Download presentation

Presentation is loading. Please wait.

1

CORPORATE FINANCE VI ESCP-EAP - European Executive MBA

14-15 Dec. 2005, London Weighted Average Cost of Capital (WACC) Cost of equity, cost of debt Capital structure I. Ertürk Senior Fellow in Banking

Cost of equity, cost of debt. Capital structure. I. Ertürk. Senior Fellow in Banking.")

3

After Tax WACC Tax Adjusted Formula

4

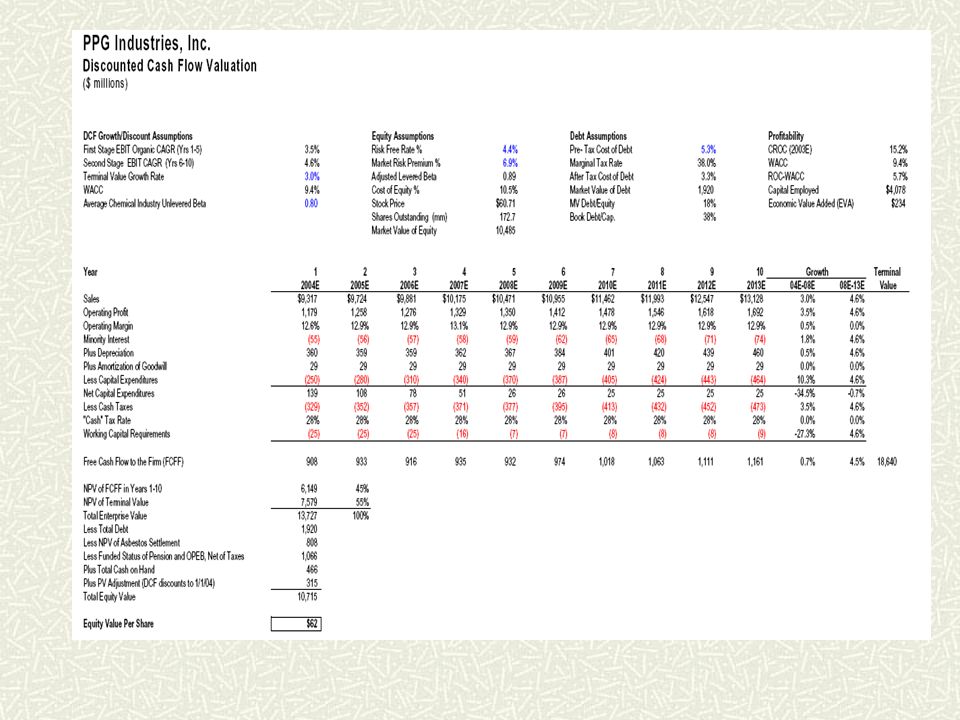

After Tax WACC Example - Sangria Corporation

The firm has a marginal tax rate of 35%. The cost of equity is 14.6% and the pretax cost of debt is 8%. Given the book and market value balance sheets, what is the tax adjusted WACC?

5

After Tax WACC Example - Sangria Corporation - continued

6

After Tax WACC Example - Sangria Corporation - continued

7

After Tax WACC Example - Sangria Corporation - continued

Debt ratio = (D/V) = 50/125 = .4 or 40% Equity ratio = (E/V) = 75/125 = .6 or 60%

= 50/125 = .4 or 40% Equity ratio = (E/V) = 75/125 = .6 or 60%")

8

After Tax WACC Example - Sangria Corporation - continued

9

After Tax WACC Preferred stock and other forms of financing must be included in the formula. Preferred Stock - Stock that takes priority over common stock in regards to dividends.

10

After Tax WACC Example - Sangria Corporation - continued

Calculate WACC given preferred stock is $25 mil of total equity and yields 10%.

11

What should be included with debt?

Long-term debt? Short-term debt? Cash (netted off?) Receivables? Deferred tax?

Receivables Deferred tax")

12

COST OF CAPITAL How are costs of financing determined?

Return on equity can be derived from market data. Cost of debt is set by the market given the specific rating of a firm’s debt. Preferred stock often has a preset dividend rate.

