Download presentation

Presentation is loading. Please wait.

1

Prospects for Building & Construction & Property BMI Forum 2010.01 Dr Johan Snyman Medium-Term Forecasting Associates STELLENBOSCH 24 March 2010

2

Framework Leading indicators Quantitative Qualitative Market sectors Residential Non-residential Construction works Property indicators Summary

7

Consumers are recovering from the global financial crisis …

8

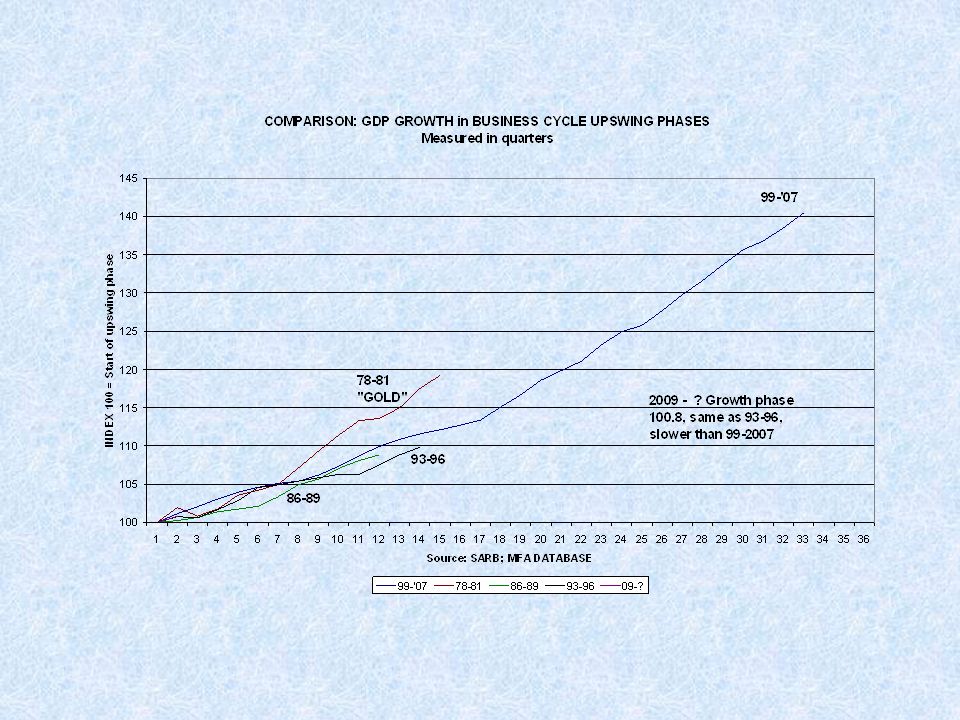

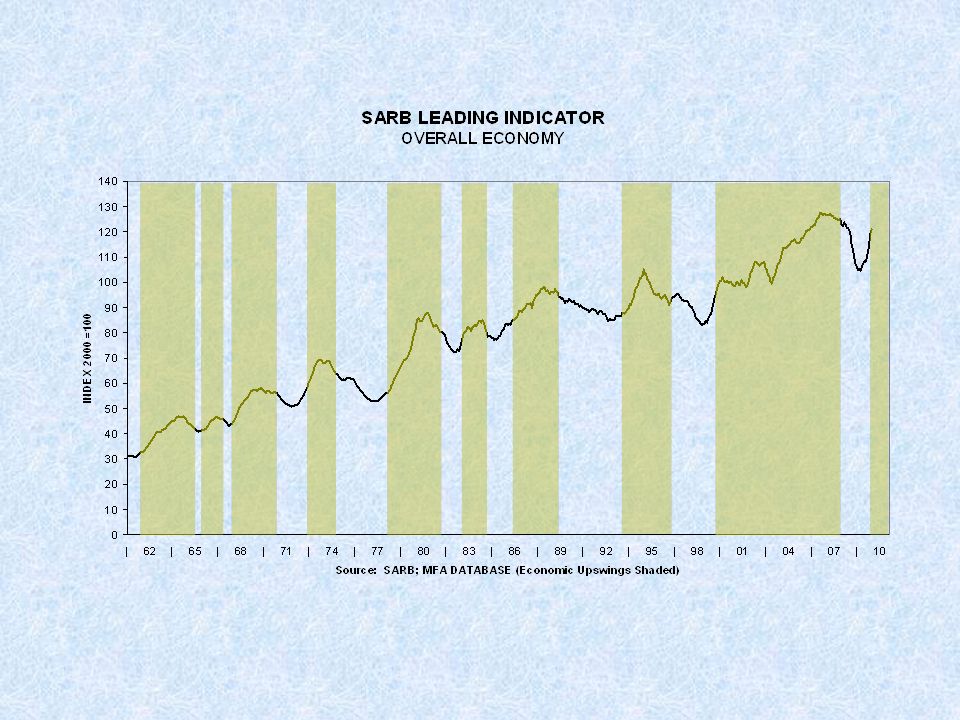

The MFA CLIBI is conforming to pattern, remember it leads the cycle …

9

The business mood of builders and architects has turned the corner, yet quantity surveyors are more pessimistic than before…

10

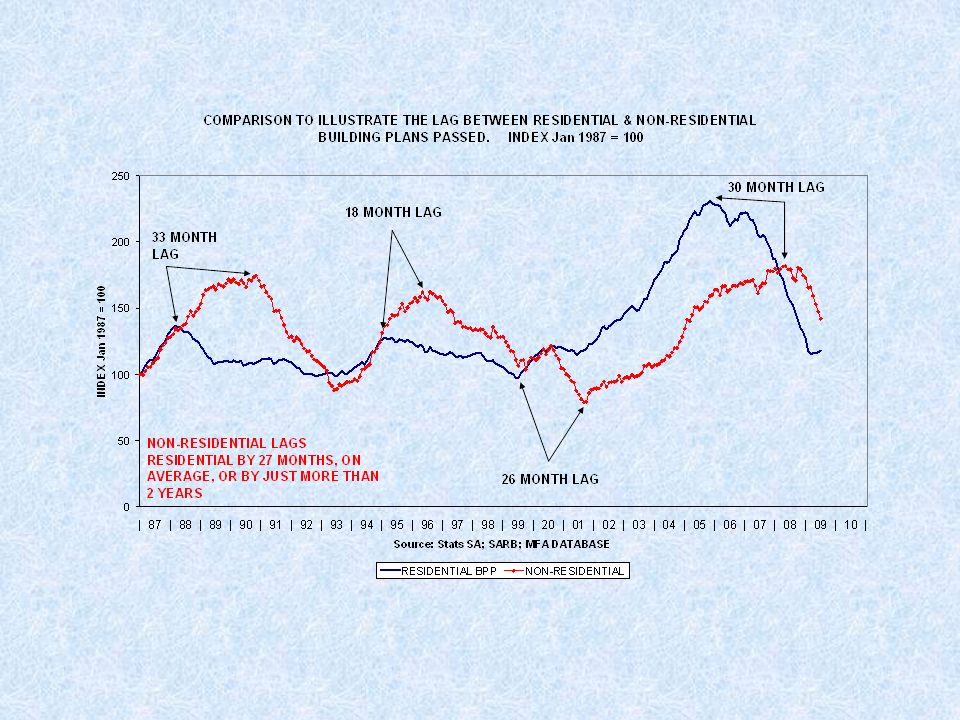

The business mood of non-residential builders lags that of residential builders … but both indicators are improving

