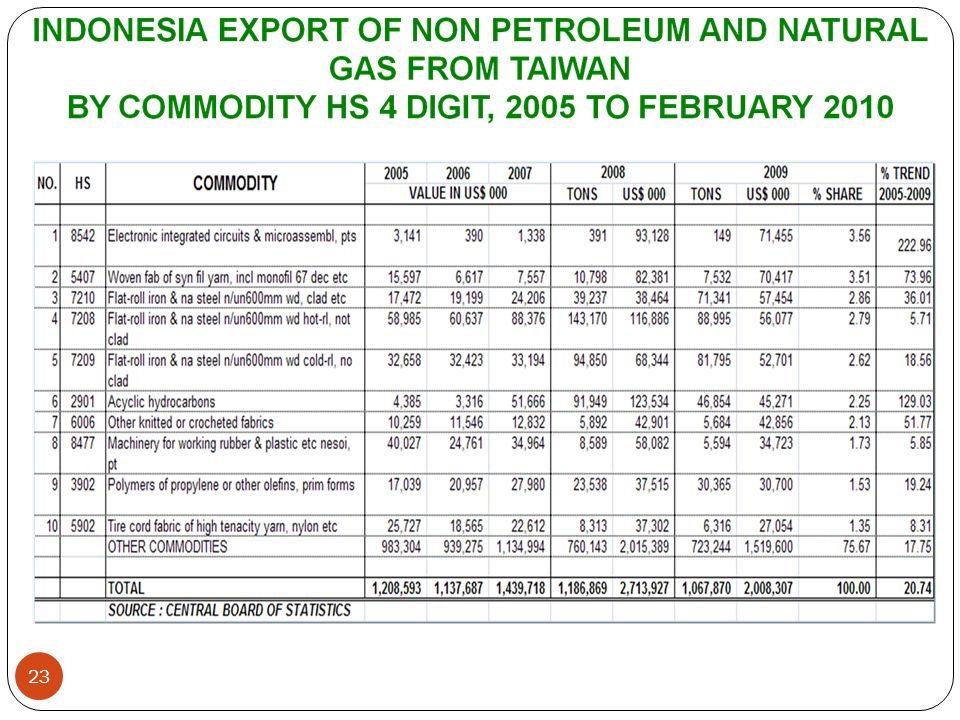

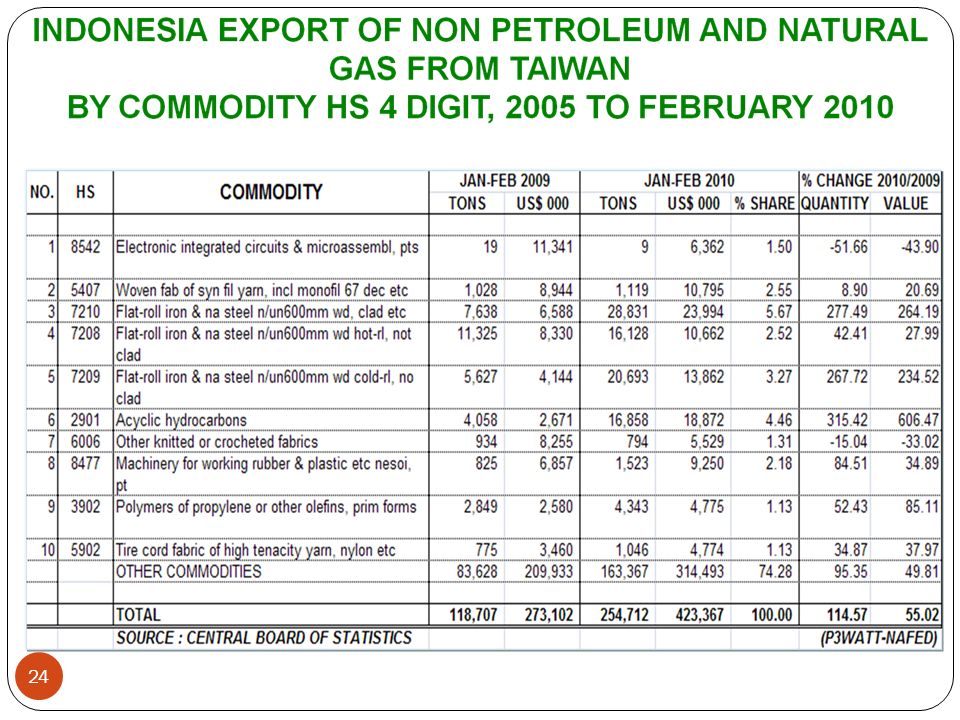

Balance of Trade Between Indonesia - Taiwan

26

Maintaining Indonesia’s Economic Reform Agenda

27

27

28

Improved Competitiveness

28

29

Improving Efficiency in Import Procedures

Improve efficiency in import procedures Create better tracking system of products with potential health and safety hazards Key points: Establish new registration system as part of National Single Window program, which will ultimately be part of ASEAN Single Window program – Registration requires 7 working days with completed requirements Technical verification and investigation to be conducted as part of creating tracking system Registered importers who have undertaken verification can go to the green lane

30

Opportunities for Trade and Investment

Indonesia and Taiwan can serve as production base: Indonesia is member of AFTA and other FTAs: ASEAN- China and ASEAN-Korea, ASEAN-Japan, ASEAN- India, ASEAN-ANZ; Come and join the 25th Indonesia Trade Expo (largest trade expo in Indonesia) 13 – 17 October 2010, Jakarta International Expo (National Agency for Export Development)

13 – 17 October 2010, Jakarta International Expo (National Agency for Export Development)")

31

Several Competitive Advantages for Investors:

Large domestic market Indonesia is a large and growing market (retail sales are growing fast) and part of Asian market Major expansions expected in infrastructure and resource based sectors, as well as increasing the competitiveness and value added of manufacturing industries Market-based macroeconomic policy Potential outsourcing partners Abundance of diversified natural resources Strategic location

and part of Asian market. Major expansions expected in infrastructure and resource based sectors, as well as increasing the competitiveness and value added of manufacturing industries. Market-based macroeconomic policy. Potential outsourcing partners. Abundance of diversified natural resources. Strategic location.")

32

Summary Government is committed to progressive reforms

Policies to support trade and investment Maintaining macroeconomic stability Strong and sustainable economic growth Enhance economic coordination and development cooperation with other main global economies

33

THANK YOU

Similar presentations

>")

10 March, 2014 In Seoul, Korea Ministry of Finance PRESENTATION AT THE PLENARY SESSION DEVELOPMENT COOPERATION.>")

>")