13

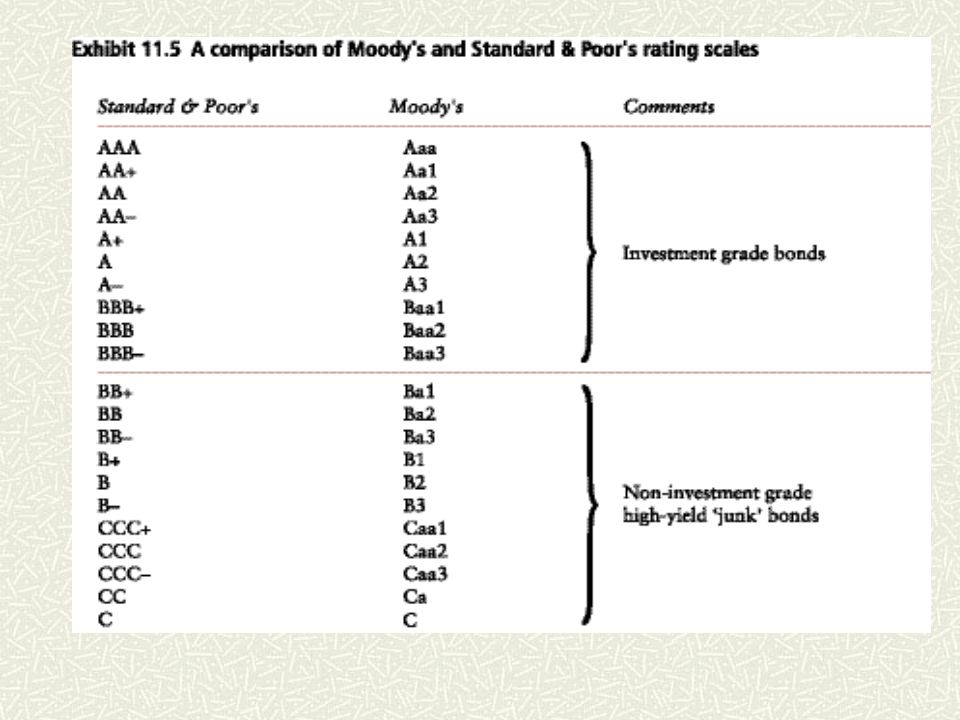

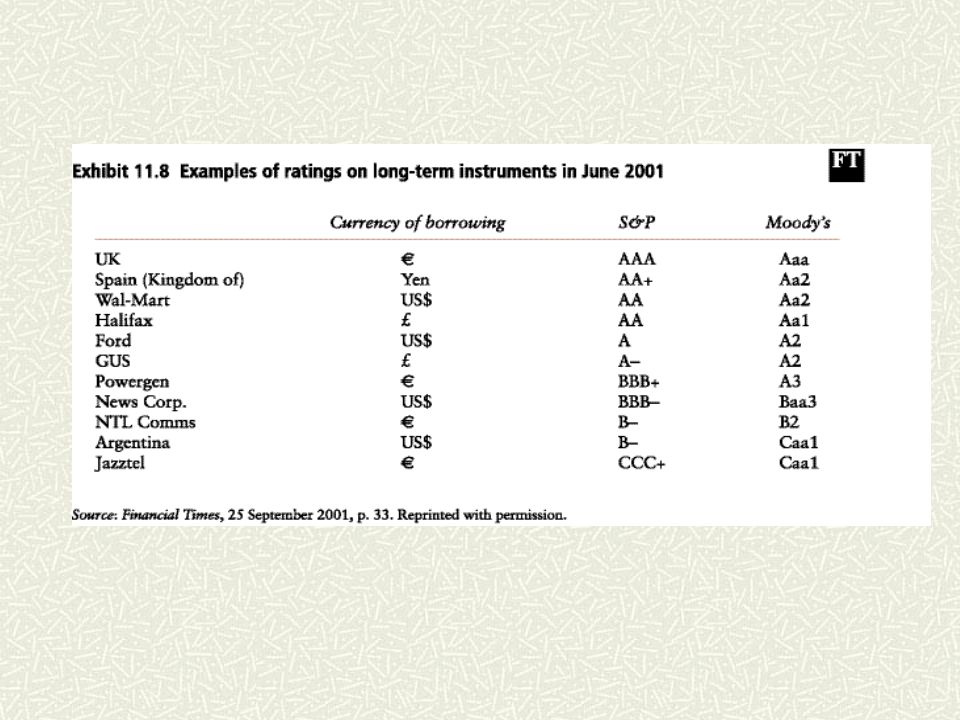

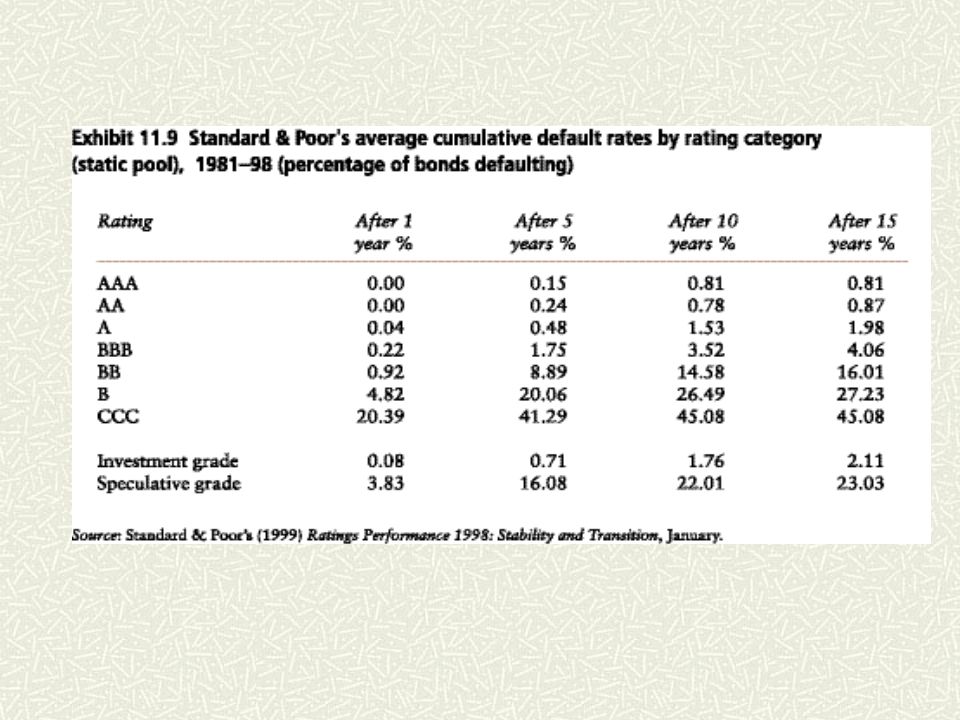

Corporate Debt Subordinate Debt - Debt that may be repaid in bankruptcy only after senior debt is repaid. Secured Debt - Debt that has first claim on specified collateral in the event of default. Investment Grade - Bonds rated Baa or above by Moody’s or BBB or above by S&P. Junk Bond - Bond with a rating below Baa or BBB. 17

14

Corporate Debt Debt has the unique feature of allowing the borrowers to walk away from their obligation to pay, in exchange for the assets of the company. “Default Risk” is the term used to describe the likelihood that a firm will walk away from its obligation, either voluntarily or involuntarily. “Bond Ratings”are issued on debt instruments to help investors assess the default risk of a firm. 15