11

Labour and materials bottlenecks are easing …

12

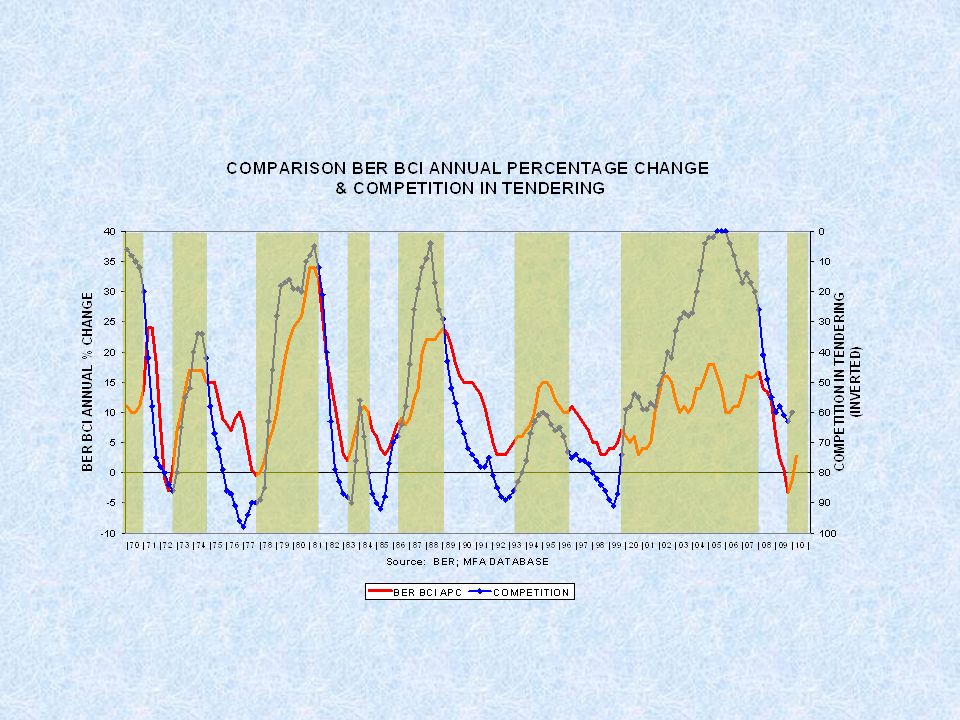

Competition in tendering is still quite keen …

13

The number of tenderers on the tender list is rising strongly, implying less work available … and this finding comports with keen competition …

14

Builders’ merchants view their stock levels as still too high, but less adequate than previously. They will probably start a restocking cycle during 2010 …