15

BONDS INTEREST PAYING DEBT, PRINCIPAL OR FACE VALUE OR PAR VALUE REPAID AT END OF LOAN STATED INTEREST RATE CALLED COUPON DENOMINATIONS (OR PAR VALUES) OF CORPORATE BONDS TYPICALLY $1,000. GOVERNMENT BONDS USUALLY HAVE GREATER PAR VALUES. PRICE OFTEN STATED AS PERCENTAGE OF PAR VALUE BOND SELLING AT PAR IS SELLING “FLAT”- 100% OF PAR AT DISCOUNT IF PRICE < 100% OF PAR AT PREMIUM IF PRICE > 100% OF PAR MATURITY IS THE LIFE OF THE BOND BONDS PAY INTEREST SEMIANNUALLY OR ANNUALLY

OF CORPORATE BONDS TYPICALLY $1,000. GOVERNMENT BONDS USUALLY HAVE GREATER PAR VALUES. PRICE OFTEN STATED AS PERCENTAGE OF PAR VALUE. BOND SELLING AT PAR IS SELLING FLAT - 100% OF PAR. AT DISCOUNT IF PRICE < 100% OF PAR. AT PREMIUM IF PRICE > 100% OF PAR. MATURITY IS THE LIFE OF THE BOND. BONDS PAY INTEREST SEMIANNUALLY OR ANNUALLY.")