15

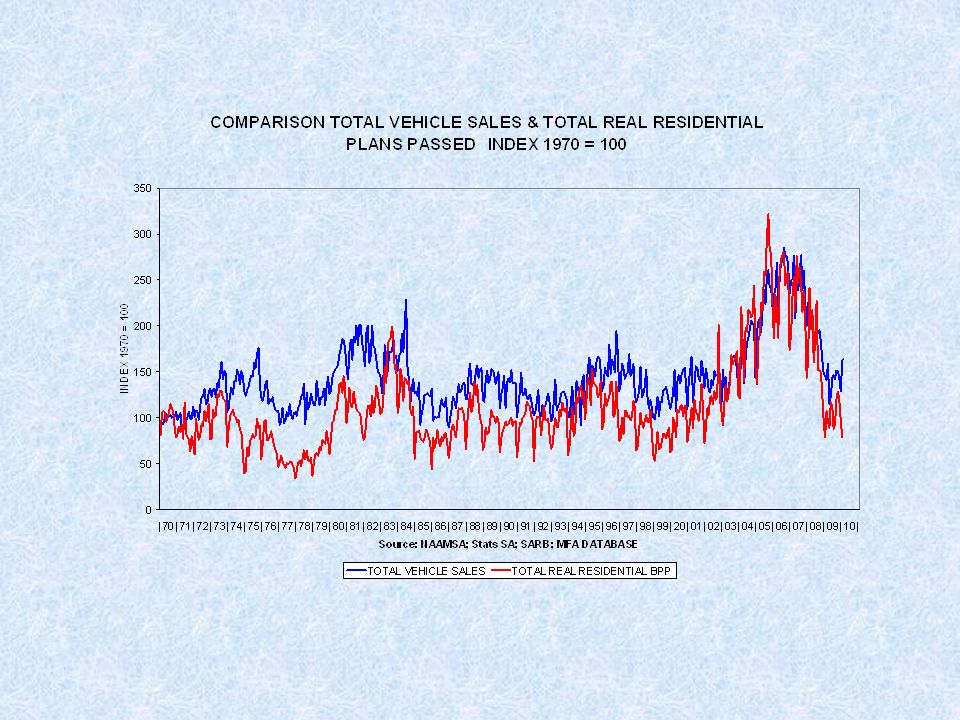

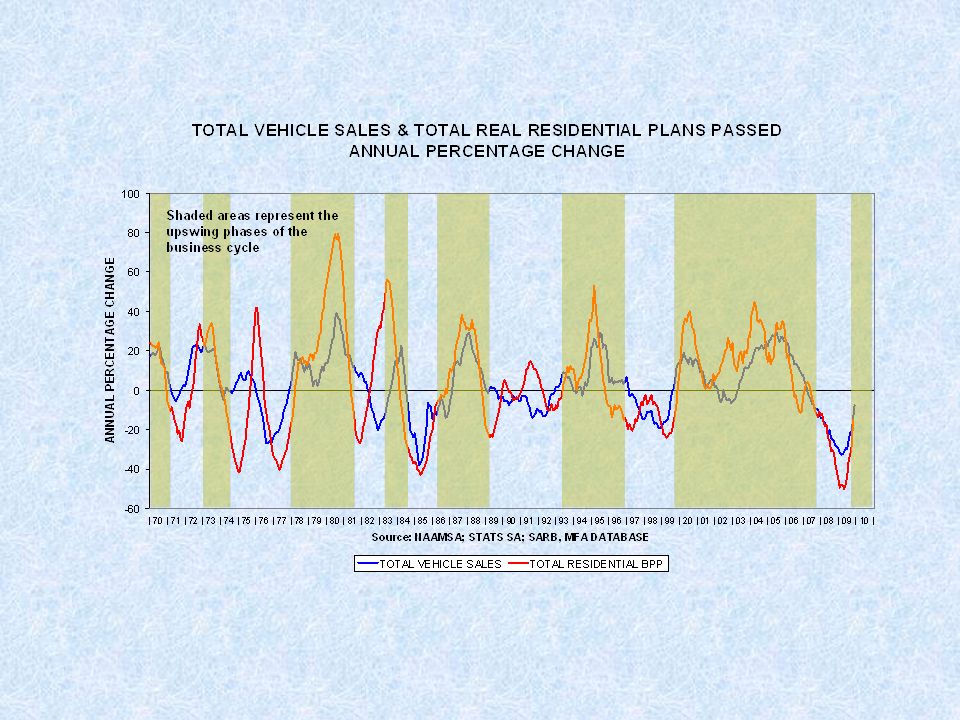

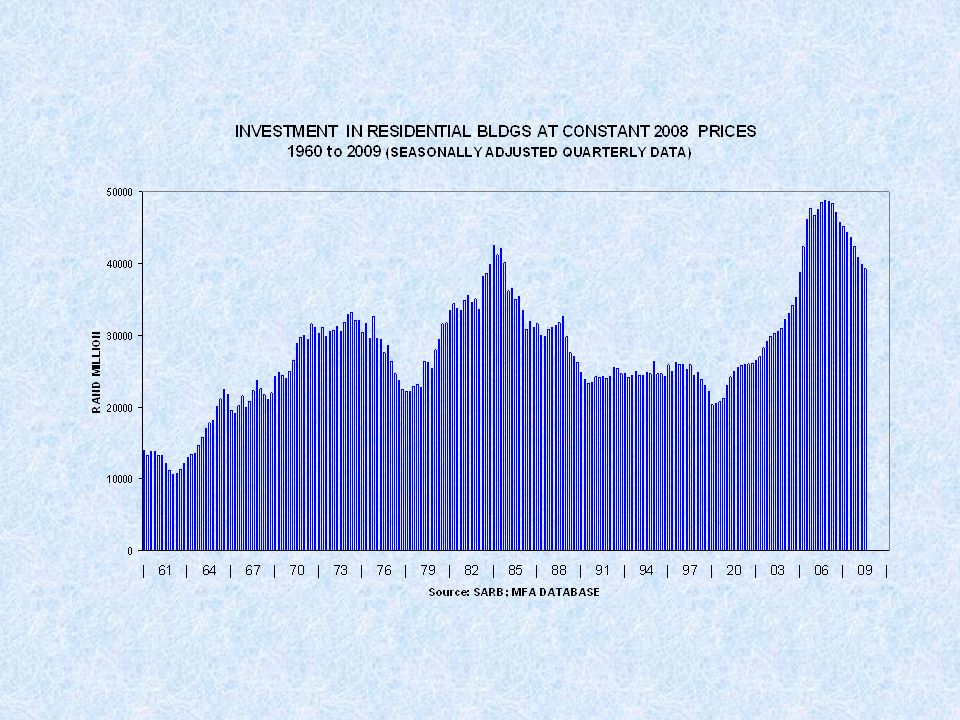

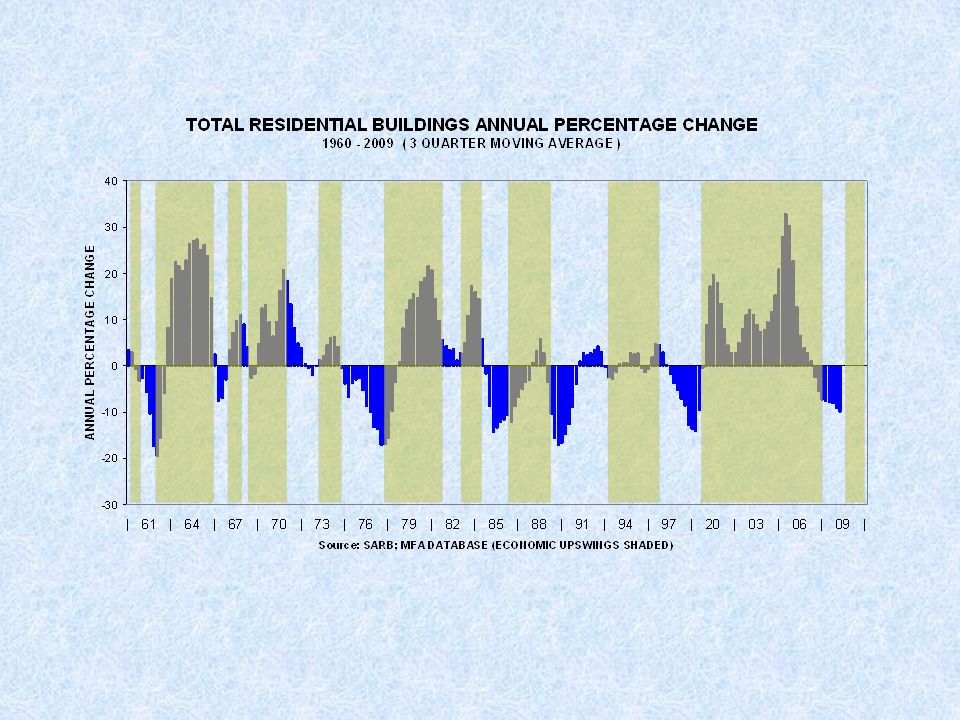

Two blows struck the private housing industry in 2007/08 … but it seems that it is responding belatedly to lower interest rates

19

Dwelling houses are still plumbing the depths …

20

Townhouses and flats are also plumbing the depths of the cycle

21

Still performing poorly …

22

There is a gradual downtrend in sizes of townhouses and flats

23

The building cost of townhouses and flats seems to have stabilised around R400 000 per unit

27

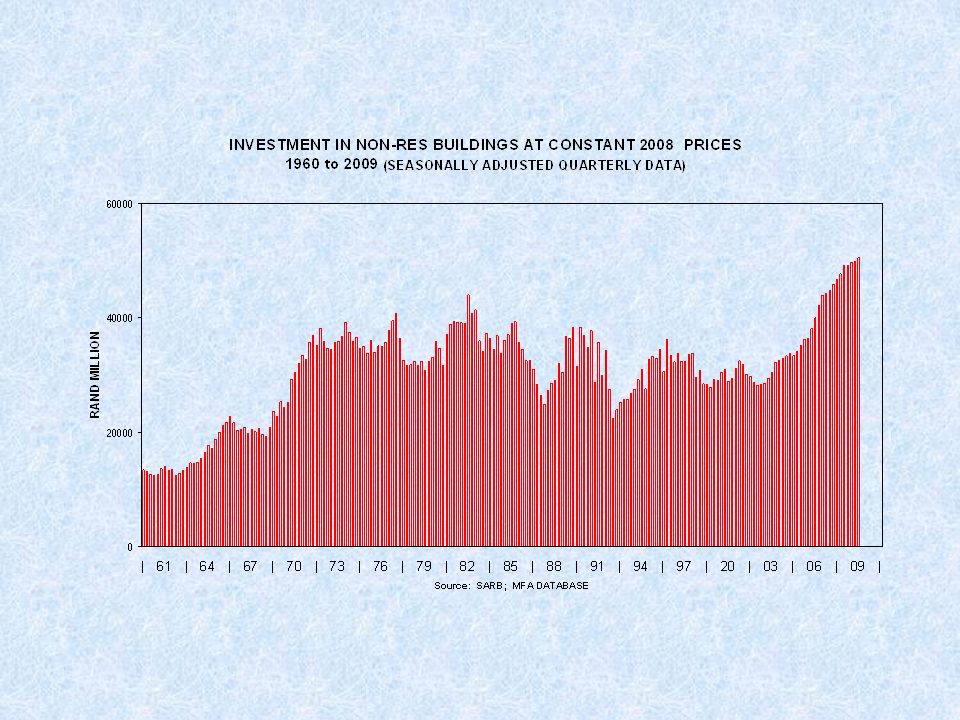

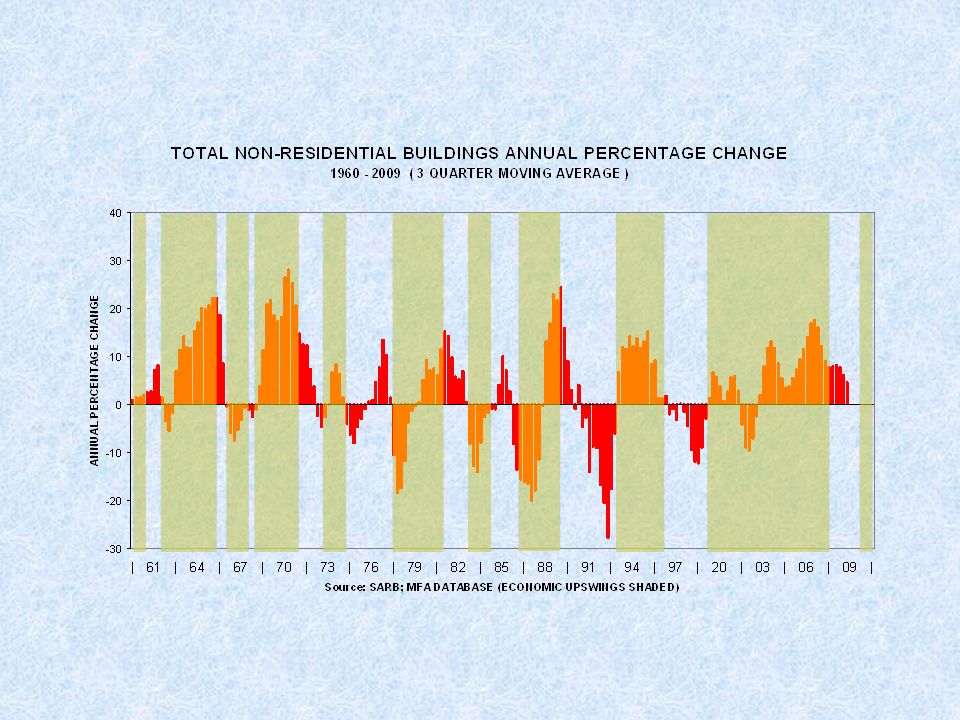

The demand for new office space is dropping to extremely low levels …

28

… because office vacancies are rising on a nationwide basis

29

Definite signs of over-building …

30

The downward trend is still in place …

31

… because industrial vacancies are still rising …

32

According to Rode, industrial vacancies have risen since 2008 on a nationwide basis