19

RENAULT

20

Corporate Debt Eurodollars - Dollars held on deposit in a bank outside the United States. Eurobond - Bond that is marketed internationally. Private Placement - Sale of securities to a limited number of investors without a public offering. Protective Covenants - Restriction on a firm to protect bondholders. Convertible Bond - Bond that the holder may exchange for a specified amount of another security. Convertibles are a combined security, consisting of both a bond and a call option. 18

21

6%, 5 year bonds CASH FLOWS AT END OF EACH YEAR

,060 SIMILAR BONDS RETURN 6.9% (YIELD TO MATURITY-YTM) BOND IS SELLING AT 96.3% (OF PAR VALUE)

BOND IS SELLING AT 96.3% (OF PAR VALUE)")

22

COUPONS ARE ANNUITY PV(BOND) =

PV (COUPON PAYMENTS) + PV (FINAL PAYMENT) PV(COUPON PAYMENTS) IS THE PV OF AN ANNUITY PV(BOND) = = €963

+ PV (FINAL PAYMENT) PV(COUPON PAYMENTS) IS THE PV OF AN ANNUITY. PV(BOND) = = €963.")

23

PRICE OF BOND AFTER BOND IS ISSUED, INTEREST RATES ON SIMILAR BONDS CHANGE BUT CASH FLOWS FROM BOND STAY SAME PRICE OF BOND WILL VARY BECAUSE THE PRICE IS THE PV OF THE REMAINING CASH FLOWS DISCOUNT RATES CHANGE WITH CHANGES IN YIELD TO MATURITY (YTM) OR YIELD ON SIMILAR BONDS

OR YIELD ON SIMILAR BONDS.")

24

YIELD TO MATURITY TURN THE QUESTION AROUND

ASK WHAT RETURN, r, DO INVESTORS EXPECT WHEN A 5-YEAR, 6% COUPON BOND IS PRICED AT 96.3? WE NEED TO FIND THE VALUE OF r THAT SATISFIES THE EQUATION r IS THE YIELD TO MATURITY (YTM) OR YIELD WE ASSUME A FLAT TERM STRUCTURE OF INTEREST RATES

OR YIELD. WE ASSUME A FLAT TERM STRUCTURE OF INTEREST RATES.")

25

BONDS MAKE SEMI-ANNUAL COUPON PAYMENTS

ANNUAL COUPON RATE IS QUOTED AS TWICE THE SEMIANNUAL COUPON RATE 6% COUPON BOND PAYS €30 TWICE A YEAR BOND YIELD IS QUOTED AS TWICE THE SEMIANNUAL BOND YIELD

26

ANNUAL COUPON C, ANNUAL YIELD TO MATURITY r, PRINCIPAL F

VALUE OF A BOND ANNUAL COUPON C, ANNUAL YIELD TO MATURITY r, PRINCIPAL F

27

INTEREST RATE RISK WHEN MARKET INTEREST RATES RISE, BOND PRICES FALL.

WHEN MARKET INTEREST RATES FALL, BOND PRICES RISE. BOND PRICE SENSITIVITY TO CHANGES IN INTEREST RATES GREATER 1. LONGER CURRENT MATURITY 2. LOWER THE COUPON RATE.

28

LONGER MATURITY BONDS ARE MORE SENSITIVE TO INTEREST RATES

MORE OF THE PRICE OF THE BOND IS DERIVED FROM CASH FLOWS (INTEREST AND PRINCIPAL) THAT OCCUR LATER IN TIME AND THEREFORE HAVE TO BE DISCOUNTED MORE MORE SENSITIVE TO CHANGES IN INTEREST RATES

THAT OCCUR LATER IN TIME. AND THEREFORE HAVE TO BE DISCOUNTED MORE. MORE SENSITIVE TO CHANGES IN INTEREST RATES.")