33

… and, consequently, industrial rental levels have dropped

34

According to Rode, there is a close correspondence between the under-utilization in manufacturing and industrial vacancies

35

Still dropping …

43

Data released by the National Treasury show that the trough in transfer duty was recorded during 2009

44

Transfer duty is improving in real terms from very low levels

45

When compared to a year ago, transfer duty is at a higher level, implying that the residential property cycle is reviving

49

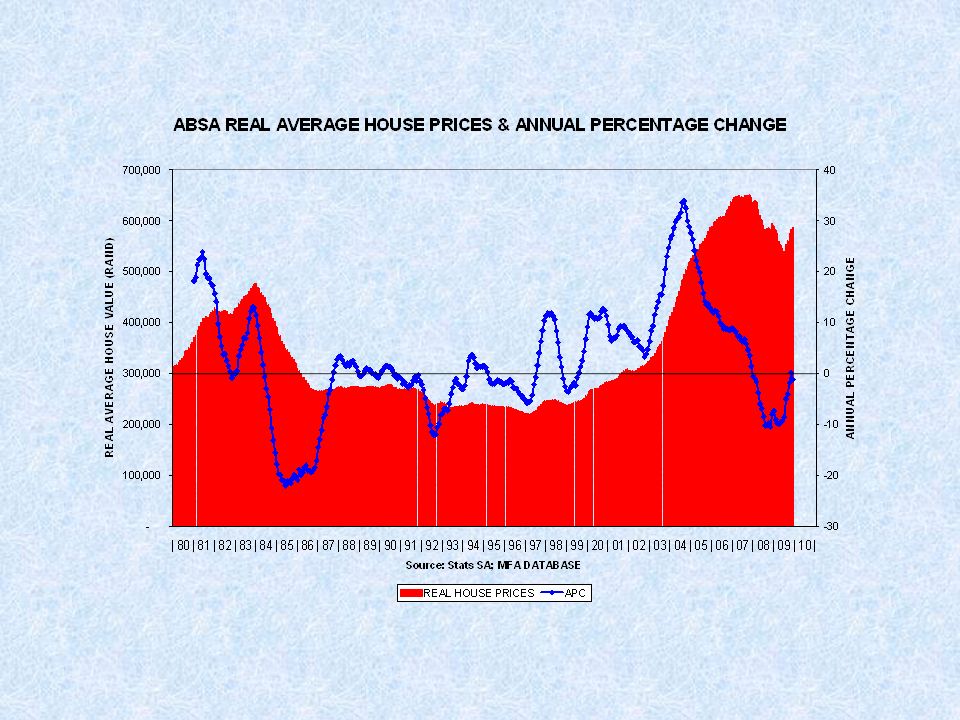

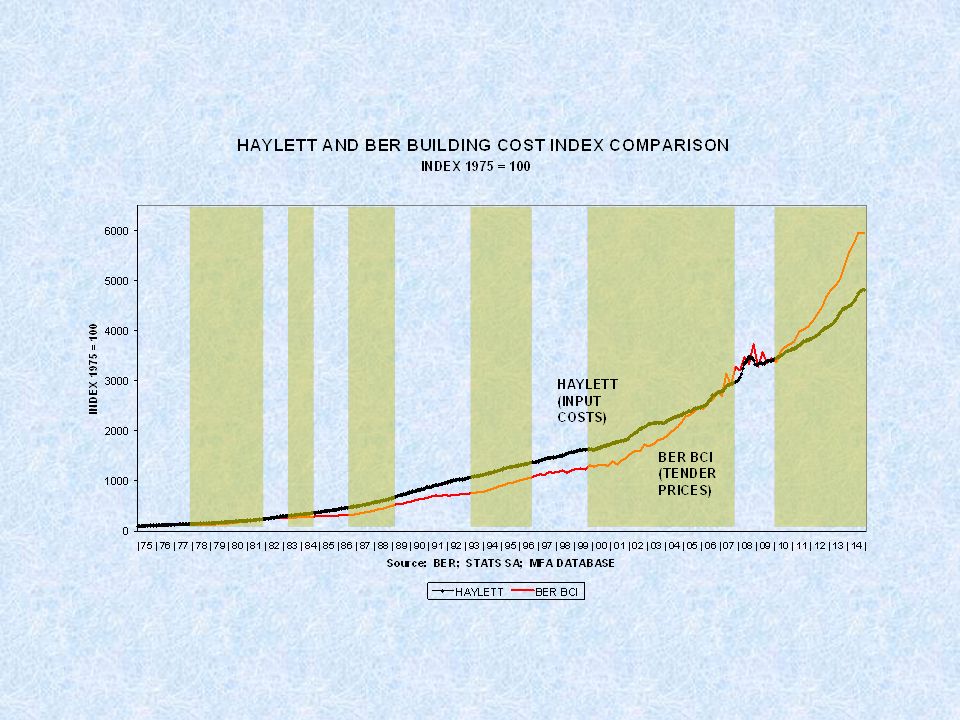

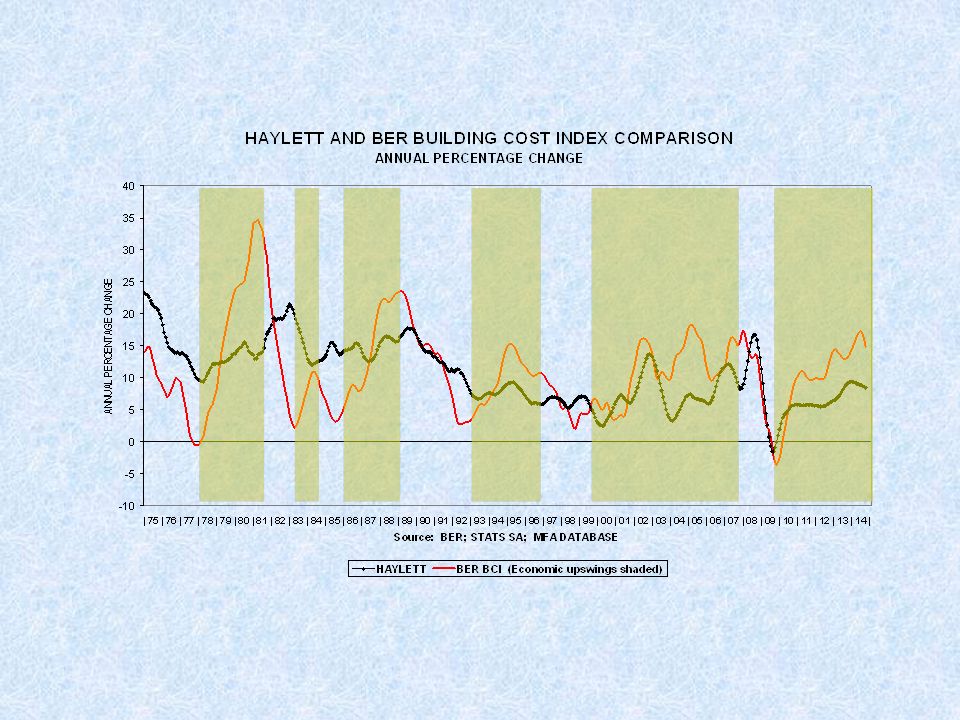

This graph shows that the movements in building costs and house prices are closely linked, and that both are influenced directly by business cycle fluctuations … with the shaded areas representing the upswing phases

50

Summary (annual percentage change) 200820092010 Investment: Res-8-93 Non-res84-9 C W3136-3 Building costs Haylett14.31.75.0 Tender prices14.4-0.85.2

Investment: Res-8-93 Non-res84-9 C W Building costs Haylett Tender prices")

51

Thank you for your attention … Johan Snyman mfa@iafrica.com

Similar presentations

Authority.>")