29

EXAMPLE: IS MORE SENSITIVE TO CHANGES IN r THAN

30

Capital Structure & Corporate Taxes

Financial Risk - Risk to shareholders resulting from the use of debt. Financial Leverage - Increase in the variability of shareholder returns that comes from the use of debt. Interest Tax Shield- Tax savings resulting from deductibility of interest payments.

31

Capital Structure Structure of Bond Yield Rates r Bond Yield D E

32

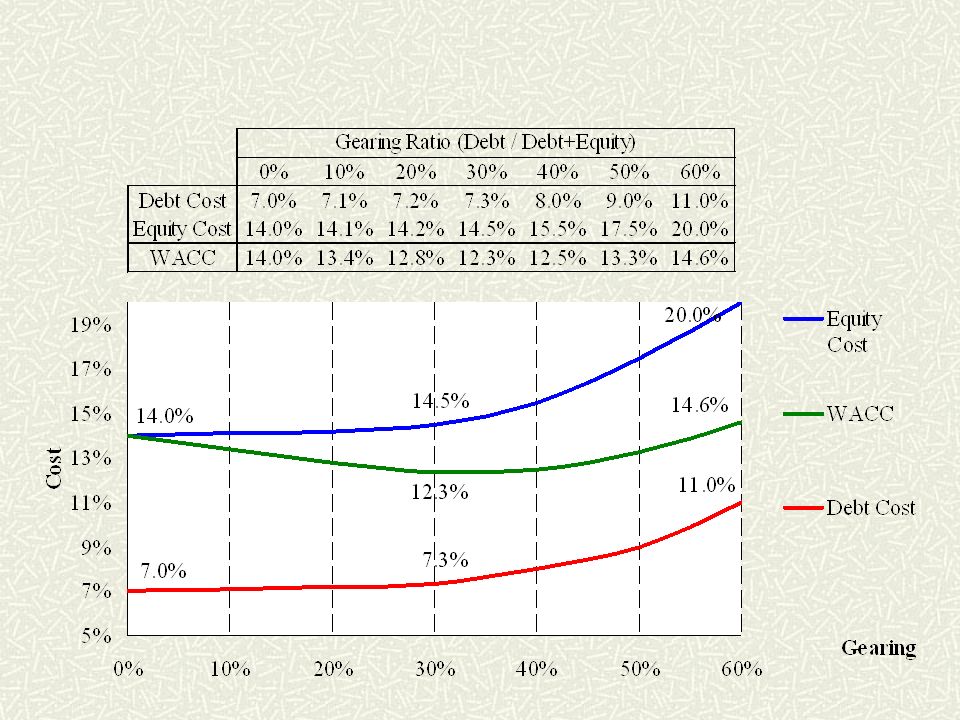

Weighted Average Cost of Capital without taxes (traditional view)

rE WACC rD D V Includes Bankruptcy Risk

34

Financial Distress Costs of Financial Distress - Costs arising from bankruptcy or distorted business decisions before bankruptcy. Market Value = Value if all Equity Financed + PV Tax Shield - PV Costs of Financial Distress

35

Financial Distress Market Value of The Firm Debt Maximum value of firm

Costs of financial distress Market Value of The Firm PV of interest tax shields Value of levered firm Value of unlevered firm Optimal amount of debt Debt

36

European Telecoms 2003

37

Patterns of Corporate Financing

38

Financial Choices Trade-off Theory - Theory that capital structure is based on a trade-off between tax savings and distress costs of debt. Pecking Order Theory - Theory stating that firms prefer to issue debt rather than equity if internal finance is insufficient.

39

Pecking Order Theory Consider the following story:

The announcement of a stock issue drives down the stock price because investors believe managers are more likely to issue when shares are overpriced. Therefore firms prefer internal finance since funds can be raised without sending adverse signals. If external finance is required, firms issue debt first and equity as a last resort. The most profitable firms borrow less not because they have lower target debt ratios but because they don't need external finance.

40

Pecking Order Theory Some Implications:

Internal equity may be better than external equity. Financial slack is valuable. If external capital is required, debt is better. (There is less room for difference in opinions about what debt is worth).

.")

41

Telus Cost of Capital

Similar presentations

FIN 200: Personal Finance Topic 19–Bonds Lawrence Schrenk, Instructor.>")

“The firm`s mix of securities(long.>")